In this briefing:

- Smartkarma’s Week that Was in 🇯🇵/🇰🇷 : Korea’s NPS, Samsung, Toshiba, Hitachi Hi-Tech, Payments

- Last Week in Event SPACE: Chiyoda, Shin Etsu Chemical, GLOW, HNA, Hyosung, Wheelock

- BGF Stub Trade: Sub Price Diverged Further than Usual, I’d Make Trade on Reversion

- ECM Weekly (16 March 2019) – Embassy Office REIT, Tiger Brokers, Dongzheng Auto, Koolearn, CanSino

- Moore’s Law May Not Be Dead, After All

1. Smartkarma’s Week that Was in 🇯🇵/🇰🇷 : Korea’s NPS, Samsung, Toshiba, Hitachi Hi-Tech, Payments

Something of a slower week on Smartkarma this week (I contributed to that slowness by being away and under the weather when back) with about 120 insights published. A list of the insights to do with Japan and Korea this week are listed below.

There will be a couple more shortly.

For more detail, read on below the fold…

For me, the MUST READS of this weak are the cashless payment-related pieces by Kirk Boodry and Michael Causton shown at the bottom.

2. Last Week in Event SPACE: Chiyoda, Shin Etsu Chemical, GLOW, HNA, Hyosung, Wheelock

Last Week in Event SPACE …

- One interpretation on how Chiyoda Corp (6366 JP) may source additional loans and equity.

- Shin Etsu Chemical (4063 JP)‘s chunky buyback, but who is the seller?

- Glow Energy Pcl (GLOW TB)‘s plain vanilla arb as the SPA completes.

- HNA cashes in its Hong Kong International Construction Investment Management Group Co., (687 HK) stake after the Kai Tak property buy/sell roller coaster.

- Both Hyosung Corporation (004800 KS) and Hyosung TNC Co Ltd (298020 KS) have under performed the broader market, however TNC is the turnaround story.

- Non-PRC exposed Wheelock (20 HK) companies in favour as cooling measures challenge Wharf Holdings (4 HK)‘s property sales forecasts.

- Plus other events, CCASS movements and upcoming key dates for M&A transactions.

(This insight covers specific insights & comments involving Stubs, Pairs, Arbitrage, share Classification and Events – or SPACE – in the past week)

EVENTS

Chiyoda Corp (6366 JP) (Mkt Cap: $649mn; Liquidity: $13mn)

Since early November, when Chiyoda incurred substantial losses, scant details regarding the structure of the likely capital raise have emerged, except that the components would include additional loans and equity from industrial partners and most likely, main shareholder Mitsubishi Corp (8058 JP).

- LightStream Research‘s conversations with the company suggest a high likelihood a deal would not be in place by the end of Mar, though in a one-on-one meeting they said they were in the final stages of discussions. Lightstream believes a deal is almost certain to be in place by the time of the company’s fiscal year earnings announcement which should be in mid May.

- Getting injections of debt capital from banks (likely Mitsubishi Ufj Financial (8306 JP)) and equity capital from Mitsubishi are unlikely to be stumbling blocks. It is plausible that Mitsubishi would be keen to retain its current 33.39% stake in the company, so if the capital is in the form of prefs, Lightstream would expect them to be convertible.

- As for the industrial partner, Chiyoda noted that there was significant interest due to their long track record as the leading LNG EPC player in the world, and that it was not so much a matter of being able to secure the financing, as it was a matter of finding a partner where there would be mutual benefits without constraining Chiyoda in terms of its business operations. But that implies the stake would be so large as to imply a controlling or heavily influential stake.

- In terms of numbers, Lightstream speculates about ¥30bn in debt from banks with MUFG a likely lead candidate given the keiretsu ties. Perhaps ¥75bn in equity (prefs and common) split between Mitsubishi and an industrial partner. More likely, if Mitsubishi opted for pref shares, the industrial partner would end up with a stake of around 20% in Chiyoda, which could mean a ¥25bn injection, with Mitsubishi buying ¥50bn in prefs.

