The Premier Li Keqiang had just conducted an annual Government Work Report in the two session conference (两会) in Beijing this morning. In this insight, we will briefly walk through key points of his report and identify bulls and bears in the market.

While the theme of cost reduction benefits manufacturing companies, it will negative for some infrastructure service providers, such as telecom companies.

In our Discover SZ/SH Connect series, we aim to help our investors understand the flow of northbound trades via the Shanghai Connect and Shenzhen Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by offshore investors in the past seven days.

We split the stocks eligible for the northbound trade into three groups: those with a market capitalization of above USD 5 billion, and those with a market capitalization between USD 1 billion and USD 5 billion.

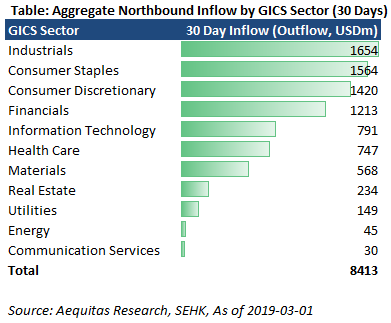

We note that offshore investors were buying all GICS sectors, and had a strong preference for Industrials, Consumer Staples, Consumer Discretionary, and Financials names. We estimate that total inflow into the A-share market via northbound trade amounted to USD 8.4 bn in February.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The Premier Li Keqiang had just conducted an annual Government Work Report in the two session conference (两会) in Beijing this morning. In this insight, we will briefly walk through key points of his report and identify bulls and bears in the market.

While the theme of cost reduction benefits manufacturing companies, it will negative for some infrastructure service providers, such as telecom companies.

In our Discover SZ/SH Connect series, we aim to help our investors understand the flow of northbound trades via the Shanghai Connect and Shenzhen Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by offshore investors in the past seven days.

We split the stocks eligible for the northbound trade into three groups: those with a market capitalization of above USD 5 billion, and those with a market capitalization between USD 1 billion and USD 5 billion.

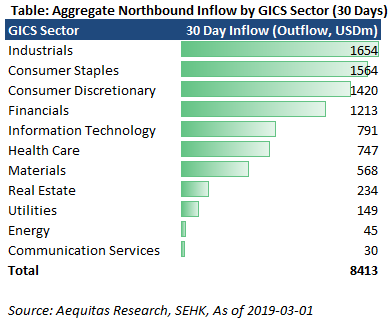

We note that offshore investors were buying all GICS sectors, and had a strong preference for Industrials, Consumer Staples, Consumer Discretionary, and Financials names. We estimate that total inflow into the A-share market via northbound trade amounted to USD 8.4 bn in February.

Lyft Inc (LYFT US), a leading US based ride-hailing company, is getting ready for an IPO in the US in the next several weeks. One of the major positives of the Lyft IPO is the timing – Lyft should be able to complete its IPO ahead of its chief rival Uber which is expected to file its IPO later in 2019.

The financials for Lyft will likely to change significantly in the next five to ten years, mainly due to the increased adoption of autonomous vehicles, which would reduce the need for Lyft to pay for the drivers. This cost can be eventually eliminated with full scale autonomous driving. Although we do not have figures as to exactly how much Lyft pays for all its drivers, in five to ten years when the fully autonomous vehicles are allowed, this could significantly change the basic economics of operating its ridesharing business.

Potential shares dilution risk from additional rights offering a few years after this IPO is a serious risk for the company. Once Lyft completes its IPO in a few weeks, depending on the institutional investors’ demand for the deal, the company is likely to be infused with several billions of dollars from IPO proceeds. However, the IPO proceeds may not be enough and the company may need to conduct another large scale rights offering in a few years (for example in 2021 or 2022) which may be prior to the fully autonomous vehicles acceptance and regulatory approval by major countries around the world such as the United States.

Late last year, in the final run-up to the vote to determine whether Alpine (6816 JP) investors would subject themselves to a bad share exchange ratio or would choose to oblige Alps (6770 JP) to have another run at it in a different format, Alps announced a shareholder return policy which included buying back ¥40 billion of shares.

It is to be noted that this meant that the combined entity was going to be left with less cash than the total deemed necessary by the two companies just a very short while before. Why? Because Alps – with the strong governance it has – obviously had the right amount – and Alpine also had the right amount (it needed substantial equity-funded cash as “working capital” because otherwise it would run a serious danger of business disruption and deterioration. So despite this severe business risk, the two companies effectively announced they would disburse 90% of Alpine’s cash on hand to shareholders POST-MERGER through the special dividend offered to sweeten the pot to get the merger through, and the ¥40 billion buyback.

