Silverlake Axis (SILV SP) published 2Q19 results which again confirmed that the long-anticipated rise in revenues (+20% YoY) and profits (+99% YoY) has finally arrived. After three years of stagnation, this is the second quarter in a row that real earnings growth is visible.

YTD the share price of SILV has run by approximately 31% as we saw some larger volume spikes earlier this year which indicate that HNA is now finally off the register as a significant shareholder. Since HNA’s stake had dropped below 5% the new buyer has not had to step forward and disclose its identity.

Importantly, management believes the first half of FY19 was just the beginning of a new 3-year growth cycle and prospects are looking good for both FY2019 (ends June 2019) and FY2020 (ends June 2020). Dividends will continue but might be tempered depending on the number of acquisitions that are made.

Risk-Reward is not as attractive as early November but continues to look solid at these levels with a total return of 20% still achievable (assuming mid-point of historical P/E range) or a total return of 60% (assuming high-end of historical P/E range).

The company’s flagship Star Vegas casino resort was victimized by an alleged diversion of VIP players by its contract management. Now under corporate control it is beginning to recover.

Its US$124m breech of contract claim against the vendor was filed in there Singapore court system and sits at final appeal stage.

Cambodia’s new gaming regulation law will stabilize and eliminate wild west dimension of Poipet casinos. This could lead to major earnings gains and increased investment going forward.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Since its announcement on 4Q2018 results and termination of Jiading plant construction, NIO’s share price has been halved. We believe the market has over-reacted on NIO’s cashflow risk. With the expected 30-50% reduction on NEV (New Energy Vehicle) subsidies, all the Start-ups would have worse-than-ever cashflow pressure in 2019. But NIO might survive.

In China’s NEV market, NIO’s market position remains unique among all the Chinese Start-ups. Tesla is still NIO’s main competitor. NIO’s ES6 has capability to compete with Tesla’s Model Y, based on our comparison. Tesla and NIO both have to rely on external funding. The other Chinese Start-ups have to compete with traditional OEMs who have much less cash flow pressures.

NIO’s 4Q2018 financial data were in good trend. We estimate its net loss in 2019 to be further narrowed to Rmb6.1bn. With estimated Rmb13.2bn cash balance at end-Feb 2019, NIO have enough money to cover its estimated cash outflow in the next two year. And it would be able to get another round of external funding in 2020/2021, as long as its business operation ramps up as expected.

Security Bank (SECB PM) trades at a premium to Asian banks on a P/Book, franchise valuation, earnings yield, and total return ratio basis.

The PH Score™ of 5.3 is neither good nor bad. (Asia median is 5.7).

In terms of fundamental traction, efficiency has eroded and interconnected profitability has narrowed. “Jaws” are negative. Funding cost growth is sharply in excess of interest income growth. On the other hand, liquidity and capital adequacy are moving in the right direction or are stable.

Asset quality seems to have dramatically improved. Headline non-performing loans are now very low due to adoption of PFRS9. These are calculated now as loans aligned to a default criteria. The bank seems to have reclassified part of “stage 3” impaired loans back into “stage 2”. “Stage 2” is comprised of assets which have experienced a SICR (significant increase in credit risk) since initial recognition, such as substandard, past-dues, and SMLs, and are not classified as NPLs. “Stage 2” represents almost 4% of the loan book versus a headline impaired or problem loan ratio of just 0.64%. In addition, unimpaired past-due loans (73% of headline NPLs) climbed 57% YoY. Charge-offs soared 47% YoY. Perhaps the asset quality is not as pristine as the NPL ratio intimates.

When we look back from 2004, we see an explosive increase in loans (+10x since 2004) coinciding with lower profitability over this period. This is not a good sign. As the bank shifts to consumer lending for growth, up 10x since 2012, we wonder whether a similar pattern will emerge.

In short, the bank resides in the bottom decile of our global VFM (Valuation, Fundamentals, Momentum) rankings.

The Thai mobile market reported another weak quarter in 4Q18, with trends deteriorating at all three operators. The weakness was partly due to the cheap unlimited fixed speed offers which were popular in 2018 but which have now been removed from the market. Growth should recover by 2H19. With Total Access Communication (DTAC TB) having acquired spectrum in 2018, it will no longer cede market share without a struggle. That suggests competitive risks are high in Thailand, with all three operators aiming to boost market share. We remain cautious on the sector and are also worried that the government seems keen to push on with 5G spectrum auctions despite a lack of use cases.

