In this briefing:

- China Tower: More Details on Non Telco Growth Suggest Further Upside to Share Price

- M1 Offer Despatched – Dynamics Still Iffy

- Would a Sale of Founder’s Holdco NXC Corp Trigger a Tender Offer for Nexon (3659 JP)?

- HOYA Corporation: Fairly Priced but Value Accretive M&A Deals Could Support a Higher Price Target

- StubWorld: Time For A BGF Setup? An Unlikely Boost for Kingboard

1. China Tower: More Details on Non Telco Growth Suggest Further Upside to Share Price

After initially being very skeptical of the China Tower (788 HK) IPO given it is essentially a price take to its three largest shareholders, we changed our view in early December to a more positive outlook. What changed our view has been series of calls and meetings with the company that suggested a more shareholder friendly approach than expected and a real opportunity to reduce capex substantially through the use of “social resources” (e.g. electricity grid, local government sites). These can be used to deliver co-locations without building towers and poles and imply much lower capital intensity at a time when revenue growth will be accelerating as 5G is rolled out. Management has also given more detail on non-Tower business prospects which can generate higher returns (not under the Master Services Agreement). While small now (2% of revenue) they are growing rapidly. With lower capex than initially guided and a more shareholder friendly management (i.e. higher dividends are possible) we reduce the SOE discount and raise our forecasts (again). We remain at BUY with a new target price of HK$2.20