The merger, of course, went through, and the ¥28.4 billion* buyback is proceeding apace.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We selectively visited a dozen companies in March and were most impressed with three of them (two of which we happily own):

SISB, Thailand’s only listed education stock, whose market cap has increased more than 30% since its IPO. The future potential growth they are currently working on in Cambodia and China will show up here and spruce the company’s already strong growth. Working in a favorable environment (Thailand’s affluent class is growing) also helps.

MINT, the country’s hotel chain giant and 20th largest chain in the world, sees great growth potential in Europe, where things are slowly turning around after they made two big acquisitions (NH Hotels and Tivoli). Synergies are also materializing with co-marketing and re-branding efforts.

After You, arguably the dessert chain with the highest margin in Thailand. No longer a newbie IPO stock, these guys boast collaboration with global giant Starbucks and branching out into new channels such as After You Durian.

The deal scores marginally positive on our framework owing to its decent track record, and price and earnings momentum.

Its past deals have done well in the long run. Even though it did not perform well over the one-month period, its first week returns have tend to hold up above the deal price.

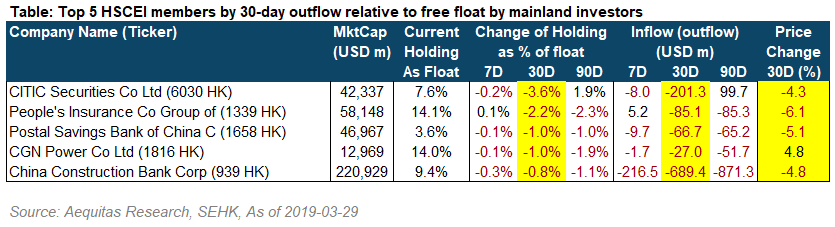

This is a monthly version of our HK Connect Weekly note, in which I highlight Hong Kong-listed companies leading the southbound flow weekly. Over the past month, we have seen the flow turned from outflow in February to inflow in March. Chinese investors were also buying Consumer Staples and Consumer Discretionary stocks.

Our March Coverage of Hong Kong Connect southbound flow

BabyTree (1761.HK)’s reported results for FY2018 continues to be impacted by the ‘shift in e-commerce strategy’ post collaboration with Alibaba Group Holding (BABA US) (also a key investor). China’s leading parenting community platform that went public in November 2018 has announced a revenue decline of 4% during 2H2018; its e-commerce revenues were down 70% as its being ‘integrated’ with Alibaba. This is expected to be completed by 2Q2019. While the details of the collaboration (and revenue share, if any) are not given, Management has stated that Alibaba will manage the back-end e-commerce at a reduced cost and better efficiency while it will ‘manage’ users. Despite the fall in revenues, gross profits were up 18% helped by growth in advertisement revenues which now account for 85% of the total. Advertising as a revenue source has limited long term growth and valuation potential compared to e-commerce. The stock is up 25% since results announcement on March 27th, likely enthused by Net profit for FY2018 at Rmb526.2 mn and EPS of Rmb0.29 (implied current Year P/E of 23x). Key risk will be failure to revive e-commerce revenues post ‘integration’.

BabyTree also announced its first global foray – it has invested USD8mn in Healofy, amongst the top 3 leading parenting apps in India currently. India’s online Parenting app segment has numerous players and revenue generation/growth may not be easy in the near term for Healofy. However, our analysis suggests that India’s overcrowded parenting app segment is now witnessing consolidation and this funding could probably help Healofy solidify its ranking amongst top 3 parenting platforms in India. In this context, BabyTree’s foray into India seems well timed. Healofy could potentially follow BabyTree’s operating model and fit into Alibaba Group Holding (BABA US) ‘s India e-commerce strategy (Refer our earlier report Alibaba’s India Game Plan – More than Meets the Eye; Investor Day Analysis (Part II) ).

In the detailed report that follows, we briefly comment on BabyTree’s reported 2018 results and also present a quick overview of India Parenting App segment – key players, investors and why we think it may be on a consolidation mode.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In our Discover SZ/SH Connect series, we aim to help our investors understand the flow of northbound trades via the Shanghai Connect and Shenzhen Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by offshore investors in the past seven days.

