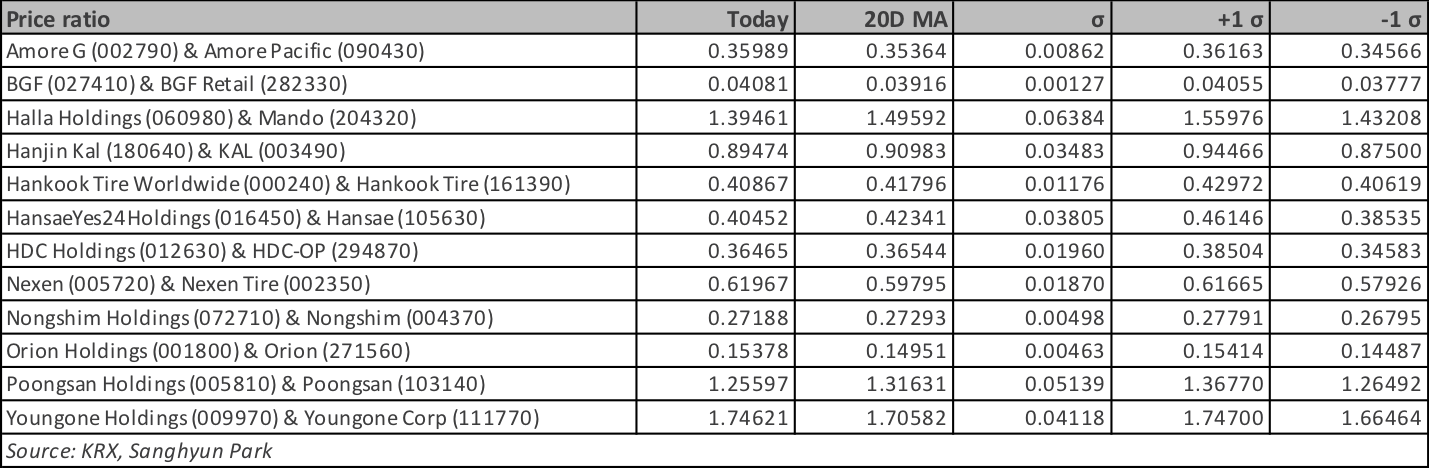

Halla has the widest gap now on a 20D MA. It is at -159% of σ. It was down 130pp yesterday alone. It is currently close to yearly mean. Poongsan is also below -1 σ, down 80pp yesterday. BGF and Nexen are above +1 σ.

Amore quickly reduced the gap yesterday. It is at 78% of σ, down 150pp. Amore Holdco stayed relatively strong yesterday. Holdco is at 78% of σ. But I wouldn’t expect a further decline. Price ratio is still close to yearly low. Holdco discount can be misleading as its two unlisted holdings are severely undervalued.

I’d trade Halla with a very short-term horizon for quick mean reversion. I wouldn’t look at long-term horizon on Halla. Single sub dependency is relatively low. Price ratio is a little above yearly mean. 46% holdco discount doesn’t seem to be particularly cheap either.

BGF, I’d continue to hold onto my long position on Holdco. I explained it in the previous BGF insight. Nexen and Poongsan, I’d wait for a bit wider divergence.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Decathlon is a category killer sans pareil and will finally open its first store in Japan in March. If Decathlon implements its store roll out well, the French sports retailer will cause a major disruption in Japan’s sports market.

Large domestic sports retailers like Xebio Holdings (8281 JP) and Alpen Co Ltd (3028 JP) will be gearing up to compete in some categories but are far behind in private label development and cost performance, and the major sports brands will have to accelerate their plans for retail stores while reviewing pricing (downwards). Sports firms like Mizuno (8022 JP), with relatively low perceived brand value, could face challenges in the newly polarised market that will emerge from Decathlon’s entry.

A major source of competition for Decathlon will come from a more unlikely retailer: the uniforms to outdoor apparel/gear firm, Workman (7564 JP). While still small, Workman is already manoeuvring to hinder Decathlon’s growth in Japan, and looks like having establishment backing to do so – and echoes the growth of Uniqlo after Gap entered the Japanese market in the 1990s and the rise and rise of Nitori (9843 JP) after IKEA’s launch in 2006.

Both Gap and IKEA have relatively small operations in Japan today compared to their early potential. Decathlon will need to expand rapidly if it is to gain sufficient share to stop Workman emerging with a clear lead in its market.

Holding floor support is vital for this trade to work. In absolute terms both APG and APC display similarly weak chart structures with risk of a final bout of weakness. APG displays a more depressed chart reading however.

Trading around its lowest implied stub inside the past five years, improving sentiment toward cosmetic stocks should support an Amorepacific Group (002790 KS) setup.

Preceding my comments on CKI/PAH, Amorepacific and JCNC are the weekly setup/unwind tables for Asia-Pacific Holdcos.

These relationships trade with a minimum liquidity threshold of US$1mn on a 90-day moving average, and a % market capitalisation threshold – the $ value of the holding/opco held, over the parent’s market capitalisation, expressed as a % – of at least 20%.

