In this briefing:

- GDS Holdings (GDS US): Placing a Good Opportunity to Gain Exposure to a High Growth Story

- ECM Weekly (16 March 2019) – Embassy Office REIT, Tiger Brokers, Dongzheng Auto, Koolearn, CanSino

- Embassy Office Parks REIT: Why You Should Avoid It

- Koolearn (新东方在线) IPO Review – Yet to See Results from Increased Spending

- NASDAQ:GDS Placement – Visible Growth, Additional Ping An Investment

1. GDS Holdings (GDS US): Placing a Good Opportunity to Gain Exposure to a High Growth Story

Last Friday, Gds Holdings (Adr) (GDS US), the largest third-party data centre operator in China, announced the placing price of its public offering of 11.9 million ADS. At the placing price of $33.50 per share, GDS will raise net proceeds of $385.5 million which will be used for the development and acquisition of new data centres.

We are positive on GDS as the business remains in rude health due to strong revenue growth, rising margins and high revenue visibility. Overall, we would participate in the public offering at the placing price.

2. ECM Weekly (16 March 2019) – Embassy Office REIT, Tiger Brokers, Dongzheng Auto, Koolearn, CanSino

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Starting with bad news in Korea, Homeplus REIT (HREIT KS)‘s IPO was pulled on the 14th of March which when it was supposed to price. The reason cited was weak demand which stemmed from growth concerns and difficulty in valuing this business.

On the other hand, Hong Kong’s IPO market is getting busier. This week alone, we had Dongzheng Automotive Finance (2718 HK) and Koolearn (1797 HK) that have already opened for bookbuilding and will price next week. We also heard that Sun Car Insurance is already started pre-marketing and it will likely open its books next week. The company had only just re-filed their draft prospectus last week.

Another upcoming Hong Kong IPOs would be Tianjin CanSino Biotechnology Inc (1337013D HK) which we heard had already started pre-marketing. Ke Yan, CFA, FRM updated his assumptions and valuation of the company in his insight, CanSino Biologics (康希诺) IPO: Valuation Update (Part 3).

In India, the focus is on Embassy Office Parks REIT (EOP IN) as this is the country’s first ever REIT IPO. It is also the first time there is a strategic tranche in an Indian IPO which has been taken up by Capital Group. Sumeet Singh has pointed out in his insight that with cost of debt of the REIT being at 9 – 9.25%, it is hard to fathom buying equity at a FY2020E dividend yield of 8.25%. This yield had already been inflated by the lack of interest payments. For detailed explanation, read his insight, Embassy Office Parks REIT IPO – FY19 Revised Down, Yield Propped up by Zero Coupon Bond.

In other countries, we heard that Leong Hup International (LEHUP MK) is aiming to pre-market next month whereas, in Australia, there had been chatter that Prospa Advance Pty (PGL AU) may be back for an IPO again after it had beaten its own estimates from the IPO prospectus.

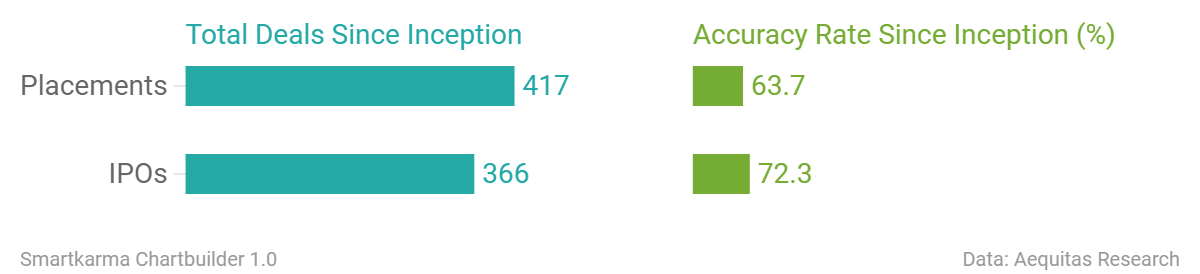

Accuracy Rate:

Our overall accuracy rate is 72.4% for IPOs and 63.7% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

- FriendTimes Inc. (Hong Kong, >US$100m)

- Frontage (Hong Kong, re-filed)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

News on Upcoming IPOs

- UBS and Rivals to Pay $100 Million to Settle Hong Kong IPO Cases

- Chinese Luxury Car Finance Firm Seeks $428 Million in Hong Kong IPO

- Online Educator Koolearn to Raise up to $233 Million in Hong Kong IPO

- Resurgence in Indian IPO market likely only after general elections

- Homeplus K-REIT Withdraws $1.5 Billion Korean IPO on Weak Demand

- Prospa may revive listing plan after beating prospectus forecasts

- Luckin Coffee chairman said to tap banks for $200m loan in exchange for IPO role

This week Analysis on Upcoming IPO

- Homeplus REIT IPO: A Key Landmark Deal in the History of the Korean REIT Market

- Up Fintech (Tiger Brokers) IPO Quick Take – It’s Not like Futu, Won’t Perform like It Either

- Embassy Office Parks REIT IPO – FY19 Revised Down, Yield Propped up by Zero Coupon Bond

- CanSino Biologics (康希诺) IPO: Valuation Update (Part 3)

- Dongzheng Auto Finance (东正汽车金融) IPO Review – Better off Buying the Parent

- Koolearn (新东方在线) IPO Review – Yet to See Results from Increased Spending

3. Embassy Office Parks REIT: Why You Should Avoid It

- Embassy Office Parks REIT (EOP IN) boasts an impressive portfolio of office assets with adequate geographic diversification, strong client relationships and sound reputation.

