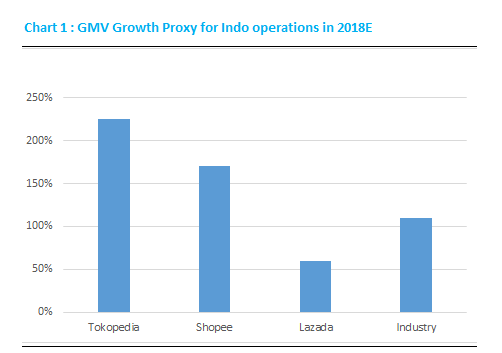

A big takeaway from our conversations with Indo e-commerce industry sources is that they vouch for Shopee’s (Sea Ltd’s (SE US) e-commerce arm) MS gains story in the country.

Indo e-commerce market has been enjoying super growth period (94% CAGR in 2015-18E) despite three major challenges (logistics, payment and highly subsidized market).

With SE’s fund raising a matter of when, not if (2H20 as most likely timetable), Shopee’s tremendous progress in key metrics (MS, take rate) provides comfort.

Assuming fair valuation of US$3 bn (vs. US$1.4 bn implied in SE’s ADR price) for Shopee, 12-mo PT for SE works out to be US$15.73/ADR, representing 43% upside potential.

In our Discover SZ/SH Connect series, we aim to help our investors understand the flow of northbound trades via the Shanghai Connect and Shenzhen Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by offshore investors in the past seven days.

We split the stocks eligible for the northbound trade into three groups: those with a market capitalization of above USD 5 billion, and those with a market capitalization between USD 1 billion and USD 5 billion.

Maoyan Entertainment, formerly Entertainment Plus (EPLUS HK), is the largest online movie ticketing service provider in China. According to press reports, Maoyan has started pre-marketing to raise $0.3 billion (down from earlier indication of $0.5-1.0 billion) through a Hong Kong IPO. Maoyan is backed by Beijing Enlight Media (300251 CH) (20.0% shareholder), Tencent Holdings (700 HK) (16.3% shareholder) and Meituan Dianping (3690 HK) (8.6% shareholder).

Maoyan is yet another proxy in the battle between Tencent and Alibaba Group Holding (BABA US). However, we believe that challenges abound for Maoyan and would be cautious about participating in the IPO.

While Rizap Group (2928 JP) has seen its share price crash and its CEO bow in apology after profit warnings and a plan to radically cut back on M&A, Jeans Mate Corp (7448 JP), which Rizap acquired last year, has quickly moved to modernise stores. It has just replaced its Shibuya store with a new concept called JEM that could mean the end of the Jeans Mate name altogether and posted its first operating profit in years. While many of Rizap’s acquisitions were dubious, Jeans Mate is one business that could be turned around into a modestly successful casual apparel retailer.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

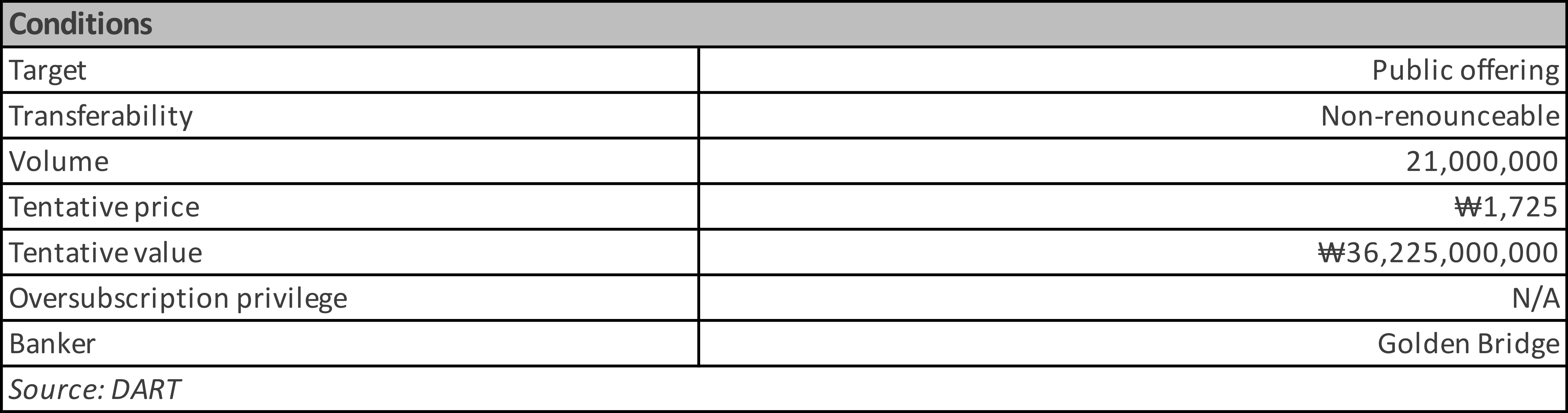

New Pride Corp (900100 KS) announced a ₩36.2bil rights offer. This is a public offering, so there won’t be subscription rights to trade. Pricing will be done as 3-day VWAP on Jan 9~11 at a 30% discount.

Supposedly, we can have ample opportunity to arb trade. This may be what the company is hoping. Simply, we wait until Jan 16~17 (subscription period) and see the spread. At this much discount, there must be a huge spread opening.

Proration risk can be much more annoying than a usual stockholder offering. In the previous public offering event by New Pride, subscription rate went as high as 370 to 1. It should be way much lower this time. But still this is risky enough.

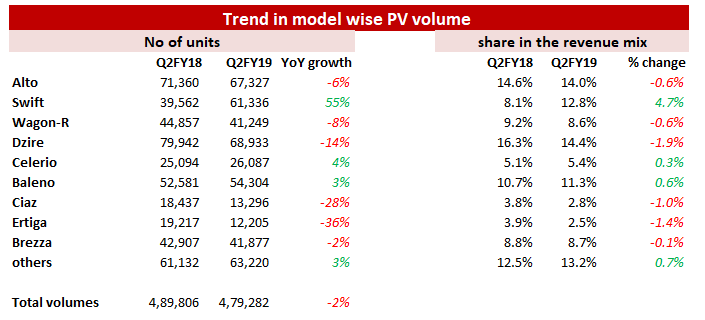

Maruti Suzuki’s Q2FY19 results were below our expectations. Sales grew by only 2% YoY in Q2FY19 led by a 3.7% increase in realization per unit. But the volumes declined by 1.5% YoY in the same period. We analyze the results.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Minnesotan Authorities declined to charge the founder of JD.

JD’s stock price has already plunged 52% in 2018. We believe JD is a defensive equity for portfolios, as the NASDAQ Composite just plunged 50% at most in the financial crisis of 2008.

Compared to 2014, today’s JD has a higher market share in the larger e-commerce market. However, JD’s stock price is at the same level as the first trading day in 2014.