China Tower (788 HK) has rallied strongly in recent months and the question raised repeatedly in recent client meetings was “how much further is China Tower likely to rally?”. Chris Hoare sees China Tower’s position as unusual as the price moves are not driven by earnings upgrades or changed 5G expectations. Rather is is a sustained move post the IPO when the information in the market was incomplete and expectations were much lower. We were negative at the time of the IPO but changed our views as more information became available. We remain positive on the scope for revaluation in China Tower given its rapid revenue growth and low valuations vs EM peers. While the recent results were somewhat disappointing, we see good upside as the market factors is lower capex and higher returns.

It has taken some time, but finally Philippine National Bank (PNB PM) is being recognized by the market. To us though, this is only the beginning. The story with PNB has for a long time been about a turnaround, moving from a sleepy state-owned bank focused on large corporate loans and with a high level of bad loans, to a more invigorated bank with far better credit quality and a new focus on the consumer. The recent milestone of paying a special dividend was a clear sign of how the bank improved since the Asian Financial Crisis (AFC). The market is now awakening to what a new CEO can do with PNB and one who comes from HSBC Philippines. Still PNB’s market capitalization is only 9% of assets compared with 14-20% for the largest three peer banks. There appears a lot more to come.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Musashino Bank (8336 JP) was one of the last regional banks to announce 3Q FY3/2019 results, and they were a nasty surprise: a consolidated net loss for the nine months to 31 December 2018, caused by heavy reserving in Q3 (October-December 2018) against the bank’s exposure to the troubled Akebono Brake Industry Co (7238 JP) . While the bank has slashed its full-year net profit guidance from ¥11.1 billion to ¥4.5 billion, this would still require an heroic level of profits in Q4 which the bank has never before achieved. The share price has fallen over 31% in the last twelve months. Valuations at current levels are still high (FY3/2019 PER is 17.6x) and we consider the share price to be vulnerable to further weakness. Caveat emptor (May the buyer beware) !

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The Thai mobile market reported another weak quarter in 4Q18, with trends deteriorating at all three operators. The weakness was partly due to the cheap unlimited fixed speed offers which were popular in 2018 but which have now been removed from the market. Growth should recover by 2H19. With Total Access Communication (DTAC TB) having acquired spectrum in 2018, it will no longer cede market share without a struggle. That suggests competitive risks are high in Thailand, with all three operators aiming to boost market share. We remain cautious on the sector and are also worried that the government seems keen to push on with 5G spectrum auctions despite a lack of use cases.

China Tower (788 HK) has rallied strongly in recent months and the question raised repeatedly in recent client meetings was “how much further is China Tower likely to rally?”. Chris Hoare sees China Tower’s position as unusual as the price moves are not driven by earnings upgrades or changed 5G expectations. Rather is is a sustained move post the IPO when the information in the market was incomplete and expectations were much lower. We were negative at the time of the IPO but changed our views as more information became available. We remain positive on the scope for revaluation in China Tower given its rapid revenue growth and low valuations vs EM peers. While the recent results were somewhat disappointing, we see good upside as the market factors is lower capex and higher returns.

It has taken some time, but finally Philippine National Bank (PNB PM) is being recognized by the market. To us though, this is only the beginning. The story with PNB has for a long time been about a turnaround, moving from a sleepy state-owned bank focused on large corporate loans and with a high level of bad loans, to a more invigorated bank with far better credit quality and a new focus on the consumer. The recent milestone of paying a special dividend was a clear sign of how the bank improved since the Asian Financial Crisis (AFC). The market is now awakening to what a new CEO can do with PNB and one who comes from HSBC Philippines. Still PNB’s market capitalization is only 9% of assets compared with 14-20% for the largest three peer banks. There appears a lot more to come.

We met up with management of two companies whose industries couldn’t have been more different. This is the quick run-down on what they are up to recently:

After You posted 14% earnings growth on the back of 20% revenue growth. While this remains healthy, it realizes that domestic market opportunities will become more limited and has started to look abroad with HK as its first market.

