In this briefing:

- Screening the Silk Road: (Small-)Mid Cap Free Cash Flow

- Climate Action – School Strikes Hit a Spot, Carbon Emitters Face Heat. Investors Take Note

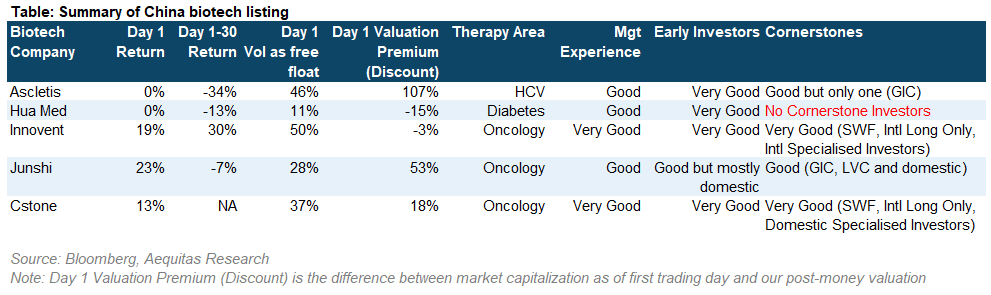

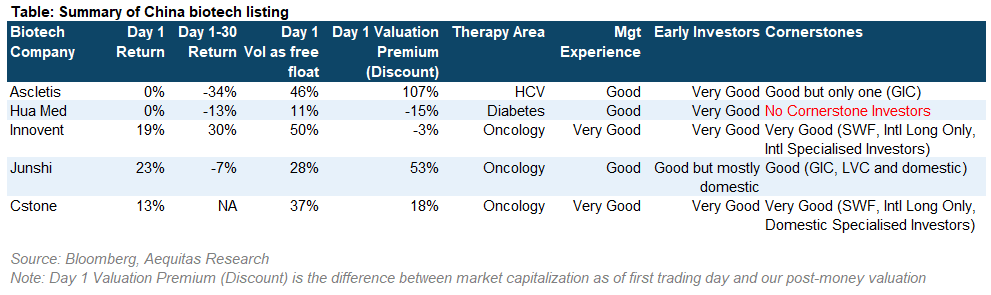

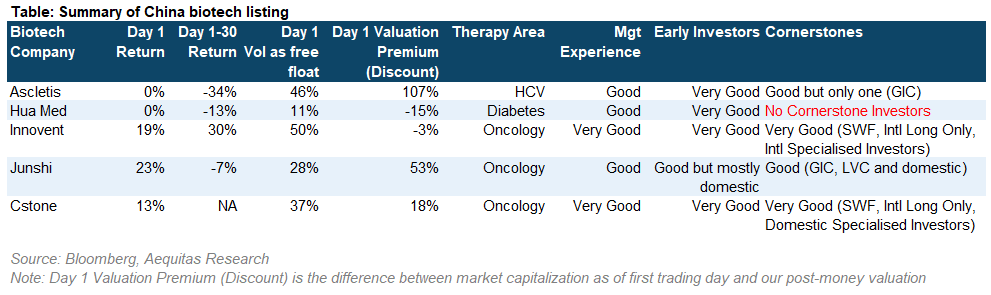

- Jinxin Fertility (锦欣生殖) Pre-IPO: Strong Foothold in Sichuan but Weak Sentiment for Sector

- TRADE IDEA – PCCW (8 HK) Stub: The Li Legacy Lives On

- Dali Foods (3799:HK) FY18 Results: Revenue Growth Collapses in H2, But Margins Hold Up So Far

1. Screening the Silk Road: (Small-)Mid Cap Free Cash Flow

In April 2018, we published a FCF screen with the sole aim of identifying potential names which could prove to be strong candidates in a Small-Mid Cap portfolio. We move to update this list with a strong bias to the mid-cap stocks appearing.

This screen performs well with markets where the value style is in favour. Given the market appears to be trending back to this style, we believe the Small-Mid Cap universe should capitalise on this over the next 12-months. We identify within the screen some high trading liquidity deep value candidates across the Asia Pacific universe.