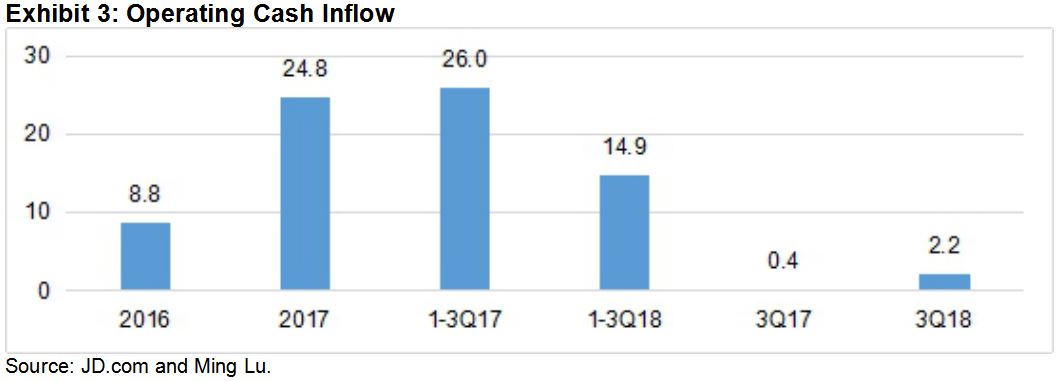

JD continued to generate operating cash inflows in 2018 as previous years despite of its zero net margins.

We are not concerned about the programmer layoff in December, as we believe JD overly invested in “hi-tech” that will not bring revenues in the near future.

Based on historical Price / GMV, we believe there is an upside of 270% for JD’s stock price.

Thanks to improved Korea-China relation, Opco (004320 KS) shares have nicely rebounded lately. Nongshim Holdco hasn’t caught up. This created the highest price ratio gap in 2 years. On a 20D MA, they are close to the mean. But on a 2 year mean, Holdco is currently and still severely undervalued.

Liquidity has played a major role in the recent price gap widening. At a rebounding cycle like this, liquidity must have been a huge factor. But it shouldn’t be too long until Holdco catches up. Opco has kinda drifted sideways for a while now. This should be time for Holdco to begin a catchup.

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of fully-diluted shares (current shares out + 26.826mm Options + ~2.1mm Award shares).

The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The other terms and conditions of this deal will be set out in the offer document which is expected to be despatched in mid-January 2019 (14-21 days from 28 December).

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.10 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

With the fourth quarter just a few hours from closing, CEO Elon Musk says he is keeping Tesla Motors (TSLA US) stores open until midnight so buyers can still get the coveted $7,500 tax credit on a new car before it gets cut in half January 1st.

This is interesting since Tesla started warning months ago that buyers need to order by October to be guaranteed delivery by December 31st since said demand was purportedly so hot the company couldn’t make its cars fast enough. It remains to be seen how many early birds rushed in, because as time passed that deadline has been extended through November and then December. I snapped this from Tesla’s website yesterday:

Tesla web site, December 30th

The takeaway here is that despite months of extraordianary sales efforts, price erosion, and declining production, Tesla’s inventory remains troublingly bloated, conditions I warned about in the third quarter as accelerating threats for the fourth quartert and likely through 2019 (see my report “Great Magic Trick Tesla; Now Do It Again,” 11/29/18).

Monthly sales trends for October and November also signalled that Tesla needs strong December performance if it still hopes to meet ambitious guidance for profits and free cash flow the company desparately needs to generate sufficiently sustainable cash flow to support operations plus hefty nearterm debt maturities, much less its burgeoning R&D and capex obligations where it’s already fallen behind.

Otherwise Tesla is likely to get really creative, again, with accounting and cash managment strategies to keep up the illusion of progress and stability.

It is our view, that come hell or high-water, in 2019, Tesla Motors (TSLA US) will establish itself as the pre-eminent large-cap growth stock. Those that are short would cover the position at a loss and those that are long are looking at another Apple Inc (AAPL US) or Amazon.com Inc (AMZN US) in the making. The ride may be volatile, but will be worth it.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We recently met with management to discuss the company’s 3Q results and outlook for the coming year.

There was clear disappointment that goals for 2018 had not been achieved: rising opex dampened the recovery in EBITDA, despite solid SSSg, the Hengqin Land sale is racked with yet further delays, and the key rental property is still untenanted. That said, we feel much of the frustration is due to positive outcomes on all front being just around the corner.

This note aims to give a brief update on the key pillars forming our thesis.

Hyosung Corporation (004800 KS) had fallen 16% just in two days. Holdco is now at a 50% discount to NAV. This is a 10%p drop from 10 days ago (Dec 19). Holdco price must have been overly corrected. The ongoing police investigation on Cho Hyun-joon’s alleged crime won’t lead to a delisting. 10%p drop in discount to NAV must be a price divergence, not a sensible price correction.

Trade volume remained steady. Local hedge funds led the selling on Dec 27. Even they changed their position the following day. No short selling spike has been seen either. Hyosung is one of the highest yielding div holdco stocks. Hyosung Capital liquidation and Anyang Plant revaluation would be another short-term plus.

I’d exploit this price divergence. It would soon revert to the Dec 19 discount level. It should at least stay at the peer average.

Just how will Harbin Electric Co Ltd H (1133 HK)‘s independent directors justify recommending an Offer to shareholders at a price which gave cash less cavalier than cash?

MYOB Group Ltd (MYO AU)‘s directors grudgingly yet understandably enter an agreed deal with KKR.

As previously discussed in Harbin Electric Expected To Be Privatised, Harbin Electric (HE) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption. The Offer price of $4.56/share, an 82.4% premium to last close, is bang in line with that paid by HEC in January this year for new domestic shares. The Offer price has been declared final.

Of note, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors (and the IFA) can justify recommending an Offer to shareholders at any price below the net cash/share, especially when the underlying business is profit-generating.

Dissension rights are available, however, there is no administrative guidance on the substantive as well as procedural rules as to how the “fair price” will be determined under PRC and HK Law.

Trading at a gross/annualised spread of 15%/28% assuming end-July completion, based on the average timeline for merger by absorption precedents. As HEC is only waiting for approval from independent H-shareholders suggests this transaction may complete earlier than precedents.

KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal. The Offer price assumes no full-year dividend is paid.

On balance, MYOB’s board has made the right decision to accept KKR’s reduced Offer. The argument that MYOB is a “known turnaround story” is challenged as cloud-based accounting software providers Xero Ltd (XRO AU)and Intuit Inc (INTU US) grab market share. This is also reflected in MYOB’s forecast 7% revenue growth in FY18 and follows a 10% decline in first-half profit, despite a 61% jump in online subscribers.

And there is justification for KKR’s lowering the Offer price: the ASX is down 10% since KKR’s initial tilt, the ASX technology index is off by ~14%, a basket of listed Aussie peers are down 17%, while Xero, the most comparable peer, is down ~20%. The Scheme Offer is at a ~27% premium to the estimated adjusted (for the ASX index) downside price of $2.68/share.

Bain was okay selling at $3.15/share to KKR and will be fine selling its remaining ~6.5% stake at $3.40. Presumably, MYOB sounded out the other major shareholders such as Fidelity, Yarra Funds Management, Vanguard etc as to their read on the revised $3.40 offer, before agreeing to the SIA with KKR.

If the markets avoid further declines, this deal will probably get up. If the markets rebound, the outcome is less assured. This Tuesday marks the beginning of a new year and a renewed mandate for investors to take risk, especially an agreed deal; but the current 5.3% annualised spread is tight.