(link to Lightstream’s insight: Chiyoda: Minor Updates About the Major Capital Infusion, Cost Overruns and Upcoming Orders)

Shin Etsu Chemical (4063 JP) (Mkt Cap: $33bn; Liquidity: $122mn)

Shin Etsu announced a share buyback program to buy up to 14mn shares for up to ¥100bn. If it were to have bought all 14mn shares, that would be 3.3% of shares outstanding. Simultaneously, it announced a ToSTNeT-3 buyback of 11,001,100 shares at today’s closing price of ¥9,090/share which if all bought would complete the buyback program.

- There was some speculation across the Street there would be a buyback because of slowing earnings expectations and a surfeit of capital, which was itself important because of the company’s lack of recent history of buybacks (the last and only time the company has bought back shares (to date) was a repurchase of 3 million shares for ¥13.6 billion in late October 2008 when things were hairy (and cheap))

- It was a decent-sized buyback. That by itself is worthwhile. But it is not enormous. And with ¥1tn in net cash, buying back ¥100bn is not huge enough. It reduces the dividend out a little, and lifts EPS a little. But…

- The BIG trade here is to identify the seller as quickly as possible – if it is a corporate seller. If it is Hachijuni Bank, buy Hachijuni Bank. If it is another small listed financial for whom the position is meaningful portion of market cap, Travis Lundy would be inclined to buy that one.

- As a follow-up…

- the result of the ToSTNeT-3 transaction was that the company bought back 9.84mm shares using 89.5% of the funds. The remaining ¥10.5bn to buy will likely be bought on market. It represents less than one day of volume.

- Travis notes that there have been no announcements on TDNET which indicate who the seller might have been. If it had been a life insurer, it would not have made the news because it was portfolio gains, not corporate gains. It is also possible that corporate or bank holders in question would have other sales to offset the gains. We may not know until the yuho.

- Nonetheless, the selldown of cross-holding has continued since the Nintendo situation discussed here (Nintendo Offering & Buyback: The Import & The Dynamics) as well-known cross-holders Tokyo Broadcasting System (9401 JP) and Ibiden Co Ltd (4062 JP) have also sold large single cross-holdings in the last two weeks.

(link to Travis’ insight: Shinetsu Buyback – Maybe More Than It Appears)

Omron Corp (6645 JP) (Mkt Cap: $9.7bn; Liquidity: $69mn)

The previous Friday, the Nikkei announced that because the third party share sale of Pioneer Corp (6773 JP) had been completed, it would be deleted from the Nikkei 225 Average (and the Nikkei 500 Index). Omron will replace Pioneer in the Nikkei 225, with a deemed par value of ¥50 per share. The date for this index deletion and inclusion event was the 15th of March.

- The Pioneer exclusion has been known/certain since the deal was approved. The Omron inclusion was less well-flagged. There is a lot of Pioneer stock to come out this week. Because it is so much, and because many people will not want to hold more than 5% of the company, Travis expects there is room for several people to increase their stake for an OK size.

- There is a possibility that Sharp Corp (6753 JP) and possibly Japan Display (6740 JP) and Murata Manufacturing (6981 JP) get hit on this because they were also in the “maybe this will be selected” group of tech shares.

- Because of the path of Omron over the past year, Travis expected there would be many foreign holders unwilling to sell their shares at the current price. And they would be ill-prepared to sell large quantities in the market on Friday just because there was a Nikkei 225 inclusion. Travis expected the shares to squeeze. It is not easy to dislodge 25% of the float.

- THE HINDSIGHT: As Travis notes in a discussion point appended to his piece, it appears every single buyer post-announcement was down-money by the inclusion, which happened at the lowest price of any traded post-announcement. This indicates substantially more pre-positioning than he thought, and the low volume on the print itself suggests substantially more shorting than might be healthy.

