Yincheng International, a China Yangtze delta focused property developer, is raising up to USD 110 million to list on the Hong Kong Stock Exchange. In this note, we will cover the following topics:

Headwinds linger, but are beginning to lose velocity as consumers defy macro fears.

VIP slowdown should peak by Q3 and begin northward creep as bankrolls replenish.

Valuations today do not yet fully reflect the beginnings of a sector recovery.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Xinyi Energy Holdings Ltd (1671746D HK) has filed IPO prospectus once again to list its solar generation business that was spun-off from its parent company Xinyi Solar Holding Ltd. Xinyi Energy has 9 operational solar farms with a total capacity of ~950MW.

The company is set to acquire additional solar farms of 540MW capacity from its parent company in a separate transaction post IPO.

Xinyi Energy has not indicated the size and pricing of its offer, however, according to various media reports the company is expected to raise nearly HK$570M (around 12% of the previous offering of HK$4.5B). A significant portion of IPO proceeds is expected to be utilised towards upfront payment of 50% for acquiring solar farms from its parent company and the remainder for working capital and debt repayment. Although we have a positive view of the solar energy sector, the IPO pricing will determine our overall view of the company.

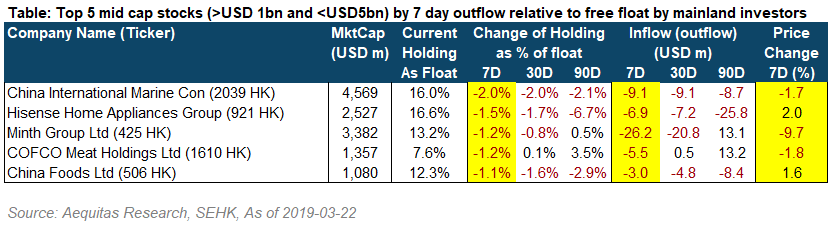

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this insight, we highlight the WH Group, which led the inflows last week.

Dongzheng Automotive Finance (2718 HK) (DAF) re-launched its IPO at a lower fixed price of HK$3.06 per share, expecting to raise about US$208m. We have covered the fundamentals and valuation of the company in:

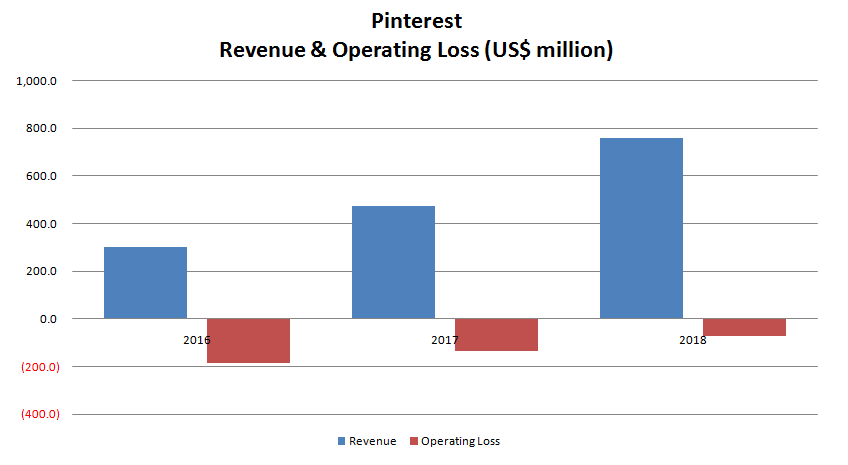

Pinterest Inc (PINS US), a leading digital media platform in the US, is getting ready for an IPO in the next several weeks. In our view, this is one of the most exciting global tech IPOs since the Elastic NV (ESTC US) IPO in October 2018. Pinterest has one of those rare combinations of strong sales growth, leading website brand awareness, loyal users network effect, and a clear path to profitability. Pinterest was most recently valued at $12.3 billion in private market valuation when it raised $150 million in 2017.

One of the attractive features about Pinterest is the fact that it has a very loyal user base among moms in the US. According to the company, about two thirds of its total user base are female, mostly in the US. Nearly 8 out of 10 moms (who are often the decision makers for purchasing household goods) and about half of the millennials in the US regularly use Pinterest.

The company has a very attractive income statement. Its revenue increased 59% CAGR from 2016 to 2018 and its operating losses have been declining nicely. Operating loss as a percentage of sales declined from 62.9% in 2016 to 9.9% in 2018.

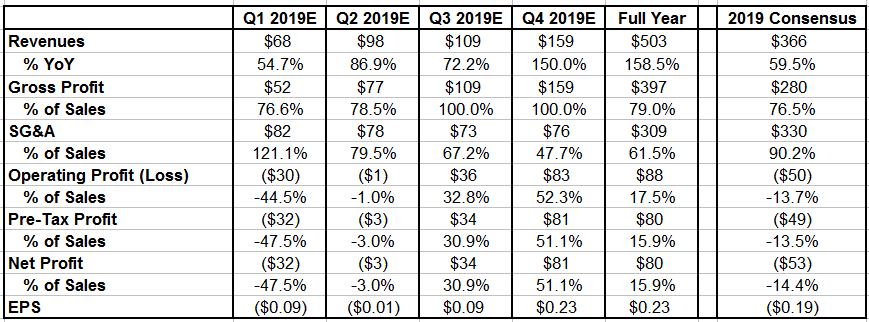

Strong Q1 to Come: We recently had a call with Amarin’s CEO, John Thero, and update our model with quarterly estimates. Q1 should see revenue growth of +55% YoY to $68m, an operating loss of -$30m, and EPS of -$0.09. Consensus is at $66m, -$38m, and -$0.12, respectively.

