Just as Pinduoduo (PDD US) lock-up expiry date (22nd January) is approaching, there was news of a massive bug that could result in an RMB20bn loss for PDD. According to the company’s official Weibo account, the bug has already been rectified and a police report has been filed.

In this insight, we will analyze the potential impact of the bug and the number of shares that could potentially be sold upon lock-up expiry.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Toppan Printing (7911 JP) is looking to sell 10.5m shares in Recruit Holdings (6098 JP) for about US$263m. Post-placement, Toppan Printing will still have about 6% stake (103m shares) in Recruit Holdings.

The deal scores well on our framework owing to its strong price and earnings momentum and stellar track record. However, it was offset by its relatively expensive valuation compared to peers. The selldown by Toppan Printing is tiny relative to the three-month ADV which the market would likely be able to absorb. The sell down is also long overdue considering that Toppan Printing skipped the 2016 secondary offering in which many shareholders have participated.

Maoyan Entertainment (EPLUS HK) is the largest online movie ticketing service provider in China. The mid-point of Maoyan’s IPO price range of HK$14.8-20.4 per share implies a market value of $2.5 billion (HK$19.8 billion). Five cornerstone investors have agreed to buy $30 million or 10% of the offering at the IPO mid-point. The cornerstone investors are Imax China Holding (1970 HK), Hylink Digital Solutions, Prestige of The Sun, Welight Capital and Xiaomi Corp (1810 HK).

Our analysis suggests Maoyan is being offered at a material premium to a peer group of major Chinese internet companies. Due to challenging prospects faced by Maoyan as outlined in our previous research, we believe a premium rating is unwarranted. Consequently, we are inclined to sit out this IPO.

HET has grown its revenue at an impressive 73% CAGR from 2015 to 2017 and has been accompanied by gross margin expansion. The strong growth was supported by improving operating metrics such as an increase in student enrollment and average spending.

However, HET has been making losses and continues to spend more than its net billing. It is unclear whether HET had already achieved break even for its proprietary courses before expanding into its CCtalk platform. But from its high level of expenses, it seems unsustainable for HET to be relying heavily on the sales and marketing spending to get users to purchase online courses.

In this insight, we will look into the company’s financial and operating performance, regulatory risks regarding K12 courses, aggressive spending on sales and marketing, and the performance of other online education companies.

Polycab India (POLY IN) plans to raise around US$280m in its IPO through a mix of selling primary and secondary shares. It is the largest manufacturer of wires and cables in India with a 12% market share, as per CRISIL research. The company has also recently entered the consumer electrical segments.

Sales growth has been decent while margin expansion has helped the company to report much higher PATMI growth. Although, cash flow from operations has lagged earnings growth as working capital requirements have been volatile. In addition, receivables quality seems to be deteriorating. To add to that the rationale for the dealers and employees rationalization hasn’t been clearly explained.

In this insight, I’ve covered the above points, compared the company to its listed peers and commented on valuations. Should the deal be offered at multiples close to its wires and cables peers, it might still be interesting.

Maoyan Entertainment (formerly Entertainment Plus) launched its institutional book building last Friday. We covered the company’s background, industry backdrop, financials, shareholders and the regulatory overhang in our previous two notes.

In this note, we will look at the recent development of the company, based on the data from the prospectus and our channel checks. We will also discuss the valuation of the company.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

HET has grown its revenue at an impressive 73% CAGR from 2015 to 2017 and has been accompanied by gross margin expansion. The strong growth was supported by improving operating metrics such as an increase in student enrollment and average spending.

However, HET has been making losses and continues to spend more than its net billing. It is unclear whether HET had already achieved break even for its proprietary courses before expanding into its CCtalk platform. But from its high level of expenses, it seems unsustainable for HET to be relying heavily on the sales and marketing spending to get users to purchase online courses.

In this insight, we will look into the company’s financial and operating performance, regulatory risks regarding K12 courses, aggressive spending on sales and marketing, and the performance of other online education companies.

Polycab India (POLY IN) plans to raise around US$280m in its IPO through a mix of selling primary and secondary shares. It is the largest manufacturer of wires and cables in India with a 12% market share, as per CRISIL research. The company has also recently entered the consumer electrical segments.