The Ministry of Finance, the major shareholder of TMB, confirmed that both Krung Thai Bank Pub (KTB TB)and Thanachart Capital (TCAP TB)had engaged in merger talks with TMB. Considering an earlier KTB/TMB courtship failed, it is more likely, but by no means guaranteed, that the deal with Thanachart will happen. Bloomberg is also reporting that Thanachart and TMB want to do a deal before the next elections, which is less than two months away.

TMB is much bigger than Thanachart and therefore it may boil down to whether TMB wants to be the target or acquirer. In Athaporn Arayasantiparb, CFA‘s view, a deal with Thanachart would leave TMB as the acquirer rather than the target. But Thanachart’s management has a better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than Bank Of Ayudhya (BAY TB) and would not change the bank rankings; but it would give TMB a bigger presence in asset management, hire-purchase finance and a re-entry into the securities business.

Mando accounts for 45% of Halla’s NAV, which is currently trading at a 50% discount. Sanghyun Park believes the recent narrowing in the discount may be due to the hype attached to Mando-Hella Elec, which he believes is overdone; and recommends a short Holdco and long Mando. Using Sanghyun’s figures, I see the discount to NAV at 51%, 2STD above the 12-month average of ~47%.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Hotel Properties (HPL SP) (“HPL”) announced on Friday evening a significant change in its shareholdings relating to the HPL shares owned by 68 Holdings Pte Ltd.

The restructuring of shareholding did not come as a surprise and was within expectations.

Now, Wheelock holds only a significant minority interest of 22.53% and without a board seat in HPL. Wheelock’s influence in HPL has been reduced significantly. Without control, Wheelock’s investment in HPL is as good as any other non-strategic investment in quoted securities.

In the event that Wheelock Properties decides to sell its HPL shares, Mr Ong will be a likely buyer of the HPL shares. This will present a very good opportunity for Mr Ong to successfully privatise and delist HPL.

Prabhat Dairy Ltd’s quarterly result is in line with our expectation. In Q2 FY19, the company registered a growth of 8.53% YoY, EBITDA margin was 9.4% improving by 119 bps since the same period last year, EBITDA grew by 24.2% YOY; the profit margin was at 2.95% improving by 60 bps YoY, Net Income grew by 35.86% YOY. For more details about the company, please refer to our initiation report Prabhat Dairy Ltd – An Emerging Star in the Indian Milky Way. B2B business contributed to 70% of revenue and the remaining 30% was driven by B2C business. Value Added Products contributed to 25% of revenue in Q2FY19.

The stock is trading at 16.3x its TTM EPS, 13.8x its FY19F EPS. Margins have improved over the past quarters due to lower cost of raw materials, we expect raw materials to continue to be lower than their historic average in short term. Lower cost of raw material along with the improving contribution from B2C will lead to higher margins in medium to long term. The company also wants to increase its B2C contribution aggressively from the current 30% to 50% by 2020.

We will monitor the stock closely to firm up our views further, albeit we remain positive on the long-term prospects of the company.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

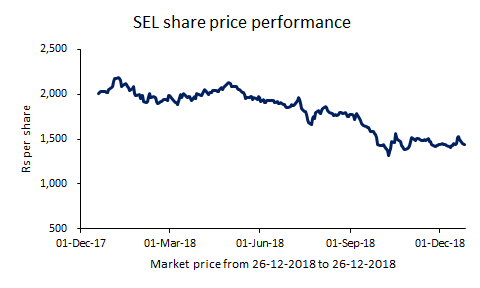

Swaraj Engines (SWE IN) (SEL)is primarily manufacturing diesel engines for fitment into Swaraj tractors manufactured by Mahindra & Mahindra Ltd. (M&M). The Company is also supplying engine components to SML Isuzu Ltd used in the assembly of commercial vehicle engines. SEL was started as a joint venture between Punjab Tractor Ltd (now acquired by M&M Ltd) and Kirloskar Oil Engines Ltd. M&M holds 33.3% stake in SEL and is its key client.

We are positive about the business because:

SEL’s growth is correlated with M&M’s tractor business growth. SEL supplies engines to the Swaraj division of M&M. M&M expects tractor growth to be around 12% YoY in FY19E. We forecast SEL’s tractor engine volumes will grow at a CAGR of 12% for FY18-21E.

The growth of the company is dependent on the monsoon and rural sentiments. We expect the profitability to improve with normal rainfall and government initiatives towards the rural sector. We expect the revenue/ EBITDA/ PAT CAGR for FY18-21E to be 14%/ 15%/ 14% respectively.

SEL is debt free and a cash generating company. It has a healthy and stable ROCE and ROE. SEL has increased its capacity from 75,000 engines in FY16 to 120,000 engines in FY18. We expect the capacity utilisation to reach 97% by FY20E from 90% in 1HFY19. SEL funds its capex through internal accruals. We forecast a capex of Rs 600 mn for FY19E to FY21E considering the requirement of the additional capacity, R&D and testing costs for new and higher HP engines & for upgradation of engines according to the TREM IV emission norms for >50 HP engines.

We initiate coverage on SEL with a fair value objective of Rs 1,655/- over the next 12 months. This represents a potential upside of 15% from the closing price of Rs 1,435/- (as on 26-12-2018). We arrive at the fair value by applying PE multiple of 18x to EPS of Rs 87/- to the year ending December-20E and add cash of Rs 82/- per share. While the business outlook is good, we think the upside in the share price is limited due to rich valuation.

Particulars (Rs mn) (Y/E March)

FY18

FY19E

FY20E

FY21E

Revenue

7,712

9,210

10,478

11,525

PAT

801

906

1,063

1,190

EPS (Rs)

64.5

74.8

87.6

98.1

PE (x)