ACC Event Leads to Stock Drop: Amarin released “late-breaking” results from its Reduce-It trial at the American College of Cardiology (ACC) conference last Monday. While the data was considered “landmark” by doctors in attendance, the stock has fallen by nearly 14% since the event, showing a clear disconnect between the market and the medical community.

New Data Upgrades Risk Reduction to 30% & Shows Strong Prevention of CVD Recurrence: The key data at the ACC showed that Vascepa has a 30% relative risk reduction (RRR) rate for total CVD events (initially, it was 25% RRR rate for “major adverse” CVD events). Additionally, it was discovered that Vascepa reduced secondary CVD events by 32%, third events by 31%, and fourth events by 48%. 50% of patients who have experienced a cardiovascular event have a recurrence within one year, while 75% have recurrences within three years.

New Data Should Fast-Track Label Expansion & Impact Earnings Significantly: Doctors on a panel discussion after Amarin’s presentation at the ACC were dazzled by the data, saying that it will change the way CVD is treated in the US. We got the sense that this should lead to the FDA giving Vascepa “fast-track” (6 months vs regular 10 months) treatment for label expansion, which will surely lead to higher revenues this year and an expanded market henceforth.

New Prescriptions up 62% YTD: Amarin’s CEO, John Thero, told us he has more talks with doctors about Vascepa these days than he does with investors, which highlights increasing interest in the US medical community over Vascepa and explains the new prescription growth of +62% year-to-date. Successful label expansion by the FDA should widen Vascepa’s addressable market by nearly 20x.

Our Talks With CEO Point to a Strong Q1: The first quarter is seasonally slow, but our impressions from our talk with CEO John Thero is that the company is most likely outperforming its internal targets for Q1 growth. Amarin assumes 53% sales growth for the full year, but has stated that Q1 should be “seasonally slower”. Weekly prescription data show that Vascepa is growing over 50% in the seasonally slow Q1. Sales should pick up from Q2 and surge in the usual peak season of Q4.

2019 Revenues should Reach $500m (+120% YoY): We see 2019 revenues of $503m, with operating profit of $88m (17.5% operating margin) and EPS of $0.23. Consensus sees sales of $363m (guidance is at $350m), with an operating loss of -$58m and EPS of -$0.17.

Buyout Possibilities Remain High: We continue to see Amarin as one of the most attractive buy-out candidates among big pharma companies in the CVD field. Because Vascepa is a treatment taken in conjunction with statin medication like Lipitor, Pfizer appears like the most likely suitor, although there many others.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Headwinds linger, but are beginning to lose velocity as consumers defy macro fears.

VIP slowdown should peak by Q3 and begin northward creep as bankrolls replenish.

Valuations today do not yet fully reflect the beginnings of a sector recovery.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this insight, we highlight the WH Group, which led the inflows last week.

Dongzheng Automotive Finance (2718 HK) (DAF) re-launched its IPO at a lower fixed price of HK$3.06 per share, expecting to raise about US$208m. We have covered the fundamentals and valuation of the company in:

Pinterest Inc (PINS US), a leading digital media platform in the US, is getting ready for an IPO in the next several weeks. In our view, this is one of the most exciting global tech IPOs since the Elastic NV (ESTC US) IPO in October 2018. Pinterest has one of those rare combinations of strong sales growth, leading website brand awareness, loyal users network effect, and a clear path to profitability. Pinterest was most recently valued at $12.3 billion in private market valuation when it raised $150 million in 2017.

One of the attractive features about Pinterest is the fact that it has a very loyal user base among moms in the US. According to the company, about two thirds of its total user base are female, mostly in the US. Nearly 8 out of 10 moms (who are often the decision makers for purchasing household goods) and about half of the millennials in the US regularly use Pinterest.

The company has a very attractive income statement. Its revenue increased 59% CAGR from 2016 to 2018 and its operating losses have been declining nicely. Operating loss as a percentage of sales declined from 62.9% in 2016 to 9.9% in 2018.

Strong Q1 to Come: We recently had a call with Amarin’s CEO, John Thero, and update our model with quarterly estimates. Q1 should see revenue growth of +55% YoY to $68m, an operating loss of -$30m, and EPS of -$0.09. Consensus is at $66m, -$38m, and -$0.12, respectively.

ACC Event Leads to Stock Drop: Amarin released “late-breaking” results from its Reduce-It trial at the American College of Cardiology (ACC) conference last Monday. While the data was considered “landmark” by doctors in attendance, the stock has fallen by nearly 14% since the event, showing a clear disconnect between the market and the medical community.

New Data Upgrades Risk Reduction to 30% & Shows Strong Prevention of CVD Recurrence: The key data at the ACC showed that Vascepa has a 30% relative risk reduction (RRR) rate for total CVD events (initially, it was 25% RRR rate for “major adverse” CVD events). Additionally, it was discovered that Vascepa reduced secondary CVD events by 32%, third events by 31%, and fourth events by 48%. 50% of patients who have experienced a cardiovascular event have a recurrence within one year, while 75% have recurrences within three years.