We split the stocks eligible for the northbound trade into three groups: those with a market capitalization of above USD 5 billion, and those with a market capitalization between USD 1 billion and USD 5 billion.

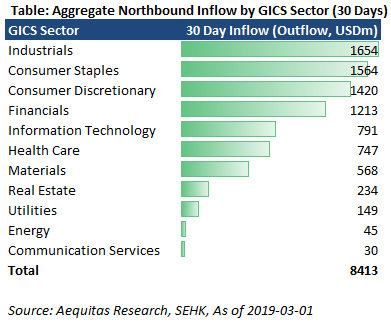

We note that offshore investors were buying all GICS sectors, and had a strong preference for Industrials, Consumer Staples, Consumer Discretionary, and Financials names. We estimate that total inflow into the A-share market via northbound trade amounted to USD 8.4 bn in February.

Lyft Inc (LYFT US), a leading US based ride-hailing company, is getting ready for an IPO in the US in the next several weeks. One of the major positives of the Lyft IPO is the timing – Lyft should be able to complete its IPO ahead of its chief rival Uber which is expected to file its IPO later in 2019.

The financials for Lyft will likely to change significantly in the next five to ten years, mainly due to the increased adoption of autonomous vehicles, which would reduce the need for Lyft to pay for the drivers. This cost can be eventually eliminated with full scale autonomous driving. Although we do not have figures as to exactly how much Lyft pays for all its drivers, in five to ten years when the fully autonomous vehicles are allowed, this could significantly change the basic economics of operating its ridesharing business.

Potential shares dilution risk from additional rights offering a few years after this IPO is a serious risk for the company. Once Lyft completes its IPO in a few weeks, depending on the institutional investors’ demand for the deal, the company is likely to be infused with several billions of dollars from IPO proceeds. However, the IPO proceeds may not be enough and the company may need to conduct another large scale rights offering in a few years (for example in 2021 or 2022) which may be prior to the fully autonomous vehicles acceptance and regulatory approval by major countries around the world such as the United States.

Late last year, in the final run-up to the vote to determine whether Alpine (6816 JP) investors would subject themselves to a bad share exchange ratio or would choose to oblige Alps (6770 JP) to have another run at it in a different format, Alps announced a shareholder return policy which included buying back ¥40 billion of shares.

It is to be noted that this meant that the combined entity was going to be left with less cash than the total deemed necessary by the two companies just a very short while before. Why? Because Alps – with the strong governance it has – obviously had the right amount – and Alpine also had the right amount (it needed substantial equity-funded cash as “working capital” because otherwise it would run a serious danger of business disruption and deterioration. So despite this severe business risk, the two companies effectively announced they would disburse 90% of Alpine’s cash on hand to shareholders POST-MERGER through the special dividend offered to sweeten the pot to get the merger through, and the ¥40 billion buyback.

The merger, of course, went through, and the ¥28.4 billion* buyback is proceeding apace.

Five interesting trends/developments that could impact Thai equities in the recent period:

Legalization of medicinal marijuana. Thailand legalized medicinal use of marijuana at end of February and has already received immense interest from potential growers. At some point, pharma and healthcare companies could be beneficiaries of this trend.

Rumbles in the airline industry. Asia Aviation (AAV TB) , parent company of Thai Air Asia, acquires a stake in competitor Nok Air. This is one of the few signs of industry consolidation in this sector.

MOU signed between TMB and Thanachart. The deal may take longer than initially expected, but the two sides have agreed on some basics such as 70% equity financing and deal size of roughly Bt130-140bn.

Read-through from US Election 2020. Some of the Democrat policies advocated by candidates in 2020 could turn out to be positive for Asian equities.

BGrimm acquires Glow SPP1 for a bargain price of Bt3.3bn, or 55% of the expected price, opening the way for the GPSC-Glow merger, potentially the largest deal of 2019.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The deal scores marginally positive on our framework owing to its decent track record, and price and earnings momentum.

Its past deals have done well in the long run. Even though it did not perform well over the one-month period, its first week returns have tend to hold up above the deal price.

This is a monthly version of our HK Connect Weekly note, in which I highlight Hong Kong-listed companies leading the southbound flow weekly. Over the past month, we have seen the flow turned from outflow in February to inflow in March. Chinese investors were also buying Consumer Staples and Consumer Discretionary stocks.