As per Technopak, BFS is one of the leading manufacturers in the non-glucose biscuit segment in Northern India. It is also one of the largest supplier of buns to the quick-service restaurants and a leading supplier of breads in Delhi NCR and Maharashtra. In addition to its Indian operations, exports account for 30% of the revenue.

Despite providing a host of numbers, the company has failed to provide clear statistics on the growth of revenue of its main segment, domestic biscuits. If one tries to back out this numbers from the other statistics it seems to imply that revenue has been flat for five years. Despite showing some revenue and PATMI growth over the past five years, cash flow from operations as well have been stagnant.

Navitas Ltd (NVT AU), an Australian-listed education company, is subject to a revised bid. On 15 January 2019, the BGH Consortium bid against itself by offering a revised proposal of A$5.825 cash per share, 6% higher than its previous rejected offer.

Navitas’ directors intend to unanimously recommend the revised proposal and have granted the BGH Consortium an exclusivity period. We believe that a binding proposal should materialise and there is also a reasonable chance of a superior proposal from a competing bidder.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The supermarket sector is the most fragmented and uncompetitive of all retail sectors, a situation encouraged by major suppliers and not ideal for consumers.

Despite some effort from the likes of Aeon, consolidation has failed to materialise beyond a few in-group mergers.

Yet pressure on supermarkets to consolidate has been building due to depopulation in the regions, competitive pressures from other food retailers such as convenience stores and drugstore chains, as well as the emerging online food services.

Change is now coming. The biggest industry consolidation yet was announced last month, a precedent-setting alliance between three major supermarkets, Arcs Co Ltd (9948 JP), Valor Holdings (9956 JP) and Retail Partners (8167 JP), carving up a large chunk of the country into three regional fiefdoms.

We initiate coverage of JKN with a BUY rating, based on a target price of Bt8.80, pegged to the the 14.8xPE’19E mean of the Asia ex-Japan Consumer Discretionary Sector.

The story:

Plenty of opportunities in the ASEAN market

Harvest season is imminent

New contracts with three new channels confirm 2019 domestic growth

Mild recovery for domestic digital TV industry in 2019E

Risks: Heavy reliance on a few major customers, probability it will have to set provisions for doubtful debts and potential inability to renew contracts with customers.

Shares of Korean Air Lines (003490 KS) are down nearly 60% since its highs in 2010 and we believe this decline has been excessive. The stock has started to recover and we expected continued outperformance this year. We like both Korean Air (Common) (003490 KS) and Korean Air (Pref) (003495) at current levels. However, we think Korean Air (Pref) has a higher upside. We are including Korean Air (Pref) (003495) in our model stock portfolio. The following are the major catalysts that could boost Korean Air (Common) and Korean Air (Pref) shares by 20-30%+ in the next 6-12 months.

Increasing possibility of a breakthrough in corporate governance with potential help from KCGI & NPS

Cheap valuation/Increasing interests from both value funds and hedge funds

Reduced political conflict between China & South Korea

Turnaround of the aerospace business unit

Huge investment plan by the Incheon International Airport to expand facilities by 2023

Current ratio of Korean Air Pref/Common is below the 1 sigma level

Our deep-dive segment profitability analysis reveals that Meituan Dianping’s (3690 HK) core business (combined food delivery and in-store, hotel & travel) has made good progress toward profitability.

The ballooning consolidated operating losses mainly stem from new initiatives (particularly car hailing and Mobike).

Furthermore, lower S&M expenses to sales ratio plus food delivery’s higher take rate suggests that competition with Ele.me is more manageable than anticipated.

Our SOTP yields intrinsic value of HK$61.07/share, that represents 37% upside potential.

ZOZO (3092 JP) has been hit from all sides recently, with a major sell-off by investors disturbed by Zozo’s execution of its private brand launch and the resulting impact on the company’s reputation among merchants and consumers alike.

Last month it launched a new campaign which, on the surface, was all about helping customers give back to society, but which drew an immediate negative response from some merchants.

One of these, Onward Holdings, withdrew all its brands from sale on Zozo. This is another damaging dent in Zozo’s reputation.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Galaxy Entertainment Group (27 HK) exhibits some valid chart support in the form of a key low at 61.8% retracement and physical price support at the 40 level. This low should stay in place for 2019.

Price and RSI wedge formations are building steam for an upside breakout. MACD bull divergence and the triangle breakout back in November will provide forward upside energy. MACD triangles are some of the most powerful chart set ups.

Currently at an attractive risk to reward support zone for an entry with a reasonably tight stop.

The recent collapse of Xiaomi Corp (1810 HK)’s shares after the end of its six-month lock-up period has focused minds on upcoming lockup expirations. Pinduoduo (PDD US) is the next major Chinese tech company with an upcoming lock-up expiration – its six-month lock-up period expires on 22 January.

We have been bulls on Pinduoduo with the shares up 32% since its IPO. While we are not privy to the shareholding plans of Pinduoduo’s shareholders, we believe that Pinduoduo will likely not mirror Xiaomi’s share price collapse after the end of its six-month lock-up period.