New Data Should Fast-Track Label Expansion & Impact Earnings Significantly: Doctors on a panel discussion after Amarin’s presentation at the ACC were dazzled by the data, saying that it will change the way CVD is treated in the US. We got the sense that this should lead to the FDA giving Vascepa “fast-track” (6 months vs regular 10 months) treatment for label expansion, which will surely lead to higher revenues this year and an expanded market henceforth.

New Prescriptions up 62% YTD: Amarin’s CEO, John Thero, told us he has more talks with doctors about Vascepa these days than he does with investors, which highlights increasing interest in the US medical community over Vascepa and explains the new prescription growth of +62% year-to-date. Successful label expansion by the FDA should widen Vascepa’s addressable market by nearly 20x.

Our Talks With CEO Point to a Strong Q1: The first quarter is seasonally slow, but our impressions from our talk with CEO John Thero is that the company is most likely outperforming its internal targets for Q1 growth. Amarin assumes 53% sales growth for the full year, but has stated that Q1 should be “seasonally slower”. Weekly prescription data show that Vascepa is growing over 50% in the seasonally slow Q1. Sales should pick up from Q2 and surge in the usual peak season of Q4.

2019 Revenues should Reach $500m (+120% YoY): We see 2019 revenues of $503m, with operating profit of $88m (17.5% operating margin) and EPS of $0.23. Consensus sees sales of $363m (guidance is at $350m), with an operating loss of -$58m and EPS of -$0.17.

Buyout Possibilities Remain High: We continue to see Amarin as one of the most attractive buy-out candidates among big pharma companies in the CVD field. Because Vascepa is a treatment taken in conjunction with statin medication like Lipitor, Pfizer appears like the most likely suitor, although there many others.

Lasertec hit a new high in the semiconductor stock rally that followed Micron Technology’s March 20 earnings call. On Friday, March 22 (March 21 was a holiday in Japan), Lasertec was up 8.4% to ¥4,900. At this price, the shares are selling at 42x our EPS estimate for FY Jun-19, 36x our estimate for FY Jun-20 and 31x our estimate for FY Jun-21. On a 5-year view, earnings growth could bring the projected P/E multiple down to 21x, in our estimation.

Following strong 1H results, management left FY Jun-19 sales and profit guidance unchanged, but raised semiconductor-related orders guidance by 13% while cutting orders guidance for FPD-related and other products by nearly 40%. Total new orders guidance was raised from ¥37 billion to ¥39 billion, compared with sales guidance of ¥28 billion, implying an increase in the order backlog from ¥39.9 billion to ¥50.9 billion.

With this in mind, we have raised our sales and profit estimates for FY Jun-20 and added new, higher estimates for FY Jun-21 and beyond. Rising demand for EUV mask blank and mask defect inspection equipment should drive an increase in total sales from ¥29 billion this fiscal year to ¥38 billion in FY Jun-21, and approximately ¥50 billion in FY Jun-23. Over the same period, operating profit should rise from ¥7.0 billion to ¥9.5 billion, and then to approximately ¥14 billion.

Risks for investors include the potential delay or reduction of orders and shipments (as just happened with FPD inspection equipment), high volatility in quarterly orders, sales and profits, and extended valuations.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Dongzheng Automotive Finance (2718 HK) (DAF) re-launched its IPO at a lower fixed price of HK$3.06 per share, expecting to raise about US$208m. We have covered the fundamentals and valuation of the company in:

Pinterest Inc (PINS US), a leading digital media platform in the US, is getting ready for an IPO in the next several weeks. In our view, this is one of the most exciting global tech IPOs since the Elastic NV (ESTC US) IPO in October 2018. Pinterest has one of those rare combinations of strong sales growth, leading website brand awareness, loyal users network effect, and a clear path to profitability. Pinterest was most recently valued at $12.3 billion in private market valuation when it raised $150 million in 2017.

One of the attractive features about Pinterest is the fact that it has a very loyal user base among moms in the US. According to the company, about two thirds of its total user base are female, mostly in the US. Nearly 8 out of 10 moms (who are often the decision makers for purchasing household goods) and about half of the millennials in the US regularly use Pinterest.

The company has a very attractive income statement. Its revenue increased 59% CAGR from 2016 to 2018 and its operating losses have been declining nicely. Operating loss as a percentage of sales declined from 62.9% in 2016 to 9.9% in 2018.

Strong Q1 to Come: We recently had a call with Amarin’s CEO, John Thero, and update our model with quarterly estimates. Q1 should see revenue growth of +55% YoY to $68m, an operating loss of -$30m, and EPS of -$0.09. Consensus is at $66m, -$38m, and -$0.12, respectively.

ACC Event Leads to Stock Drop: Amarin released “late-breaking” results from its Reduce-It trial at the American College of Cardiology (ACC) conference last Monday. While the data was considered “landmark” by doctors in attendance, the stock has fallen by nearly 14% since the event, showing a clear disconnect between the market and the medical community.