22.3

19.2

16.4

14.6

Source: SEL Annual Report FY18, Trivikram Consultants Research as on 26-12-2018

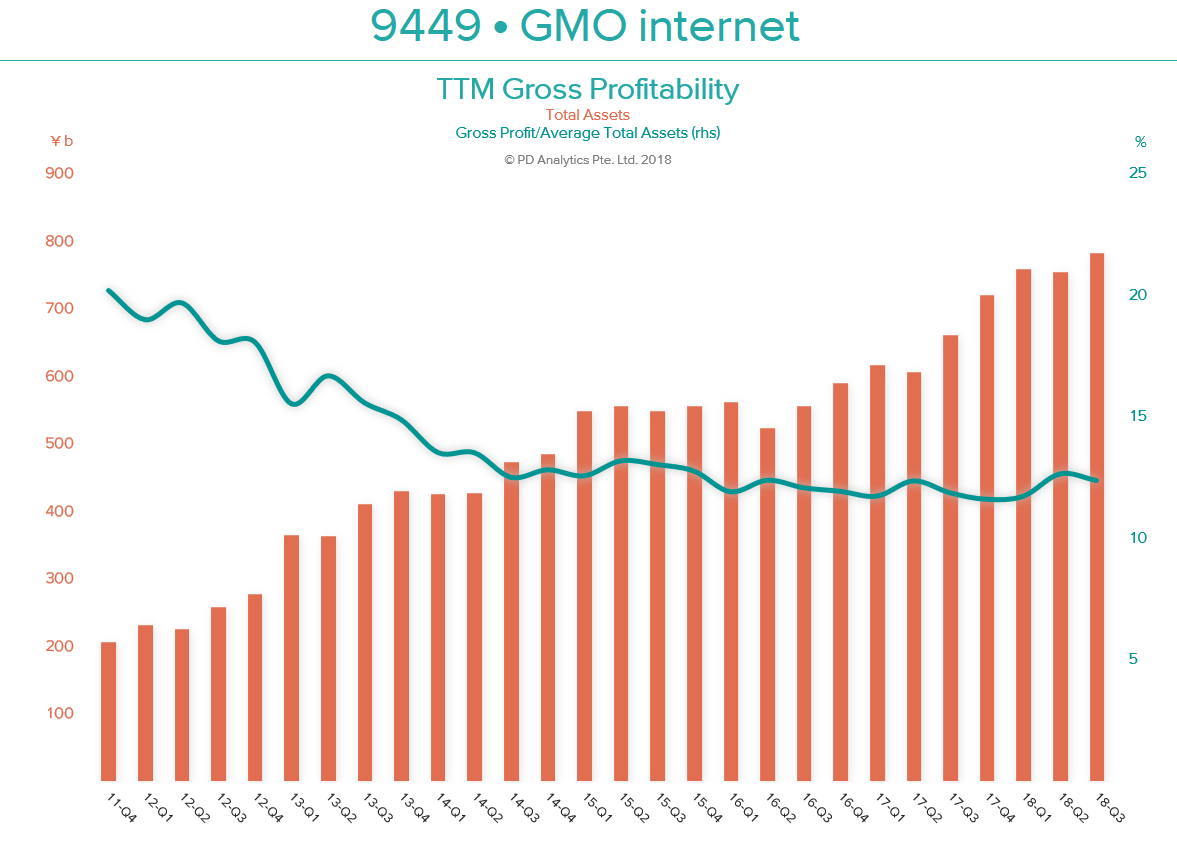

THE GMO INTERNET (9449 JP) STORY – GMO internet (GMO-i) has attracted much attention in the last eighteen months from an unusual trinity of value, activist and ‘cryptocurrency’ equity investors.

VALUE– Many traditional, but mostly foreign, value investors have seen the persistent negative difference between GMO-i’s market capitalisation and the value of the company’s holdings in its eight listed consolidated subsidiaries as an opportunity to invest in GMO-i with a considerable ‘margin of safety’.

ACTIVIST – Since July 2017, the activist investor, Oasis, has waged a so-far-unsuccessful campaign with the aim of improving GMO’s corporate governance, removing takeover defences, addressing a ‘secularly undervalued stock price we are not able to tolerate’ (sic), and redefining the role and influence of the company’s Chairman, President, Representative Director and largest shareholder, Masatoshi Kumagai.

‘CRYPTO!’ – In December 2017, GMO-i committed to spending more than ¥35b or 10% of non-current assets. The aim was threefold: to set up a bitcoin ‘mining’ headquarters in Switzerland (with the ‘mining’ operations being carried out at an undisclosed location in Scandinavia), to develop proprietary state-of-the-art 7nm-node ‘mining chips’, and, in due course, to sell GMO-branded and developed ‘mining’ machines. The move was hailed in the ‘crypto’ fraternity as GMO-i became the largest non-Chinese and the first well-established Internet conglomerate to make a major investment in ‘cryptocurrency’ infrastructure.

OUTSTANDING – Following the December 2017 announcement, trading volumes spiked into ‘Overtraded’ territory – as measured by our Volume Score. Many investors saw GMO-i shares as a safer way of gaining exposure to ‘cryptocurrencies’, even as the price of bitcoin began to subside. By early June 2018, GMO-i’s shares had reached a closing price of ¥3,020: up 157% from the low of the prior year and outperforming TOPIX by 135%. Whatever the primary driver of this outstanding performance, each of our trio of investor groups no doubt felt vindicated in their approach to the stock.

CRYPTO CLOSURE – On December 25th 2018, GMO-i’s shares reached a new 52-week low of ¥1,325, a decline of 56% from the June high. Year to date, GMO-i shares have now declined by 31%, underperforming TOPIX by nine percentage points. On the same day, GMO-i announced that the company would post an extraordinary ¥35.5b loss for the fourth quarter, incurring an impairment loss of ¥11.5b in relation to the closure of the Swiss ‘mining’ headquarters and a loss of ¥24b to cover the closure of the ‘mining chip’ and ‘mining machine’ development, manufacturing and sales businesses. GMO-i will continue to ‘mine’ bitcoin from its Tokyo headquarters and intends to relocate the ‘mining’ centre from Scandinavia to (sic) ‘a region that will allow us to secure cleaner and less expensive power supply, but we have not yet decided the details’. Unlisted subsidiary GMO Coin’s ‘cryptocurrency’ exchange will also continue to operate, and the previously-announced plans to launch a ¥-based ‘stablecoin’ in 2019 will proceed. In the two trading days following this announcement, the shares have recovered 13% to ¥1,505.

RAIDING THE LISTCO PIGGY BANK – As we shall relate, this is the second time since listing that GMO-i has written off a significant new business venture which the company had commenced only a short time before. In both cases, the company was forced to sell stakes in its listed consolidated subsidiaries to offset the resulting losses. On this occasion, the sale of shares in GMO Financial (7177 JP) (GMO-F) on September 25 2018, and GMO Payment Gateway (3769 JP) (GMO-PG) on December 17 2018, raised a combined ¥55.6b and, after the deduction of the yet-to-be-determined tax on the realised gains, should more than offset the ‘crypto’ losses. According to CFO Yasuda, any surplus from this exercise will be used to pay down debt. Also discussed below and in keeping with this GMO-i ‘MO’, in 2015, the company twice sold shares in its listed subsidiaries to ‘smooth out’ less-than-desirable operating results.

In the DETAIL section below we will cover the following topics:-

I: THE GMO-i TRACK RECORD – TOP-DOWN v. BOTTOM UP

BOTTOM LINE No. 1: NET INCOME

BOTTOM LINE No.2 – COMPREHENSIVE INCOME

II: THE GMO-i BUSINESS MODEL – THROWING JELLY AT THE WALL

III: THE GMO-i BALANCE SHEET – NOT SO HAPPY RETURNS

IV: THE GMO-i CASH FLOW – DEBT-FUNDED CASH PILE

V: THE GMO-i VALUATION – TWO METHODS > SAME RESULT

VALUATION METHOD No.1 – THE ‘LISTCO DISCOUNT’

VALUATION METHOD No.2 – RESIDUAL INCOME

CONCLUSION – For those unable or unwilling to read further, we conclude that GMO-i ‘rump’ is a grossly-overrated business. Despite having started and spun off several valuable GMO Group entities, CEO Kumagai bears responsibility for two decades of serial and very poorly-timed ‘mal-investments’. As a result, the stock market has, except for the ‘cryptocurrency’-induced frenzy of the first six months of 2018, historically not accorded GMO-i any premium for future growth, and has correctly looked beyond the ‘siren song’ of the ‘HoldCo discount’. According to the two valuation methodologies described below, the company is, however, fairly valued at the current share price of ¥1,460. Investors looking for a return to the market-implied 3% perpetual growth rate of mid–2018 are likely to be as disappointed as those wishing for BTC to triple from here.

Halla Holdings is falling nearly 5% today. Holdco said it’d give a ₩2,000 div per share. This is about 4.5% div yield at yesterday’s closing price. 5% drop today shouldn’t be much as an ex-dividend date price drop. Mando fell 5%. Mando was oversold relative to the other local auto stocks, particularly to Halla Holdings. They are still close to +1 σ on a 20D MA.

