In this briefing:

- China Zheshang Bank – A Look Beyond Doubling Impairment Costs

- China Mobile 4Q18 Trends Improved Slightly. It Remains Most Exposed to 5G Capex Uncertainty.

- China Unicom Weak 4Q18 Mobile Results Offset by Strength in Fixed Line Business

- US Lake Charles LNG Liquefaction Plant Tendering for Contractors: Positive for TechnipFMC

- Xinyi Energy IPO Preview: Second Time Lucky?

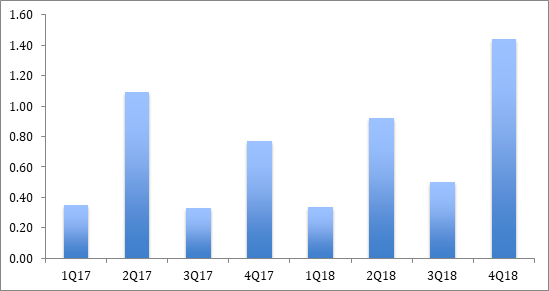

1. China Zheshang Bank – A Look Beyond Doubling Impairment Costs

It should be no surprise to see China Zheshang Bank (2016 HK; “CZB”) reveal a dramatic rise of impairment costs in 4Q18. It is one of only few China banks to yet announced quarterly results, and here it reported profit at -12% YoY in 4Q18. The doubling of impairment costs in the period goes to our long-standing concerns of continued credit tdeterioration in China and well more than headline figures suggest. This is partly based on our China corporate analysis of interest cover and debt/ebitda, which remain weak. It is also notable that CZB has been one of the faster growing banks in the country, putting its ‘unseasoned’ loans higher than many others; where we believe these banks are more likely to see higher impairment costs. Perhaps that is now coming through? And with RMB250bn of write-offs in December 2018 for China’s bank system, this suggests there will have to sizeable impairment costs to replenish balance sheet provisions.

2. China Mobile 4Q18 Trends Improved Slightly. It Remains Most Exposed to 5G Capex Uncertainty.

Chris Hoare downgraded China Mobile (941 HK) some time ago on rising concerns that 5G capex would be higher than expected. While China Unicom (762 HK) and China Telecom (728 HK) both laid out very modest 2019 5G capex plans, China Mobile did not. And despite what we saw as reasonable results, earnings guidance was weak and the lack of a rising dividend payout suggests internal concerns over 5G spending. We had seen China Mobile as a defensive stock, but recent strong performance and rising 5G worries led us to downgrade our recommendation. It remains at Reduce with a HK$75 target.

3. China Unicom Weak 4Q18 Mobile Results Offset by Strength in Fixed Line Business

China Unicom’s (762 HK) recent 4Q18 results were not great. The overall figures look ok due to strength in the fixed line business which offset weakness in mobile. However, they were the weakest of the three operators and the stock, which has had a strong run, now looks due for a pause. We have turned more cautious on the Chinese telcos on concerns that 5G spending could be higher than expected. Chris Hoare believes a major reason for the Chinese telcos outperforming in the past year has come from declining capex spending expectations. That trend may now start to reverse. While China Unicom has guided for only modest 5G capex in 2019 the focus will turn to 2020 where it is a much bigger issue and while we expect China Unicom to do a joint roll-out with China Telecom (728 HK) we expect the scale of the spending to be larger than an individual build.