The recent negative sales in the Chinese auto industry and Nissan’s case of Carlos Ghosn removal could put additional pressure on the already thin margin of auto supplier industry. One of the Carlos Ghosn early contribution to Nissan was to cut cost and outsource the auto parts maker to a wide variety of suppliers including to Hanon Systems (018880 KS) . Nissan’s new management may want to undo some of Carlos Ghosn’ legacy including changing the selection criteria of parts supplier.

Hanon’s global peers also experienced a decrease in the inventory turnover and most of them have been priced at PER <10 but Hanon is still trading at 24x PER while its sales growth and profitability is still in low single digit? Facing the onset of the slowdown in the Chinese auto industry, won’t it be another headwind for Hanon Systems?

Local institutions are busy scooping up Hyosung Corporation (004800 KS) shares lately. The owner risk is now gone. There are increasing signs of improving fundamentals on all of the four major subs. Some are already expecting ₩5,000 per share. This is a 9.2% annual div yield at the last closing price.

Discount is also attractive. It is now at 46% to NAV. With this much div yield, discount should be much below the local peer average of 40%.

I’d continue to long Holdco. Hedge would be tricky. Heavy is up 15% YTD. I admit that there is no clear cointegrated relationship between them. But Heavy’s recent rally is more of a speculative money pushing up on the hydrogen vehicle theme. I’d pick Heavy for a hedge.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Leading Indonesian mini-mart operator Sumber Alfaria Trijaya Tbk P (AMRT IJ) (Alfamart) has undergone quite a dramatic transformation over the past 12 months, with a dramatic slowdown in its new store buildout paving the way for a significant pick up in SSSG and a reduction in debt.

The company plans to start to step up its store openings selectively over the next year, with 500 new stores planned and fewer closures. Last year it only opened net 200 new stores having opened 1200 stores the previous year.

The market segment continues to see consolidation, with supermarkets and hypermarts suffering and mini-markets continuing to gain ground as the “pantry of the middle-class”.

The company continues to grow its fee-income business, which is highly profitable, with increasing collaboration with utilities, finance companies, and e-commerce players to name but a few.

After a difficult 2017, Sumber Alfaria Trijaya Tbk P (AMRT IJ) looks to be well and truly back on a growth trajectory, with a rationalisation of its stores, a slow down in its expansion, reduced gearing, and a focus on operational efficiencies. The Mini-market continues to win out in the retail space and is increasingly being used as a distribution network for e-commerce companies. The growth in fee-service from bill payment and other services will be positive for the bottom line. The stock is by no means cheap on a PE basis but provides quite unique exposure to what is still a high-growth area of the economy. According to Capital IQ consensus estimates, the company trades on 51x FY19E PER and 44x FY20E PER, with forecast EPS growth of +30% and +16% for FY19E and FY20E respectively.

Corrigenda: There is an error in this insight. Please note the correction.

Correction: Please ignore the incomplete sentence at the end of the second paragraph in the blue box below (“On the valuation end,…”).

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

It has been a fairly busy week. Activity in the ECM space seems to be picking up with block trades taking the lead this week. We had Xiaomi Corp (1810 HK), Ayala Corporation (AC PM), Puregold Price Club (PGOLD PM), and Longfor Properties (960 HK) placements this week and most of them secondary sell-downs except for Puregold which was a top-up placement. Most placements performed well, trading above their IPO price, except for Longfor which only managed to claw back to its deal price on Friday.

Starting with Xiaomi, we think that there would likely be more selling considering that there is a massive overhang after the lock-up expired on 9th of January. Our calculation indicated that major shareholders may have about 6bn shares to be sold. Even if we exclude the founders’ shares, there will still be about 4bn shares left to be sold. The share price has managed to claw back above HK$10 level on Friday and we also heard that the books were several times covered with allocation being concentrated among a handful of investors. The tighter discount of this placement compared to the one earlier that crossed at 14% discount probably indicated demand is relatively better for this placement. On the valuation end, we

Ayala Corp’s placement was upsized and has also done well contrary to our view. We thought that the sell-down may perhaps indicate that there is an overhang from Mitsubishi’s remaining stake. But, we heard that books were well covered.

For IPOs this week, Weimob.com (2013 HK) traded well on the first day but took a spectacular dive on the second day of trading. It was down 30% intraday before bouncing back up and finally closing at IPO price on Friday. On the other hand, Chengdu Expressway Company Limited (1785 HK) hovered around its IPO price with little liquidity.

In terms of upcoming deals, PH Resorts Group (PHR PM) is looking to launch a US$350m share sale in about two months time. Maoyan Entertainment (EPLUS HK) has already launched its IPO on Friday while there will be more IPOs heading to the US. Jubilant Pharma is said to have turned to the US for its US$500m IPO after trying to list in Singapore last year. Home Credit Group and Sinopec’s retail unit might be seeking to this in Hong Kong this year. Luckin Coffee is also said to be seeking an IPO in Hong Kong.

Accuracy Rate:

Our overall accuracy rate is 71.9% for IPOs and 64.1% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

Shenwan Hongyuang Group (Hong Kong, >US$1bn)

Tai Hing Holdings (Hong Kong, ~US$200m)

Changsha Broad Homes Industrial Group (Hong Kong, >US$100m)

Shanghai Gench Education (Hong Kong, >US$100m)

China Yunfang Holdings (Hong Kong, ~US$100m)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Mitsubishi has finally given up its hope of convincing Aeon to merge Ministop (9946 JP) with Lawson and is selling its stake in the largest retail group.

