In this briefing:

- New J Hutton – Exploration Report (Weeks Ending 22/03/22)

- Cupid Ltd: Attractive Valuation Post Significant Correction

- SNK Corp IPO Preview

- Jinxin Fertility (锦欣生殖) Pre-IPO: Strong Foothold in Sichuan but Weak Sentiment for Sector

- Cracking the Keyence Conundrum

1. New J Hutton – Exploration Report (Weeks Ending 22/03/22)

- Uranium Price has fallen 7% over the past two months

- Actively looking for uranium short positions

- Provide summarised watch list

- Wisdom from Samuel Longhorne Clemens

- Yellow Cake PLC (YCA LN), Berkeley Energy (BKY AU), Cameco Corp (CCO CN), Kazatomprom Natsionalnaya At (KZAP KZ), Jangada Mines PLC (JAN LN), Europa Metals Ltd (EUZ LN), Buxton Resources (BUX AU), Musgrave Minerals (MGV AU), Myanmar Metals (MYL AU), Archer Exploration (AXE AU), Canyon Resources (CAY AU), Catalyst Metals (CYL AU), Core Exploration (CXO AU), Exore Resources (ASX: ERX), Stavely Minerals (SVY AU), Tietto Minerals Ltd (TIE AU), Horizonte Minerals PLC (HZM LN), Bellevue Gold (ASX: BGL), Allegiance Coal (AHQ AU), First Au (ASX: FAU), Base Resources (BSE AU), Breaker Resources Nl (BRB AU)

2. Cupid Ltd: Attractive Valuation Post Significant Correction

Cupid Ltd one of the largest manufacturers of condoms in India 9MFY19 revenue was largely as per our expectations, as there was some order slippages. As forecasted in our initiation report Cupid Ltd: Protecting the Needy, the company reported a 20% decline in revenue at Rs 505mn, which also resulted in lower profitability both at the operating as well as net level. EBITDA stood at INR 161.6 mn declining by 32.53% with EBITDA margin at 31.95%. PAT was INR 108.5 mn declining by 24.58% with PAT margin at 21.46%.

Despite this below-par performance in the 9MFY19, we are fairly positive on the future growth prospects of the company. As of March 2019, it has a healthy order book of INR 1300 m with Book to Bill ratio of 1.99 times on its TTM sales. We expect revenues to grow at 15% over FY18-19 and margins to improve in medium to long term horizon.

Having corrected by 67% from its peak, the stock currently trades at 10.20x its FY19 EPS and 8.34x its FY20 EPS; we believe that this provides a good entry point for this niche high margin healthcare company with attractive long term growth possibilities.

3. SNK Corp IPO Preview

SNK Corp (950180 KS), a Japanese game company founded in 1978, is trying to complete its IPO in the Korean stock market (KOSDAQ) in April. SNK is well known its The King of Fighters game. The IPO price range is between 30,800 won and 40,400 won. The IPO base deal size ranges from $114 million to $150 million.

This is the second time that SNK Corp is trying to complete the IPO after a failed attempt in late 2018. The company has reduced the average IPO price range by 12% this time compared to the first try in late 2018.

The bankers used four comparable companies including Webzen, NCsoft, Pearl Abyss, and Netmarble Games to value SNK Corp. Using P/B valuation method, the bankers derived an average P/B multiple of 4.1x. The bankers then took the applied equity (controlling interest) of the company and applied the P/B multiple of 4.1x to derive an implied value of the company. After applying additional 8.57% to 32.99% IPO discount, the bankers derived an IPO price range of 34,300 – 46,800 won.

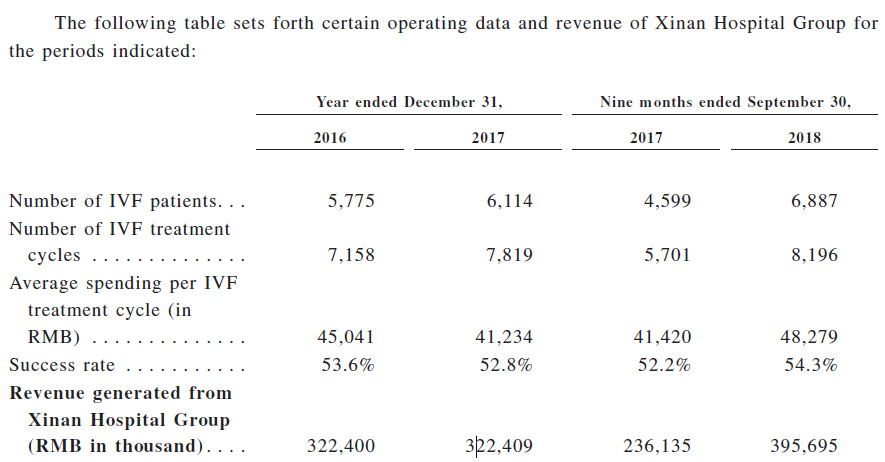

4. Jinxin Fertility (锦欣生殖) Pre-IPO: Strong Foothold in Sichuan but Weak Sentiment for Sector

Jinxin Fertility, a leading privately owned assisted reproductive service provider in China and the US, refiled to list in Hong Kong. Per news reports, the company planned to raise up to USD 500 million. In this insight, we will cover the following topics:

- Business lines and its hospitals

- The assisted reproductive service industry

- Key risks

- Shareholders and use of proceeds

- Our early thoughts on valuation

5. Cracking the Keyence Conundrum

Keyence Corp (6861 JP) has long been a standout within the Japanese machinery sector for its exceptional margins, with only Fanuc Corp (6954 JP) and perhaps Smc Corp (6273 JP) really operating in the same the stratosphere. But while Fanuc has faded, with its OPM now struggling to stay over 30% and SMC has only recently peaked its head over the 30% level, Keyence has been powering ahead and is on the cusp of recording five straight years over 50% OPM.

With relatively limited disclosures to go along with such stellar performance it is understandable then that some investors are concerned that the story is too good to be true, and even the FT has written a series of articles with a slightly critical bent: 1 2 34

Having recently visited the company, we analyse below, the nature of its competitive advantages by comparing it with its most similar peer Cognex Corp (CGNX US).

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.