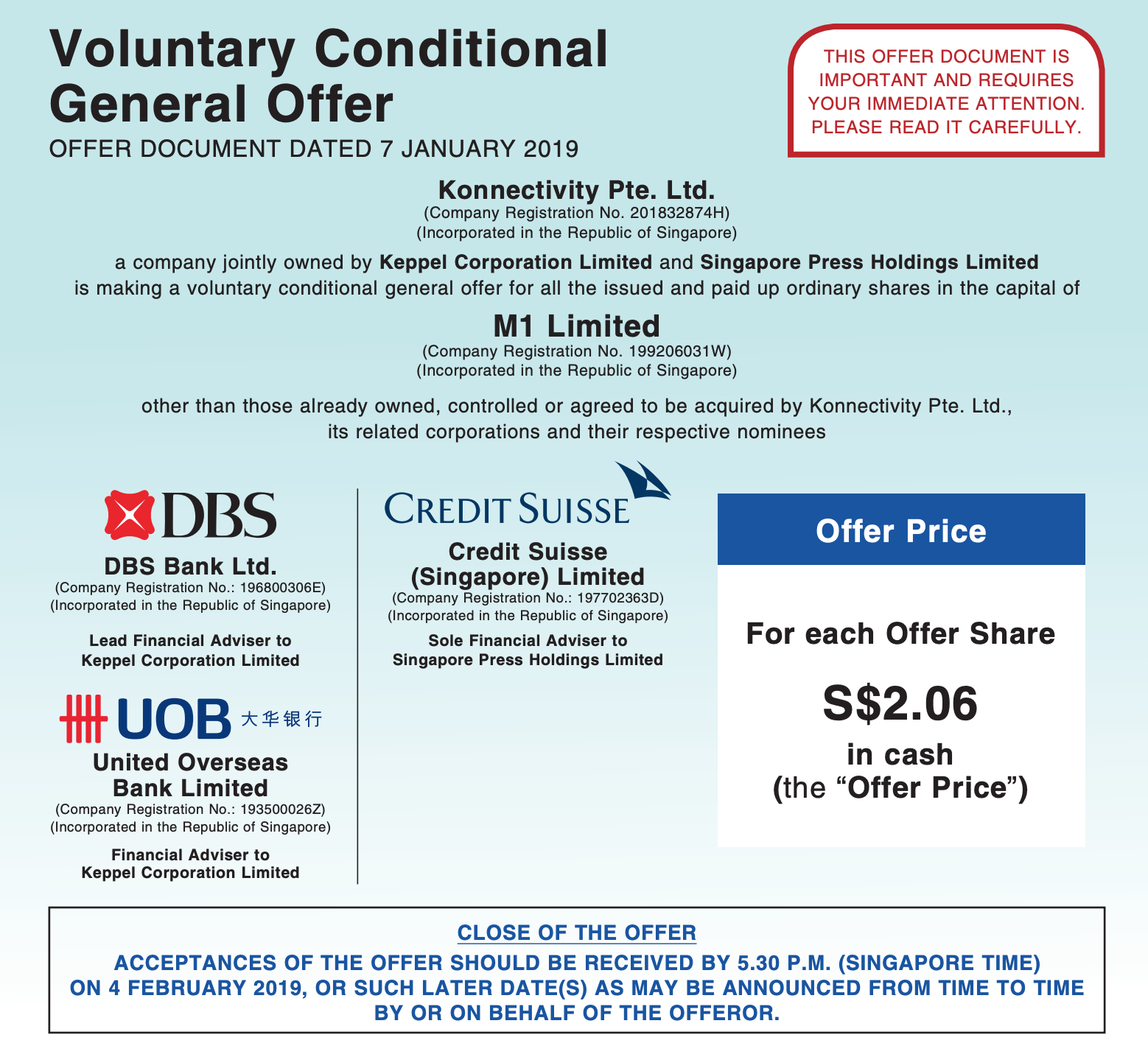

2. M1 Offer Despatched – Dynamics Still Iffy

On January 7th after the close of trading, Konnectivity Pte. Ltd officially announced the launch of its Offer to by M1 Ltd (M1 SP).

The closing date, as clear there, is 4 February.

After three-plus months of speculation that Axiata Group (AXIATA MK) was unhappy with the price and might make a counter-offer, no offer has been forthcoming.

After I wrote on the 2nd in M1 Offer Coming – Market Odds Suggest a Bump But… that the reward/risk did not look that great, shares drifted downward from the S$2.09-2.11 area and into the afternoon of the 7th, traded in the S$2.05-2.07 range, which was the first time in months the shares had traded at or below the prospective offer price.

Some 20mm+ shares (5.5% of the shares out other than the three major holders) traded between 3pm Singapore time on the 7th and a few minutes after the open the day after the announcement. Then part-way through the day, someone bought a large number of shares lifting the share price two spreads for a while. Since then, the shares have settled back down to the $2.07-2.08 range.

Depending on your opinion of the likelihood of a bump, your execution strategy will differ. It’s still not clear that a bump or counterbid will be forthcoming, but at S$2.07, the risks are better than they were higher.

3. Would a Sale of Founder’s Holdco NXC Corp Trigger a Tender Offer for Nexon (3659 JP)?

It was reported on January 3rd that Korean founder and heretofore effective controller of Nexon Co Ltd (3659 JP) Mr. Kim Jung-Ju and family, who exercise their ownership of Nexon through near 100% (98.64% according to Douglas Kim) control of NXC Corp (Korea) and NXC’s control of NXMH B.V.B.A (Belgium), planned to sell their stakes in NXC for up to 10 trillion won (US$8.9 billion).

Those two companies – NXC Corp (Korea) and NXMH (Belgium) – own 253.6mm shares and 167.2mm shares respectively, or direct and indirect ownership by NXC of just under a 48% stake in Nexon (3659 JP). Yoo Junghyun (Kim Jung-Ju’s wife) directly holds another 5.12mm shares at last look.

The speculation is that it might be sold to Tencent Holdings (700 HK) or another global buyer because it might be too big a mouthful to swallow for NCsoft Corp (036570 KS) and Netmarble Games (251270 KS), each of which have a market cap in the area of 10 trillion won themselves.

Nexon was founded in Korea in 1994 and moved its headquarters from Seoul to Tokyo in 2005, listing itself on the TSE in December 2011. The company is a well-known gamemaker (over 80 PC and online/mobile games), with famous games such as MapleStory, Dungeon & Fighter, and Counter Strike.