There will be no change to the extensive supply relationship between the two companies and Mitsubishi’s food wholesale arm, Mitsubishi Shokuhin (7451 JP).

While Aeon seems to have spurned Mitsubishi for now, it is hard to see how Aeon will progress in the convenience store sector without Mitsubishi’s help. In the short-term Ministop looks like a poor investment but Aeon may have to sell to Mitsubishi eventually and will want a good price for it.

Courts Asia Ltd (COURTS SP), a leading electrical, consumer electronics and furniture retailer in predominantly Singapore and Malaysia, has announced a voluntary conditional offer from Nojima Corp (7419 JP) at $0.205/share, a 34.9% premium to the last closing price.

The key condition to the Offer is the valid acceptances of 50% of shares out. Singapore Retail Group, with 73.8%, has given an irrevocable to tender. Once tendered, this offer will become unconditional.

CAL’s share price has endured a steady decline since touching $1.14 back in May 2015. It traded above the Offer price as recently as late-July 2018.

However, the controlling shareholder, which has maintained its stake since CAL’s listing in 2012, is cashing in. Nojima has stated it will exercise its right to compulsorily acquisition if acceptances reach 90%; and it does not intend to support any action or take steps to maintain the listing status of the company in the event its suspended due to free float requirements. I would look to cash out also. Consideration under the Offer may be remitted as early as the fourth week of Feb.

Hankook Tire Worldwide (000240 KS) is again in an interesting position. Its sub, Hankook Tire (161390 KS), is up 2.2% today, putting the duo at -2.2σ. Sub had lost nearly 10% on Jan 2~10 mainly on weakening outlook. Sub has then fully recovered this 10% loss this week. This is putting Holdco at a severely undervalued position on a 20D MA. Holdco discount is now at 41% to NAV.

I initiated a reverse stub trade on this duo on Jan 8. It started at a 0.44953 price ratio. We are now at 0.38882. We would have enjoyed 15% tasteful yield if we had held onto this position up to this day. We have no apparent signal of improving fundamentals on Sub. It appears that Sub’s recent gain should be the work of bargain hunters. Holdco discount is at the local peer average. Price ratio is at yearly mean.

Importantly, this is the first time that price ratio is hitting below -2σ since late September last year. We should expect another quick mean reversion at this level. Just, this time it will be the other way. I’d go long Holdco and go short Sub now.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

China Meidong Auto (1268 HK) has been on a rollercoaster ride in 2018. The stock price of Meidong started 2018 around 2.7 HKD and recently has been trading around 2.9 HKD.

Nice and steady ride? Not exactly, as it has swung from 4.3 HKD in June to 2.6 HKD in August. After analyzing how NPAT estimates evolved over the past year there should be no justifications for these wild swings.

Meidong is likely to report solid FY18 results by late March vs industry peers which are expected to report a weak 2H18. While BMW dealers have been reportedly suffering in China during 2018, Meidong was fortunate to have other luxury brands pick up the slack.

FY19 should be another growth year for Meidong as 1) recently acquired BMW showrooms contribute their maiden results and 2) other luxury brands continue to perform despite overall doom and gloom in the Chinese auto market. Should the Chinese government launch car replacement stimulus measures this would be icing on the cake.

Fair Value lowered slightly from 4.7 HKD to 4.4 HKD (10x 2019E) on lower 2019 profit estimates, which leaves 52% upside excluding dividends.

INVESTMENT VIEW: The Australian Bureau of Meteorology has just downgraded its risk of El Niño from ‘Alert’ to ‘Watch’, and as a result, we temper our optimism for a near-term rally in CPO prices. Longer-term, we remain bullish on Golden Agri Resources (GGR SP), but higher CPO prices remain a key catalyst for our bullish call on the shares.

After adjusting for the interim distribution of A$0.036/share (ex-date 28 December; payment 31 January), the amount payable by ESR under the Offer is A$1.164/share, cash.

The Target Statement issued back on the 20 November included a “fair and reasonable” opinion from KPMG, together with unanimous PLG board support.

To recap: after PLG rebuffed an offer from Centuria Capital (CNI AU) in September, followed by PLG making an offer for Centuria Industrial Reit (CIP AU) – in which both CNI (23.5%) and PLG (17.3%) have sizeable stakes – ESR launched its offer for PLG. Adding to the cross-holdings, ESR also acquired major positions in both PLG (18.06% initially, now up to 19.9%) and CNI (14.9%).

ESR’s Offer is conditional on a minimum acceptance condition of 50.1%. CNI has a 19.5% stake and Vinva Investment Management 5%.

The next key event is CNI’s shareholder vote on the 31 January. This is not a vote to decide on tendering the shares held by CNI in PLG into ESR’s offer; but to give CNI’s board the authorisation to tender (or not to tender) those PLG shares.