Sales growth has been decent while margin expansion has helped the company to report much higher PATMI growth. Although, cash flow from operations has lagged earnings growth as working capital requirements have been volatile. In addition, receivables quality seems to be deteriorating. To add to that the rationale for the dealers and employees rationalization hasn’t been clearly explained.

In this insight, I’ve covered the above points, compared the company to its listed peers and commented on valuations. Should the deal be offered at multiples close to its wires and cables peers, it might still be interesting.

Maoyan Entertainment (formerly Entertainment Plus) launched its institutional book building last Friday. We covered the company’s background, industry backdrop, financials, shareholders and the regulatory overhang in our previous two notes.

In this note, we will look at the recent development of the company, based on the data from the prospectus and our channel checks. We will also discuss the valuation of the company.

Just as Pinduoduo (PDD US) lock-up expiry date (22nd January) is approaching, there was news of a massive bug that could result in an RMB20bn loss for PDD. According to the company’s official Weibo account, the bug has already been rectified and a police report has been filed.

In this insight, we will analyze the potential impact of the bug and the number of shares that could potentially be sold upon lock-up expiry.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Polycab India (POLY IN) plans to raise around US$280m in its IPO through a mix of selling primary and secondary shares. It is the largest manufacturer of wires and cables in India with a 12% market share, as per CRISIL research. The company has also recently entered the consumer electrical segments.

Sales growth has been decent while margin expansion has helped the company to report much higher PATMI growth. Although, cash flow from operations has lagged earnings growth as working capital requirements have been volatile. In addition, receivables quality seems to be deteriorating. To add to that the rationale for the dealers and employees rationalization hasn’t been clearly explained.

In this insight, I’ve covered the above points, compared the company to its listed peers and commented on valuations. Should the deal be offered at multiples close to its wires and cables peers, it might still be interesting.

Maoyan Entertainment (formerly Entertainment Plus) launched its institutional book building last Friday. We covered the company’s background, industry backdrop, financials, shareholders and the regulatory overhang in our previous two notes.

In this note, we will look at the recent development of the company, based on the data from the prospectus and our channel checks. We will also discuss the valuation of the company.

Just as Pinduoduo (PDD US) lock-up expiry date (22nd January) is approaching, there was news of a massive bug that could result in an RMB20bn loss for PDD. According to the company’s official Weibo account, the bug has already been rectified and a police report has been filed.

In this insight, we will analyze the potential impact of the bug and the number of shares that could potentially be sold upon lock-up expiry.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Weimob.com (2013 HK) IPO was priced at the low-end at HKD2.80/share. The retail tranche was 0.79x covered while the institutional tranche was slightly over-subscribed.

I’ve covered most aspects of the deal in my earlier insights:

In this insight, I’ll provide an update on the deal dynamics, valuations and provide a table with the implied valuations at different share price levels.

Overall, the company has continued to show that its undergraduate program is the driver behind its growth. It grew its 8M 2018 revenue and gross profit both by about 24% YoY. However, there are significant near-term risks if the MOJ Draft for Comments gets implemented. It may result in Kepei registering its schools as for-profit private schools which would shrink its net profit margin.

In this insight, we will provide updates on the company’s 8M 2018 financials and operating performance, the potential impact of policy change and compare its valuation to other listed education peers. We will also run the deal through our framework.

Japan Hotel Reit Investment (8985 JP) (JHR) plans to raise around US$300m/JPY33bn to part fund the acquisition of Hilton properties located in Tokyo and Osaka.

We have previously covered four other capital raising by JHR:

The prior-deals have given mixed bag results over the short-term. In this insight, we will run the deal through our framework and analyse past performance.