Our March Coverage of Hong Kong Connect southbound flow

BabyTree (1761.HK)’s reported results for FY2018 continues to be impacted by the ‘shift in e-commerce strategy’ post collaboration with Alibaba Group Holding (BABA US) (also a key investor). China’s leading parenting community platform that went public in November 2018 has announced a revenue decline of 4% during 2H2018; its e-commerce revenues were down 70% as its being ‘integrated’ with Alibaba. This is expected to be completed by 2Q2019. While the details of the collaboration (and revenue share, if any) are not given, Management has stated that Alibaba will manage the back-end e-commerce at a reduced cost and better efficiency while it will ‘manage’ users. Despite the fall in revenues, gross profits were up 18% helped by growth in advertisement revenues which now account for 85% of the total. Advertising as a revenue source has limited long term growth and valuation potential compared to e-commerce. The stock is up 25% since results announcement on March 27th, likely enthused by Net profit for FY2018 at Rmb526.2 mn and EPS of Rmb0.29 (implied current Year P/E of 23x). Key risk will be failure to revive e-commerce revenues post ‘integration’.

BabyTree also announced its first global foray – it has invested USD8mn in Healofy, amongst the top 3 leading parenting apps in India currently. India’s online Parenting app segment has numerous players and revenue generation/growth may not be easy in the near term for Healofy. However, our analysis suggests that India’s overcrowded parenting app segment is now witnessing consolidation and this funding could probably help Healofy solidify its ranking amongst top 3 parenting platforms in India. In this context, BabyTree’s foray into India seems well timed. Healofy could potentially follow BabyTree’s operating model and fit into Alibaba Group Holding (BABA US) ‘s India e-commerce strategy (Refer our earlier report Alibaba’s India Game Plan – More than Meets the Eye; Investor Day Analysis (Part II) ).

In the detailed report that follows, we briefly comment on BabyTree’s reported 2018 results and also present a quick overview of India Parenting App segment – key players, investors and why we think it may be on a consolidation mode.

It was reported over the weekend that the troubled display supplier to iPhone maker Apple, Japan Display (JDI) has almost finalized a deal to raise more than JPY110bn (US$990m) from a China-Taiwan consortium and Japanese public-private fund INCJ Ltd.

The China-Taiwan consortium is expected to secure some 50% stake in Japan Display while the top shareholder INCJ’s current stake of 25.3% is expected to be halved.

The consortium is aiming to restructure JDI’s remaining debt payments of about JPY100bn from Apple for the construction of its plant while it also aims to procure parts for the latest iPhone. In addition, the consortium is also trying to modify a contract stipulating that Apple can seize plants if JDI’s cash and deposits fall below a certain amount.

The consortium along with JDI is planning to build an OLED panel plant in China with JDI providing the technological know-how while the consortium partners invest in capital expenditures and equity.

Japan Display has been struggling to navigate its display business due to the slowdown in iPhone sales, falling behind competition on OLED technology and facing stiff price competition from Chinese panel makers.

We expect the proposed OLED plant in China could help the company stabilize its panel business with Chinese smartphone makers Huawei and Xiaomi who prefer to source panels locally from domestic panel makers such as BOE Technology and Tianma.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Lyft Inc (LYFT US), a leading US based ride-hailing company, is getting ready for an IPO in the US in the next several weeks. One of the major positives of the Lyft IPO is the timing – Lyft should be able to complete its IPO ahead of its chief rival Uber which is expected to file its IPO later in 2019.

The financials for Lyft will likely to change significantly in the next five to ten years, mainly due to the increased adoption of autonomous vehicles, which would reduce the need for Lyft to pay for the drivers. This cost can be eventually eliminated with full scale autonomous driving. Although we do not have figures as to exactly how much Lyft pays for all its drivers, in five to ten years when the fully autonomous vehicles are allowed, this could significantly change the basic economics of operating its ridesharing business.

Potential shares dilution risk from additional rights offering a few years after this IPO is a serious risk for the company. Once Lyft completes its IPO in a few weeks, depending on the institutional investors’ demand for the deal, the company is likely to be infused with several billions of dollars from IPO proceeds. However, the IPO proceeds may not be enough and the company may need to conduct another large scale rights offering in a few years (for example in 2021 or 2022) which may be prior to the fully autonomous vehicles acceptance and regulatory approval by major countries around the world such as the United States.