Locally, the desserts leader is still planning a slew of new products and some in exclusive partnerships with various airlines such as Air Asia and Thai Smile.

In an effort to reduce storefront expenses, they will start selling certain products outside stores and even online, now 3% of total sales.

Amata’s earnings crashed 28% in 2018 on the back of 2% revenue decline, as Vietnam retroactively forbid certain land sales and even fines the company for past transactions that abided with the law back then!

Grifols SA (GRF SM) and Shanghai RAAS Blood Products Co Ltd (002252.SZ) recently announced an asset exchange that effectively combines the companies’ blood products operations in China. This transaction marks the third investment (two are cross-border) into the industry in the last two years. Despite some challenges arising from recent healthcare reforms, the industry has favorable supply/demand dynamics and high barriers to entry. US-listed China Biologic Products (CBPO US) trades at a significant discount to the implied private market values, but requires patience as management adjusts to the new operating environment.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

China Tower (788 HK) has rallied strongly in recent months and the question raised repeatedly in recent client meetings was “how much further is China Tower likely to rally?”. Chris Hoare sees China Tower’s position as unusual as the price moves are not driven by earnings upgrades or changed 5G expectations. Rather is is a sustained move post the IPO when the information in the market was incomplete and expectations were much lower. We were negative at the time of the IPO but changed our views as more information became available. We remain positive on the scope for revaluation in China Tower given its rapid revenue growth and low valuations vs EM peers. While the recent results were somewhat disappointing, we see good upside as the market factors is lower capex and higher returns.

It has taken some time, but finally Philippine National Bank (PNB PM) is being recognized by the market. To us though, this is only the beginning. The story with PNB has for a long time been about a turnaround, moving from a sleepy state-owned bank focused on large corporate loans and with a high level of bad loans, to a more invigorated bank with far better credit quality and a new focus on the consumer. The recent milestone of paying a special dividend was a clear sign of how the bank improved since the Asian Financial Crisis (AFC). The market is now awakening to what a new CEO can do with PNB and one who comes from HSBC Philippines. Still PNB’s market capitalization is only 9% of assets compared with 14-20% for the largest three peer banks. There appears a lot more to come.

We met up with management of two companies whose industries couldn’t have been more different. This is the quick run-down on what they are up to recently:

After You posted 14% earnings growth on the back of 20% revenue growth. While this remains healthy, it realizes that domestic market opportunities will become more limited and has started to look abroad with HK as its first market.

Locally, the desserts leader is still planning a slew of new products and some in exclusive partnerships with various airlines such as Air Asia and Thai Smile.

In an effort to reduce storefront expenses, they will start selling certain products outside stores and even online, now 3% of total sales.

Amata’s earnings crashed 28% in 2018 on the back of 2% revenue decline, as Vietnam retroactively forbid certain land sales and even fines the company for past transactions that abided with the law back then!

Grifols SA (GRF SM) and Shanghai RAAS Blood Products Co Ltd (002252.SZ) recently announced an asset exchange that effectively combines the companies’ blood products operations in China. This transaction marks the third investment (two are cross-border) into the industry in the last two years. Despite some challenges arising from recent healthcare reforms, the industry has favorable supply/demand dynamics and high barriers to entry. US-listed China Biologic Products (CBPO US) trades at a significant discount to the implied private market values, but requires patience as management adjusts to the new operating environment.

Given overhang risk, investors have been bailing out of Woori or taking short positions. Woori Bank Employees Stock Ownership Association seems to have absorbed part of the selling from the likes of Blackrock, Samsung Asset, SEB Investment, Northern Trust, State Street, Russell Investment, and JP Morgan Asset. We do note though that Vanguard and TIAA have increased their position during the HoldCo transition.

We delve into the latest financials of Woori Financial Group. The picture is mixed. While efficiency advances were the main positive standout, we highlight sharply higher funding costs and a build-up of precautionary loans as main areas of concern. The bottom line was also boosted by much lower loan loss provisions as headline NPLs fell.

A constructive view of the Group is thus based on the credibility of what appears to be underlying asset improvement and the benefits of returning to HoldCo status.