We expect Chinese domestic express demand to continue to moderate in 2019, and in response we expect the express companies to increase their investments in ‘last-mile’ and international delivery, which will probably create a drag on profitability in the medium-term. Although we believe e-commerce giants Alibaba and JD.com would like their growing portfolios of logistics investments to become self-funding sooner rather than later, we foresee somewhat limited investor appetite for more large Chinese logistics IPOs in 2019, since many high-profile offerings have faltered since going public.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We are bullish on the Chunbo Co. IPO. Our base case valuation of the company suggests a market cap of 448.4 billion won or44,845 won, which would be 19.5% higher than the mid-point of the bankers’ IPO price band of 37,500 won. We used an estimated P/E of 21.1x (30% premium to the comps’ average P/E of 16.2x) and an estimated net profit of 21.2 billion won in 2019 to derive our base case valuation.

Chunbo Co Ltd (278280 KS) is a provider of fine chemical materials in Korea, is planning to start its institutional bookbuilding of its IPO starting January 21st. Its chemical materials are used in numerous industries including the display, semiconductors, rechargeable batteries, and medical. The IPO base deal size is between $78 million to $89 million.

Chunbo is more profitable and generates higher returns on equity than its peers. For example, Chunbo’s operating margin and ROE averaged 20.7% and 22.0%, respectively in 2016 and 2017. In comparison, the peers’ operating margin and ROE averaged 12.3% and 15.2%, respectively in 2016 and 2017.

As per Technopak, BFS is one of the leading manufacturers in the non-glucose biscuit segment in Northern India. It is also one of the largest supplier of buns to the quick-service restaurants and a leading supplier of breads in Delhi NCR and Maharashtra. In addition to its Indian operations, exports account for 30% of the revenue.

Despite providing a host of numbers, the company has failed to provide clear statistics on the growth of revenue of its main segment, domestic biscuits. If one tries to back out this numbers from the other statistics it seems to imply that revenue has been flat for five years. Despite showing some revenue and PATMI growth over the past five years, cash flow from operations as well have been stagnant.

An undisclosed institutional shareholder of Xiaomi Corp (1810 HK) is looking to sell 231m shares of the company for approximately US$273m.

There will likely to be more selling pressure in the near term. The 594m shares sold down by Apoletto and the anonymous shareholder who sold at a 14% discount does not inspire confidence. Furthermore, there will be even more overhang to come from the twelve-month lock-up expiry. The deal also scores poorly on our framework owing to its expensive valuation and the lack of information on the seller.

Mitsubishi Corp (8058 JP) is looking to sell 9m shares of Ayala Corporation (AC PM) for approximately US$155m. Post-placement, Mitsubishi Corp will still hold 7.2% of Ayala Corp if the upsize option is not exercised.

The deal scores poorly on our framework owing to its the large deal size relative to its three-month ADV. The company is also slightly more leveraged than its peers. However, it was offset by cheaper valuation and a strong track record.

But, our deal breaker here is the fact that the selldown one year after 2018’s selldown may signal that Mitsubishi Corp. may return to sell more on the market again in the near-term. While Mitsubishi, in the past, has reaffirmed that their partnership with AC will likely continue, it should not serve as a reassurance that it will continue to hold shares in AC.

In this insight, we will update on the deal dynamics, implied valuation, and include a valuation sensitivity table.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The founding team comes mostly from Tencent, which might explain Tencent’s large stake in the company. Growth for the company has been stupendous despite the jittery markets, with margin financing adding to the top-line growth.

While its low costs will help it to steal clients from the more traditional brokers, other new low-cost brokers seem to be offering similar services at comparable rates. In addition, the company is not licensed or regulated by any entities in China, despite the majority of its client base being Chinese nationals. Furthermore, the company plans to expand into newer overseas market where it doesn’t seem to have much of a cost advantage.

China Tobacco International (GHALPZ CH) is a subsidiary and offshore unit of China National Tobacco Corp., a state-owned enterprise (SOE). The company procures tobacco leaves from regions around the world and exports tobacco leaf products and branded cigarettes to the duty-free outlets outside China’s customs area and in Southeast Asia.

The IPO is expected to raise US$100M and the company expects to use the proceeds to expand market share, acquire new cigarette brands, working capital, and other corporate purposes.

Futu Holdings Ltd (FHL US) is the fourth largest online broker in Hong Kong. Futu has filed for a Nasdaq IPO to raise $300 million, down from an earlier indication of a $500 million raise according to press reports. Futu is backed by Tencent Holdings (700 HK) (38.2% shareholder), Matrix Partners (6.1%) and Sequoia Capital (4.0%).