(link to Travis’ insight: Omron into the Nikkei 225, Pioneer Out)

Hyundai Heavy Industries (009540 KS) (Mkt Cap: $7.8bn; Liquidity: $39mn)

The Daewoo Shipbuilding & Marine Engineering (042660 KS) deal between HHI and KDB is now officially finalised, and it will take the following four-step process: the HHI (to be renamed Korea Shipbuilding & Offshore Engineering, or KSOE) spin-off of the opco (HHI opco); the KDB PIK into HHI; the KSOE rights issue; followed by the DSME rights issue. These details were further elaborated upon in Sanghyun Park‘s prior insight: Hyundai Heavy/DSME Event – Comprehensive Summary.

- HHI declined 4% when the deal was finalized while DSME stayed flat. Apparently HHI and Korea Eximbank agreed that the ₩2.3tril CBs wouldn’t be converted into DSME shares and disposed any time soon. Plus, there will be a downward interest adjustment to help ease DSME’s financial burden.

- This sparked a speculation that HHI must have pledged Korea Eximbank with some sort of DSME expected valuation. Sanghyun would close the current HHI long/DSME short position. Short-term, he expects DSME will outperform HHI. Longer term, he’d rather stay away from both.

(link to Sanghyun Park‘s insight: HHI – DSME Acquisition: Current Situation & Trade Approach)

M&A – ASIA-PAC

Glow Energy Pcl (GLOW TB) (Mkt Cap: $4.2bn; Liquidity: $5mn)

The revised SPA between Engie SA (ENGI FP) and Global Power Synergy Company Ltd (GPSC TB) closed this week – i.e. Engie crossed its 69.11% holding in GLOW to GPSC – triggering a mandatory Tender offer for GLOW.

- The revision – the divestment on the SPP1 co-generation plant – was a remedial requirement by the ERC regulator. The sale of SPP1 to B Grimm Power (BGRIM TB) for Bt3.3bn was announced on the 22 February and was completed mid-week.

- Subsequent to the SPP1 sale, the purchase price under the SPA was adjusted to Bt91.9906/share, a ~3% decline from the initial Bt94.892/share price under the original SPA.

- My discussions with GLOW indicate that the 247-4 Tender Offer form may be submitted to the SEC & SEC by GPSC as early as next week, with the Offer open to acceptances shortly after. The ERC signed off on the SPA the previous Friday. Assuming mid-May payment, this is currently trading at a gross/annualised spread of 1.6%/10.8%.

(link to my insight: GLOW’s Done Deal As SPA (Almost) Completes)

Hong Kong International Construction Investment Management Group Co., (687 HK) (“HKICM”) (Mkt Cap: $1.3bn; Liquidity: $2mn)

HKICIM announced HNA Finance had entered into a SPA in which Times Holdings, a Blackstone-controlled vehicle, had conditionally agreed to buy 69.54% of HKICIM’s issued shares for HK$3/share in an HK$7bn transaction. Should the SPA complete, Times will make a mandatory unconditional offer – also at $3.00/share (14.5% premium to last close) – for the remaining 30.46% of shares out. This proposal arrives nearly three years after HNA bought a 66% in Tysan Holdings – as HKICIM was previously known – from Blackstone for HK$4.53 per share, triggering an MGO.

- After a rapid-fire acquisition spree – at record prices, oddly motivated to “snatch land and pricing power from the city’s real estate cartel” – and similar disposal pace of Kai Tak properties, HNA is presumably recycling these sales proceeds to offset its debt obligations.

- This will continue to trade tight to, if not through terms, with an anticipated completion late April. There will be no bump to the Offer. Times does not intend to avail itself to compulsory acquisition and intends to maintain HKICIM’s listing; while both Times and HKICIM will take appropriate steps to maintain a sufficient public float after the close of the Offer.

