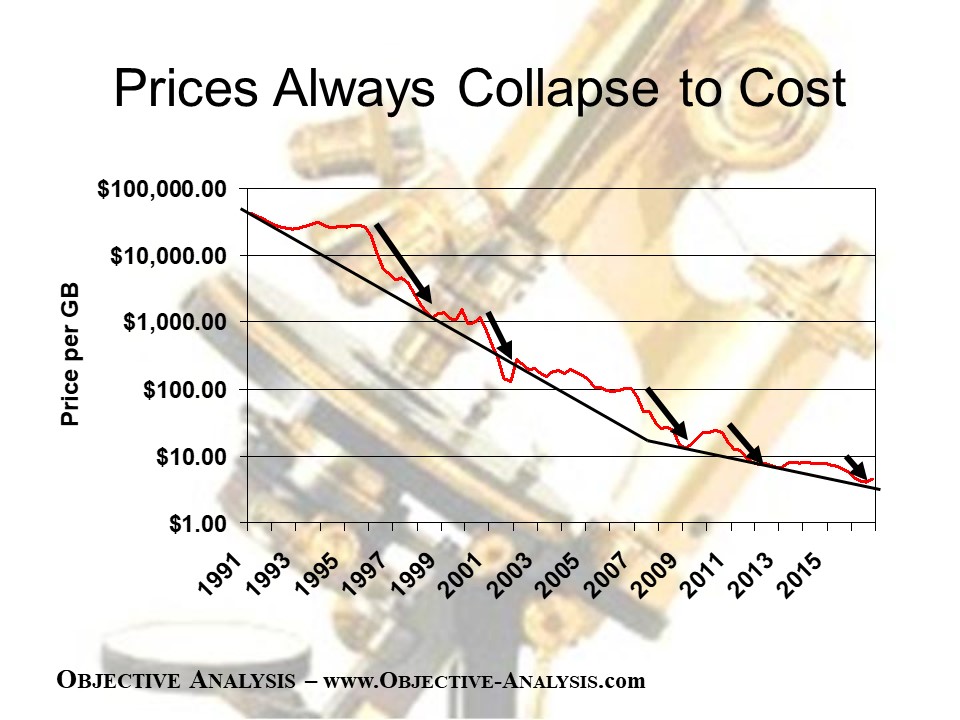

An earlier post outlined the general direction of the Objective Analysis 2019 forecast but didn’t provide any numbers. In this post I explain the 5%+ decrease in revenues that the market will experience and how and why various elements play into that number.

As new numbers are released, we have a better glimpse of where we are in the bad loan cycle, and the data is not reassuring. And we see that it is not only about risk with infrastructure or corporate loans in India, even if these are the most well-known credit risks. Housing loans are not immune from the economic malaise that remains in place. Non-bank financial company (NBFC) Can Fin Homes (CANF IN) shows exceptionally high quarterly bad loan growth in the latest period. Recalling our note on HDFC Bank, consumer loans more generally, may not be as robust as most believe. And there are others.

US sanctions against Venezuela’s central bank and PDVSA, announced on Monday (January 28), have sent refiners on the US Gulf Coast scrambling for replacement supplies of heavy crude. Though they do not cover the business of non-US entities with PDVSA, the move has put Venezuelan crude importers in China and India on notice.

For US refiners, the three main alternative suppliers of heavy, sour crude — Canada, Mexico and Saudi Arabia — are either constrained in their ability to step up supply or are deliberately reducing shipments.

Venezuela’s upstream oil sector has been limping for a long time now. But the sanctions against PDVSA may deal it a death blow. The crude market is keeping a wary eye on the situation but appears unwilling to price in the worst-case scenario for the time being, as it remains fixated on the global economic prospects and concerns over oil demand growth.

We look at the fallout of the latest move by Washington on the primary entities doing oil business with Venezuela: refiners in the US, China and India (the main markets for Venezuelan crude) and Russian giants Rosneft and Lukoil.

