In this briefing:

- Dongzheng Auto Finance (东正汽车金融) Trading Update – Could Be Worth Setting up a Trade

- BabyTree(1761.HK) FY18 Results: E-Com Further Hit by ‘integration’ with Alibaba; India Foray Timely

- Japan Display: Deal to Raise JPY110bn from China-Taiwan Consortium and Japanese Investment Fund

- Haitian: Trade War Fears Fade, Full Stream Ahead

- Bilibili Placement: Momentum Bodes Well

1. Dongzheng Auto Finance (东正汽车金融) Trading Update – Could Be Worth Setting up a Trade

Dongzheng Automotive Finance (2718 HK) raised US$208m at a fixed price of HK$3.06 per share. We have covered the IPO extensively in:

- Dongzheng Auto Finance (东正汽车金融) Pre-IPO Review – Dependent on Dealership Network for Growth

- Dongzheng Auto Finance (东正汽车金融) IPO Review – Better off Buying the Parent

- Dongzheng Auto Finance (东正汽车金融) IPO Review – Relaunched at Lower Price

In this insight, we will update on the deal dynamics, implied valuation, and include a valuation sensitivity table.

2. BabyTree(1761.HK) FY18 Results: E-Com Further Hit by ‘integration’ with Alibaba; India Foray Timely

BabyTree (1761.HK)’s reported results for FY2018 continues to be impacted by the ‘shift in e-commerce strategy’ post collaboration with Alibaba Group Holding (BABA US) (also a key investor). China’s leading parenting community platform that went public in November 2018 has announced a revenue decline of 4% during 2H2018; its e-commerce revenues were down 70% as its being ‘integrated’ with Alibaba. This is expected to be completed by 2Q2019. While the details of the collaboration (and revenue share, if any) are not given, Management has stated that Alibaba will manage the back-end e-commerce at a reduced cost and better efficiency while it will ‘manage’ users. Despite the fall in revenues, gross profits were up 18% helped by growth in advertisement revenues which now account for 85% of the total. Advertising as a revenue source has limited long term growth and valuation potential compared to e-commerce. The stock is up 25% since results announcement on March 27th, likely enthused by Net profit for FY2018 at Rmb526.2 mn and EPS of Rmb0.29 (implied current Year P/E of 23x). Key risk will be failure to revive e-commerce revenues post ‘integration’.

BabyTree also announced its first global foray – it has invested USD8mn in Healofy, amongst the top 3 leading parenting apps in India currently. India’s online Parenting app segment has numerous players and revenue generation/growth may not be easy in the near term for Healofy. However, our analysis suggests that India’s overcrowded parenting app segment is now witnessing consolidation and this funding could probably help Healofy solidify its ranking amongst top 3 parenting platforms in India. In this context, BabyTree’s foray into India seems well timed. Healofy could potentially follow BabyTree’s operating model and fit into Alibaba Group Holding (BABA US) ‘s India e-commerce strategy (Refer our earlier report Alibaba’s India Game Plan – More than Meets the Eye; Investor Day Analysis (Part II) ).

In the detailed report that follows, we briefly comment on BabyTree’s reported 2018 results and also present a quick overview of India Parenting App segment – key players, investors and why we think it may be on a consolidation mode.

3. Japan Display: Deal to Raise JPY110bn from China-Taiwan Consortium and Japanese Investment Fund

- It was reported over the weekend that the troubled display supplier to iPhone maker Apple, Japan Display (JDI) has almost finalized a deal to raise more than JPY110bn (US$990m) from a China-Taiwan consortium and Japanese public-private fund INCJ Ltd.

- The China-Taiwan consortium is expected to secure some 50% stake in Japan Display while the top shareholder INCJ’s current stake of 25.3% is expected to be halved.

- The consortium is aiming to restructure JDI’s remaining debt payments of about JPY100bn from Apple for the construction of its plant while it also aims to procure parts for the latest iPhone. In addition, the consortium is also trying to modify a contract stipulating that Apple can seize plants if JDI’s cash and deposits fall below a certain amount.

- The consortium along with JDI is planning to build an OLED panel plant in China with JDI providing the technological know-how while the consortium partners invest in capital expenditures and equity.