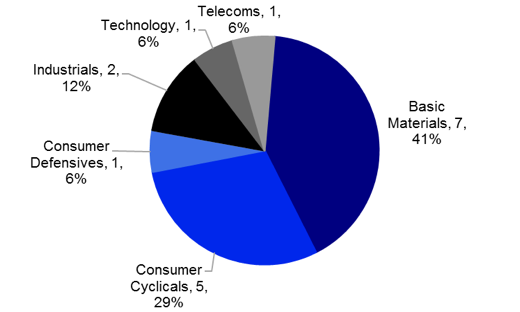

Our updated 2019 list of names contains 17 stocks, with a more diversified spread of countries and sectors, compared to April 2018. A point to note is that basic material stocks have strengthened within the composition. Interestingly, the style of stock which has increased its presence amongst the list is the contrarian style, highlighting an opening up in value.

2. Climate Action – School Strikes Hit a Spot, Carbon Emitters Face Heat. Investors Take Note

On Friday, March 15th, an estimated 1.6 million students in over 120 countries (source: Time magazine) walked out of classrooms and took to streets demanding radical climate action. Climate change activism rarely grabbed headlines or wider public attention as it is doing now. Rising climate activism will continue to train the spotlight on industries/businesses associated with carbon-emission making it increasingly difficult for them to expand capacities or secure funding. Large institutional investors – sovereign funds, pension funds, insurance companies – have begun to incorporate climate risk into investment policy and are limiting exposure to sectors that directly contribute to carbon emissions – primarily coal, crude oil producers and power plants based on them. Expect sector devaluation; active investors may well look beyond juicy near term earnings and dividend yield.

Even as scientists and meteorological organisations keep warning of dire consequences unless concrete action is taken to limit carbon emissions to stall climate change, political establishment/regulators in most countries are in denial while others are doing little more than lip service. If so, should corporates care? even though businesses are the ones that play a direct role in escalating carbon emissions. With rising consumer awareness and activism, several industries associated with carbon emissions are already facing operational and funding challenges; we believe, it pays for all businesses to be above par on ‘climate action’ – it would be in their own self-interest, not just general good. And do Investors bother? Under the aegis of Climate Action 100+, an investor initiative with 320 signatories having more than USD33 trillion in assets collectively under management, they have been engaging companies on improving governance, curbing emissions and strengthening climate-related financial disclosures. It has listed out Oil & Gas, Mining, Utilities and Auto manufacturers as target sectors. Investors have already been making an impact – by vote or exit. It sure makes logical sense to effect positive change and minimise climate risk when you have a long term investment horizon.

In the detailed note below we

- discuss how rising consumer/investor activism and/or political/regulatory changes are posing challenges to key sectors –Coal, Oil & Gas, Automobiles/Aviation, Consumer goods – that are associated with carbon emissions.

- analyse how rising climate activism is negatively impacting growth prospects and valuation of companies in these sectors.

- highlight the opportunities for businesses to capitalise on changing consumer preferences for products that minimise carbon footprint and differentiate themselves by being on the right side of climate action.

- present a quick primer on climate change and lay down the key facts and data on climate change as presented by World Meteorological Organisation, NASA and IPCC.

However, the report does NOT discuss potential risks to businesses from the aftermath of Climate change. Unlike our recently released report Fast Fashion in Asia: Trendy Clothing’s Toxic Trails – Investors Beware that looked into sector’s environmental violations and attempted to estimate potential earnings/growth/valuation downside as leading textile players adopt sustainable practices, we believe the impact of unpredictable climate change poses a threat that is not easy to identify or quantify.

3. Jinxin Fertility (锦欣生殖) Pre-IPO: Strong Foothold in Sichuan but Weak Sentiment for Sector

Jinxin Fertility, a leading privately owned assisted reproductive service provider in China and the US, refiled to list in Hong Kong. Per news reports, the company planned to raise up to USD 500 million. In this insight, we will cover the following topics:

- Business lines and its hospitals

- The assisted reproductive service industry

- Key risks

- Shareholders and use of proceeds

- Our early thoughts on valuation

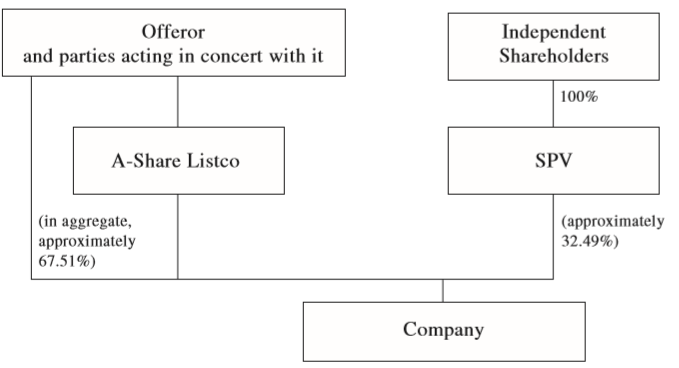

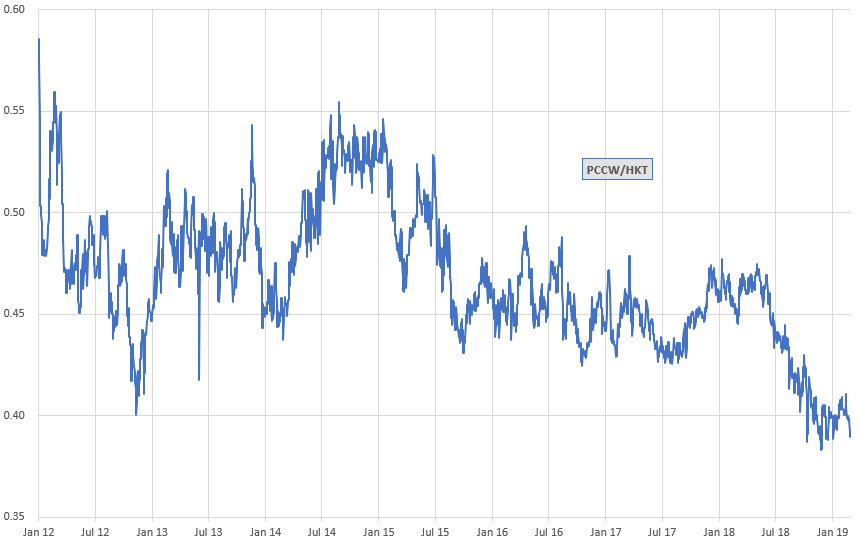

4. TRADE IDEA – PCCW (8 HK) Stub: The Li Legacy Lives On

Have you ever wondered how a company secures the Chinese lucky number “8” as their ticker in Hong Kong? I’ll explain later on, but let’s just say that being the son of Li Ka Shing helps.

Li Ka Shing is a name that hardly needs introduction in Hong Kong and Richard Li, Li Ka Shing’s youngest son and Chairman of PCCW Ltd (8 HK), follows suit. After being born into Hong Kong’s richest family, Richard Li was educated in the US where he worked various odd jobs at McDonald’s and as a caddy at a local golf course before enrolling at Menlo College and eventually withdrawing without a degree. As fate would have it, Mr. Li went on to set up STAR TV, Asia’s satellite-delivered cable TV service, at the tender age of 24. Three years after starting STAR TV, Richard Li sold the venture, which had amassed a viewer base of 45 million people, to Rupert Murdoch’s News Corp (NWS AU) for USD 1 billion in 1993. During the same year, Mr. Li founded the Pacific Century Group and began a streak of noteworthy acquisitions.

You may be starting to wonder what all of this has to do with a trade on PCCW Ltd (8 HK) and I don’t blame you. In the rest of this insight I will:

- finish the historical overview of the Li family and PCCW

- present my trade idea and rationale

- give a detailed overview of the business units of PCCW and the associated performance of each

- recap ALL of my stub trades on Smartkarma and the performance of each

5. Dali Foods (3799:HK) FY18 Results: Revenue Growth Collapses in H2, But Margins Hold Up So Far

We launched coverage of Dali Foods Group (3799 HK) in February with a Sell rating and a HK$4.18 target price. FY18 financial results, which were released late Tuesday March 26th, appear to confirm at least half of our negative thesis (slowing revenue growth), though the other half (margin compression) has failed to materialize so far.

Dali Foods appears to have met — just — the FY18 consensus EPS target of HK$0.307 per share. The company cut its Final dividend from HK$0.10 to HK$0.075 per share.

However, the pace of revenue growth plummeted in H218. From solid growth of +11.4% YoY in H118, H218 revenues actually declined by -0.6% YoY in the latter half of the year. This result was beyond even our pessimistic view and we believe bulls on the company will be forced to revisit their overly optimistic assumptions about double-digit revenue growth in 2019e.

Besides assuming slower revenue growth going forward, the other leg of our negative thesis on Dali Foods was the expectation of margin compression due to rising raw materials costs, specifically for paper and key food and beverage ingredients. Although H218 gross margin declined versus H217 (to 37.7% from 37.8%), it did so only marginally, and probably due to a change in product mix (ie, a decline in high-margin beverage sales).

After reviewing FY and H218 results, we see no reasons to change our negative view of Dali Foods, and our HK$4.18 price target (-26% potential downside) and Sell rating remain unchanged.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.