(link to my insight: Another MGO For HKICIM As HNA Sells Stake Back To Blackstone)

Xenith Ip (XIP AU) (Mkt Cap: $115mn; Liquidity: $1mn)

Iph Ltd (IPH AU) has gate crashed Xenith/Qantm Intellectual Property (QIP AU)‘s marriage of equals, submitting a proposal (by way of a Scheme) for Xenith comprising cash (A$1.28) and IPH shares (0.1056 IPH shares) or A$1.97/share, 23.3% above the implied QANTM all-scrip merger consideration, based on QANTM’s 26 Nov 2016 closing price.

- On the same day as the Xenith/QANTM announcement, IPH lobbed a non-binding cash & scrip proposal to acquire QANTM at $1.80/share (including a A$0.05 dividend) by way of a scheme, or a 42% premium to last close. QANTM’s board rejected the proposal due to its highly conditional nature, significant execution risk, and that the offer undervalued the company. So, IPH bought a 19.9% stake in Xenith at $1.85/share (or ~A$33mn) from institutional investors, and further added that is does not support QANTM’s merger and intends to vote against it at the forthcoming scheme meeting on the 3 April.

- The key risk to IPH’s proposal is ACCC’s consent – the provisional clearance date for the QANTM/Xenith merger is the 21 March; while IPH/Xenith‘s is the 2 May. IPH, QANTM and Xenith are the only three ASX-listed intellectual property companies, and IPH is the largest (in terms of revenue). However privately owned companies collectively hold a larger market share – and growing – compared to the three listcos. It is not apparent a merger between either of these two listcos would lessen IP service competition in Australia.

- With a 19.9% blocking stake, the QANTM/Xenith scheme is toast. 19.9% of institutional investors have already cashed out at $1.85/share. Xenith should engage with IPH.

(link to my insight: IPH Goes Hostile on Xenith)

STUBS & HOLDCOS

Hyosung Corporation (004800 KS) / Hyosung TNC Co Ltd (298020 KS)

In the past six months, Hyosung Corp is up 62% while Hyosung TNC is down 12%. Corp’s share price has surged in the past six months on account of excellent dividends, strong financial results and the timing of the increased insider ownerships/completion of tender offers. Douglas Kim believes the market has already factored into Corp’s share price many of these positive factors.

- Both TNC and Corp have underperformed the market. However, TNC appears to be a turnaround story driven by a decline in raw material prices, aggressive spandex investment in India, the stabilization of spandex prices in 2H19 and the consolidation of the global spandex industry

- Douglas would be long TNC and short Corp on a dollar-for-dollar basis. His base case strategy is to achieve gains of 7-9% on this pair trade. Plugging in Douglas’s numbers results in the discount to NAV at extreme levels. One pushback is that TNC accounts for just 16% of Corps’ NAV. Five other listco holdings total 40% of NAV.

(link to Douglas’ insight: Korean Stubs Spotlight: A Pair Trade Between Hyosung Corp and Hyosung TNC)

Hang Lung (10 HK) / Hang Lung Properties (101 HK)

Curtis Lehnert flags this simple holdco structure wherein the bifurcation between the two counters is in excess of 2 STDs. I also touched on this pair last month (StubWorld: Hang Lung’s Implied Stub At Extreme Levels) and this unreasonably wide discount which is made more than unreasonable by the fact that there is very little to distinguish between the two stocks.

- Curtis proposes one avenue for narrowing the discount – by HLG divesting its stake in HLP. Maybe. Over a decade ago, HLG’s stake dipped below 50% in HLP, but it still consolidated the accounts.

- However the last few years has seen HLG gradually increasing its stake in HLP; and in one instance selling property to HLP (at book), then buying shares in HLP at 0.6x P/B. HLG is cheap, but a catalyst for narrowing the discount remains elusive.

(link to Curtis’ insight: TRADE IDEA – Hang Lung (10 HK) Stub: A Timeless Arb)

Wheelock & (20 HK) / Wharf Holdings (4 HK) / Wharf Real Estate Investment (1997 HK)

Inputting the latest of Wheelock’s, Wharf’s and WREIC’s FY18’s numbers backs out a discount to NAV of 37.5%, bang in line with its 12-month average. Wheelock is coming up “expensive” vs. Wharf, but Wharf accounts for only 25% and 22% of NAV & GAV respectively.

