This weekly newsletter pulls together summaries of the top ten most-read Insights across Equity Capital Markets on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

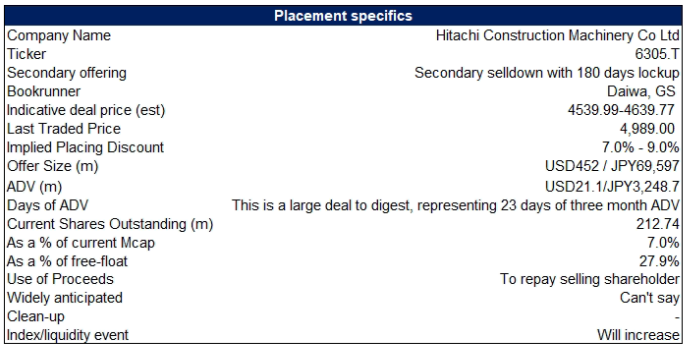

1. Hitachi Construction Machinery Block – US$450m Selldown by Hitachi

- Hitachi Ltd (6501 JP) aims to raise around US$452m via a 6.97% stake sale in Hitachi Construction Machinery Co. Post the selldown, Hitachi’s stake will reduce to 18.4%.

- Hitachi Construction Machinery Co (HCMC) is a Japanese company that designs, manufactures, sells, and services construction and mining equipment.

- In this note we talk about the deal dynamics and run the deal through our ECM framework.

2. ECM Weekly (3 November 2025)-Sany, Seres, CIG, PonyAI, WeRide, Mininglamp, Lenskart, Groww, Softcare

- Aequitas Research’s weekly update on the IPOs, placements, lockup expiry and other ECM linked events that were covered by the team over the past week.

- On the IPO front, there were a flurry of deal launches across Hong Kong and India.

- On the placements front, while the week was rather quiet, we did have a look at the upcoming lockup release.

3. PonyAI and WeRide Secondary HK Trading – Weakish Demand, WeRide Did Better but Trading Lower

- Pony AI (PONY US) raised around US$860m and WeRide (WRD US) raised around US$310m in their HK Secondary offering.

- We have looked at the deal dynamics in our previous note.

- In this note, we talk about the trading dynamics for the two deals.

4. CNGR A/H Listing: PHIP Update and Thoughts on A/H Premium

- CNGR Advanced Material (300919 CH), a Chinese battery-component producer, aims to raise up to US$700m in its H-share listing.

- CNGR is a Chinese battery-component producer and a new energy materials company.

- In this note, we look at its past performance and other deal dynamics that might impact the listing.

5. Seres Group A/H Trading – Demand Wasn’t Very Strong, Close to Fair Value

- Seres Group (601127 CH), a Chinese NEV manufacturer, raised around US$2.1bn in its H-share listing.

- Seres Group (SG) is principally engaged in the research and development, manufacturing, sales and services of new energy vehicles (NEV) as well as core NEV components.

- We have looked at the past performance and likely A/H premium in our previous note. In this note, we talk about IPO trading dynamics.

6. Pony.AI Hong Kong Public Offering Valuation Analysis

- Pony.ai has finalized the Hong Kong public offering price at HK$139 per share and it expects to raise HK$6.71 billion (US$860 million) from its planned secondary listing in Hong Kong.

- Our base case valuation of Pony.Ai is HK$178.2 per share over the next 6-12 months, which represents 28% higher than the Hong Kong public offering price.

- Given the solid upside, we have a Positive View of Pony.ai. Despite our Positive view, there have been increasing concerns about the overstretched valuations of major AI/tech related companies globally.

7. Seres Group H Share Listing (9927 HK): Trading Debut

- Seres Group (9927 HK) priced its H Share at HK$131.50 to raise HK$14,283 million (US$1.8 billion) in gross proceeds. The H Share will be listed tomorrow.

- I discussed the H Share listing in Seres Group H Share Listing: The Investment Case and Seres Group H Share Listing (9927 HK): Valuation Insights.

- The price momentum is weak, and the international oversubscription rates were below the median of recent large AH listings. Nevertheless, Seres’ AH discount remains attractive.

8. Groww IPO – Peer Comp and Thoughts on Valuation

- Groww (1573648D IN) is looking to raise around US$747m in its India IPO.Groww, officially called Billionbrains Garage Ventures, is a direct-to-customer digital investment platform providing multiple financial products and services.

- With Groww, customers can invest and trade in stocks (including via IPOs), derivatives, bonds, mutual funds and other products. Customers can also avail margin trading facility and personal loans.

- In our earlier notes, we have looked at the company’s past performance. In this note, we talk about the peer comp and implied valuations in the price range.

9. Groww IPO Review – India’s Largest & Fastest Growing Broker / Investment Platform.

- Groww is India’s largest stockbroker with 13mn active users. It is progressing towards a full-stack investment platform, expecting to cross-sell multiple financial products to over 18mn users on its platform.

- It is aggressively expanding into lending (MTF, LAS) and has recently acquired ‘Fisdom’ to offer premiumised wealth solutions (AIF, insurance, tax-filing). It also owns Groww AMC, offering debt/equity/Fixed income products.

- At 33 times FY25 earnings, IPO is priced reasonably considering its deep penetration in the market (customers from 98% Pincodes) and strong ARPU and profitability supported by decent retention metrics.

10. Pre-IPO Softcare (PHIP Updates) – Some Points Worth the Attention

- The rise of Softcare is in line with the logic of “Chinese supply chain going global”.It has solved channel/cost problems through localized production, quickly captured market share with low-price tactic.

- Our forecast benefiting from market penetration/capacity expansion, revenue growth could be 15% YoY in 2025.In 2026-2027, as competition intensifies, revenue growth may slow down to 12% YoY, 10% YoY respectively.

- Given that Softcare’s main market is in Africa, which is characterized by high growth and high risk, a forecasted P/E of 8-12x for 2025 could be a comfortable valuation range.