At first glance, Futu appears to be a winning new economy company as its rapid revenue growth has been accompanied by rising margins. However, on closer inspection, we believe that Futu’s fundamentals are at best mixed.

In August 2017, Honda stole the top spot in Thai passenger cars from Toyota and held it for a few months. They are still formidable players, and ACG (AutoCorp) which runs Honda dealerships and service centers across Thailand, is expected to IPO some time in 2019. Here’s our quick look at the company.

We value this IPO at Bt2/sh using DCF, since there’s really no good comparables. The company is expected to enjoy slower revenue growth and higher margins going forward as car sales slow down nationally and maintenance becomes a bigger chunk of the revenues.

They only operate in four provinces and run 8 showrooms with over 6,000 sqm of display space. The service centers account for almost 17,200 sqm. The big chunk comes from lower margin car sales. Along with accessories, these account for 84% of revenues.

The IPO is firmly underwritten by Singapore’s Phillips Securities and is good for more than a quarter of shares outstanding (26%). The founding Rangkanuwat family control all remaining shares and have committed to 6 month lock-up period.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Leong Hup International (LEHUP MK) is one of the largest producers of poultry, eggs and livestock feeds in Southeast Asia. After an unusually quite 2018, Malaysia’s equity capital market is set for rebound with at least three issuers looking to raise up to $500 million from IPOs. Leong Hup is set to the be the first as it has started the search for cornerstone investors.

Helped by the current imbalance between available Malaysian IPOs and the dry powder among investors, Leong Hup is seeking a premium rating. However, our analysis suggests the ability of Leong Hup to command a premium rating faces challenges.

Metropolis Health Services Limited (MHL IN) is the 3rd largest pathology chain in India and caters to the Rs600bn market growing at 15% Cagr. It is strongest in the lucrative Mumbai and Chennai markets.

Though India’s pathology market has seen intense price competition and price discounting, Metropolis managed to grow revenue/patient much ahead of peers

Its revenue/patient is 20% higher than its nearest competitor and the gap has been widening over FY16-18

It is the only major pathology chain to have accelerated revenue growth over FY16-18 despite the lowest A&P spend

It managed to grow Gross Margin 330bps and hold Ebitda margins over FY16-18. Major competitors like Dr Lal Pathlabs (DLPL IN) (-340bps) and SRL (-520bps) saw sharp contraction in Ebitda margins.

On the flip side, its patient growth has lagged its retail network growth by a wide margin. Its cash conversion cycle is much longer than DLAL’s. It is also the most vulnerable to any government regulated price caps on testing in the future owing to its premium pricing.

Lastly, it doesn’t need any fresh money and the entire IPO is an offer for sale by the promoters and Carlyle Group.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Despite a shaky 2018 Q4 market and the disappointing Softbank Corp (9434 JP)‘s IPO, we have been getting a steady stream of newsflow on upcoming IPOs.

Starting with upcoming IPOs, Chengdu Expressway Company Limited (1785 HK) and Weimob.com (2013 HK) will be listing next week on Tuesday, 15th January. Weimob was priced at the low end of its price range while Chengdu Expressway’s IPO was at a fixed price of HK$2.20. We are bearish on both IPOs. Weimob is overly reliant on Tencent for its SaaS and Ads business and, at the same time, Tencent will only own less than 3% stake after listing. Whereas Chengdu Expressway has been a well-managed company but valuation implies limited upside. Trading liquidity will likely remain tepid as like Qilu Expressway Co Ltd (1576 HK) which listed mid last year.

In the pipeline, we are hearing that Kepei Education (KEPEI HK) will likely open its book next Monday. We will be following up with a note on valuation. In other IPOs that are coming in this quarter, Helenbergh China and Zhongliang, both property developers, are looking to IPO in this quarter. Viva Biotech Shanghai Ltd (1577881D HK) is also looking to list in Hong Kong Q2 while Urban Commons, a US property developer, is planning a US$500m REIT IPO in Singapore.