- Japan Display has been struggling to navigate its display business due to the slowdown in iPhone sales, falling behind competition on OLED technology and facing stiff price competition from Chinese panel makers.

- We expect the proposed OLED plant in China could help the company stabilize its panel business with Chinese smartphone makers Huawei and Xiaomi who prefer to source panels locally from domestic panel makers such as BOE Technology and Tianma.

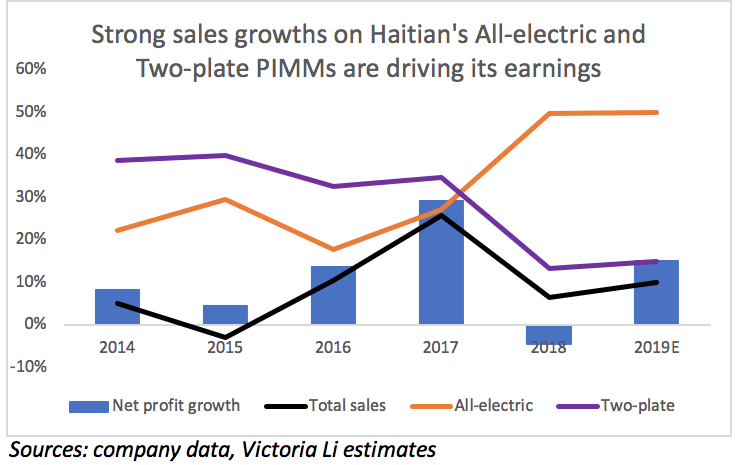

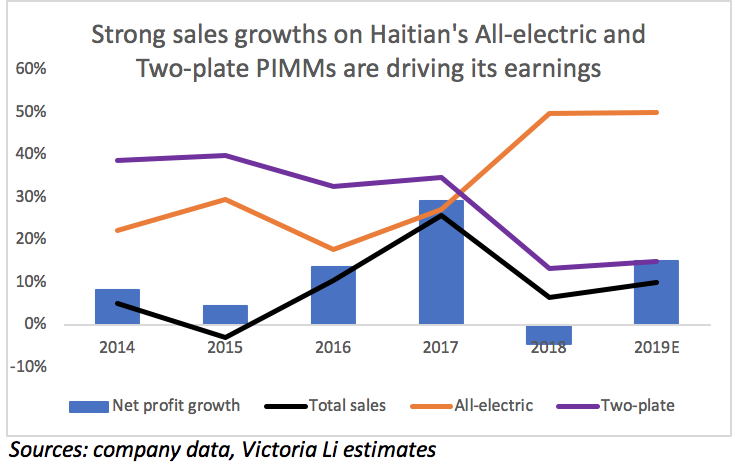

4. Haitian: Trade War Fears Fade, Full Stream Ahead

We expect Haitian’s margins go up in 2019, because 1) steel price in China is expected to decrease by 10% yoy with the re-balance of sector demand-supply, 2) Haitian’s newly launched third generation PIMM, and increasing sales propotion of high margin products, would improve the company’s overall margin.

Market demand is warming up in March, according to the management. The third generation PIMM is expected to trigger clients’ demand on upgrading their existing machines. High margin products, all-electric PIMM and large two-plate PIMM, would further increasing their sales and profit contribution. Overseas revenue growth would continue going faster than domestic revenue growth, with its new plants in Germany and Turkey coming on stream. We estimate Haitian’s net profit growth to reach 15% yoy in 2019E, vs. a 4% yoy decline in 2018.

Market concern on potential risk from Trade War, which had triggered Haitian’s valuation de-rating, should fade. As we expected, Haitian’s business wasn’t hurt by the Trade War in 2018, as the company has only 3% of overall revenue from US market. And the negotiations between US and China are on the right way to terminate the Trade War. Valuation re-rating might come with earnings improvement.

5. Bilibili Placement: Momentum Bodes Well

Bilibili announced a USD 300 million share placement and a USD 300 million convertible note placement after market close on Monday. This is the first major placement since Bilibili’s IPO in March 2018. In this insight, we will provide our thoughts on the deal and score the deal in our ECM Framework.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.