- Constructing/acquiring new office area is an integral part of Embassy’s growth strategy.

- This requires massive capex (e.g. Embassy’s last 3 year’s capex is Rs32bn). Since it pledges to distribute 100% of its EBITDA to unit holders, it will have no cash left for capex or making interest payments.

- Hence, post the IPO borrowings will increase to fund the capex. The interest expenses will lower the NDCF and in turn Dividend per unit.

- Embassy may choose to issue fresh units to fund part of the capex in the future. This will also result in lower Dividend per unit.

- Ascendas India Trust (AIT SP) shows us why you should be conservative while building in capital appreciation of REIT units. Despite revenues growing 3.18x over FY08-18, Ascendas’ Dividend per unit is flat over the period as its borrowings growth (29% Cagr) far outdid its revenue growth (12.3% Cagr). It also diluted equity to the tune of 37% over the period. Its units have seen no capital appreciation over the last decade.

- Embassy’s effective yield (adjusted for interest outgo notwithstanding its proposed workaround) works out to 6.4%- unattractive in our view.

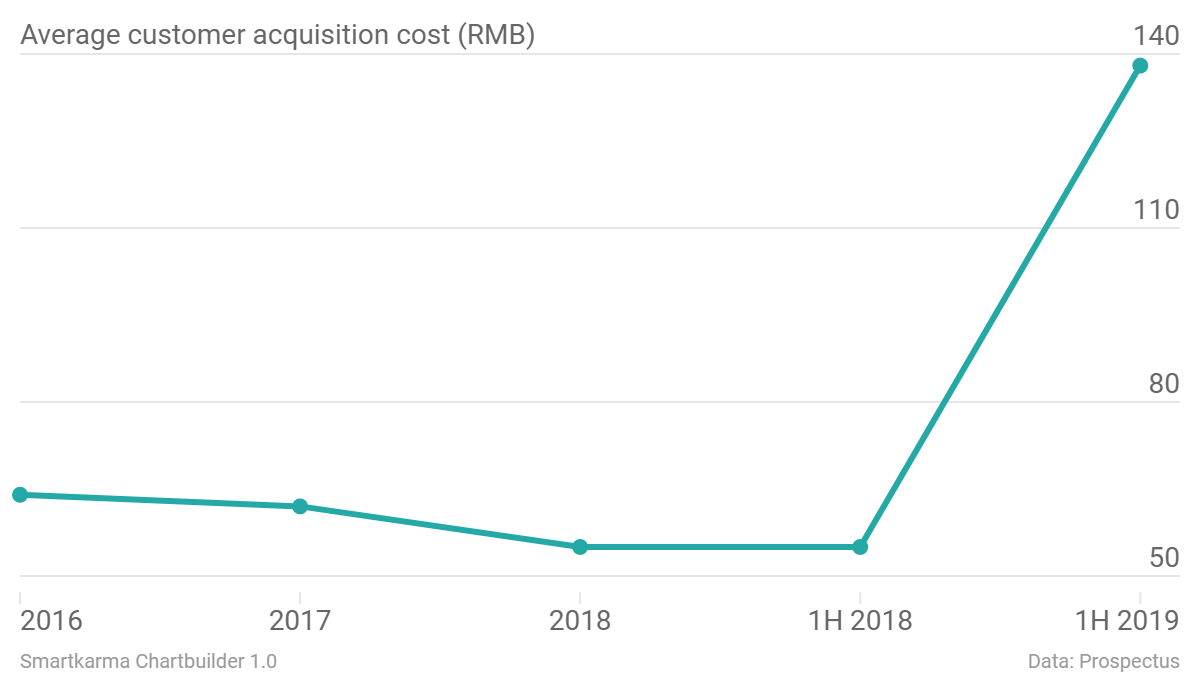

4. Koolearn (新东方在线) IPO Review – Yet to See Results from Increased Spending

Koolearn (1797 HK) is looking to raise up to US$S234m in its upcoming IPO. We have previously covered the company in:

- Koolearn (新东方在线) Pre-IPO – Profitable Online Edu Company but Poor Sentiment Weighs

- New Regulatory Tightening on Online Education Reads Badly on Koolearn IPO

In this insight, we will look at the updates on financials and operating metrics, compare it to other listed online education companies, and run the deal through our framework.

The increase in spending on marketing has not yielded the intended results as the growth rates of student enrollment and gross billings slowing down. Furthermore, aggressive spending behavior is similar to that of STG and LAIX and both companies did not perform well post listing.

5. NASDAQ:GDS Placement – Visible Growth, Additional Ping An Investment

GDS Holding, the largest carrier-neutral, cloud-neutral data centre operator in China, is raising USD 400 million from a private placement. The deal was launched last night (US time) post the company’s results announcement. In this insight, we will cover:

- Details of the deal

- Key takeaways from its 4Q2018 results

- USD 150 million investment by Ping An

- Its shareholders

- The score in our Placement Framework

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.