We also discuss the likelihood and impact of Venezuelan crude production grinding down from the current 1 million b/d to zero.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

An earlier post outlined the general direction of the Objective Analysis 2019 forecast but didn’t provide any numbers. In this post I explain the 5%+ decrease in revenues that the market will experience and how and why various elements play into that number.

This is a monthly version of our HK Connect Weekly note, in which I highlight Hong Kong-listed companies leading the southbound flow weekly. Over the past month, we have seen the flow turning from outflow to inflow. Our previous insights published in Jan can be found in the links below. In this insight, we will focus on the month flow to get a bigger picture vs the weekly flow.

Our January Coverage of Hong Kong Connect southbound flow

This share class monitor provides a snapshot of the premium/discounts for various share classifications around the region, and comprises four sets of data:

The average premium/discount for each set over a one-year period is graphed below.

Source: CapIQ

For a granular breakdown of each data set, PDFs are attached at the bottom of this insight.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

An earlier post outlined the general direction of the Objective Analysis 2019 forecast but didn’t provide any numbers. In this post I explain the 5%+ decrease in revenues that the market will experience and how and why various elements play into that number.

The Indonesian property sector has only had a few glittering moments in the sun over the past five years, since the boom times of 2012-2013. The sector continues to trade at near record discounts to NAV despite the back-drop of record-low mortgage rates, rising affordability and high levels of pent-up demand. In this series under Smartkarma Originals, CrossASEAN insight providers AngusMackintosh and Jessica Irene seek to determine whether or not we are close to the end of the rainbow and to a period of outperformance for the sector. Our end conclusions will be based on a series of company visits to the major listed property companies in Indonesia, conversations with local banks, property agents, and other relevant channel checks.

In this series of Insights we will discuss in depth:

The drivers to the property sector, including the economic drivers, with a more benign outlook on interest rates, overall supply and demand, correlations to mortgage rates, the currency impact, construction costs, regulation and tax law change over the years and the influx of foreign developers and potential buyers.

The profiles of the biggest players in each segment of the property market. We will also map out the details of each company’s location, accessibility, and longevity of their land bank.

How each development is interconnected and how it benefits from new infrastructure projects, such as the new toll roads or MRT, or LRT projects, and the rise of the T.O.D. (transport orientated development).

Each developer’s target segment, whether they are focused on landed township developments, high rise, mixed-use, or industrial developments, and how each segment fared during boom time (2012-2014) or bust (2015-2018).

How much of each developer’s revenues are coming from recurrent investment property sources such as the office, hotel, or retail properties, and which have the biggest proportion of speculative buyers versus end-users?

Last year saw a pick-up in sales activity for most developers but the question is can this be sustained going forward? With a more benign outlook on interest rates and a less hawkish tack from Bank Indonesia for 2019, the potential for positive regulatory changes to support the property sector, and a potential post-election tailwind from May onwards, there are good reasons to revisit this beaten up sector.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

An earlier post outlined the general direction of the Objective Analysis 2019 forecast but didn’t provide any numbers. In this post I explain the 5%+ decrease in revenues that the market will experience and how and why various elements play into that number.

Healthscope Ltd (HSO AU) has announced it has entered into an Implementation Deed with Brookfield, under which Brookfield seeks to acquire 100% of Healthscope by way of a scheme at A$2.50/share, and a simultaneous Off-market takeover Offer at $2.40/share.

The considerations under these proposals compares to the earlier indicative considerations of $2.585/share and $2.455/share respectively under the unsolicited conditional proposals announced back in November.

The $2.50/share under the scheme – which is priced at a 40% premium to the undisturbed price – includes an interim dividend of $.035/share. The scheme consideration represents an EV/EBITDA (Dec-18 end) of ~14.7x.

Both proposals are subject to limited conditions and neither are subject to due diligence and financing. The Off-market is subject to a 50.1% acceptance condition and the Scheme not being successful.

Brookfield’s proposals have unanimous HSO Board backing.