New Data Upgrades Risk Reduction to 30% & Shows Strong Prevention of CVD Recurrence: The key data at the ACC showed that Vascepa has a 30% relative risk reduction (RRR) rate for total CVD events (initially, it was 25% RRR rate for “major adverse” CVD events). Additionally, it was discovered that Vascepa reduced secondary CVD events by 32%, third events by 31%, and fourth events by 48%. 50% of patients who have experienced a cardiovascular event have a recurrence within one year, while 75% have recurrences within three years.

New Data Should Fast-Track Label Expansion & Impact Earnings Significantly: Doctors on a panel discussion after Amarin’s presentation at the ACC were dazzled by the data, saying that it will change the way CVD is treated in the US. We got the sense that this should lead to the FDA giving Vascepa “fast-track” (6 months vs regular 10 months) treatment for label expansion, which will surely lead to higher revenues this year and an expanded market henceforth.

New Prescriptions up 62% YTD: Amarin’s CEO, John Thero, told us he has more talks with doctors about Vascepa these days than he does with investors, which highlights increasing interest in the US medical community over Vascepa and explains the new prescription growth of +62% year-to-date. Successful label expansion by the FDA should widen Vascepa’s addressable market by nearly 20x.

Our Talks With CEO Point to a Strong Q1: The first quarter is seasonally slow, but our impressions from our talk with CEO John Thero is that the company is most likely outperforming its internal targets for Q1 growth. Amarin assumes 53% sales growth for the full year, but has stated that Q1 should be “seasonally slower”. Weekly prescription data show that Vascepa is growing over 50% in the seasonally slow Q1. Sales should pick up from Q2 and surge in the usual peak season of Q4.

2019 Revenues should Reach $500m (+120% YoY): We see 2019 revenues of $503m, with operating profit of $88m (17.5% operating margin) and EPS of $0.23. Consensus sees sales of $363m (guidance is at $350m), with an operating loss of -$58m and EPS of -$0.17.

Buyout Possibilities Remain High: We continue to see Amarin as one of the most attractive buy-out candidates among big pharma companies in the CVD field. Because Vascepa is a treatment taken in conjunction with statin medication like Lipitor, Pfizer appears like the most likely suitor, although there many others.

Lasertec hit a new high in the semiconductor stock rally that followed Micron Technology’s March 20 earnings call. On Friday, March 22 (March 21 was a holiday in Japan), Lasertec was up 8.4% to ¥4,900. At this price, the shares are selling at 42x our EPS estimate for FY Jun-19, 36x our estimate for FY Jun-20 and 31x our estimate for FY Jun-21. On a 5-year view, earnings growth could bring the projected P/E multiple down to 21x, in our estimation.

Following strong 1H results, management left FY Jun-19 sales and profit guidance unchanged, but raised semiconductor-related orders guidance by 13% while cutting orders guidance for FPD-related and other products by nearly 40%. Total new orders guidance was raised from ¥37 billion to ¥39 billion, compared with sales guidance of ¥28 billion, implying an increase in the order backlog from ¥39.9 billion to ¥50.9 billion.

With this in mind, we have raised our sales and profit estimates for FY Jun-20 and added new, higher estimates for FY Jun-21 and beyond. Rising demand for EUV mask blank and mask defect inspection equipment should drive an increase in total sales from ¥29 billion this fiscal year to ¥38 billion in FY Jun-21, and approximately ¥50 billion in FY Jun-23. Over the same period, operating profit should rise from ¥7.0 billion to ¥9.5 billion, and then to approximately ¥14 billion.

Risks for investors include the potential delay or reduction of orders and shipments (as just happened with FPD inspection equipment), high volatility in quarterly orders, sales and profits, and extended valuations.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Theme of the week: Block trades/Placements + news flow on upcoming IPOs

Starting with placements, the shareholders of Wuxi Biologics (Cayman) Inc (2269 HK) are back on the market again to sell some shares. They been quite consistent with the selling and our team have covered the company the IPO each of the placements. Wisetech Global (WTC AU) and Platinum Asset Management (PTM AU) also had blocks that were sold earlier this week. The former did excceedingly well post-placement, currently more than 10% above its deal price while the latter had struggled as a result of Kerr and his ex-wife selling a portion of their shares in the company.

As for upcoming IPOs, Hong Kong ECM activity is ramping up. Megvii, the Chinese AI startup is looking to list in Hong Kong or US whereas China Feihe (FEIHE HK) is said to be revisit its US$1bn HK IPO. Ke Yan, CFA, FRM has covered the latter in this insight almost two years ago.

We also heard that Frontage had already met investors and Ke Yan, CFA, FRM has provided preliminary thoughts on valuation in:

Mulsanne Group (previously known as Alpha Smart (GXG)), Xinyi Energy Holdings, CMGE Tech, and 360 ludashi (鲁大师) re-filed their draft prospectuses. We have covered Mulsanne and Xinyi Energy in:

360 ludashi’s previous filing indicated that its IPO deal size will be small (<US$100m). However, the updated financials shown an almost 50% YoY PATMI growth which could put its IPO at a borderline deal size of US$100m if growth maintains at 50%.

In the U.S, Yunji Inc. (YJ US) filed for a US$200m IPO. The company runs a Chinese e-commerce site that uses a social platform to promote its products. We will be writing an early note on the company next week.