We conclude that despite the overhang risk, shares are not expensive. Shares inhabit the highest decile of our global VFM (Valuation, Fundamentals, Momentum) rankings. There may though be a better entry point for bargain hunters.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

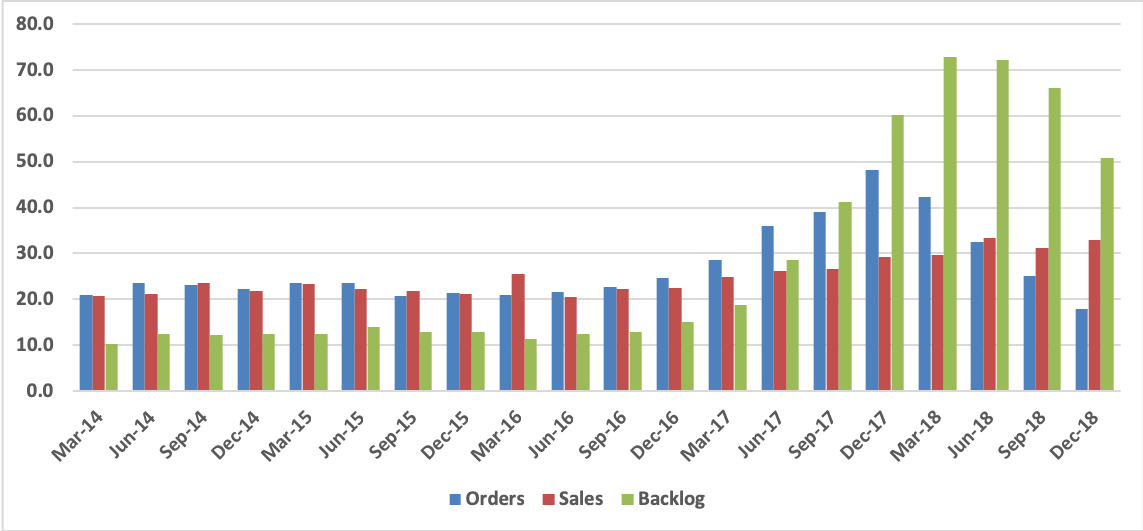

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

It has taken some time, but finally Philippine National Bank (PNB PM) is being recognized by the market. To us though, this is only the beginning. The story with PNB has for a long time been about a turnaround, moving from a sleepy state-owned bank focused on large corporate loans and with a high level of bad loans, to a more invigorated bank with far better credit quality and a new focus on the consumer. The recent milestone of paying a special dividend was a clear sign of how the bank improved since the Asian Financial Crisis (AFC). The market is now awakening to what a new CEO can do with PNB and one who comes from HSBC Philippines. Still PNB’s market capitalization is only 9% of assets compared with 14-20% for the largest three peer banks. There appears a lot more to come.

We met up with management of two companies whose industries couldn’t have been more different. This is the quick run-down on what they are up to recently:

After You posted 14% earnings growth on the back of 20% revenue growth. While this remains healthy, it realizes that domestic market opportunities will become more limited and has started to look abroad with HK as its first market.

Locally, the desserts leader is still planning a slew of new products and some in exclusive partnerships with various airlines such as Air Asia and Thai Smile.

In an effort to reduce storefront expenses, they will start selling certain products outside stores and even online, now 3% of total sales.

Amata’s earnings crashed 28% in 2018 on the back of 2% revenue decline, as Vietnam retroactively forbid certain land sales and even fines the company for past transactions that abided with the law back then!

Grifols SA (GRF SM) and Shanghai RAAS Blood Products Co Ltd (002252.SZ) recently announced an asset exchange that effectively combines the companies’ blood products operations in China. This transaction marks the third investment (two are cross-border) into the industry in the last two years. Despite some challenges arising from recent healthcare reforms, the industry has favorable supply/demand dynamics and high barriers to entry. US-listed China Biologic Products (CBPO US) trades at a significant discount to the implied private market values, but requires patience as management adjusts to the new operating environment.

Given overhang risk, investors have been bailing out of Woori or taking short positions. Woori Bank Employees Stock Ownership Association seems to have absorbed part of the selling from the likes of Blackrock, Samsung Asset, SEB Investment, Northern Trust, State Street, Russell Investment, and JP Morgan Asset. We do note though that Vanguard and TIAA have increased their position during the HoldCo transition.