The Off-market takeover will remain open for at least four weeks after the date of the Scheme meeting, providing shareholders with opportunity to consider the Offer, depending on the outcome of the Scheme vote.

HSO also announced that the BGH-led consortium, which holds a ~20% stake, said it could improve the terms of its previous offer of $2.36/share, provided it was given access to Healthscope’s data room.

An explanatory booklet for Brookfield’s proposals is expected to be dispatched in April/May and the Scheme meeting to take place in May/June.

Currently trading tight to the Scheme consideration at $2.45/share.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

An earlier post outlined the general direction of the Objective Analysis 2019 forecast but didn’t provide any numbers. In this post I explain the 5%+ decrease in revenues that the market will experience and how and why various elements play into that number.

Korean stock market surged in January with KOSPI up 8% this past month. KOSPI was led by the market leaders including Samsung Electronics (005930 KS), SK Hynix Inc (000660 KS), and Hyundai Motor Co (005380 KS), whose share prices were up 19%, 22%, and 9%, respectively in January. There were several high-profile, M&A announcements including the potential sale of Nexon founder’s stake as well the consolidation of DSME with Hyundai Heavy Industries. The market also received strong additional boost from the dovish comments from the US Fed Chairman Jerome Powell.

The top 10 events impacting the Korean stock market, economy, & politics in January were as follows:

Below is a comprehensive summary of the Hyundai Heavy/DSME event that engulfed the Korean market yesterday. This is a multi step process. Details of most events will be determined after one month of holdback period.

I will provide a trade approach on each name in a follow-up post.

SK Telecom (017670 KS) reported disappointing 4Q18 earnings results. SK Telecom’s revenue of 4,351.7 billion won was 0.2% lower than consensus and its operating profit of 225 billion won was 23% lower than the consensus in 4Q18. Despite the disappointing 4Q18 results (especially due to lower operating income and lack of flow through of SK Hynix dividends to SKT), we remain positive on SK Telecom.

We believe that SK Telecom’s 10,000 won DPS in 2018 is a disappointment. However, we believe the stage has been set for higher DPS policy, linking SK Hynix’s dividends to SK Telecom and as mentioned in the conference call numerous times, this is likely to be announced in the AGM in March. In terms of amount, we believe 13,000 won to 15,000 won appears to be reasonable in 2019.

The company’s comment about its sales and profits improving starting in 2H 2019 is consistent with its previous statement in the third quarter conference call. However, the company’s statement about its revenue target of more than 1 trillion won growth YoY in 2019 is new and positive. In 2018, SK Telecom generated consolidated sales of 16.9 trillion won, down 3.7% YoY. If the company is able to generate revenue of 17.9 trillion won in 2019, this would represent a growth of 5.9% YoY. The current consensus estimate of the company’s sales is 17.47 trillion won in 2019. Thus, the company has basically guided the 2019 sales target by 2.5% higher than the current consensus estimate.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

An earlier post outlined the general direction of the Objective Analysis 2019 forecast but didn’t provide any numbers. In this post I explain the 5%+ decrease in revenues that the market will experience and how and why various elements play into that number.

Broad global indexes (MSCI ACWI, ACWI ex-U.S., and EAFE) are showing signs of bottoming due to positive short-term price inflections topside their respective downtrends. Additionally, cyclical Sectors Technology, Consumer Discretionary, and Manufacturing exhibit early signs of price and RS bottoms throughout Europe, Japan, and EM. In today’s report we highlight attractive and actionable opportunities within these cyclical Sectors, and provide a technical appraisal of major global indexes.

Following on from last months publication that gave a brief introduction into the viability of constructing a model using machine learning techniques that can predict the direction of daily moves in the European high yield index using data from the previous trading day.

In this months note, we have taken a step back and constructed a simple model using traditional statistical techniques that use GDP forecasts to predict moves in the Dow Jones ETF’s.

Over the coming months, we will endeavor to show how data science can be used as an integral part of the investment management process and highlight its advantage over basic statistical modeling techniques traditionally used in finance.