In Singapore, Eagle Hospitality REIT is said to have started investor education for its IPO while Lendlease is planning to raise up to US$500m for its retail REIT according to media reports.

In other ASEAN markets, there are also a handful of IPOs to watch out for.

In Indonesia, Lion Air is said to be targeting US$1bn listing in the third quarter of this year and it is starting to gauge investor interest. MAP Actif has already started pre-marketing its IPO.

In Thailand, Kerry Express Thailand is said to have hired banks to prepare for a >US$100m IPO.

In Malaysia, QSR Brands (QSR MY) has started to pre-market for its US$500m IPO. Sumeet Singh had previously written an early note:

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Pinterest Inc (PINS US), a leading digital media platform in the US, is getting ready for an IPO in the next several weeks. In our view, this is one of the most exciting global tech IPOs since the Elastic NV (ESTC US) IPO in October 2018. Pinterest has one of those rare combinations of strong sales growth, leading website brand awareness, loyal users network effect, and a clear path to profitability. Pinterest was most recently valued at $12.3 billion in private market valuation when it raised $150 million in 2017.

One of the attractive features about Pinterest is the fact that it has a very loyal user base among moms in the US. According to the company, about two thirds of its total user base are female, mostly in the US. Nearly 8 out of 10 moms (who are often the decision makers for purchasing household goods) and about half of the millennials in the US regularly use Pinterest.

The company has a very attractive income statement. Its revenue increased 59% CAGR from 2016 to 2018 and its operating losses have been declining nicely. Operating loss as a percentage of sales declined from 62.9% in 2016 to 9.9% in 2018.

Strong Q1 to Come: We recently had a call with Amarin’s CEO, John Thero, and update our model with quarterly estimates. Q1 should see revenue growth of +55% YoY to $68m, an operating loss of -$30m, and EPS of -$0.09. Consensus is at $66m, -$38m, and -$0.12, respectively.

ACC Event Leads to Stock Drop: Amarin released “late-breaking” results from its Reduce-It trial at the American College of Cardiology (ACC) conference last Monday. While the data was considered “landmark” by doctors in attendance, the stock has fallen by nearly 14% since the event, showing a clear disconnect between the market and the medical community.

New Data Upgrades Risk Reduction to 30% & Shows Strong Prevention of CVD Recurrence: The key data at the ACC showed that Vascepa has a 30% relative risk reduction (RRR) rate for total CVD events (initially, it was 25% RRR rate for “major adverse” CVD events). Additionally, it was discovered that Vascepa reduced secondary CVD events by 32%, third events by 31%, and fourth events by 48%. 50% of patients who have experienced a cardiovascular event have a recurrence within one year, while 75% have recurrences within three years.

New Data Should Fast-Track Label Expansion & Impact Earnings Significantly: Doctors on a panel discussion after Amarin’s presentation at the ACC were dazzled by the data, saying that it will change the way CVD is treated in the US. We got the sense that this should lead to the FDA giving Vascepa “fast-track” (6 months vs regular 10 months) treatment for label expansion, which will surely lead to higher revenues this year and an expanded market henceforth.

New Prescriptions up 62% YTD: Amarin’s CEO, John Thero, told us he has more talks with doctors about Vascepa these days than he does with investors, which highlights increasing interest in the US medical community over Vascepa and explains the new prescription growth of +62% year-to-date. Successful label expansion by the FDA should widen Vascepa’s addressable market by nearly 20x.

Our Talks With CEO Point to a Strong Q1: The first quarter is seasonally slow, but our impressions from our talk with CEO John Thero is that the company is most likely outperforming its internal targets for Q1 growth. Amarin assumes 53% sales growth for the full year, but has stated that Q1 should be “seasonally slower”. Weekly prescription data show that Vascepa is growing over 50% in the seasonally slow Q1. Sales should pick up from Q2 and surge in the usual peak season of Q4.

2019 Revenues should Reach $500m (+120% YoY): We see 2019 revenues of $503m, with operating profit of $88m (17.5% operating margin) and EPS of $0.23. Consensus sees sales of $363m (guidance is at $350m), with an operating loss of -$58m and EPS of -$0.17.

Buyout Possibilities Remain High: We continue to see Amarin as one of the most attractive buy-out candidates among big pharma companies in the CVD field. Because Vascepa is a treatment taken in conjunction with statin medication like Lipitor, Pfizer appears like the most likely suitor, although there many others.

Lasertec hit a new high in the semiconductor stock rally that followed Micron Technology’s March 20 earnings call. On Friday, March 22 (March 21 was a holiday in Japan), Lasertec was up 8.4% to ¥4,900. At this price, the shares are selling at 42x our EPS estimate for FY Jun-19, 36x our estimate for FY Jun-20 and 31x our estimate for FY Jun-21. On a 5-year view, earnings growth could bring the projected P/E multiple down to 21x, in our estimation.

Following strong 1H results, management left FY Jun-19 sales and profit guidance unchanged, but raised semiconductor-related orders guidance by 13% while cutting orders guidance for FPD-related and other products by nearly 40%. Total new orders guidance was raised from ¥37 billion to ¥39 billion, compared with sales guidance of ¥28 billion, implying an increase in the order backlog from ¥39.9 billion to ¥50.9 billion.