Activity seems healthy for the ECM space, but sentiment has not been the best as seen from Xiaomi’s high profile IPO that took a hit just as its lockup expired. Its share price has corrected from a high of HK$22.20 to just above HK$10.34 this Friday. This should not have been a big surprise since many have already pointed out that its valuation should really have been closer to that of a hardware business and we pointed out that the IPO’s trajectory would likely be similar to Razer.

This reminds us of a particular listing last year, Razer Inc (1337 HK) , and, in fact, both bear quite a handful of similarities. Strong portfolio of investors, hardware business with software capabilities, expensive valuations, and etc. The stock did well at first but has come back down to earth since then.

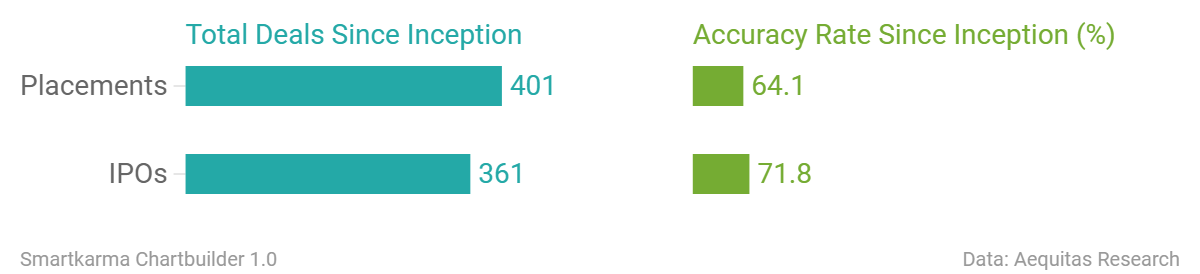

Accuracy Rate:

Our overall accuracy rate is 72% for IPOs and 64% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

China Tobacco International (Hong Kong, US$100m)

China East Education (Hong Kong, US$400m)

Ebang International (Hong Kong, re-filed)

MicuRx Pharma (Hong Kong, re-filed)

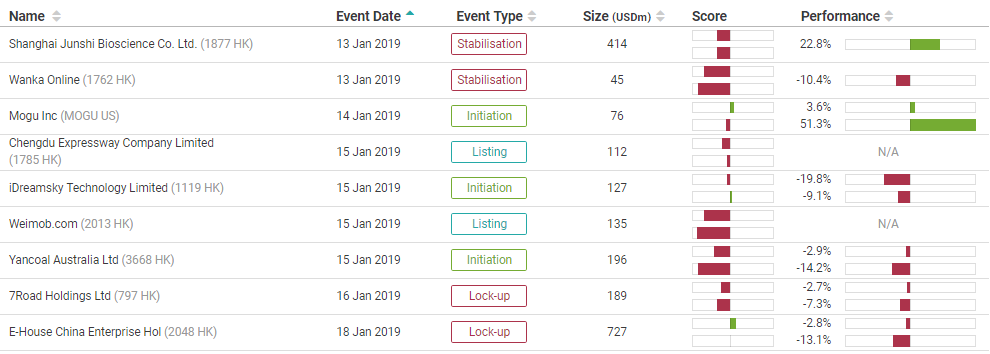

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Over 2017-18, the Australian Securities & Investments Commission (ASIC) undertook a review of allocation in equity raising transactions. The review involved large and mid-sized licensees (brokers), Issuers, International investors and other international regulators. The results of the review were published by ASIC in Dec 2018. This insight highlights some of the key findings.

It’s good to see that some of the standard practices of banks allocating more to existing clients and participants of earlier deals have at least been acknowledged. Even though some institutional investors have outright labelled the allocation process as a “black box”, ASIC doesn’t seem to want to do much about it.

The area where ASIC is more concerned is the messaging to investors which highlights the different definitions of “well-covered” across banks. Although, the banks seem to have mislead the regulator on interpretation of “real-demand” with ECM bankers saying that all orders are taken at face-value. That raises a whole new level of questions on the messaging around demand for the deal.