Douglas Kim has started the discussion of this situation in Korea M&A Spotlight: Nexon’s Founder Plans to Sell; Will Tencent Buy Nexon? and Korea M&A Spotlight: Will the Nexon Group Sell the Korean or the Japanese Company?.

The Korea Economic Daily said in its report on the 3rd of January that Deutsche Bank and Morgan Stanley had been selected as advisors to run a sale process, and a formal non-binding offer to potential bidders was expected next month. A Korea Herald article suggested that “potential buyers, according to industry speculation, include China’s Tencent, Korea’s Netmarble Games, China’s NetEase and Electronic Arts of the US.”

The Big Question

In the second piece, Douglas Kim questions whether Kim Jung-Ju would sell NXC (and NXMH) as reported by the local press, or whether NXC and NXMH would sell their stakes in Japan-listed Nexon, the implication being that if they sold the stake in Nexon, it would mean buyers would get a large stake in a single company, whereas there is a bunch of other stuff floating around in NXC and its subsidiaries.

The other question is whether Tencent or another buyer buying NXC would trigger a mandatory Tender Offer for the shares in Nexon in Japan. The letter of the law in the TOB Rules changed a bit over 10 years ago would indicate not, but there are questions (and precedents) here.

Discussion ensues.

4. HOYA Corporation: Fairly Priced but Value Accretive M&A Deals Could Support a Higher Price Target

HOYA Corporation is currently trading at JPY6,867 per share which we believe is fairly valued based on our SOTP valuation. The company operates with a few stable businesses and holds solid shares in the markets in which it operates. The company generates nearly 50.0% of its revenue from its core business of selling eyeglass lenses and contact lenses. The advancement in eyeglass and contact lenses technology, the growth in global population with vision-related issues due to increased use of PCs, smartphones and tablets and an ageing population will drive demand for eyeglasses and contact lenses. Although the company’s IT Segment which generates around 33.0% of company revenue is growing slowly, the management has aggressively managed the costs to improve the segment’s pre-tax profit margin to over 40.0%. While the Lifecare segment remains the engine of revenue growth for HOYA, it focuses on the IT segment for profitability. HOYA has grown its businesses, mainly the Lifecare segment through value adding M&A deals. The company has announced that it has entered into definitive agreements to acquire US-based Mid Labs and Germany-based Fritz by the end of FY19 (March 2019). The proposed acquisitions could help HOYA to expand its footprint in the global retinal market and further its Lifecare growth. The company has a strong balance sheet with a debt-to-equity ratio of 0.3% as of 2QFY19 with cash and cash equivalents worth JPY252.3bn (35.2% of total assets).

According to our analysis, HOYA operates solid businesses with impressive ROE and positive FCF, however, we believe, the market has already factored most of this into the share price. Therefore, we believe HOYA is worth looking at on the long side if its management continues to find value adding M&A deals which complement its existing lines of business or new business opportunities which would be transformative for HOYA. Our valuation is neutral, but we favour HOYA within the sector as it has held up relatively well despite the tech sell off due to its attractive health care business and shareholder friendliness which was perhaps underappreciated while the market was in its bull phase.

5. StubWorld: Time For A BGF Setup? An Unlikely Boost for Kingboard

This week in StubWorld …

- With concerns over its tender offer for BGF Retail (282330 KS) now behind it, now may be the time for a BGF Co Ltd (027410 KS) setup.

- Kingboard Chemical (148 HK) gets a boost after buying properties from its major shareholder, however, the implied yield is uninspiring.

Preceding my comments on BGF and KBC are the weekly setup/unwind tables for Asia-Pacific Holdcos.

These relationships trade with a minimum liquidity threshold of US$1mn on a 90-day moving average, and a % market capitalisation threshold – the $ value of the holding/opco held, over the parent’s market capitalisation, expressed as a % – of at least 20%.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.