- Wharf’s net profit decreased by 11% in FY18. While the company said cooling measures in China have had minimal impact on demand, it added “the timing of sales launch continued to be dictated by local government approval to sell at full or close to full market price“.

- Chairman & MD Stephen Ng said it will sell/reduce its mainland property investments, ruling out any possibility of returning. This suggests the momentum is with non-PRC asset portfolio companies under the Wheelock group, favouring both Wheelock and WREIC.

(link to my insight: StubWorld: Wharf Under Pressure As Cooling Measures Bite)

Briefly …

- Sanghyun flagged the Street’s FY19 net profit for Nongshim Co Ltd (004370 KS) will touch ₩100bn or a ~16% increase yoy. He sees the Holdco/Sub at -2σ and recommends a set-up trade. Plugging in Sanghyun’s numbers, I back out a discount to NAV of ~47% vs. the 12-month average of 42.5% and one-year range of 34%-53%. The pushback: Nong Shim Holdings Co (072710 KS) is illiquid. (link to Sanghyun’s insight: Nongshim Stub Trade: Sub Moving Up on New Hit Product, Now at Near -2σ)

First Pacific Co (142 HK) exits from the Goodman Fielder JV for US$300mn. First Pac will incur a US$280mn non-cash loss on the sale. Not an ideal return on a five-year investment. Shares closed marginally up suggesting this announcement was largely expected.

SHARE CLASS

Samsung Electronics (005930 KS)‘s Common/1P has reached a +2σ level and on a 120D horizon, the price ratio is currently at the peak. The div yield difference on FY19E is 0.87%p, even higher than last year which was a record high in 3 years. Sanghyun favours SamE’s 1P over Common here. (link to Sanghyun’s insight: Samsung Electronics Share Class Trade: Common at +2σ, Expect Reversion After AGM This Week)

OTHER M&A UPDATES

MYOB Group Ltd (MYO AU)‘s scheme doc is out. The Scheme meeting is scheduled for 17 April, with an expected implementation date of the 8 May. The independent expert, Grant Samuels, considers the Scheme consideration to be fair & reasonable, with an assessed value range of $3.19-$3.69 vs KKR’s Offer of $3.40.

- Trade Me (TME NZ)‘s scheme book is out. The vote will take place on the 3 April. The Independent Adviser concluded that the Scheme consideration of NZ$6.45 is above its valuation range for the shares of NZ$5.93 – NZ$6.39. OIO consent has also been received.

- The IFA believes Delta Electronics Thai (DELTA TB) shareholders should accept the Tender Offer of Bt71/share as it is above its fair value range of Bt62.33-Bt67.80/share.

Sigma Healthcare (SIG AU) has rejected Australian Pharma Industries (API AU)’s non-binding indicative offer and terminated discussions in relation to the merger. Sigma believes its future potential is on a standalone basis. Sigma also cited API’s share price decline of >15% since the 11 October announcement, implying a 12% decline in value for its shareholders; and also flagged the potential execution risk in regards to ACCC consent. (link to Arun George‘s insight: Sigma Healthcare (SIG AU): Rejecting the API Bid Is the Difficult but Right Choice)

- Restaurant Brands Nz (RBD NZ)‘s takeover is now unconditional after Finaccess waived the 75% condition. The offer has been extended until 26 March.

Mastercard’s offer has now lapsed, leaving Visa as the sole bidder for Earthport plc (EPO LN). Visa’s 37 pence offer has been extended for two weeks until the 25 March.

The IFA (UOB) considers the $3.10/share Offer for Kian Joo Can Factory (KJC MK) is “not fair” but “reasonable”. (Best to open the link in Chrome not Edge). UOB considers the Offer price represents a 25 sen or 7.46% discount to the estimated fair value of RM3.35/share. The Offer will be open for acceptances until the 22 March – unless extended.