With further modeling and analysis to confirm this basic investigation, investors may be able to use this information in their asset allocation decisions and profit from equity market beta-selection.

US sanctions against Venezuela’s central bank and PDVSA, announced on Monday (January 28), have sent refiners on the US Gulf Coast scrambling for replacement supplies of heavy crude. Though they do not cover the business of non-US entities with PDVSA, the move has put Venezuelan crude importers in China and India on notice.

For US refiners, the three main alternative suppliers of heavy, sour crude — Canada, Mexico and Saudi Arabia — are either constrained in their ability to step up supply or are deliberately reducing shipments.

Venezuela’s upstream oil sector has been limping for a long time now. But the sanctions against PDVSA may deal it a death blow. The crude market is keeping a wary eye on the situation but appears unwilling to price in the worst-case scenario for the time being, as it remains fixated on the global economic prospects and concerns over oil demand growth.

We look at the fallout of the latest move by Washington on the primary entities doing oil business with Venezuela: refiners in the US, China and India (the main markets for Venezuelan crude) and Russian giants Rosneft and Lukoil.

We also discuss the likelihood and impact of Venezuelan crude production grinding down from the current 1 million b/d to zero.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In our Discover SZ/SH Connect series, we aim to help our investors understand the flow of northbound trades via the Shanghai Connect and Shenzhen Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by offshore investors in the past seven days.

We split the stocks eligible for the northbound trade into three groups: those with a market capitalization of above USD 5 billion, and those with a market capitalization between USD 1 billion and USD 5 billion.

We note that offshore investors were buying all GICS sectors, and had a strong preference for Consumer Staples, Financials and Consumer Discretionary names. We estimate that total inflow into A-share market via northbound trade amounted to USD 8.5 bn in January.

An earlier post outlined the general direction of the Objective Analysis 2019 forecast but didn’t provide any numbers. In this post I explain the 5%+ decrease in revenues that the market will experience and how and why various elements play into that number.

This is a monthly version of our HK Connect Weekly note, in which I highlight Hong Kong-listed companies leading the southbound flow weekly. Over the past month, we have seen the flow turning from outflow to inflow. Our previous insights published in Jan can be found in the links below. In this insight, we will focus on the month flow to get a bigger picture vs the weekly flow.

Our January Coverage of Hong Kong Connect southbound flow

China’s 4Q GDP grew just 6.4% in Q4, 2018, the lowest since the Global Financial Crisis (GFC). We do not believe the number matched the market expectation, however. Since the GFC, every rebound of the Chinese economy has been accompanied with the rebound of the real estate sector (such as in 2009, in 2012 and in 2016). However, this time is different, in our view. The real estate sector only grew 2% in Q4, 2018, the lowest in 4 years.

If the Chinese government had relaxed its regulation on this sector, China would have grown higher, but that would be at the expense of bigger bubble-driven growth, in our judgment. As we argued before, the consumption growth is closely-corelated with the wealth effect from real estate market. Accordingly, as to the questions such as why the Chinese economy has slowed down, and why Chinese consumption has declined, we believe the answer lies in the real estate sector. As a result, this has become a matter of real estate bubble versus consumption, the debacle we believe will last at least this year.

In addition, the industrial-value added growth, infrastructure investment, electricity generation and retail sales as well, have all marginally rebounded in December. China’s growth may finally rebound in the second quarter of 2019.

This share class monitor provides a snapshot of the premium/discounts for various share classifications around the region, and comprises four sets of data:

The average premium/discount for each set over a one-year period is graphed below.

Source: CapIQ

For a granular breakdown of each data set, PDFs are attached at the bottom of this insight.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Beyond the aggregate figures, most investors interested in China housing markets would look at the breakdown by Tier. We introduce a few alternative ways to cut the house price growth data, illustrating some consistent patterns that could be more meaningful for any investment thesis than the simple by-tier.

For the December quarter results, the market is focusing on the slowdown of the revenue growth, but we notice that the growth rate of operating profits recovered.

In two of our previous reports, we mentioned BABA’s efforts on cost control in the second half of 2018. Now we can see the results.