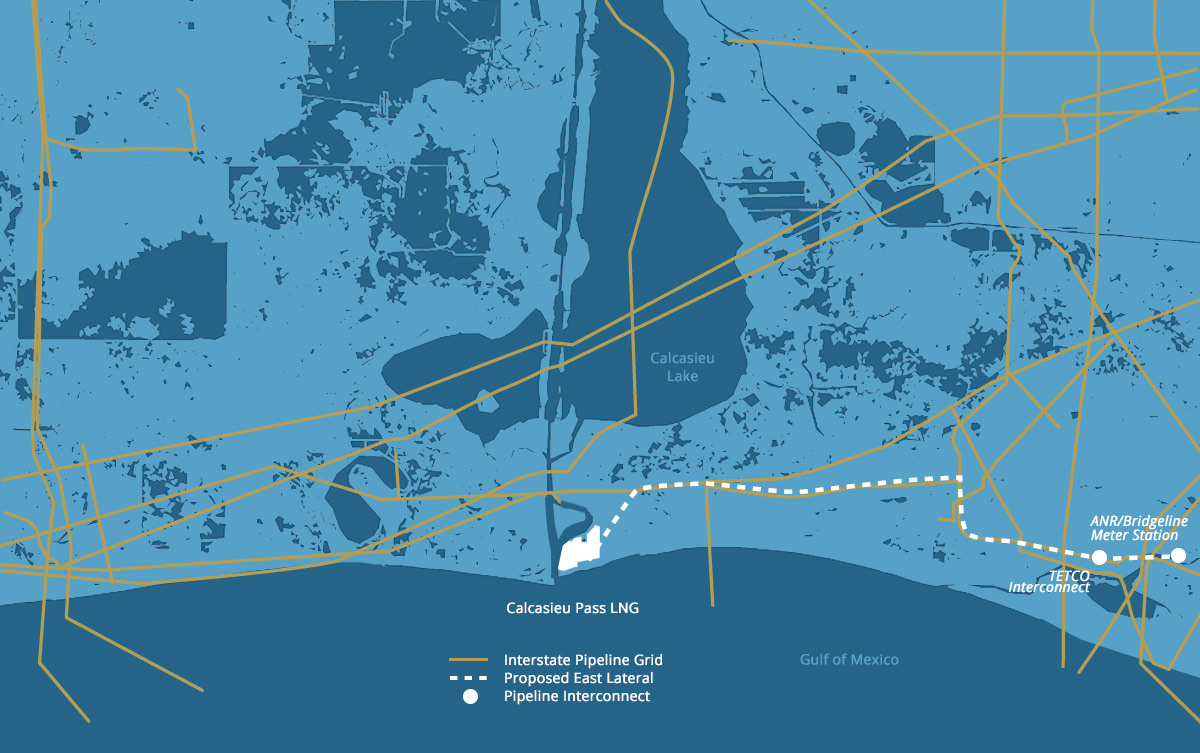

4. US Lake Charles LNG Liquefaction Plant Tendering for Contractors: Positive for TechnipFMC

Energy Transfer LP (ET US) and Royal Dutch Shell (RDSA LN) have signed a Project Framework Agreement to further develop a large-scale LNG export facility in Lake Charles, Louisiana and move toward a potential final investment decision (FID). They have started actively engaging with LNG Engineering, Procurement and Contracting (EPC) companies with a plan to issue an Invitation to Tender (ITT) in the weeks ahead. We look at the potential contract size and winners and also the other US LNG projects that could be negatively impacted. More detail on the LNG project queue for this year in: A Huge Wave of New LNG Projects Coming in the Next 18 Months: Positive for The E&C Companies.

5. Xinyi Energy IPO Preview: Second Time Lucky?

Xinyi Energy Holdings Ltd (1671746D HK) has filed IPO prospectus once again to list its solar generation business that was spun-off from its parent company Xinyi Solar Holding Ltd. Xinyi Energy has 9 operational solar farms with a total capacity of ~950MW.

The company is set to acquire additional solar farms of 540MW capacity from its parent company in a separate transaction post IPO.

Xinyi Energy has not indicated the size and pricing of its offer, however, according to various media reports the company is expected to raise nearly HK$570M (around 12% of the previous offering of HK$4.5B). A significant portion of IPO proceeds is expected to be utilised towards upfront payment of 50% for acquiring solar farms from its parent company and the remainder for working capital and debt repayment. Although we have a positive view of the solar energy sector, the IPO pricing will determine our overall view of the company.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.