In this briefing:

- Bilibili Offering: Unnecessary and Opportunistic

- Bilibili Placement: Momentum Bodes Well

- Map Aktif Follow-On Offering – Lace up for a Potential Long Run

- Embassy Office Parks REIT Trading Update – Lowest Volume Traded for Any Indian Listing Since 2018

- Last Week in GER Research: Lyft, Rakuten, Lynas, Yunji IPO, Xinyi IPO and Ruhnn IPO

1. Bilibili Offering: Unnecessary and Opportunistic

On Monday, Bilibili Inc (BILI US) unveiled plans to raise around $192 million (based on the closing price of $18.95 per ADS) through a public offering of 10.6 million ADS and a concurrent offering of $300 million convertible senior notes. Also, certain selling shareholders will offer 6.5 ADS in the offering.

We believe bilibili’s fundamentals are mixed as rapid monthly active users (MAUs) and non-mobile games growth is offset by a declining margin and higher cash burn. Overall, the proposed offering is unnecessary and highly opportunistic, and we would not participate in the offering.

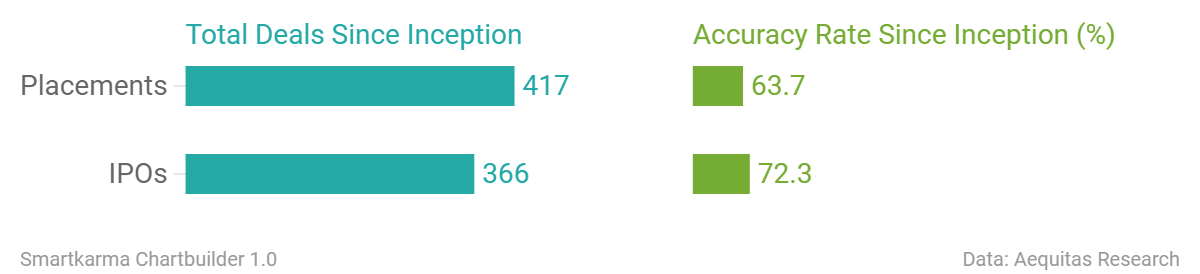

2. Bilibili Placement: Momentum Bodes Well

Bilibili announced a USD 300 million share placement and a USD 300 million convertible note placement after market close on Monday. This is the first major placement since Bilibili’s IPO in March 2018. In this insight, we will provide our thoughts on the deal and score the deal in our ECM Framework.

3. Map Aktif Follow-On Offering – Lace up for a Potential Long Run

CVC is looking to raise about US$353m through the sale of about 648m Map Aktif Adiperkasa PT (MAPA IJ) shares in the follow-on offering.

Map Aktif (MAPA) is a sports, leisure, and kids retailer in Indonesia. It is a subsidiary of Mitra Adiperkasa (MAPI IJ). The selldown might not be totally unexpected as CVC planned to exit its investment by 2020. However, post this selldown it will still have 192m share left.

4. Embassy Office Parks REIT Trading Update – Lowest Volume Traded for Any Indian Listing Since 2018

Embassy Office Parks REIT (EOP IN) raised US$665m in its IPO, making it the first REIT listing for India.

In my previous insights I’ve covered the company background, its projected growth, compared it to its main listed peer and other yield assets in India:

- Embassy Office Parks REIT – Good Assets but Projections Might Be a Tad Too Bullish

- Embassy Office Parks REIT – Comparison with AIT and a Look at the Required Yield, and

- Embassy Office Parks REIT IPO – FY19 Revised Down, Yield Propped up by Zero Coupon Bond

In this insight, I will re-visit some of the deal dynamics, comment on share price drivers and provide a table with implied valuations.

5. Last Week in GER Research: Lyft, Rakuten, Lynas, Yunji IPO, Xinyi IPO and Ruhnn IPO

Below is a recap of the key analysis produced by the Global Equity Research team. This week, we update on Lyft Inc (LYFT US) now that it is below its IPO price and remind of the potentially muted impact for strategic holder Rakuten Inc (4755 JP). On the M&A front, Arun digs into the conditional deal for Lynas Corp Ltd (LYC AU) from Wesfarmers Ltd (WES AU). With regards to IPO research, we initiate on e-commerce player Yunji Inc. (YJ US) and solar company Xinyi Energy Holdings Ltd (1671746D HK) while we update on the IPO valuation of Ruhnn Holding Ltd (RUHN US).

In addition, we have provided an updated calendar of upcoming catalysts for EVENT driven names below.

Best of luck for the new week – Arun, Venkat and Rickin

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.