Late last year, in the final run-up to the vote to determine whether Alpine (6816 JP) investors would subject themselves to a bad share exchange ratio or would choose to oblige Alps (6770 JP) to have another run at it in a different format, Alps announced a shareholder return policy which included buying back ¥40 billion of shares.

It is to be noted that this meant that the combined entity was going to be left with less cash than the total deemed necessary by the two companies just a very short while before. Why? Because Alps – with the strong governance it has – obviously had the right amount – and Alpine also had the right amount (it needed substantial equity-funded cash as “working capital” because otherwise it would run a serious danger of business disruption and deterioration. So despite this severe business risk, the two companies effectively announced they would disburse 90% of Alpine’s cash on hand to shareholders POST-MERGER through the special dividend offered to sweeten the pot to get the merger through, and the ¥40 billion buyback.

The merger, of course, went through, and the ¥28.4 billion* buyback is proceeding apace.

Five interesting trends/developments that could impact Thai equities in the recent period:

Legalization of medicinal marijuana. Thailand legalized medicinal use of marijuana at end of February and has already received immense interest from potential growers. At some point, pharma and healthcare companies could be beneficiaries of this trend.

Rumbles in the airline industry. Asia Aviation (AAV TB) , parent company of Thai Air Asia, acquires a stake in competitor Nok Air. This is one of the few signs of industry consolidation in this sector.

MOU signed between TMB and Thanachart. The deal may take longer than initially expected, but the two sides have agreed on some basics such as 70% equity financing and deal size of roughly Bt130-140bn.

Read-through from US Election 2020. Some of the Democrat policies advocated by candidates in 2020 could turn out to be positive for Asian equities.

BGrimm acquires Glow SPP1 for a bargain price of Bt3.3bn, or 55% of the expected price, opening the way for the GPSC-Glow merger, potentially the largest deal of 2019.

Sea Ltd (SE US) is looking to raise about US$1.2bn in its upcoming placement. It will be larger than its IPO in 2017, which raised about US$880m.

The deal scores well on our framework owing to decent valuation, strong price and earnings momentum but had little track record for comparison. The company announced a strong set of FY2018/Q4 2018 results which had beaten estimates.

Even though, the deal size is large, representing 23.2 days of three-month ADV, there is enough time between the announcement to the end of the bookbuild to price in the impact of the placement.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

This is a monthly version of our HK Connect Weekly note, in which I highlight Hong Kong-listed companies leading the southbound flow weekly. Over the past month, we have seen the flow turned from outflow in February to inflow in March. Chinese investors were also buying Consumer Staples and Consumer Discretionary stocks.

Our March Coverage of Hong Kong Connect southbound flow

BabyTree (1761.HK)’s reported results for FY2018 continues to be impacted by the ‘shift in e-commerce strategy’ post collaboration with Alibaba Group Holding (BABA US) (also a key investor). China’s leading parenting community platform that went public in November 2018 has announced a revenue decline of 4% during 2H2018; its e-commerce revenues were down 70% as its being ‘integrated’ with Alibaba. This is expected to be completed by 2Q2019. While the details of the collaboration (and revenue share, if any) are not given, Management has stated that Alibaba will manage the back-end e-commerce at a reduced cost and better efficiency while it will ‘manage’ users. Despite the fall in revenues, gross profits were up 18% helped by growth in advertisement revenues which now account for 85% of the total. Advertising as a revenue source has limited long term growth and valuation potential compared to e-commerce. The stock is up 25% since results announcement on March 27th, likely enthused by Net profit for FY2018 at Rmb526.2 mn and EPS of Rmb0.29 (implied current Year P/E of 23x). Key risk will be failure to revive e-commerce revenues post ‘integration’.

BabyTree also announced its first global foray – it has invested USD8mn in Healofy, amongst the top 3 leading parenting apps in India currently. India’s online Parenting app segment has numerous players and revenue generation/growth may not be easy in the near term for Healofy. However, our analysis suggests that India’s overcrowded parenting app segment is now witnessing consolidation and this funding could probably help Healofy solidify its ranking amongst top 3 parenting platforms in India. In this context, BabyTree’s foray into India seems well timed. Healofy could potentially follow BabyTree’s operating model and fit into Alibaba Group Holding (BABA US) ‘s India e-commerce strategy (Refer our earlier report Alibaba’s India Game Plan – More than Meets the Eye; Investor Day Analysis (Part II) ).