We delve into the latest financials of Woori Financial Group. The picture is mixed. While efficiency advances were the main positive standout, we highlight sharply higher funding costs and a build-up of precautionary loans as main areas of concern. The bottom line was also boosted by much lower loan loss provisions as headline NPLs fell.

A constructive view of the Group is thus based on the credibility of what appears to be underlying asset improvement and the benefits of returning to HoldCo status.

We conclude that despite the overhang risk, shares are not expensive. Shares inhabit the highest decile of our global VFM (Valuation, Fundamentals, Momentum) rankings. There may though be a better entry point for bargain hunters.

On March 11’th 2019, Nvidia announced the acquisition of market leading high-speed interconnect company Mellanox for $6.9 billion in an all-cash deal. At first blush, the benefits touted by both companies and accepted by most commentators make sense and the deal will be immediately accretive to both EPS and revenues upon closing according to NVIDIA.

However, the clear and present threat to NVIDIA’s future success has little to do with interconnect technologies. Rather, it is the competitive challenge to their GPU solutions for data center acceleration from a broad spectrum of alternatives from the likes of Alphabet, Baidu, Intel, Xilinx, Advanced Micro Devices etc, not to mention the host of custom-ASIC accelerator startups poised to launch their products this year. The acquisition of Mellanox will do nothing to address this situation and we see it as being a distraction from where the company really needs to be focusing.

It will serve one purpose though, as a BandAid to mask the otherwise inevitable decline in its data center revenue growth in the face of ever-increasing competition.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Silverlake Axis (SILV SP) published 2Q19 results which again confirmed that the long-anticipated rise in revenues (+20% YoY) and profits (+99% YoY) has finally arrived. After three years of stagnation, this is the second quarter in a row that real earnings growth is visible.

YTD the share price of SILV has run by approximately 31% as we saw some larger volume spikes earlier this year which indicate that HNA is now finally off the register as a significant shareholder. Since HNA’s stake had dropped below 5% the new buyer has not had to step forward and disclose its identity.

Importantly, management believes the first half of FY19 was just the beginning of a new 3-year growth cycle and prospects are looking good for both FY2019 (ends June 2019) and FY2020 (ends June 2020). Dividends will continue but might be tempered depending on the number of acquisitions that are made.

Risk-Reward is not as attractive as early November but continues to look solid at these levels with a total return of 20% still achievable (assuming mid-point of historical P/E range) or a total return of 60% (assuming high-end of historical P/E range).

The company’s flagship Star Vegas casino resort was victimized by an alleged diversion of VIP players by its contract management. Now under corporate control it is beginning to recover.

Its US$124m breech of contract claim against the vendor was filed in there Singapore court system and sits at final appeal stage.

Cambodia’s new gaming regulation law will stabilize and eliminate wild west dimension of Poipet casinos. This could lead to major earnings gains and increased investment going forward.

Musashino Bank (8336 JP) was one of the last regional banks to announce 3Q FY3/2019 results, and they were a nasty surprise: a consolidated net loss for the nine months to 31 December 2018, caused by heavy reserving in Q3 (October-December 2018) against the bank’s exposure to the troubled Akebono Brake Industry Co (7238 JP) . While the bank has slashed its full-year net profit guidance from ¥11.1 billion to ¥4.5 billion, this would still require an heroic level of profits in Q4 which the bank has never before achieved. The share price has fallen over 31% in the last twelve months. Valuations at current levels are still high (FY3/2019 PER is 17.6x) and we consider the share price to be vulnerable to further weakness. Caveat emptor (May the buyer beware) !

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We met up with management of two companies whose industries couldn’t have been more different. This is the quick run-down on what they are up to recently:

After You posted 14% earnings growth on the back of 20% revenue growth. While this remains healthy, it realizes that domestic market opportunities will become more limited and has started to look abroad with HK as its first market.

Locally, the desserts leader is still planning a slew of new products and some in exclusive partnerships with various airlines such as Air Asia and Thai Smile.

In an effort to reduce storefront expenses, they will start selling certain products outside stores and even online, now 3% of total sales.

Amata’s earnings crashed 28% in 2018 on the back of 2% revenue decline, as Vietnam retroactively forbid certain land sales and even fines the company for past transactions that abided with the law back then!