Although no definitive decision has been made public by CNI, calling the EGM to get shareholder approval and attaching a “fair & reasonable” opinion from an independent expert (Deloitte) to CNI’s EGM notice, can be construed as sending a strong signal CNI’s board will ultimately tender in its shares. According to the AFR (paywalled), CNI’s John Mcbain said: “We want to make sure when we do decide to vote, if we get shareholder approval, the timing is with us“.

Assuming the resolution passes, CNI’s board decision on PLG shares will take place shortly afterwards. My bet is this turns unconditional the first week of Feb. The consideration under the Offer would then be paid 20 business days after the Offer becomes unconditional. Now trading with completion in mind at a gross/annualised spread of 0.8%/6.7%, assuming payment the first week of March.

M1 Ltd (M1 SP), the third largest telecom operator in Singapore, is subject to a voluntary conditional offer (VGO) at S$2.06 cash per share from Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP) (KCL-SPH). KCL-SPH said on Tuesday that they wouldn’t increase their S$2.06 offer price “under any circumstances whatsoever.”

KCL-SPH’s stance not to increase their S$2.06 offer price is a clever ploy to the put the ball in Axiata Group (AXIATA MK)’s court. Axiata has three options, in our view. We believe that the probability of a material bid to KCL-SPH’s offer is low with Axiata most likely to retain its stake as a minority shareholder.

Maoyan Entertainment (formerly Entertainment Plus) launched its institutional book building last Friday. We covered the company’s background, industry backdrop, financials, shareholders and the regulatory overhang in our previous two notes.

In this note, we will look at the recent development of the company, based on the data from the prospectus and our channel checks. We will also discuss the valuation of the company.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Meanwhile, Descente has brought in Wacoal (3591 JP) as a white knight and made a splash in the business media about its recent success.

Itochu insists that Descente needs Itochu’s management skills, particularly to build a stronger business in China and other overseas markets, and says the only way to make Descente listen is to buy more stock – more than its current nearly 30%.

Healthscope Ltd (HSO AU), Australia’s second-largest private hospital operator, noted today that Brookfield Asset Management (BAM US) is seeking the necessary internal approvals to submit a binding proposal by 31 January. We believe that Brookfield will come through with its binding proposal as the delays are not due to issues cropping up from the due diligence but due to ongoing financing negotiations with multiple banks.

Notably, there is renewed optimism that BGH-AustralianSuper could materialise with a superior proposal. AustralianSuper has three options available, which lead us to conclude that the floor is Brookfield’s Scheme bid with an option of a minor bump from BGH-AustralianSuper.

Just as Pinduoduo (PDD US) lock-up expiry date (22nd January) is approaching, there was news of a massive bug that could result in an RMB20bn loss for PDD. According to the company’s official Weibo account, the bug has already been rectified and a police report has been filed.

In this insight, we will analyze the potential impact of the bug and the number of shares that could potentially be sold upon lock-up expiry.

A week ago, former Nissan Chief Performance Officer and onetime potential successor to Ghosn and/or Saikawa-san – Jose Munoz – who was put on leave to help Nissan deal with its internal investigation – resigned effective immediately. Some suggest this is the start of a bloodbath of Ghosn loyalists.

Former Nissan CEO and still-CEO at Renault Carlos Ghosn was in court to appeal the decision to not allow him bail. I expect that will end up at the Supreme Court in not too long, but for the moment he might stay in detention for another 7-8 weeks.

Nissan sources said (according to a Reuters report) earlier in the week they would be looking to file suit for damages against Ghosn.

Nissan and Mitsubishi officiallyannounced Friday that as a result of a joint investigation by Nissan and Mitsubishi Motors (7211 JP) into the Nissan-Mitsubishi Alliance entity (Nissan Mitsubishi BV), it was discovered that “Ghosn entered into a personal employment contract with NMBV and that under that contract he received a total of 7,822,206.12 euros (including tax) in compensation and other payments of NMBV funds. Despite the clear requirement that any decisions regarding director compensation and employment contracts specifying compensation must be approved by NMBV’s board of directors, Ghosn entered into the contract without any discussion with the other board members, Nissan CEO Hiroto Saikawa and Mitsubishi Motors CEO Osamu Masuko, to improperly receive the payments.” Saikawa and Masuko were not informed and did not also get paid by the company. The NMBV entity will attempt to recoup the funds from Ghosn. Nissan and Mitsubishi are thinking of dissolving their Dutch alliance entity.

The Nissan panel reviewing Nissan’s governance structure, made up of three independent directors and four external members, met for the first time Sunday. The proposals are due end-March, upon which the board will propose a new management system/structure for approval at the shareholder meeting at end-June 2019. The co-chair said in a comment after today’s meeting that Ghosn perhaps had questionable ethics.

French business newspaper Les Echos carried an “exclusive” interview with Nissan CEO Hiroto Saikawa which was reasonably enlightening, or should have been from a French point of view. In the interview, Saikawa is adamant that he fully supports the Renault-Nissan Alliance saying that it was not just important but “crucial” and he “would do nothing to render it harm”, and that the French state’s stake in Renault “posed no problem at all” because the “French state does not impose in any way on Nissan.” Saikawa-san also noted that he had no intention of ridding Nissan of French/foreign employees.

