This weekly newsletter pulls together summaries of the top ten most-read Insights across Macro and Cross Asset Strategy on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. UK Course-Corrected CPI Stays High

- UK inflation unsurprisingly slowed in May as a correction to vehicle excise duty knocked 0.1pp from the rate, reversing all the upside to our above-consensus April forecast.

- Services inflation aligns with the BoE’s forecast from its May forecast, where MPC members were biased towards slowing their easing. Underlying rates remain too high.

- Inflation keeps trending above the consensus, cumulating a 1pp error since rate cuts began, but aligning with our forecast from 1yr and 2yrs ago. We remain hawkish.

2. BoE Still Seeking Evidence

- Guidance around an unsurprisingly unchanged BoE rate preserved the necessary uncertainty about when it might ease again, albeit with a broad bias to do more later.

- Dave Ramsden joined the dovish dissent, taking it to three for a 25bp cut, but none of them are in the MPC majority revealed in May as leaning towards a slower pace of cuts.

- We believe the August decision remains finely balanced for the majority. Ongoing data resilience, discouraging the Fed and ECB from easing, should also keep the BoE on hold.

3. US/China: Sprint vs Stamina

- The recent US/China trade talks highlighted Beijing’s superior leverage and determination.

- Beijing is in a stronger position in terms of both leverage and willingness to persist.

- Avoiding a re-escalation after the current 90-day truce relies on Washington making more concessions.

4. HEW: Playing For Time

- US diplomacy with Iran has been given two weeks, bringing it close to the reciprocal tariff deferral date. Both may roll later, while central bankers wait to see the impact.

- Unsurprising UK and EA inflation data offered little direction, nor did the BoE or Fed. Brazil and Norway delivered opposite surprises outside a flood of cautious statements.

- Next week is much quieter for data and decisions (TH and MX). The flash PMIs are the main global highlight, although some HICP and PCE data are notable on Friday.

5. Euro Area Wage Costs Closer To Target

- Non-wage labour costs rebounded in Q1, damping the overall slowdown to a surprisingly modest extent after the crash in negotiated wage growth revealed in May.

- Unit labour cost growth has encouragingly slowed below 3%, with the latest impulse only 0.6% q-o-q. Any further easing here could encourage monetary easing to resume.

- Stability at a low unemployment rate still suggests the policy setting is close to neutral, so we doubt disinflationary pressures will mount further and forecast no more rate cuts.

6. EA Inflation Predictably Near The Target

- Disinflationary news from May’s flash inflation release was confirmed in the final print, although a rebound in some underlying inflation measures damped the initial signal.

- Resurgent oil prices could rapidly reverse the dovish space expanded by past falls. Our forecast bumps around the target through 2026 and 2027, settling at 2%.

- Other forecasts are a little lower and only suffer a slight bias to be exceeded. The ECB can remain reassured by an outlook close to 2% without cuts, and not deliver any more.

7. China – Where To Invest?

- Overweight AI, high tech, robotics, renewables and bio-tech. Underweight on consumer discretionary, property and export cyclicals.

- China has become even more vital to its green transition. At the same time the shift in government mindset means that domestic innovation is advancing at a breathtaking pace.

- That said the economy is yet bottom. The profit cycle downturn is worsening; As of April 30% of manufacturing companies were loss making, up from 25% in November

8. Steno Signals #201 – The Mullahs Are Toast – Re-Inflation Is Back!

- Happy Monday from Copenhagen.

- What a comeback by JJ Spaun at Oakmont yesterday (sorry to the non-golfers), and what a comeback risk is about to make this week.

- Iran’s mullah-tocracy is on the brink, and it could be a catalyst for a big bounce in risk appetite.

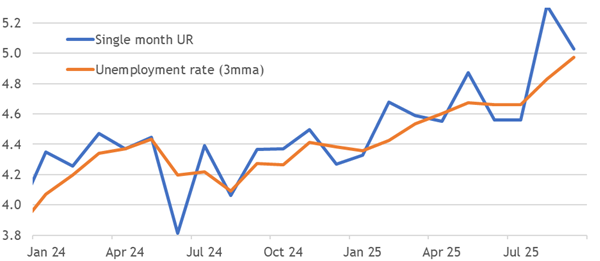

9. Walker’s Weekly: Dr. Jim’s Summary of Key Global Macro Developments – 20 June 2025

US interest rate cuts expected soon as economic data deteriorates across sectors.

Indonesia delays rate cuts; Philippines eases but risks peso weakness.

China retail sales rise, but property sector continues to underperform.

10. Cancellation of Existing Treasury Shares in Korea – Government Likely to Provide a GRACE PERIOD

- The Korean government may not force the listed companies to suddenly cancel all their treasury shares all at once.

- Rather, a GRACE PERIOD is likely to be given for companies with existing treasury shares by which they need to cancel them.

- Going forward, the Korean government is likely to decide to allow acquisition new of treasury stocks only when the purpose is to cancel them, excluding bonus payments or stock compensation.