- Australian property developer, Villa World Ltd (VLW AU) announced that it had received an unsolicited proposal from AVID Property Group Australia to acquire all of the company’s shares for A$231/share (a 12% premium to last close) by way of a scheme of arrangement.

CCASS

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Name | % chg | Into | Out of | Comment |

Noble Eng (8445 HK) | 51.67% | Chaoshang | Outside CCASS | |

Charmacy Pharm (2289 HK) | 11.38% | Deutsche | JPM | |

10.26% | Emperor | Sincere |

UPCOMING M&A EVENTS

Country | Target | Deal Type | Event | E/C | |

| Aus | GrainCorp | Scheme | March | Offer to be Announced | E |

| Aus | Propertylink | Off Mkt | 8-Apr | Last Payment Date | Completed |

| Aus | Sigma | Scheme | March | Binding Offer to be Announced | Rejected |

| Aus | Eclipx Group | Scheme | March | First Court Hearing | E |

| Aus | MYOB Group | Scheme | 14-Apr | Scheme Meeting | E |

| Aus | Healthscope | Scheme | April/May | Despatch of Explanatory Booklet | E |

| HK | Harbin Electric | Scheme | 29-Mar | Despatch of Composite Document | C |

| HK | Hopewell | Scheme | 21-Mar | Court Meeting | C |

| India | GlaxoSmithKline | Scheme | 9-Apr | Target Shareholder Decision Date | E |

| Japan | Showa Shell | Scheme | 1-Apr | Close of offer | E |

| NZ | Trade Me Group | Scheme | 19-Mar | Scheme Booklet Circulated | C |

| Singapore | Courts Asia | Scheme | 26-Mar | Last Payment Date | C |

| Singapore | M1 Limited | Off Mkt | 18-Mar | Closing date of offer | C |

| Singapore | PCI Limited | Scheme | March | Release of Scheme Booklet | E |

| Thailand | Delta Electronics | Off Mkt | 1-Apr | Closing date of offer | C |

| Finland | Amer Sports | Off Mkt | 27-Mar | Closing date of Subsequent Offer for remaining shares | C |

| Norway | Oslo Børs VPS | Off Mkt | 29-Mar | Acceptance Period Ends | C |

| Switzerland | Panalpina | Off Mkt | 5-Apr | EGM | C |

| US | Red Hat, Inc. | Scheme | March/April | Deal lodged for approval with EU Regulators | C |

3. BGF Stub Trade: Sub Price Diverged Further than Usual, I’d Make Trade on Reversion

- BGF Holdco/Sub have been oscillating within ±1σ since early Feb. Last Friday, Sub again made a move. This time it diverted a little further. They are now close to -2σ. Holdco is now at a 46% discount to NAV.

- Overall sector outlook is still unpromising. Local street sentiments are still divided. BGF Retail is showing interest in Korea’s third internet bank. This may become a price divergence factor. But this issue is still too early to have real impact.

- Shorting is still going pretty heavy on Sub. Sub price divergence shouldn’t last any further from this point. I’d make my trade here.

4. ECM Weekly (16 March 2019) – Embassy Office REIT, Tiger Brokers, Dongzheng Auto, Koolearn, CanSino

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Starting with bad news in Korea, Homeplus REIT (HREIT KS)‘s IPO was pulled on the 14th of March which when it was supposed to price. The reason cited was weak demand which stemmed from growth concerns and difficulty in valuing this business.

On the other hand, Hong Kong’s IPO market is getting busier. This week alone, we had Dongzheng Automotive Finance (2718 HK) and Koolearn (1797 HK) that have already opened for bookbuilding and will price next week. We also heard that Sun Car Insurance is already started pre-marketing and it will likely open its books next week. The company had only just re-filed their draft prospectus last week.