In the detailed report that follows, we briefly comment on BabyTree’s reported 2018 results and also present a quick overview of India Parenting App segment – key players, investors and why we think it may be on a consolidation mode.

It was reported over the weekend that the troubled display supplier to iPhone maker Apple, Japan Display (JDI) has almost finalized a deal to raise more than JPY110bn (US$990m) from a China-Taiwan consortium and Japanese public-private fund INCJ Ltd.

The China-Taiwan consortium is expected to secure some 50% stake in Japan Display while the top shareholder INCJ’s current stake of 25.3% is expected to be halved.

The consortium is aiming to restructure JDI’s remaining debt payments of about JPY100bn from Apple for the construction of its plant while it also aims to procure parts for the latest iPhone. In addition, the consortium is also trying to modify a contract stipulating that Apple can seize plants if JDI’s cash and deposits fall below a certain amount.

The consortium along with JDI is planning to build an OLED panel plant in China with JDI providing the technological know-how while the consortium partners invest in capital expenditures and equity.

Japan Display has been struggling to navigate its display business due to the slowdown in iPhone sales, falling behind competition on OLED technology and facing stiff price competition from Chinese panel makers.

We expect the proposed OLED plant in China could help the company stabilize its panel business with Chinese smartphone makers Huawei and Xiaomi who prefer to source panels locally from domestic panel makers such as BOE Technology and Tianma.

We expect Haitian’s margins go up in 2019, because 1) steel price in China is expected to decrease by 10% yoy with the re-balance of sector demand-supply, 2) Haitian’s newly launched third generation PIMM, and increasing sales propotion of high margin products, would improve the company’s overall margin.

Market demand is warming up in March, according to the management. The third generation PIMM is expected to trigger clients’ demand on upgrading their existing machines. High margin products, all-electric PIMM and large two-plate PIMM, would further increasing their sales and profit contribution. Overseas revenue growth would continue going faster than domestic revenue growth, with its new plants in Germany and Turkey coming on stream. We estimate Haitian’s net profit growth to reach 15% yoy in 2019E, vs. a 4% yoy decline in 2018.

Market concern on potential risk from Trade War, which had triggered Haitian’s valuation de-rating, should fade. As we expected, Haitian’s business wasn’t hurt by the Trade War in 2018, as the company has only 3% of overall revenue from US market. And the negotiations between US and China are on the right way to terminate the Trade War. Valuation re-rating might come with earnings improvement.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Late last year, in the final run-up to the vote to determine whether Alpine (6816 JP) investors would subject themselves to a bad share exchange ratio or would choose to oblige Alps (6770 JP) to have another run at it in a different format, Alps announced a shareholder return policy which included buying back ¥40 billion of shares.

It is to be noted that this meant that the combined entity was going to be left with less cash than the total deemed necessary by the two companies just a very short while before. Why? Because Alps – with the strong governance it has – obviously had the right amount – and Alpine also had the right amount (it needed substantial equity-funded cash as “working capital” because otherwise it would run a serious danger of business disruption and deterioration. So despite this severe business risk, the two companies effectively announced they would disburse 90% of Alpine’s cash on hand to shareholders POST-MERGER through the special dividend offered to sweeten the pot to get the merger through, and the ¥40 billion buyback.

The merger, of course, went through, and the ¥28.4 billion* buyback is proceeding apace.

Five interesting trends/developments that could impact Thai equities in the recent period:

Legalization of medicinal marijuana. Thailand legalized medicinal use of marijuana at end of February and has already received immense interest from potential growers. At some point, pharma and healthcare companies could be beneficiaries of this trend.

Rumbles in the airline industry. Asia Aviation (AAV TB) , parent company of Thai Air Asia, acquires a stake in competitor Nok Air. This is one of the few signs of industry consolidation in this sector.

MOU signed between TMB and Thanachart. The deal may take longer than initially expected, but the two sides have agreed on some basics such as 70% equity financing and deal size of roughly Bt130-140bn.

Read-through from US Election 2020. Some of the Democrat policies advocated by candidates in 2020 could turn out to be positive for Asian equities.

BGrimm acquires Glow SPP1 for a bargain price of Bt3.3bn, or 55% of the expected price, opening the way for the GPSC-Glow merger, potentially the largest deal of 2019.