Renault Director Martin Vial visited Japan with French officials including Emmanuel Moulin – chief of staff to Bruno Le Maire, who is French Minister of the Economy – to meet with Hiroto Saikawa and Japanese officials Wednesday and Thursday. This trip was first reported by Le Figaro in the early hours of Wednesday morning (15 Jan) Asia time, and the point of the trip was reportedly to discuss the changes in governance at the top of Renault which might be coming – i.e. a new chairman as the French state and Renault’s independent directors appear to have decided that another two months of detention for Carlos Ghosn is enough to warrant a change even if they still presume his innocence in the charges brought in Japan. They were also to inquire after Ghosn’s case, though that seemed to have been secondary.

As a sidebar to this trip, Bruno Le Maire came out Wednesday saying that the State had asked the Renault board to hold a board meeting to replace Ghosn, and said that the French state would leave it to Renault’s directors to choose, but also came out and said that Cie Generale Des Etablissement MIchelin (ML FP) CEO Jean-Dominique Senard would be a great choice (though other suggestions are that he might take the role of Chairman as others note that Renault Interim CEO Thierry Bolloré’s role could be made permanent). His comments about Mr. Senard included those suggesting that Mr. Senard adheres to certain ideas of the “social responsibilities” of the company – ideas which Mr. Le Maire shares.

Mr Le Maire also said this week…

“Nous souhaitons la pérennité de l’alliance. La question des participations au sein de l’alliance n’est pas sur la table.”

Another quote from an article which came out Saturday night at midnight Paris time was similar.

“Un rééquilibrage actionnarial, une modification des participations croisées entre Renault et Nissan n’est pas sur la table”, déclare Bruno Le Maire. “Nous sommes attachés au bon fonctionnement de cette alliance qui fait sa force.”

Both quotes say “we” (the French state) seek for the Alliance to continue functioning in a stable manner and changes of the crossholding relationship or ownership rates between the companies were not on the table.

The second appears to be a quote from the Journal du Dimanche (article linked above) which was probably conducted a day or two earlier – and it makes a reference to it having been conducted just after his return from Tokyo (it was not revealed earlier this week that he had made the trip with Mssrs. Vial and Moulin so this is something of a question mark).

All of this was out by Friday. It was all very measured and reassuring.

Then Sunday saw a bombshell dropped… again…

In the Nikkei and Bloomberg, it was revealed that the French visitors to Tokyo had informed Japanese officials of their intention to have Renault appoint the next chairman of Nissan (as apparently the Alliance agreement allows) and of the French State’s intention to seek to integrate Nissan and Renault under the umbrella of a single holding company.

This is interesting for three reasons…

A holding company where the two companies stay listed does nothing that the Alliance does not do now except put a single board in place on top of both companies. That would be a Dutch Foundation structure. A holding company where one of the two companies loses its listing (because it is taken over) would require one of those companies lose a set of shareholders.

A Dutch Foundation (which is effectively the same thing if the two companies stay listed) was an idea which a year ago in the previous kerfuffle last spring about merging was “not an option acceptable to the government” (Les Echos, 7-Mar-18)

This is, once again, the French state seeking to intervene in the governance of Nissan. That’s a no-no according to the Alliance Agreement as modified in December 2015.

This is widely reported in English, Japanese, and French on Sunday.

There is a conciliatory article in Bloomberg with a headline suggesting a French official (Le Maire) downplayed the French comments about a holding company, but that refers to the JDD article, which is probably days old and repeated the same comment he made publicly earlier this week, reported by Les Echos and Le Figaro about a lack of change in cross-holding, but a careful read of the timeline suggests his comments were made in France before someone leaked this to the Nikkei.

Saikawa-san was reported to have said this morning (Monday 21 Jan 2019) that he had not heard about this, but that now was not the time to consider revising capital ties.

One should note, once again, that this is not the CEO or independent Chairman of Renault saying this. It is not the board or Nissan saying this. It is the French state.

What does this all mean? What are the possibilities and ramifications? Read on…

Tracking Traffic/Chinese Express & Logistics is the hub for our research on China’s express parcels and logistics sectors. Tracking Traffic/Chinese Express & Logistics features analysis of monthly Chinese express and logistics data, notes from our conversations with industry players, and links to company and thematic notes.

This month’s issue covers the following topics:

December express parcel pricing fell by over 9% Y/Y. Average pricing per express parcel fell by 9.1% Y/Y, the worst decline since Q216 (excluding January/February figures distorted by the Lunar New Year holiday).

Express parcel revenue growth remained well below 20% last month. Weak pricing dragged sector revenue growth down to 17% in December, the 4th consecutive month of sub-20% growth.

Intra-city pricing (ie, local delivery) was strong in 2018. Relative to weak inter-city pricing (down 3.1% Y/Y in 2018), pricing for intra-city express shipments was firm, rising by 0.1% last year. In fact, average pricing for intra-city express shipments has risen in four of the last five years.

Underlying domestic transport demand remained firm in December. Although demand for inter-city express shipments appears to be moderating (from high levels), underlying transportation activity in December remained firm. The three modes of freight transport we track (rail, highway, air) in aggregate rose 6.6% Y/Y in December, even as the growth of air freight slowed.