China Xinhua Education (2779 HK) listed in Q1 of 2018 and we wrote in our insight that the founder had vocational schools that have been separated from China Xinhua that seemed to be his prized asset. Fast forward to December 2018, the prized asset has finally filed its draft prospectus under the entity China East Education (CEE HK) and it is looking to raise US$400m in its IPO.

In this insight, we will analyze the company’s financial and operating performance, compare it to listed education companies, and provide some questions we have for management.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We expect Chinese domestic express demand to continue to moderate in 2019, and in response we expect the express companies to increase their investments in ‘last-mile’ and international delivery, which will probably create a drag on profitability in the medium-term. Although we believe e-commerce giants Alibaba and JD.com would like their growing portfolios of logistics investments to become self-funding sooner rather than later, we foresee somewhat limited investor appetite for more large Chinese logistics IPOs in 2019, since many high-profile offerings have faltered since going public.

Leong Hup International (LEHUP MK) is one of the largest producers of poultry, eggs and livestock feeds in Southeast Asia. After an unusually quite 2018, Malaysia’s equity capital market is set for rebound with at least three issuers looking to raise up to $500 million from IPOs. Leong Hup is set to the be the first as it has started the search for cornerstone investors.

Helped by the current imbalance between available Malaysian IPOs and the dry powder among investors, Leong Hup is seeking a premium rating. However, our analysis suggests the ability of Leong Hup to command a premium rating faces challenges.

Metropolis Health Services Limited (MHL IN) is the 3rd largest pathology chain in India and caters to the Rs600bn market growing at 15% Cagr. It is strongest in the lucrative Mumbai and Chennai markets.

Though India’s pathology market has seen intense price competition and price discounting, Metropolis managed to grow revenue/patient much ahead of peers

Its revenue/patient is 20% higher than its nearest competitor and the gap has been widening over FY16-18

It is the only major pathology chain to have accelerated revenue growth over FY16-18 despite the lowest A&P spend

It managed to grow Gross Margin 330bps and hold Ebitda margins over FY16-18. Major competitors like Dr Lal Pathlabs (DLPL IN) (-340bps) and SRL (-520bps) saw sharp contraction in Ebitda margins.

On the flip side, its patient growth has lagged its retail network growth by a wide margin. Its cash conversion cycle is much longer than DLAL’s. It is also the most vulnerable to any government regulated price caps on testing in the future owing to its premium pricing.

Lastly, it doesn’t need any fresh money and the entire IPO is an offer for sale by the promoters and Carlyle Group.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Despite a shaky 2018 Q4 market and the disappointing Softbank Corp (9434 JP)‘s IPO, we have been getting a steady stream of newsflow on upcoming IPOs.

Starting with upcoming IPOs, Chengdu Expressway Company Limited (1785 HK) and Weimob.com (2013 HK) will be listing next week on Tuesday, 15th January. Weimob was priced at the low end of its price range while Chengdu Expressway’s IPO was at a fixed price of HK$2.20. We are bearish on both IPOs. Weimob is overly reliant on Tencent for its SaaS and Ads business and, at the same time, Tencent will only own less than 3% stake after listing. Whereas Chengdu Expressway has been a well-managed company but valuation implies limited upside. Trading liquidity will likely remain tepid as like Qilu Expressway Co Ltd (1576 HK) which listed mid last year.

In the pipeline, we are hearing that Kepei Education (KEPEI HK) will likely open its book next Monday. We will be following up with a note on valuation. In other IPOs that are coming in this quarter, Helenbergh China and Zhongliang, both property developers, are looking to IPO in this quarter. Viva Biotech Shanghai Ltd (1577881D HK) is also looking to list in Hong Kong Q2 while Urban Commons, a US property developer, is planning a US$500m REIT IPO in Singapore.

Activity seems healthy for the ECM space, but sentiment has not been the best as seen from Xiaomi’s high profile IPO that took a hit just as its lockup expired. Its share price has corrected from a high of HK$22.20 to just above HK$10.34 this Friday. This should not have been a big surprise since many have already pointed out that its valuation should really have been closer to that of a hardware business and we pointed out that the IPO’s trajectory would likely be similar to Razer.