Sea Ltd (SE US) is looking to raise about US$1.2bn in its upcoming placement. It will be larger than its IPO in 2017, which raised about US$880m.

The deal scores well on our framework owing to decent valuation, strong price and earnings momentum but had little track record for comparison. The company announced a strong set of FY2018/Q4 2018 results which had beaten estimates.

Even though, the deal size is large, representing 23.2 days of three-month ADV, there is enough time between the announcement to the end of the bookbuild to price in the impact of the placement.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Late last year, in the final run-up to the vote to determine whether Alpine (6816 JP) investors would subject themselves to a bad share exchange ratio or would choose to oblige Alps (6770 JP) to have another run at it in a different format, Alps announced a shareholder return policy which included buying back ¥40 billion of shares.

It is to be noted that this meant that the combined entity was going to be left with less cash than the total deemed necessary by the two companies just a very short while before. Why? Because Alps – with the strong governance it has – obviously had the right amount – and Alpine also had the right amount (it needed substantial equity-funded cash as “working capital” because otherwise it would run a serious danger of business disruption and deterioration. So despite this severe business risk, the two companies effectively announced they would disburse 90% of Alpine’s cash on hand to shareholders POST-MERGER through the special dividend offered to sweeten the pot to get the merger through, and the ¥40 billion buyback.

The merger, of course, went through, and the ¥28.4 billion* buyback is proceeding apace.

Five interesting trends/developments that could impact Thai equities in the recent period:

Legalization of medicinal marijuana. Thailand legalized medicinal use of marijuana at end of February and has already received immense interest from potential growers. At some point, pharma and healthcare companies could be beneficiaries of this trend.

Rumbles in the airline industry. Asia Aviation (AAV TB) , parent company of Thai Air Asia, acquires a stake in competitor Nok Air. This is one of the few signs of industry consolidation in this sector.

MOU signed between TMB and Thanachart. The deal may take longer than initially expected, but the two sides have agreed on some basics such as 70% equity financing and deal size of roughly Bt130-140bn.

Read-through from US Election 2020. Some of the Democrat policies advocated by candidates in 2020 could turn out to be positive for Asian equities.

BGrimm acquires Glow SPP1 for a bargain price of Bt3.3bn, or 55% of the expected price, opening the way for the GPSC-Glow merger, potentially the largest deal of 2019.

Sea Ltd (SE US) is looking to raise about US$1.2bn in its upcoming placement. It will be larger than its IPO in 2017, which raised about US$880m.

The deal scores well on our framework owing to decent valuation, strong price and earnings momentum but had little track record for comparison. The company announced a strong set of FY2018/Q4 2018 results which had beaten estimates.

Even though, the deal size is large, representing 23.2 days of three-month ADV, there is enough time between the announcement to the end of the bookbuild to price in the impact of the placement.

Shenwan Hongyuan filed in November to list in Hong Kong. It is a leading brokerage house in China. With an A-share market capitalization of USD 18 billion, the company plans to issue up to 20% of its shares for an A+H listing. In this insight, we will discuss:

Company’s history.

Comparison with leading Chinese brokers.

Our thoughts on valuation.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Assuming a sum of the parts valuation the shares are cheap. We can assume the fintech business is worth perhaps Y800-900bn (based on 10x ebit, similar to Credit Saison), the domestic e-commerce operation (which makes an operating profit of about Y70bn on revenue of Y450bn) is worth perhaps Y1.2tr (assuming a valuation of 3x sales vs. 3.5x for Amazon). There are other parts of the business which detract and there are others, including a Y350bn plus investment portfolio which add but overall, all this compares with a market cap of a mere Y1.3tr. This suggests the market is thinking that Rakuten is more than throwing its MNO investment of Y600bn away. Given the Governments desire to reduce prices in the mobile market, and its desire for 4 operators, we would suggest this is overly negative. The recent announcement that Lyft will seek an IPO has lifted the share price given its 10% stake in this name (rumoured valuation of $23bn vs. $15bn currently), but we suspect the shares have much further to run. The market knows earnings will be depressed for the next 2 years or so but does not anticipate any recovery thereafter it would appear.

* We believe that the stagnancy in membership was due to the new competitor Ke.com and will make total revenues more volatile in the future.

* We assume total revenues will slow down, but the operating margin will be stable in 2019.

* We compare WUBA’s expected P/E for 2019 with other vertical platforms in China and conclude 17% downside.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.