We retain a negative view of China’s express industry’s fundamentals: demand growth is slowing and pricing for inter-city shipments appears to be falling faster than costs can be cut, leading to margin compression.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

LVS shot at Japan license enhanced by his role in lobbying US Justice Department’s reverse opinion on online gambling published last week. Read why in this insight.

Owning Sands China makes a strong case based on an ROCE analysis vs. the hospitality sector.

Owning both at current trade is one of the screaming bargains in the entire sector

Maoyan Entertainment (EPLUS HK) is the largest online movie ticketing service provider in China. The mid-point of Maoyan’s IPO price range of HK$14.8-20.4 per share implies a market value of $2.5 billion (HK$19.8 billion). Five cornerstone investors have agreed to buy $30 million or 10% of the offering at the IPO mid-point. The cornerstone investors are Imax China Holding (1970 HK), Hylink Digital Solutions, Prestige of The Sun, Welight Capital and Xiaomi Corp (1810 HK).

Our analysis suggests Maoyan is being offered at a material premium to a peer group of major Chinese internet companies. Due to challenging prospects faced by Maoyan as outlined in our previous research, we believe a premium rating is unwarranted. Consequently, we are inclined to sit out this IPO.

In this report, we provide an analysis of our pair trade idea between Amorepacific Group (002790 KS) and Shiseido Co Ltd (4911 JP). Our strategy will be to long Amorepacific Group (APG) and short Shiseido. As mentioned in our report, Korean Stubs Biweekly Sigma σ (#1): The Inaugural Edition, our base case strategy is to achieve gains of 8-10% on this pair trade. Our risk control is to close the trade if it generates 4-5% in combined losses. Cost of commissions are not included in the calculations and closing prices as of January 23rd are used in our pair trade. [Long APG – $0.5 million; Short Shiseido – $0.5 million for total of $1.0 million].

The following are the major catalysts that could boost APG shares higher than Shiseido shares within the next six to twelve months:

Amorepacific Group shares are extremely oversold and forming a base

THAAD is no longer an issue

Amorepacific Group’s NAV discount

Attractive relative valuations

Amorepacific’s new headquarters building distraction out of the way

Chinese tourists are coming back to Korea & slower growth rate of visitors to Japan

HET has grown its revenue at an impressive 73% CAGR from 2015 to 2017 and has been accompanied by gross margin expansion. The strong growth was supported by improving operating metrics such as an increase in student enrollment and average spending.

However, HET has been making losses and continues to spend more than its net billing. It is unclear whether HET had already achieved break even for its proprietary courses before expanding into its CCtalk platform. But from its high level of expenses, it seems unsustainable for HET to be relying heavily on the sales and marketing spending to get users to purchase online courses.

In this insight, we will look into the company’s financial and operating performance, regulatory risks regarding K12 courses, aggressive spending on sales and marketing, and the performance of other online education companies.

It seems that Panasonic Corp (6752 JP) is planning for long term growth by concentrating on building its relationship with Toyota Motor (7203 JP) while witnessing its key customer, Tesla Motors (TSLA US), drifts away. Toyota and Panasonic are in discussion to form a JV by 2020E with the aim of mass manufacturing EV batteries with possible benefits from cost-cutting efforts. We mentioned in Tesla Drifting Away Could Leave Panasonic Struggling to Gain Traction in China, that Tesla is looking for Chinese local players to source its factory in China upon the refusal from Panasonic to join hands with them in investing in their Chinese factory. Panasonic, which seemed to have felt the pressure mounting from Tesla potentially distancing itself from them, given that the majority of their battery sales are currently dependent on Tesla, is now preparing itself for the future by building long terms plans with its not-so-new customer, Toyota. Panasonic entered a partnership agreement with Toyota back in 2017 to develop EV batteries including their traditional prismatic batteries while also aiming to develop new battery solutions for the growing and evolving EV market. Thus, its plan to form a JV with Toyota by 2020E displays the confidence Panasonic has in Toyota while also indicating that the former is paving a path for some steady growth in its battery business being supported by one of the leading automakers.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In Q2 of FY19, the company has grown at 10.15% with revenue of INR 2.92 bn. EBITDA was INR 0.24 bn and EBITDA margin stood at 8.4% down by 167 bps, Net profit stood at 0.113 bn with margins at 3.87% down by 102 bps. Raw materials cost has increased in the first half of the year leading to lower margins.

The company has acquired 80% in Avadh Snacks, a Gujarat based snacks company for INR1.48 bn, we have discussed the implications in the report.

The stock is currently tradings at its 54x its FY18 EPS (Pre-acquisition) and 42x its FY19 EPS (post-acquisition), we believe the stock is currently overvalued but are positive on the long term prospects of the firm.

Orion sub is now falling 6% this morning. Holdco is currently down only 1.6%. They are currently above +2.2σ on a 20D MA. This is a 120D high. Price ratio wise, they are at 0.16549. This is a little above 120D mean. Holdco discount is now 50% to NAV.

Sub’s 6% fall this morning should be due to the market speculation that 4Q numbers may be worse than expected. But there are still more signals of improving fundamentals going forward. Weaker 4Q numbers do not indicate that Sub is entering a dull cycle business wise.