This reminds us of a particular listing last year, Razer Inc (1337 HK) , and, in fact, both bear quite a handful of similarities. Strong portfolio of investors, hardware business with software capabilities, expensive valuations, and etc. The stock did well at first but has come back down to earth since then.

Accuracy Rate:

Our overall accuracy rate is 72% for IPOs and 64% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

China Tobacco International (Hong Kong, US$100m)

China East Education (Hong Kong, US$400m)

Ebang International (Hong Kong, re-filed)

MicuRx Pharma (Hong Kong, re-filed)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Over 2017-18, the Australian Securities & Investments Commission (ASIC) undertook a review of allocation in equity raising transactions. The review involved large and mid-sized licensees (brokers), Issuers, International investors and other international regulators. The results of the review were published by ASIC in Dec 2018. This insight highlights some of the key findings.

It’s good to see that some of the standard practices of banks allocating more to existing clients and participants of earlier deals have at least been acknowledged. Even though some institutional investors have outright labelled the allocation process as a “black box”, ASIC doesn’t seem to want to do much about it.

The area where ASIC is more concerned is the messaging to investors which highlights the different definitions of “well-covered” across banks. Although, the banks seem to have mislead the regulator on interpretation of “real-demand” with ECM bankers saying that all orders are taken at face-value. That raises a whole new level of questions on the messaging around demand for the deal.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

China Xinhua Education (2779 HK) listed in Q1 of 2018 and we wrote in our insight that the founder had vocational schools that have been separated from China Xinhua that seemed to be his prized asset. Fast forward to December 2018, the prized asset has finally filed its draft prospectus under the entity China East Education (CEE HK) and it is looking to raise US$400m in its IPO.

In this insight, we will analyze the company’s financial and operating performance, compare it to listed education companies, and provide some questions we have for management.

The founding team comes mostly from Tencent, which might explain Tencent’s large stake in the company. Growth for the company has been stupendous despite the jittery markets, with margin financing adding to the top-line growth.

While its low costs will help it to steal clients from the more traditional brokers, other new low-cost brokers seem to be offering similar services at comparable rates. In addition, the company is not licensed or regulated by any entities in China, despite the majority of its client base being Chinese nationals. Furthermore, the company plans to expand into newer overseas market where it doesn’t seem to have much of a cost advantage.

China Tobacco International (GHALPZ CH) is a subsidiary and offshore unit of China National Tobacco Corp., a state-owned enterprise (SOE). The company procures tobacco leaves from regions around the world and exports tobacco leaf products and branded cigarettes to the duty-free outlets outside China’s customs area and in Southeast Asia.

The IPO is expected to raise US$100M and the company expects to use the proceeds to expand market share, acquire new cigarette brands, working capital, and other corporate purposes.

Futu Holdings Ltd (FHL US) is the fourth largest online broker in Hong Kong. Futu has filed for a Nasdaq IPO to raise $300 million, down from an earlier indication of a $500 million raise according to press reports. Futu is backed by Tencent Holdings (700 HK) (38.2% shareholder), Matrix Partners (6.1%) and Sequoia Capital (4.0%).

At first glance, Futu appears to be a winning new economy company as its rapid revenue growth has been accompanied by rising margins. However, on closer inspection, we believe that Futu’s fundamentals are at best mixed.

In August 2017, Honda stole the top spot in Thai passenger cars from Toyota and held it for a few months. They are still formidable players, and ACG (AutoCorp) which runs Honda dealerships and service centers across Thailand, is expected to IPO some time in 2019. Here’s our quick look at the company.

We value this IPO at Bt2/sh using DCF, since there’s really no good comparables. The company is expected to enjoy slower revenue growth and higher margins going forward as car sales slow down nationally and maintenance becomes a bigger chunk of the revenues.

They only operate in four provinces and run 8 showrooms with over 6,000 sqm of display space. The service centers account for almost 17,200 sqm. The big chunk comes from lower margin car sales. Along with accessories, these account for 84% of revenues.

The IPO is firmly underwritten by Singapore’s Phillips Securities and is good for more than a quarter of shares outstanding (26%). The founding Rangkanuwat family control all remaining shares and have committed to 6 month lock-up period.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.