We believe the most important risk is the significant operating losses in the minor business “digital media”.

The P/E band suggests that the stock price has an upside of 40%.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Cyberagent Inc (4751 JP) reported 1Q FY09/19 financial results on Wednesday (30th January) after the market close. CyberAgent reported revenue of JPY110.8bn (+13.2%YoY) and OP of JPY5.3bn (-35.2%YoY) for 1Q FY09/19.

Revenue and OP both missed consensus (JPY111.7bn and JPY8.2bn respectively). This was mostly due to low OP from the Game business due to increased advertising expenditure for new titles. OP margin of the Internet Advertisement business also fell due to upfront investments for expansion. Media business, driven by AbemaTV, demonstrated strong topline growth driven by robust increase in the number of AbemaTV premium users but continued to make losses due to heavy investment in content development.

CyberAgent revised down its full-year FY03/19E OP guidance to JPY20bn from JPY30bn previously, but we continue to remain positive about the company’s long term performance, driven by the prospects of its passive TV business (see Mio Kato‘s previous note on this Cyberagent: Aggressive Plans for Passive TV).

CyberAgent’s share price closed at JPY3,500 on Thursday (31st January) down 16% from its previous close. CyberAgent’s share price has been on a bearish trend for the last two quarters, down 49% from an all-time high of JPY6,800 in July. We believe this presents an ideal buying opportunity for the stock. Our SOTP valuation for CyberAgent gives a FY1 target price of JPY4,480 which implies a 28% upside to the current market price.

TDK revised its FY03/19E guidance following the 3QFY03/19 earnings release, which underperformed both consensus and LSR expectations.

The company has been affected by the US-China trade war and the deceleration of the Chinese economy in the third quarter.

Revenue guidance for FY03/19E has been decreased to JPY1,370bn from JPY1,420bn (-3.5%) projected in October 2018. OP guidance for the year has been reduced to JPY110bn compared to the previous expectation of JPY120bn (-8.3%).

On our estimates, TDK is currently trading at a FY1 PE of 12x, lower than its historical median of 16.4x.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

A Japanese newspaper recently reported that JDI is expected to post a consolidated loss for the current fiscal year. However, the company claims that the newspaper report was not based on any forecast made by JDI. The company has stated that it is currently calculating topline and bottomline for the third quarter and it expects the economic slowdown in China, prolonged user lifecycles for smartphones and the US China trade war to in fact have a greater than expected impact on the company’s financial performance. While its third quarter results are to be released in mid-February 2019, consensus expects the company to turnaround its losses to make an overall net profit for the year.

Koito Manufacturing (7276 JP) released its 3QFY03/19 earnings that saw revenue outpace consensus estimates by +2%, while Stanley Electric (6923 JP) ’s revenue fell below consensus estimates by -1%. While Koito witnessed revenue growth of 10% YoY, Stanley posted a decline in revenue for the quarter by -4% YoY. On profitability as well, Koito witnessed growth of +6% YoY, achieving an OPM of 12%. Stanley, on the other hand, experienced a decline in OP for the quarter by -7% YoY, although still managing to achieve a relatively higher OPM of 13%. Here again, Koito managed to beat consensus estimates by +1% while Stanley fell below consensus estimates by -3%. Our conservative estimates for 3Q looked a bit light for Koito while they were slightly high for Stanley. Koito has been the company which usually disappoints the market with its earnings results, although it has proved otherwise this quarter.

That being said, it should be noted that, although Stanley’s three months ended results did not look particularly robust, its nine months ended results were quite favourable. The company witnessed the revenue grow 0.5% YoY (for the nine months ended 30th Dec 2018) while OP grew by 5.9% YoY, supported by the steady growth in the high-margin LED headlamps. For Koito, on the other hand, the three months ended results seemed quite favourable, although the nine months ended results displayed a revenue decline of -5.1% YoY and OP decline of -2.4% YoY, citing the deconsolidation of its Chinese subsidiary and the decrease in the volume of automobile production in some of its business regions as the key reasons. Thus, the overall YTD financial performance of Stanley looks still attractive compared to that of Koito. Following the earnings release, Stanley opened -3.7% down on Thursday from Tuesday’s close, while Koito closed +4.8% up on Wednesday since Friday’s close.