With this in mind, we have raised our sales and profit estimates for FY Jun-20 and added new, higher estimates for FY Jun-21 and beyond. Rising demand for EUV mask blank and mask defect inspection equipment should drive an increase in total sales from ¥29 billion this fiscal year to ¥38 billion in FY Jun-21, and approximately ¥50 billion in FY Jun-23. Over the same period, operating profit should rise from ¥7.0 billion to ¥9.5 billion, and then to approximately ¥14 billion.

Risks for investors include the potential delay or reduction of orders and shipments (as just happened with FPD inspection equipment), high volatility in quarterly orders, sales and profits, and extended valuations.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Theme of the week: Block trades/Placements + news flow on upcoming IPOs

Starting with placements, the shareholders of Wuxi Biologics (Cayman) Inc (2269 HK) are back on the market again to sell some shares. They been quite consistent with the selling and our team have covered the company the IPO each of the placements. Wisetech Global (WTC AU) and Platinum Asset Management (PTM AU) also had blocks that were sold earlier this week. The former did excceedingly well post-placement, currently more than 10% above its deal price while the latter had struggled as a result of Kerr and his ex-wife selling a portion of their shares in the company.

As for upcoming IPOs, Hong Kong ECM activity is ramping up. Megvii, the Chinese AI startup is looking to list in Hong Kong or US whereas China Feihe (FEIHE HK) is said to be revisit its US$1bn HK IPO. Ke Yan, CFA, FRM has covered the latter in this insight almost two years ago.

We also heard that Frontage had already met investors and Ke Yan, CFA, FRM has provided preliminary thoughts on valuation in:

Mulsanne Group (previously known as Alpha Smart (GXG)), Xinyi Energy Holdings, CMGE Tech, and 360 ludashi (鲁大师) re-filed their draft prospectuses. We have covered Mulsanne and Xinyi Energy in:

360 ludashi’s previous filing indicated that its IPO deal size will be small (<US$100m). However, the updated financials shown an almost 50% YoY PATMI growth which could put its IPO at a borderline deal size of US$100m if growth maintains at 50%.

In the U.S, Yunji Inc. (YJ US) filed for a US$200m IPO. The company runs a Chinese e-commerce site that uses a social platform to promote its products. We will be writing an early note on the company next week.

In Singapore, Eagle Hospitality REIT is said to have started investor education for its IPO while Lendlease is planning to raise up to US$500m for its retail REIT according to media reports.

In other ASEAN markets, there are also a handful of IPOs to watch out for.

In Indonesia, Lion Air is said to be targeting US$1bn listing in the third quarter of this year and it is starting to gauge investor interest. MAP Actif has already started pre-marketing its IPO.

In Thailand, Kerry Express Thailand is said to have hired banks to prepare for a >US$100m IPO.

In Malaysia, QSR Brands (QSR MY) has started to pre-market for its US$500m IPO. Sumeet Singh had previously written an early note:

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Hankyu Hanshin has outperformed the department store sector in the last few years and continues to invest to lock in its dominance of the Osaka market.

It is now about to unveil a major new update to its Tokyo store, creating a more luxurious Men’s Emporium.

The investment is an example of how the better department stores are repositioning individual buildings to better meet target market needs and find relevance in an e-commerce age.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

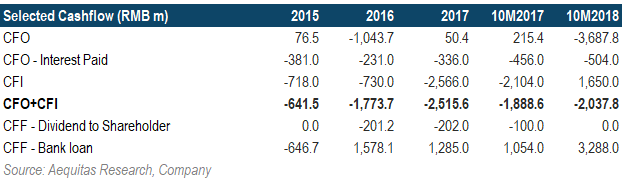

Investors who have bought CSE Global on dips since my last note would have profited ~18%.

The upbeat guidance by management and supply-demand environment should give some legs to the recent rebound.

While risks of slower global growth may weigh on the stock, the stock is trading below its five-year average PE despite significantly improved cash flow from operations and a healthy order intake (three-year high).

Yincheng International, a China Yangtze delta focused property developer, is raising up to USD 110 million to list on the Hong Kong Stock Exchange. In this note, we will cover the following topics:

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Starting with listings in Hong Kong next week, CStone Pharma (2616 HK) and Dexin China Holdings (2019 HK) will list on the 26th of February. Dexin is said to have priced at the mid-point of its price range while CStone is priced above its mid-point.

We also heard that Haitong Unitrust International Leasing was given the green light by CSRC for its Hong Kong IPO. The company had previously re-filed its draft prospectus in September last year. Shanghai Dongzheng Automotive Finance has also received approval from CSRC for its IPO.

There had also been a small property developer, YinCheng, that had launched its US$100m IPO. Jinxin Fertility had also just filed its draft prospectus with the HKEX.

Our overall accuracy rate is 72.1% for IPOs and 63.7% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

Jinxin Fertility Group (US$600m, Hong Kong)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Strong Q1 to Come: We recently had a call with Amarin’s CEO, John Thero, and update our model with quarterly estimates. Q1 should see revenue growth of +55% YoY to $68m, an operating loss of -$30m, and EPS of -$0.09. Consensus is at $66m, -$38m, and -$0.12, respectively.