Grifols SA (GRF SM) and Shanghai RAAS Blood Products Co Ltd (002252.SZ) recently announced an asset exchange that effectively combines the companies’ blood products operations in China. This transaction marks the third investment (two are cross-border) into the industry in the last two years. Despite some challenges arising from recent healthcare reforms, the industry has favorable supply/demand dynamics and high barriers to entry. US-listed China Biologic Products (CBPO US) trades at a significant discount to the implied private market values, but requires patience as management adjusts to the new operating environment.

Given overhang risk, investors have been bailing out of Woori or taking short positions. Woori Bank Employees Stock Ownership Association seems to have absorbed part of the selling from the likes of Blackrock, Samsung Asset, SEB Investment, Northern Trust, State Street, Russell Investment, and JP Morgan Asset. We do note though that Vanguard and TIAA have increased their position during the HoldCo transition.

We delve into the latest financials of Woori Financial Group. The picture is mixed. While efficiency advances were the main positive standout, we highlight sharply higher funding costs and a build-up of precautionary loans as main areas of concern. The bottom line was also boosted by much lower loan loss provisions as headline NPLs fell.

A constructive view of the Group is thus based on the credibility of what appears to be underlying asset improvement and the benefits of returning to HoldCo status.

We conclude that despite the overhang risk, shares are not expensive. Shares inhabit the highest decile of our global VFM (Valuation, Fundamentals, Momentum) rankings. There may though be a better entry point for bargain hunters.

On March 11’th 2019, Nvidia announced the acquisition of market leading high-speed interconnect company Mellanox for $6.9 billion in an all-cash deal. At first blush, the benefits touted by both companies and accepted by most commentators make sense and the deal will be immediately accretive to both EPS and revenues upon closing according to NVIDIA.

However, the clear and present threat to NVIDIA’s future success has little to do with interconnect technologies. Rather, it is the competitive challenge to their GPU solutions for data center acceleration from a broad spectrum of alternatives from the likes of Alphabet, Baidu, Intel, Xilinx, Advanced Micro Devices etc, not to mention the host of custom-ASIC accelerator startups poised to launch their products this year. The acquisition of Mellanox will do nothing to address this situation and we see it as being a distraction from where the company really needs to be focusing.

It will serve one purpose though, as a BandAid to mask the otherwise inevitable decline in its data center revenue growth in the face of ever-increasing competition.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this insight, we will provide an analysis of the performance of selected stocks that just joined the Stock Connect last week.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The company’s flagship Star Vegas casino resort was victimized by an alleged diversion of VIP players by its contract management. Now under corporate control it is beginning to recover.

Its US$124m breech of contract claim against the vendor was filed in there Singapore court system and sits at final appeal stage.

Cambodia’s new gaming regulation law will stabilize and eliminate wild west dimension of Poipet casinos. This could lead to major earnings gains and increased investment going forward.

Musashino Bank (8336 JP) was one of the last regional banks to announce 3Q FY3/2019 results, and they were a nasty surprise: a consolidated net loss for the nine months to 31 December 2018, caused by heavy reserving in Q3 (October-December 2018) against the bank’s exposure to the troubled Akebono Brake Industry Co (7238 JP) . While the bank has slashed its full-year net profit guidance from ¥11.1 billion to ¥4.5 billion, this would still require an heroic level of profits in Q4 which the bank has never before achieved. The share price has fallen over 31% in the last twelve months. Valuations at current levels are still high (FY3/2019 PER is 17.6x) and we consider the share price to be vulnerable to further weakness. Caveat emptor (May the buyer beware) !

Sales and profits were above management’s guidance in FY Dec-18, with operating profit rising 36.9% on a 10.9% increase in sales. But new orders continuously declined and were down about two-thirds year-on-year in 4Q.

In view of the order flow, management is guiding for a 12% decline in sales and a 44% decline in operating profit in FY Dec-19, a forecast that is roughly in line with our own.

On the positive side, historical data indicates that new orders are at or near the bottom of the cycle. Anticipating a better investment climate after some resolution of the U.S.-China trade problem, we are forecasting an increase in sales and profits going into FY Dec-20.

The shares have rebounded by 41% since the beginning of January. At ¥2,720 (Friday, February 15, close), they are selling at 15.6x our estimate for FY Dec-19 and 13.8x our estimate for FY Dec-20E. These multiples look reasonably attractive in comparison with the company’s recent P/E range.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.