Mando-Hella Elec has been another reason behind Holdco’s valuation divergence against Mando lately. I believe Mando-Hella is being overhyped. Mando-Hella-caused divergence should no longer be effective. I expect ‘downwardly’ mean reversion from now on. I’d go short Holdco and long Mando at this point.

Good payout ratio, good growth in core profit, and strong long-term sales growth relative to its sector

Acquisition of 49% stake in a 30MW solar farm in Malaysia with a commercial operation date (COD) set for 1Q20 to support revenue growth

High volume of solar rooftop installation projects planned for Charoen Pokphand Foods Pub (CPF TB) and other private firms to boost GUNKUL’s construction revenue

Attractive at 19CE* PEG ratio of 0.5 relative to ASEAN Industry at 1.6

Risk: Lower than expected electricity demand, unfavorable weather conditions

We maintain a BUY rating on ASAP with new 2019E target price of Bt3.80 (from Bt6.50), derived from 19.6xPE, which is 1.0x PEG of earnings growth in 2019-20E.

The story:

Trimmed 2018-20F earnings forecast by 35%

Not a falling knife, but fallen angel

Potential disruptor in car rental industry

Expect a 20% CAGR for earnings in 2019-20E

Risks:

Contract termination of airport space leases

Participating in a highly competitive industry

Cash-flow management will be a challenge in a growth phase

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Thanks to improved Korea-China relation, Opco (004320 KS) shares have nicely rebounded lately. Nongshim Holdco hasn’t caught up. This created the highest price ratio gap in 2 years. On a 20D MA, they are close to the mean. But on a 2 year mean, Holdco is currently and still severely undervalued.

Liquidity has played a major role in the recent price gap widening. At a rebounding cycle like this, liquidity must have been a huge factor. But it shouldn’t be too long until Holdco catches up. Opco has kinda drifted sideways for a while now. This should be time for Holdco to begin a catchup.

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of fully-diluted shares (current shares out + 26.826mm Options + ~2.1mm Award shares).

The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The other terms and conditions of this deal will be set out in the offer document which is expected to be despatched in mid-January 2019 (14-21 days from 28 December).

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.10 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

With the fourth quarter just a few hours from closing, CEO Elon Musk says he is keeping Tesla Motors (TSLA US) stores open until midnight so buyers can still get the coveted $7,500 tax credit on a new car before it gets cut in half January 1st.

This is interesting since Tesla started warning months ago that buyers need to order by October to be guaranteed delivery by December 31st since said demand was purportedly so hot the company couldn’t make its cars fast enough. It remains to be seen how many early birds rushed in, because as time passed that deadline has been extended through November and then December. I snapped this from Tesla’s website yesterday:

Tesla web site, December 30th

The takeaway here is that despite months of extraordianary sales efforts, price erosion, and declining production, Tesla’s inventory remains troublingly bloated, conditions I warned about in the third quarter as accelerating threats for the fourth quartert and likely through 2019 (see my report “Great Magic Trick Tesla; Now Do It Again,” 11/29/18).

Monthly sales trends for October and November also signalled that Tesla needs strong December performance if it still hopes to meet ambitious guidance for profits and free cash flow the company desparately needs to generate sufficiently sustainable cash flow to support operations plus hefty nearterm debt maturities, much less its burgeoning R&D and capex obligations where it’s already fallen behind.

Otherwise Tesla is likely to get really creative, again, with accounting and cash managment strategies to keep up the illusion of progress and stability.

It is our view, that come hell or high-water, in 2019, Tesla Motors (TSLA US) will establish itself as the pre-eminent large-cap growth stock. Those that are short would cover the position at a loss and those that are long are looking at another Apple Inc (AAPL US) or Amazon.com Inc (AMZN US) in the making. The ride may be volatile, but will be worth it.

We recently met with management to discuss the company’s 3Q results and outlook for the coming year.

There was clear disappointment that goals for 2018 had not been achieved: rising opex dampened the recovery in EBITDA, despite solid SSSg, the Hengqin Land sale is racked with yet further delays, and the key rental property is still untenanted. That said, we feel much of the frustration is due to positive outcomes on all front being just around the corner.

This note aims to give a brief update on the key pillars forming our thesis.

THE GMO INTERNET (9449 JP) STORY – GMO internet (GMO-i) has attracted much attention in the last eighteen months from an unusual trinity of value, activist and ‘cryptocurrency’ equity investors.

VALUE– Many traditional, but mostly foreign, value investors have seen the persistent negative difference between GMO-i’s market capitalisation and the value of the company’s holdings in its eight listed consolidated subsidiaries as an opportunity to invest in GMO-i with a considerable ‘margin of safety’.

ACTIVIST – Since July 2017, the activist investor, Oasis, has waged a so-far-unsuccessful campaign with the aim of improving GMO’s corporate governance, removing takeover defences, addressing a ‘secularly undervalued stock price we are not able to tolerate’ (sic), and redefining the role and influence of the company’s Chairman, President, Representative Director and largest shareholder, Masatoshi Kumagai.

‘CRYPTO!’ – In December 2017, GMO-i committed to spending more than ¥35b or 10% of non-current assets. The aim was threefold: to set up a bitcoin ‘mining’ headquarters in Switzerland (with the ‘mining’ operations being carried out at an undisclosed location in Scandinavia), to develop proprietary state-of-the-art 7nm-node ‘mining chips’, and, in due course, to sell GMO-branded and developed ‘mining’ machines. The move was hailed in the ‘crypto’ fraternity as GMO-i became the largest non-Chinese and the first well-established Internet conglomerate to make a major investment in ‘cryptocurrency’ infrastructure.

OUTSTANDING – Following the December 2017 announcement, trading volumes spiked into ‘Overtraded’ territory – as measured by our Volume Score. Many investors saw GMO-i shares as a safer way of gaining exposure to ‘cryptocurrencies’, even as the price of bitcoin began to subside. By early June 2018, GMO-i’s shares had reached a closing price of ¥3,020: up 157% from the low of the prior year and outperforming TOPIX by 135%. Whatever the primary driver of this outstanding performance, each of our trio of investor groups no doubt felt vindicated in their approach to the stock.

CRYPTO CLOSURE – On December 25th 2018, GMO-i’s shares reached a new 52-week low of ¥1,325, a decline of 56% from the June high. Year to date, GMO-i shares have now declined by 31%, underperforming TOPIX by nine percentage points. On the same day, GMO-i announced that the company would post an extraordinary ¥35.5b loss for the fourth quarter, incurring an impairment loss of ¥11.5b in relation to the closure of the Swiss ‘mining’ headquarters and a loss of ¥24b to cover the closure of the ‘mining chip’ and ‘mining machine’ development, manufacturing and sales businesses. GMO-i will continue to ‘mine’ bitcoin from its Tokyo headquarters and intends to relocate the ‘mining’ centre from Scandinavia to (sic) ‘a region that will allow us to secure cleaner and less expensive power supply, but we have not yet decided the details’. Unlisted subsidiary GMO Coin’s ‘cryptocurrency’ exchange will also continue to operate, and the previously-announced plans to launch a ¥-based ‘stablecoin’ in 2019 will proceed. In the two trading days following this announcement, the shares have recovered 13% to ¥1,505.