ACC Event Leads to Stock Drop: Amarin released “late-breaking” results from its Reduce-It trial at the American College of Cardiology (ACC) conference last Monday. While the data was considered “landmark” by doctors in attendance, the stock has fallen by nearly 14% since the event, showing a clear disconnect between the market and the medical community.

New Data Upgrades Risk Reduction to 30% & Shows Strong Prevention of CVD Recurrence: The key data at the ACC showed that Vascepa has a 30% relative risk reduction (RRR) rate for total CVD events (initially, it was 25% RRR rate for “major adverse” CVD events). Additionally, it was discovered that Vascepa reduced secondary CVD events by 32%, third events by 31%, and fourth events by 48%. 50% of patients who have experienced a cardiovascular event have a recurrence within one year, while 75% have recurrences within three years.

New Data Should Fast-Track Label Expansion & Impact Earnings Significantly: Doctors on a panel discussion after Amarin’s presentation at the ACC were dazzled by the data, saying that it will change the way CVD is treated in the US. We got the sense that this should lead to the FDA giving Vascepa “fast-track” (6 months vs regular 10 months) treatment for label expansion, which will surely lead to higher revenues this year and an expanded market henceforth.

New Prescriptions up 62% YTD: Amarin’s CEO, John Thero, told us he has more talks with doctors about Vascepa these days than he does with investors, which highlights increasing interest in the US medical community over Vascepa and explains the new prescription growth of +62% year-to-date. Successful label expansion by the FDA should widen Vascepa’s addressable market by nearly 20x.

Our Talks With CEO Point to a Strong Q1: The first quarter is seasonally slow, but our impressions from our talk with CEO John Thero is that the company is most likely outperforming its internal targets for Q1 growth. Amarin assumes 53% sales growth for the full year, but has stated that Q1 should be “seasonally slower”. Weekly prescription data show that Vascepa is growing over 50% in the seasonally slow Q1. Sales should pick up from Q2 and surge in the usual peak season of Q4.

2019 Revenues should Reach $500m (+120% YoY): We see 2019 revenues of $503m, with operating profit of $88m (17.5% operating margin) and EPS of $0.23. Consensus sees sales of $363m (guidance is at $350m), with an operating loss of -$58m and EPS of -$0.17.

Buyout Possibilities Remain High: We continue to see Amarin as one of the most attractive buy-out candidates among big pharma companies in the CVD field. Because Vascepa is a treatment taken in conjunction with statin medication like Lipitor, Pfizer appears like the most likely suitor, although there many others.

Lasertec hit a new high in the semiconductor stock rally that followed Micron Technology’s March 20 earnings call. On Friday, March 22 (March 21 was a holiday in Japan), Lasertec was up 8.4% to ¥4,900. At this price, the shares are selling at 42x our EPS estimate for FY Jun-19, 36x our estimate for FY Jun-20 and 31x our estimate for FY Jun-21. On a 5-year view, earnings growth could bring the projected P/E multiple down to 21x, in our estimation.

Following strong 1H results, management left FY Jun-19 sales and profit guidance unchanged, but raised semiconductor-related orders guidance by 13% while cutting orders guidance for FPD-related and other products by nearly 40%. Total new orders guidance was raised from ¥37 billion to ¥39 billion, compared with sales guidance of ¥28 billion, implying an increase in the order backlog from ¥39.9 billion to ¥50.9 billion.

With this in mind, we have raised our sales and profit estimates for FY Jun-20 and added new, higher estimates for FY Jun-21 and beyond. Rising demand for EUV mask blank and mask defect inspection equipment should drive an increase in total sales from ¥29 billion this fiscal year to ¥38 billion in FY Jun-21, and approximately ¥50 billion in FY Jun-23. Over the same period, operating profit should rise from ¥7.0 billion to ¥9.5 billion, and then to approximately ¥14 billion.

Risks for investors include the potential delay or reduction of orders and shipments (as just happened with FPD inspection equipment), high volatility in quarterly orders, sales and profits, and extended valuations.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Theme of the week: Block trades/Placements + news flow on upcoming IPOs

Starting with placements, the shareholders of Wuxi Biologics (Cayman) Inc (2269 HK) are back on the market again to sell some shares. They been quite consistent with the selling and our team have covered the company the IPO each of the placements. Wisetech Global (WTC AU) and Platinum Asset Management (PTM AU) also had blocks that were sold earlier this week. The former did excceedingly well post-placement, currently more than 10% above its deal price while the latter had struggled as a result of Kerr and his ex-wife selling a portion of their shares in the company.

As for upcoming IPOs, Hong Kong ECM activity is ramping up. Megvii, the Chinese AI startup is looking to list in Hong Kong or US whereas China Feihe (FEIHE HK) is said to be revisit its US$1bn HK IPO. Ke Yan, CFA, FRM has covered the latter in this insight almost two years ago.

We also heard that Frontage had already met investors and Ke Yan, CFA, FRM has provided preliminary thoughts on valuation in:

Mulsanne Group (previously known as Alpha Smart (GXG)), Xinyi Energy Holdings, CMGE Tech, and 360 ludashi (鲁大师) re-filed their draft prospectuses. We have covered Mulsanne and Xinyi Energy in:

360 ludashi’s previous filing indicated that its IPO deal size will be small (<US$100m). However, the updated financials shown an almost 50% YoY PATMI growth which could put its IPO at a borderline deal size of US$100m if growth maintains at 50%.