Current +2.2σ on a 20D MA is something rare to see. It should be rare even if we look much beyond 120 days. Given the market’s favorable sentiments on Sub’s mid-term outlook, current +2.2σ should be held here and reverted pretty soon. I’d go long Sub and short Holdco until +0~0.5σ.

Nexen Sub made a run yesterday. It climbed 6% yesterday. Holdco stayed flat with a 0.34% gain. This created a huge price divergence. The duo made nearly 2σ gap in one single day. They are now slightly below -1σ on a 20D MA. Holdco discount is 46% to NAV.

This much divergence in a single day is very rare for the Nexen duo. Sub’s stronger 4Q numbers should have been already priced in. Yesterday was more of a sentimental boost, thanks to HMG. Short-term wise, further price pushing up on Sub is unlikely.

The duo is well below 120D mean and 2Y mean on a 20D MA price ratio. Price divergence should be held back at the current level. I’d go for a quick reversion in favor of Holdco. Just, Holdco liquidity can be a major issue to many of us here.

The weight of the evidence suggests that the pullback has begun. This belief is supported by overbought conditions combined with the S&P 500, MSCI ACWI, and nearly all Sectors hitting logical resistance. Assuming the pullback continues, the next question is how deep or damaging will it be? In this report we highlight various market/technical indicators we are monitoring, as well as pointing out attractive set ups within Consumer Discretionary and Health Care Sectors.

The record net losses were mainly due to a seasonally weak quarter and recognition of the impairment in a subsidiary.

Q2 revenues did not slow down and management does not believe Q3 revenues will slow down.

EDU will not be negatively impacted by the new law from the Ministry of Education.

The P/E band suggests an upside of 27% and a price target of USD90.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In spite of a stellar quarter (Q3 FY19), we remain cautious on Zee Entertainment Enterprises (Z IN) and the prospects of broadcasters in India. Hindi GEC is consolidating, and most of the growth is likely to happen in regional channels which remain competitive. Global data suggests ad spends as a % of revenue for many broadcasters and cable operators has been disrupted and couple of year’s down the line, India should be no exception. Contrary to consensus, driven by millennials and non-affordability of second television, cord cutting in India could accelerate sooner than excepted. With an hyper competitive OTT landscape, uncertainty post TRAI Tariff implementations, in an industry suspect to easy value migration, the long term outlook for Zee Entertainment Enterprises (Z IN) and the broadcast Industry warrants attention. The only near term positive for the stock is the potential stake sale to a strategic partner, which is likely to keep the stock price buoyant but only in the near term.

Kepei Education (1890 HK) has raised US$112m at HK$2.48 per share, just slightly above the mid-end of the IPO price range. We have previously covered the insight in:

Our overall global outlook remains cautious and continued downward pressure on global equities remains our expectation. One bright spot is EM (more on this below), which continues to give us hope that global equities can bottom out. We provide a technical appraisal of major markets and highlight actionable setups within the global Utilities and Staples Sectors.

Next week promises to be a large catalyst driven week, with Apple Inc (AAPL US), NTT Docomo Inc (9437 JP) and Tesla Motors (TSLA US) expected to report results, among others. We have provided a list below of the key equity catalysts for next week as well as potential drivers for M&A deals and stubs. If you are interested in importing this directly into Outlook or have any further requests, please let us know.

Kabu.com shares were bid limit up all day long and closed at ¥462, which is a 10+ year closing high.

The idea is not a new one. The mobile telecommunications market in Japan is mature, and one of the few ways Type 1 telecom providers can grow is by adding content through the “pipes.”

KDDI already has an investment in an online banking 50/50 joint venture with MUFG called Jibun Bank (“My Bank” or “Myself Bank”) which it launched in 2008. KDDI established a smartphone-based asset management service with Daiwa Securities Group (8601 JP) just under a year ago, where KDDI owns 66.6% and Daiwa 33.4%. This was to attract younger customers to savings products accessible through an app in order to make those customers stickier over the long-term. KDDI also bought into Lifenet Insurance Co (7157 JP) in 2015 through a capital raise, and is now its largest shareholder at just over 25% (a decent (and recent) presentation of the company is here). About six months ago, KDDI injected ¥6bn (link is Japanese) into Japanese financial services company Finatext to help spark their new service of a ¥0 commission brokerage. I would note that Finatext and partner (now sub) NOWCAST launched an algorithmic personal asset management advisory service using for kabu.com Securities in 2016.

Owning a stake in a broker would go a long ways towards providing comprehensive financial services access by smartphone under a KDDI-owned profit umbrella.

Is a deal like this feasible? Reasonable? Likely?

The two companies’ first response was pretty standard. This was the version from KDDI:

KDDI is considering various possibilities in financial business with kabu.com Securities, however, there is no determined facts. [a better translation of the Japanese is “however… no decisions have been made”]

This is pretty standard in Japanese corporate “clarifications.” There are, in fact, no ‘decisions’ unless a board meeting has been convened and put their stamp on it.

But the Japanese market will look at a comment like this and figure that where there is smoke there is fire.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.