Another upcoming Hong Kong IPOs would be Tianjin CanSino Biotechnology Inc (1337013D HK) which we heard had already started pre-marketing. Ke Yan, CFA, FRM updated his assumptions and valuation of the company in his insight, CanSino Biologics (康希诺) IPO: Valuation Update (Part 3).

In India, the focus is on Embassy Office Parks REIT (EOP IN) as this is the country’s first ever REIT IPO. It is also the first time there is a strategic tranche in an Indian IPO which has been taken up by Capital Group. Sumeet Singh has pointed out in his insight that with cost of debt of the REIT being at 9 – 9.25%, it is hard to fathom buying equity at a FY2020E dividend yield of 8.25%. This yield had already been inflated by the lack of interest payments. For detailed explanation, read his insight, Embassy Office Parks REIT IPO – FY19 Revised Down, Yield Propped up by Zero Coupon Bond.

In other countries, we heard that Leong Hup International (LEHUP MK) is aiming to pre-market next month whereas, in Australia, there had been chatter that Prospa Advance Pty (PGL AU) may be back for an IPO again after it had beaten its own estimates from the IPO prospectus.

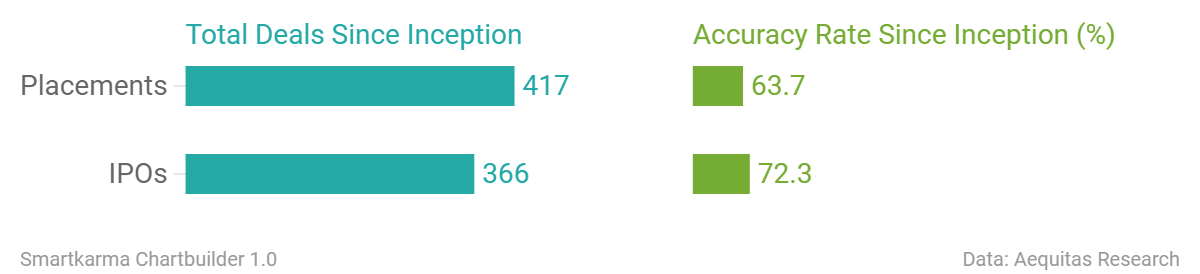

Accuracy Rate:

Our overall accuracy rate is 72.4% for IPOs and 63.7% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

- FriendTimes Inc. (Hong Kong, >US$100m)

- Frontage (Hong Kong, re-filed)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

News on Upcoming IPOs

- UBS and Rivals to Pay $100 Million to Settle Hong Kong IPO Cases

- Chinese Luxury Car Finance Firm Seeks $428 Million in Hong Kong IPO

- Online Educator Koolearn to Raise up to $233 Million in Hong Kong IPO

- Resurgence in Indian IPO market likely only after general elections

- Homeplus K-REIT Withdraws $1.5 Billion Korean IPO on Weak Demand

- Prospa may revive listing plan after beating prospectus forecasts

- Luckin Coffee chairman said to tap banks for $200m loan in exchange for IPO role

This week Analysis on Upcoming IPO

- Homeplus REIT IPO: A Key Landmark Deal in the History of the Korean REIT Market

- Up Fintech (Tiger Brokers) IPO Quick Take – It’s Not like Futu, Won’t Perform like It Either

- Embassy Office Parks REIT IPO – FY19 Revised Down, Yield Propped up by Zero Coupon Bond

- CanSino Biologics (康希诺) IPO: Valuation Update (Part 3)

- Dongzheng Auto Finance (东正汽车金融) IPO Review – Better off Buying the Parent

- Koolearn (新东方在线) IPO Review – Yet to See Results from Increased Spending

5. Moore’s Law May Not Be Dead, After All

For years semiconductor makers and investors have worried that Moore’s Law will end. Although it is not difficult to find proponents of this argument today, this Insight provides evidence that the venerable phenomenon not only is still moving forward, but that it has, in some cases, been moving faster than it has in the past.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.