RAIDING THE LISTCO PIGGY BANK – As we shall relate, this is the second time since listing that GMO-i has written off a significant new business venture which the company had commenced only a short time before. In both cases, the company was forced to sell stakes in its listed consolidated subsidiaries to offset the resulting losses. On this occasion, the sale of shares in GMO Financial (7177 JP) (GMO-F) on September 25 2018, and GMO Payment Gateway (3769 JP) (GMO-PG) on December 17 2018, raised a combined ¥55.6b and, after the deduction of the yet-to-be-determined tax on the realised gains, should more than offset the ‘crypto’ losses. According to CFO Yasuda, any surplus from this exercise will be used to pay down debt. Also discussed below and in keeping with this GMO-i ‘MO’, in 2015, the company twice sold shares in its listed subsidiaries to ‘smooth out’ less-than-desirable operating results.

In the DETAIL section below we will cover the following topics:-

I: THE GMO-i TRACK RECORD – TOP-DOWN v. BOTTOM UP

BOTTOM LINE No. 1: NET INCOME

BOTTOM LINE No.2 – COMPREHENSIVE INCOME

II: THE GMO-i BUSINESS MODEL – THROWING JELLY AT THE WALL

III: THE GMO-i BALANCE SHEET – NOT SO HAPPY RETURNS

IV: THE GMO-i CASH FLOW – DEBT-FUNDED CASH PILE

V: THE GMO-i VALUATION – TWO METHODS > SAME RESULT

VALUATION METHOD No.1 – THE ‘LISTCO DISCOUNT’

VALUATION METHOD No.2 – RESIDUAL INCOME

CONCLUSION – For those unable or unwilling to read further, we conclude that GMO-i ‘rump’ is a grossly-overrated business. Despite having started and spun off several valuable GMO Group entities, CEO Kumagai bears responsibility for two decades of serial and very poorly-timed ‘mal-investments’. As a result, the stock market has, except for the ‘cryptocurrency’-induced frenzy of the first six months of 2018, historically not accorded GMO-i any premium for future growth, and has correctly looked beyond the ‘siren song’ of the ‘HoldCo discount’. According to the two valuation methodologies described below, the company is, however, fairly valued at the current share price of ¥1,460. Investors looking for a return to the market-implied 3% perpetual growth rate of mid–2018 are likely to be as disappointed as those wishing for BTC to triple from here.

Halla Holdings is falling nearly 5% today. Holdco said it’d give a ₩2,000 div per share. This is about 4.5% div yield at yesterday’s closing price. 5% drop today shouldn’t be much as an ex-dividend date price drop. Mando fell 5%. Mando was oversold relative to the other local auto stocks, particularly to Halla Holdings. They are still close to +1 σ on a 20D MA.

Mando-Hella Elec has been another reason behind Holdco’s valuation divergence against Mando lately. I believe Mando-Hella is being overhyped. Mando-Hella-caused divergence should no longer be effective. I expect ‘downwardly’ mean reversion from now on. I’d go short Holdco and long Mando at this point.

Good payout ratio, good growth in core profit, and strong long-term sales growth relative to its sector

Acquisition of 49% stake in a 30MW solar farm in Malaysia with a commercial operation date (COD) set for 1Q20 to support revenue growth

High volume of solar rooftop installation projects planned for Charoen Pokphand Foods Pub (CPF TB) and other private firms to boost GUNKUL’s construction revenue

Attractive at 19CE* PEG ratio of 0.5 relative to ASEAN Industry at 1.6

Risk: Lower than expected electricity demand, unfavorable weather conditions

We maintain a BUY rating on ASAP with new 2019E target price of Bt3.80 (from Bt6.50), derived from 19.6xPE, which is 1.0x PEG of earnings growth in 2019-20E.

The story:

Trimmed 2018-20F earnings forecast by 35%

Not a falling knife, but fallen angel

Potential disruptor in car rental industry

Expect a 20% CAGR for earnings in 2019-20E

Risks:

Contract termination of airport space leases

Participating in a highly competitive industry

Cash-flow management will be a challenge in a growth phase

New Pride Corp (900100 KS) announced a ₩36.2bil rights offer. This is a public offering, so there won’t be subscription rights to trade. Pricing will be done as 3-day VWAP on Jan 9~11 at a 30% discount.

Supposedly, we can have ample opportunity to arb trade. This may be what the company is hoping. Simply, we wait until Jan 16~17 (subscription period) and see the spread. At this much discount, there must be a huge spread opening.

Proration risk can be much more annoying than a usual stockholder offering. In the previous public offering event by New Pride, subscription rate went as high as 370 to 1. It should be way much lower this time. But still this is risky enough.

Hyosung Corporation (004800 KS) had fallen 16% just in two days. Holdco is now at a 50% discount to NAV. This is a 10%p drop from 10 days ago (Dec 19). Holdco price must have been overly corrected. The ongoing police investigation on Cho Hyun-joon’s alleged crime won’t lead to a delisting. 10%p drop in discount to NAV must be a price divergence, not a sensible price correction.

Trade volume remained steady. Local hedge funds led the selling on Dec 27. Even they changed their position the following day. No short selling spike has been seen either. Hyosung is one of the highest yielding div holdco stocks. Hyosung Capital liquidation and Anyang Plant revaluation would be another short-term plus.

I’d exploit this price divergence. It would soon revert to the Dec 19 discount level. It should at least stay at the peer average.

Just how will Harbin Electric Co Ltd H (1133 HK)‘s independent directors justify recommending an Offer to shareholders at a price which gave cash less cavalier than cash?

MYOB Group Ltd (MYO AU)‘s directors grudgingly yet understandably enter an agreed deal with KKR.

As previously discussed in Harbin Electric Expected To Be Privatised, Harbin Electric (HE) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption. The Offer price of $4.56/share, an 82.4% premium to last close, is bang in line with that paid by HEC in January this year for new domestic shares. The Offer price has been declared final.

Of note, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors (and the IFA) can justify recommending an Offer to shareholders at any price below the net cash/share, especially when the underlying business is profit-generating.

Dissension rights are available, however, there is no administrative guidance on the substantive as well as procedural rules as to how the “fair price” will be determined under PRC and HK Law.

Trading at a gross/annualised spread of 15%/28% assuming end-July completion, based on the average timeline for merger by absorption precedents. As HEC is only waiting for approval from independent H-shareholders suggests this transaction may complete earlier than precedents.

KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal. The Offer price assumes no full-year dividend is paid.

On balance, MYOB’s board has made the right decision to accept KKR’s reduced Offer. The argument that MYOB is a “known turnaround story” is challenged as cloud-based accounting software providers Xero Ltd (XRO AU)and Intuit Inc (INTU US) grab market share. This is also reflected in MYOB’s forecast 7% revenue growth in FY18 and follows a 10% decline in first-half profit, despite a 61% jump in online subscribers.

And there is justification for KKR’s lowering the Offer price: the ASX is down 10% since KKR’s initial tilt, the ASX technology index is off by ~14%, a basket of listed Aussie peers are down 17%, while Xero, the most comparable peer, is down ~20%. The Scheme Offer is at a ~27% premium to the estimated adjusted (for the ASX index) downside price of $2.68/share.

