This weekly newsletter pulls together summaries of the top ten most-read Insights across Macro and Cross Asset Strategy on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Is Japan Back?

- Japan, a country big in ETFs, is discussed in the Trillions podcast with guest Jeremy Schwartz from WisdomTree

- DXJ, the WisdomTree Japan Hedged ETF, had a successful run in 2013 but later underperformed, potentially due to currency manipulation and changes in leadership

- Despite past fluctuations, Japan never left and DXJ has outperformed the S&P 500 since 2012, highlighting the potential for growth and investment opportunities in Japan

This content is sourced through publicly available sources and has been machine generated. Information displayed is for general informational purposes only.

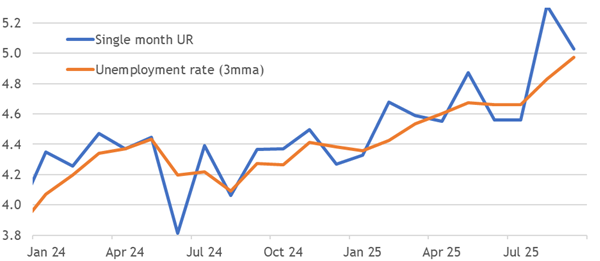

2. Credit For Inflation

- Credit and monetary holdings are booming in the UK, enabling consumers to spend their devalued pounds, supporting CPI inflation beyond the target.

- Falling rates have neutered the refinancing shock, facilitating the affordability of loan demand. Rapid ongoing wage growth further reduces the debt burden.

- The ECB also sees bullish monetary trends, but they only took it to a good place. The BoE is not in a good place, with policy accommodating above-target inflation pressures.

3. Ready for the Contrarian Gold Trade?

- We have been bull bulls, but point and figure charts of gold and gold miners show that they are either very near or have outrun their measured price objectives.

- Tactically, the contrarian trade would be to sell gold and buy bonds.

- However, a cycle analysis leads us to conclude that the market is undergoing a shift to a hard asset price leadership cycle.

4. China/US: Sauce For The Goose…

- Donald Trump and Xi Jinping’s 30 October summit will likely stave off, for now, any further escalation of trade tensions between China and the US.

- However, thanks to its monopoly on strategic minerals and Xi Jinping’s willingness to play a long game — even beyond ‘mere’ trade — China holds the stronger hand.

- Irrespective of whatever Mr Trump concedes this week to secure a ‘headline grabber’, Xi Jinping will therefore come back for more, not least on Taiwan.

5. HEW: Cautious Committees

- Central bankers broadly delivered on expectations this week, while cautioning that changes will likely be less than markets assume. The BOJ and ECB were also cautious.

- Flash EA inflation slowed, as expected, but services and core stoked hawkish pressure, while money and credit data in the EA and UK show accommodation of inflation.

- Next week’s BoE decision is no longer priced as a forgone conclusion, but the case to cut is weak. Like its peers, the BoE should cautiously damp dovish expectations.

6. CHINA HOUSEHOLD CONSUMPTION: Unlocking Growth Potential in Five-Year Plan

- China has announced that it will significantly boost the share of domestic consumption in its next five years, while maintaining tech and manufacturing as top priorities.

- The nation’s banks will be instrumental in providing consumption financing to spur a virtual growth driver for the economy. Easing monetary policies will be in addition to the trade-in programs.

- Consumer in service sectors like e-commerce, travel & tourism, healthcare, elderly care and AI will benefit from increasing consumption. Local brands stand to gain market share against foreign competitors.

7. EM Fixed Income: Reviewing the global & previewing the upcoming idiosyncratic

- EM markets trading with strong global beta, lack of US key data due to government shutdown affecting market direction

- EM currencies look okay, EM rates may be less favorable, EM credit suffering from tight spreads

- Key takeaways from IMF conference in Washington include focus on impact of AI-related investments on global growth and employment, overall mood on growth is flat with risks but no panic or euphoria

This content is sourced through publicly available sources and has been machine generated. Information displayed is for general informational purposes only.

8. Time to Sound the All-Clear?

- The U.S. stock market’s technical conditions are turning more constructive.

- Market internals such as breadth and risk appetite indicators have stopped deteriorating and they are starting to heal

- Risks remain, and we would like to see the resolution of key event risks before sounding the all-clear signal.

9. The Art of the Trade War: U.S. ON THE HAMSTER WHEEL!

- The much hyped meeting between the presidents of the world’s two largest economies fell short of global expectations. Key issues were only delayed, not resolved.

- China has been steadfast in the face of U.S. hardball tactics, resulting in the U.S. reversal of announced measures, like the expansion of the restricted entity list.

- The effective tariff rate on Chinese exports to the U.S. will be approximately 30%, which is 20% higher than when President Trump took office.

10. Global Active Funds Struggle to Close the Gap in 2025

- Active Global funds averaged +15.5% YTD, trailing the SPDR ACWI ETF’s +18.8%, with 73% underperforming the benchmark.

- Value strategies led performance; Aggressive Growth funds lagged sharply, averaging just +10.15%.

- Underweights in US Tech names like NVIDIA and Palantir, plus 2.4% cash holdings, drove relative losses.