In the U.S, Yunji Inc. (YJ US) filed for a US$200m IPO. The company runs a Chinese e-commerce site that uses a social platform to promote its products. We will be writing an early note on the company next week.

In Singapore, Eagle Hospitality REIT is said to have started investor education for its IPO while Lendlease is planning to raise up to US$500m for its retail REIT according to media reports.

In other ASEAN markets, there are also a handful of IPOs to watch out for.

In Indonesia, Lion Air is said to be targeting US$1bn listing in the third quarter of this year and it is starting to gauge investor interest. MAP Actif has already started pre-marketing its IPO.

In Thailand, Kerry Express Thailand is said to have hired banks to prepare for a >US$100m IPO.

In Malaysia, QSR Brands (QSR MY) has started to pre-market for its US$500m IPO. Sumeet Singh had previously written an early note:

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Hankyu Hanshin has outperformed the department store sector in the last few years and continues to invest to lock in its dominance of the Osaka market.

It is now about to unveil a major new update to its Tokyo store, creating a more luxurious Men’s Emporium.

The investment is an example of how the better department stores are repositioning individual buildings to better meet target market needs and find relevance in an e-commerce age.

These are the five developments/news flows/trends and their potential impact on Thai equities you should be aware of in recent weeks:

Reversing Brexit. A special report highlighting the possible reversal of Brexit should have limited impact on Thai equities, though a few names like SSI, Thai Union, and Minor do float up on the screen.

TMB announces a 5 for 1 rights issue at Bt2.07/sh, which could raise US$570m of new capital for their acquisition of Thanchart and imply a 65-35 split of ownership between the two banks.

Politically motivated wage hike. Some of the political campaigns by smaller parties are even more populist than the major parties, implying wage increases between 10-30% from current levels. This could really destabilize Thailand’s long-term prospects as an investment base.

Italian-Thai Chairman thrown into prison. Premchai Karnasutra, who killed one of Thailand’s last 9 black leopards, is sentenced to 16 months in jail. Share prices actually rose!

Bangkok’s third airport! The Navy is putting up the UTaPao airport construction up for bid. Front runners include the CP-led consortium, which includes ITD, but contenders include the BTS-STEC consortium and another smaller one.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Yincheng International, a China Yangtze delta focused property developer, is raising up to USD 110 million to list on the Hong Kong Stock Exchange. In this note, we will cover the following topics:

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Starting with listings in Hong Kong next week, CStone Pharma (2616 HK) and Dexin China Holdings (2019 HK) will list on the 26th of February. Dexin is said to have priced at the mid-point of its price range while CStone is priced above its mid-point.

We also heard that Haitong Unitrust International Leasing was given the green light by CSRC for its Hong Kong IPO. The company had previously re-filed its draft prospectus in September last year. Shanghai Dongzheng Automotive Finance has also received approval from CSRC for its IPO.

There had also been a small property developer, YinCheng, that had launched its US$100m IPO. Jinxin Fertility had also just filed its draft prospectus with the HKEX.

Our overall accuracy rate is 72.1% for IPOs and 63.7% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

Jinxin Fertility Group (US$600m, Hong Kong)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Yincheng International, a China Yangtze delta focused property developer, is raising up to USD 110 million to list on the Hong Kong Stock Exchange. In this note, we will cover the following topics:

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Starting with listings in Hong Kong next week, CStone Pharma (2616 HK) and Dexin China Holdings (2019 HK) will list on the 26th of February. Dexin is said to have priced at the mid-point of its price range while CStone is priced above its mid-point.

We also heard that Haitong Unitrust International Leasing was given the green light by CSRC for its Hong Kong IPO. The company had previously re-filed its draft prospectus in September last year. Shanghai Dongzheng Automotive Finance has also received approval from CSRC for its IPO.

There had also been a small property developer, YinCheng, that had launched its US$100m IPO. Jinxin Fertility had also just filed its draft prospectus with the HKEX.

Our overall accuracy rate is 72.1% for IPOs and 63.7% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

Jinxin Fertility Group (US$600m, Hong Kong)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Legislation on rice tariffication signed by President Duterte into law allows for liberal rice imports, thus, effectively dismantling the State regulatory control over the grains sector. This bodes well for stabilizing food inflation that has been the scourge of low income groups. Lower food prices over time help anchor inflation expectations while ‘freeing’ up purchasing power among low income households for redeployment to support non-food demand. Rice imports would be slapped tariffs with the proceeds targeted at developmental support for vulnerable local rice farmers.

Market segmentation (between local and imported rice), bias for affordable food choices among households with limited incomes, and fiscal interventions to attain food security, would spare the local market from the heavy assault of rice imports.

As these laws on rice tariffication and BSP charter amendments gain traction, we expect the BSP to depend largely on market-based, policy tools in inflation and liquidity management. As high bank reserve ratios lose policy relevance, we sense the likelihood of a conversion to a single-digit reserve ratio over the medium-term. This policy outcome augurs for lower intermediation costs among banks that hopefully translates into better yielding, regular savings and time deposits that could appeal to low income depositors.

Inclusive of the TRAIN law package 1 that’s intact despite the high inflation challenge, the recent institutional reforms provide the backdrop for another round of investment-credit ratings upgrade.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.