SCSK currently holds 4,768,000 shares or 69.52% of voting rights.

The Tender Offer is at ¥2,750/share which is a 39.3% premium to the last traded price of the day before the announcement (¥1,974), a 38% premium to the one-month average, and a 41% premium to the 3-month and 6-month averages.

It is being done at about 7.5x TTM EV/EBITDA.

This is one of those situations with which the currently underway METI M&A Fairness enquiry might have a problem.

TOPPAN PRINTING (7911 JP) is Japan’s current Negative Enterprise Value ‘champion’. Although only growing in the low single digits and with margins to match, comprehensive income margins and returns are significantly higher, as they take Toppan’s significant investment portfolio gains into account. The investment portfolio has grown at a 39.1% compound annual growth rate (CAGR) over the last five years, outperforming Toppan’s core operations (6.4% CAGR) and the overall stock market (7.5% CAGR).

Source: Japan Analytics

MARKET MYOPIA – Despite the investment portfolio’s ¥411b contribution to Shareholder’s Equity, which has otherwise only increased by ¥98b, the stock market preferred to focus on the stagnating top-line, and the shares have been serial underperformers. Toppan’s market capitalisation has grown by only 2% per annum or just ¥34b since December 2013. From the recent peak in June 2017, Toppan shares have underperformed the market by 27% and, for the last year, have been at their most extreme value relative to TOPIX over the previous thirty years. During this period, Toppan’s equity holdings rose from 43% of the company’s market capitalisation to close to parity at the recent market peak in September 2018.

Source: Japan Analytics

BOTTOMING OUT – With the upcoming boost to sales in the printing business from the change in Japan’s gengō (元号) or era name on the accession of the new Emperor in April, the shares have finally broken out of a one-year period in the Oversold ‘doldrums’.

Source: Toppan Printing Investor Presentation November 12th 2018

SELLING STRATEGIC INVESTMENTS – More importantly, the company has become more proactive in managing equity risk. On 23rd January, Toppan sold 10.5m shares in Recruit Holdings (6098 JP) for approximately ¥31.5b, reducing Toppan’s holding in Japan’s leading listing employment services business from 6.57% to 6.05%. Despite the boilerplate language used to describe the company’s strategy towards strategic shareholdings, Toppan has begun to address the portfolio more proactively and in accordance with the spirit of the new guidelines on Corporate Governance in Japan.

Source: Japan Analytics

BUYBACK POTENTIAL – With this sale, Toppan’s liquid assets will now exceed US$3b or 58% of the current market capitalisation, while the company has committed to capital expenditures totalling only ¥125b over the next five years. Toppan last conducted a modest 0.2% share buyback in 2015-Q2, which was ‘unwound’ by a 0.5% reduction in Treasury Stock in 2017-Q3, which was not accompanied by a share cancellation. With just 8% of shares outstanding held in treasury, there is ample room for further buybacks.

Source: Japan Analytics

For Japan’s ‘Deep Value’ investors or even the ‘activists’, Toppan is an attractive opportunity.

In the DETAIL below, we list the ‘top’ twenty-five negative enterprise value companies in Japan and provide a brief overview of Toppan’s business, the investment portfolio and explain why, with apologies to our ‘Brothers in Arms’, Dire Straits, investors in Toppan are, at present, getting their ‘money for nothin’ and clicks for free’.

Dire Straits: Brothers in Arms/Money for Nothing – Knopfler/Sting – 1985

This share class monitor provides a snapshot of the premium/discounts for various share classifications around the region, and comprises four sets of data:

The average premium/discount for each set over a one-year period is graphed below.

Source: CapIQ

For a granular breakdown of each data set, PDFs are attached at the bottom of this insight.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.