Bain was okay selling at $3.15/share to KKR and will be fine selling its remaining ~6.5% stake at $3.40. Presumably, MYOB sounded out the other major shareholders such as Fidelity, Yarra Funds Management, Vanguard etc as to their read on the revised $3.40 offer, before agreeing to the SIA with KKR.

If the markets avoid further declines, this deal will probably get up. If the markets rebound, the outcome is less assured. This Tuesday marks the beginning of a new year and a renewed mandate for investors to take risk, especially an agreed deal; but the current 5.3% annualised spread is tight.

The Ministry of Finance, the major shareholder of TMB, confirmed that both Krung Thai Bank Pub (KTB TB)and Thanachart Capital (TCAP TB)had engaged in merger talks with TMB. Considering an earlier KTB/TMB courtship failed, it is more likely, but by no means guaranteed, that the deal with Thanachart will happen. Bloomberg is also reporting that Thanachart and TMB want to do a deal before the next elections, which is less than two months away.

TMB is much bigger than Thanachart and therefore it may boil down to whether TMB wants to be the target or acquirer. In Athaporn Arayasantiparb, CFA‘s view, a deal with Thanachart would leave TMB as the acquirer rather than the target. But Thanachart’s management has a better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than Bank Of Ayudhya (BAY TB) and would not change the bank rankings; but it would give TMB a bigger presence in asset management, hire-purchase finance and a re-entry into the securities business.

Mando accounts for 45% of Halla’s NAV, which is currently trading at a 50% discount. Sanghyun Park believes the recent narrowing in the discount may be due to the hype attached to Mando-Hella Elec, which he believes is overdone; and recommends a short Holdco and long Mando. Using Sanghyun’s figures, I see the discount to NAV at 51%, 2STD above the 12-month average of ~47%.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Hotel Properties (HPL SP) (“HPL”) announced on Friday evening a significant change in its shareholdings relating to the HPL shares owned by 68 Holdings Pte Ltd.

The restructuring of shareholding did not come as a surprise and was within expectations.

Now, Wheelock holds only a significant minority interest of 22.53% and without a board seat in HPL. Wheelock’s influence in HPL has been reduced significantly. Without control, Wheelock’s investment in HPL is as good as any other non-strategic investment in quoted securities.

In the event that Wheelock Properties decides to sell its HPL shares, Mr Ong will be a likely buyer of the HPL shares. This will present a very good opportunity for Mr Ong to successfully privatise and delist HPL.

Prabhat Dairy Ltd’s quarterly result is in line with our expectation. In Q2 FY19, the company registered a growth of 8.53% YoY, EBITDA margin was 9.4% improving by 119 bps since the same period last year, EBITDA grew by 24.2% YOY; the profit margin was at 2.95% improving by 60 bps YoY, Net Income grew by 35.86% YOY. For more details about the company, please refer to our initiation report Prabhat Dairy Ltd – An Emerging Star in the Indian Milky Way. B2B business contributed to 70% of revenue and the remaining 30% was driven by B2C business. Value Added Products contributed to 25% of revenue in Q2FY19.

The stock is trading at 16.3x its TTM EPS, 13.8x its FY19F EPS. Margins have improved over the past quarters due to lower cost of raw materials, we expect raw materials to continue to be lower than their historic average in short term. Lower cost of raw material along with the improving contribution from B2C will lead to higher margins in medium to long term. The company also wants to increase its B2C contribution aggressively from the current 30% to 50% by 2020.

We will monitor the stock closely to firm up our views further, albeit we remain positive on the long-term prospects of the company.

Swaraj Engines (SWE IN) (SEL)is primarily manufacturing diesel engines for fitment into Swaraj tractors manufactured by Mahindra & Mahindra Ltd. (M&M). The Company is also supplying engine components to SML Isuzu Ltd used in the assembly of commercial vehicle engines. SEL was started as a joint venture between Punjab Tractor Ltd (now acquired by M&M Ltd) and Kirloskar Oil Engines Ltd. M&M holds 33.3% stake in SEL and is its key client.

We are positive about the business because:

SEL’s growth is correlated with M&M’s tractor business growth. SEL supplies engines to the Swaraj division of M&M. M&M expects tractor growth to be around 12% YoY in FY19E. We forecast SEL’s tractor engine volumes will grow at a CAGR of 12% for FY18-21E.

The growth of the company is dependent on the monsoon and rural sentiments. We expect the profitability to improve with normal rainfall and government initiatives towards the rural sector. We expect the revenue/ EBITDA/ PAT CAGR for FY18-21E to be 14%/ 15%/ 14% respectively.

SEL is debt free and a cash generating company. It has a healthy and stable ROCE and ROE. SEL has increased its capacity from 75,000 engines in FY16 to 120,000 engines in FY18. We expect the capacity utilisation to reach 97% by FY20E from 90% in 1HFY19. SEL funds its capex through internal accruals. We forecast a capex of Rs 600 mn for FY19E to FY21E considering the requirement of the additional capacity, R&D and testing costs for new and higher HP engines & for upgradation of engines according to the TREM IV emission norms for >50 HP engines.

We initiate coverage on SEL with a fair value objective of Rs 1,655/- over the next 12 months. This represents a potential upside of 15% from the closing price of Rs 1,435/- (as on 26-12-2018). We arrive at the fair value by applying PE multiple of 18x to EPS of Rs 87/- to the year ending December-20E and add cash of Rs 82/- per share. While the business outlook is good, we think the upside in the share price is limited due to rich valuation.

Particulars (Rs mn) (Y/E March)

FY18

FY19E

FY20E

FY21E

Revenue

7,712

9,210

10,478

11,525

PAT

801

906

1,063

1,190

EPS (Rs)

64.5

74.8

87.6

98.1

PE (x)

22.3

19.2

16.4

14.6

Source: SEL Annual Report FY18, Trivikram Consultants Research as on 26-12-2018

Maruti Suzuki’s Q2FY19 results were below our expectations. Sales grew by only 2% YoY in Q2FY19 led by a 3.7% increase in realization per unit. But the volumes declined by 1.5% YoY in the same period. We analyze the results.

Improving asset turnover, good risk adjusted price momentum, and relatively strong analyst recommendations relative to its sector

Larger distribution channel through acquisition of DNA Retail Link to add 95 more stores to current 518 stores

New mobile product launches in 4Q18 and COM7’s focus on high margin products, such as Android smartphones, should support high earnings growth which was up 56% YoY in 3Q18

Attractive at a 19CE* PEG of 0.9 versus ASEAN sector at a PEG of 2.7

Risks: Lower-than-expected demand for new IT products, slower-than-expected store expansions

Tracking Traffic/Chinese Express & Logistics is the hub for our research on China’s express parcels and logistics sectors. Tracking Traffic/Chinese Express & Logistics features analysis of monthly Chinese express and logistics data, notes from our conversations with industry players, and links to company and thematic notes.

This month’s issue covers the following topics:

November express parcel pricing remained weak. Average pricing per express parcel fell by 7.8% Y/Y to just 11.06 RMB per piece. November’s average price represents a new all-time low for the industry, and November’s Y/Y decline was the steepest monthly decline in over two years (excluding Lunar New Year months, which tend to be distorted by the timing of the holiday).

Express parcel revenue growth dipped below 15% last month. Weak per-parcel pricing pulled express sector Y/Y revenue growth down to just 14.6% in November, the worst on record (again excluding distorted Lunar New Year comparisons). Chinese e-commerce demand has slowed and we suspect ‘O2O’ initiatives, under which online purchases are fulfilled via local stores, are also undermining express demand growth.

Intra-city pricing (ie, local delivery) remains firm relative to inter-city. Relative to weak inter-city express pricing (where ZTO Express (ZTO US) and the other listed express companies compete), pricing for local, intra-city express deliveries remained firm. In the first 11 months of 2018, express pricing rose 1.7% Y/Y versus a -2.9% decline in inter-city shipments (international pricing fell sharply, -14.5% Y/Y). Relatively firm pricing on local shipments may make it hard for local food delivery companies like Meituan Dianping (3690 HK) and Alibaba Group Holding (BABA US) ‘s ele.me to beat down unit operating costs.

Underlying domestic transport demand held up well again in November. Although demand for speedy, relatively expensive express service (and air freight) appears to be moderating, demand for rail and highway freight transport has held up well. The relative strength of rail and water transport (slow, cheap, industry-facing) versus express and air freight (fast, expensive, consumer-oriented) suggests a couple of things: a) upstream industrial activity is stronger than downstream retail activity and b) the people in charge of paying freight are shifting to cheaper modes of transport when possible.

We retain a negative view of China’s express industry’s fundamentals: demand growth is slowing and pricing appears to be falling faster than costs can be cut. Overall domestic transportation demand, however, remains solid and shows no signs of slowing.

It is our view, that come hell or high-water, in 2019, Tesla Motors (TSLA US) will establish itself as the pre-eminent large-cap growth stock. Those that are short would cover the position at a loss and those that are long are looking at another Apple Inc (AAPL US) or Amazon.com Inc (AMZN US) in the making. The ride may be volatile, but will be worth it.

We recently met with management to discuss the company’s 3Q results and outlook for the coming year.

There was clear disappointment that goals for 2018 had not been achieved: rising opex dampened the recovery in EBITDA, despite solid SSSg, the Hengqin Land sale is racked with yet further delays, and the key rental property is still untenanted. That said, we feel much of the frustration is due to positive outcomes on all front being just around the corner.

This note aims to give a brief update on the key pillars forming our thesis.

Hyosung Corporation (004800 KS) had fallen 16% just in two days. Holdco is now at a 50% discount to NAV. This is a 10%p drop from 10 days ago (Dec 19). Holdco price must have been overly corrected. The ongoing police investigation on Cho Hyun-joon’s alleged crime won’t lead to a delisting. 10%p drop in discount to NAV must be a price divergence, not a sensible price correction.

Trade volume remained steady. Local hedge funds led the selling on Dec 27. Even they changed their position the following day. No short selling spike has been seen either. Hyosung is one of the highest yielding div holdco stocks. Hyosung Capital liquidation and Anyang Plant revaluation would be another short-term plus.

I’d exploit this price divergence. It would soon revert to the Dec 19 discount level. It should at least stay at the peer average.

Just how will Harbin Electric Co Ltd H (1133 HK)‘s independent directors justify recommending an Offer to shareholders at a price which gave cash less cavalier than cash?

MYOB Group Ltd (MYO AU)‘s directors grudgingly yet understandably enter an agreed deal with KKR.

As previously discussed in Harbin Electric Expected To Be Privatised, Harbin Electric (HE) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption. The Offer price of $4.56/share, an 82.4% premium to last close, is bang in line with that paid by HEC in January this year for new domestic shares. The Offer price has been declared final.

Of note, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors (and the IFA) can justify recommending an Offer to shareholders at any price below the net cash/share, especially when the underlying business is profit-generating.

Dissension rights are available, however, there is no administrative guidance on the substantive as well as procedural rules as to how the “fair price” will be determined under PRC and HK Law.

Trading at a gross/annualised spread of 15%/28% assuming end-July completion, based on the average timeline for merger by absorption precedents. As HEC is only waiting for approval from independent H-shareholders suggests this transaction may complete earlier than precedents.

KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal. The Offer price assumes no full-year dividend is paid.

On balance, MYOB’s board has made the right decision to accept KKR’s reduced Offer. The argument that MYOB is a “known turnaround story” is challenged as cloud-based accounting software providers Xero Ltd (XRO AU)and Intuit Inc (INTU US) grab market share. This is also reflected in MYOB’s forecast 7% revenue growth in FY18 and follows a 10% decline in first-half profit, despite a 61% jump in online subscribers.

And there is justification for KKR’s lowering the Offer price: the ASX is down 10% since KKR’s initial tilt, the ASX technology index is off by ~14%, a basket of listed Aussie peers are down 17%, while Xero, the most comparable peer, is down ~20%. The Scheme Offer is at a ~27% premium to the estimated adjusted (for the ASX index) downside price of $2.68/share.

Bain was okay selling at $3.15/share to KKR and will be fine selling its remaining ~6.5% stake at $3.40. Presumably, MYOB sounded out the other major shareholders such as Fidelity, Yarra Funds Management, Vanguard etc as to their read on the revised $3.40 offer, before agreeing to the SIA with KKR.

If the markets avoid further declines, this deal will probably get up. If the markets rebound, the outcome is less assured. This Tuesday marks the beginning of a new year and a renewed mandate for investors to take risk, especially an agreed deal; but the current 5.3% annualised spread is tight.

The Ministry of Finance, the major shareholder of TMB, confirmed that both Krung Thai Bank Pub (KTB TB)and Thanachart Capital (TCAP TB)had engaged in merger talks with TMB. Considering an earlier KTB/TMB courtship failed, it is more likely, but by no means guaranteed, that the deal with Thanachart will happen. Bloomberg is also reporting that Thanachart and TMB want to do a deal before the next elections, which is less than two months away.

TMB is much bigger than Thanachart and therefore it may boil down to whether TMB wants to be the target or acquirer. In Athaporn Arayasantiparb, CFA‘s view, a deal with Thanachart would leave TMB as the acquirer rather than the target. But Thanachart’s management has a better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than Bank Of Ayudhya (BAY TB) and would not change the bank rankings; but it would give TMB a bigger presence in asset management, hire-purchase finance and a re-entry into the securities business.

Mando accounts for 45% of Halla’s NAV, which is currently trading at a 50% discount. Sanghyun Park believes the recent narrowing in the discount may be due to the hype attached to Mando-Hella Elec, which he believes is overdone; and recommends a short Holdco and long Mando. Using Sanghyun’s figures, I see the discount to NAV at 51%, 2STD above the 12-month average of ~47%.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Hotel Properties (HPL SP) (“HPL”) announced on Friday evening a significant change in its shareholdings relating to the HPL shares owned by 68 Holdings Pte Ltd.

The restructuring of shareholding did not come as a surprise and was within expectations.

Now, Wheelock holds only a significant minority interest of 22.53% and without a board seat in HPL. Wheelock’s influence in HPL has been reduced significantly. Without control, Wheelock’s investment in HPL is as good as any other non-strategic investment in quoted securities.

In the event that Wheelock Properties decides to sell its HPL shares, Mr Ong will be a likely buyer of the HPL shares. This will present a very good opportunity for Mr Ong to successfully privatise and delist HPL.