This weekly newsletter pulls together summaries of the top ten most-read Insights across Macro and Cross Asset Strategy on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. UK Disinflationary Kool-Aid

- UK disinflation relied on smaller utility price hikes and only went as far as the 3.6% forecast before September’s dovish surprise. It does not mean a path to 2% lies ahead.

- A broad rebound in price increases took the annualised median impulse above 4% to average 2.5% over two months, or 3% on the year, as the underlying problem persists.

- The BoE’s December decision pivots around the Governor, who seemingly needs upside news to avoid delivering a cut, so this outcome preserves that riskily dovish course.

2. Japan Picks a Fight with China!! What Happens Now?

- Japan has intentionally stepped into the middle of the geopolitical battle between the U.S. and China with Prime Minister Takaichi’s policy-changing Taiwan comments to Japan’s parliament.

- China’s retaliation has been swift and tactical, issuing travel warnings, high-level diplomatic reprimands, and conducting military exercises near the Senkaku Islands. China has promised a continuing substantial and broad-based response.

- We expect China’s response to include rare earth export and Japanese trade restrictions and targeted boycotts of Japanese goods on the mainland.

3. HEW: Micro Risk Off

- Risk assets have suffered, despite decent Nvidia results suggesting AI demand hasn’t turned yet, and the macro data remaining resilient. Fears are more theme-specific.

- US labour market activity entered the shutdown solidly, and low jobless claims suggest it survived fine. Meanwhile, UK inflation only lost a little excess, and our forecast rose.

- Next week’s UK Budget is the lowlight of our week, but it may struggle to live up to all the noisy hype. Sneaky backloaded tax hikes will close the latest forecast hole again.

4. EA: Unsatisfying disinflationary snack

- Slower food price inflation nibbled the EA rate down to 2.1% in October, while services increased to their fastest pace since April. Labour costs are still rising too fast.

- Underlying inflation metrics are broadly a bit beyond target, risking a slight overshoot in the medium term, but the median impulse is reassuring, weighed down by France.

- Energy prices are set to bump inflation around the target in 2026, averaging above the consensus in our view. The ECB would need tightness elsewhere to shift rates, though.

5. The Dollar Is Smiling But It’s Not Happy 🙁

- The dollar has strengthened in the face of weakening equity markets, however it is not the Dollar Smile theory supporting its move this time.

- A more hawkish Fed signals a break with past conditioning for a Fed Put to bail out the stock market. Post-COVID inflation caused by Fed policies will constrain aggressive easing.

- Safe-Haven support for the dollar and Treasuries broke down during the April selloff, indicating a change in foreigners’ perception of holding USD assets and leading to significantly increased dollar hedging.

6. Japan: The New Takaichi Trade, SELL THE RIP!

- Sentiment in Japan has reversed sharply showing strains in the JPY and JGB markets. The Nikkei 225 has retraced all its gains since the election of Prime Minister Takaichi.

- The market is nervous about the size of Takaichi’s economic package, which will be ¥21.3 trillion; 27%. more than her predecessor pledged. It will increase bond issuance substantially.

- Tensions from Takaichi’s provocation of China show no sign of easing. China has started economic and other measures to respond. The US has removed a missile launcher from Japan.

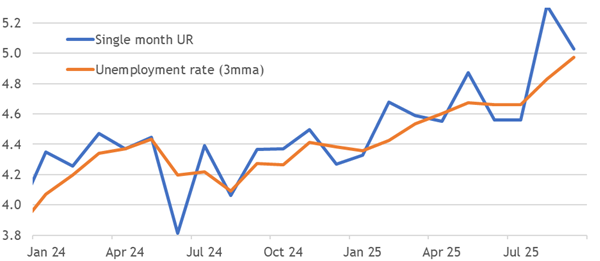

7. US: Resilient Into Shutdown

- US payroll data revealed resilience going into the US government shutdown, with jobs growth the strongest since April and annualising to a pace capable of plateauing growth.

- Surging labour force participation drove unemployment up in the least disappointing way, with the employment to population ratio making a contradictory improvement.

- Jobless claims suggest stability into the shutdown’s end, besides noisy federal claims. The FOMC may not get the evidence it needs to cut again in December. It may not exist.

8. Asian Equities: A Correction, Not a Bear Market; Rates Still Falling and Earnings Are Catching Up

- Combination of concerns about Fed rate trajectory, AI capex monetization, Chinese growth slowdown and Japanese Yen carry trade unwinding brought the US and Asian markets 4-5% down since late October.

- Expensive valuations are now justifiably correcting. Notwithstanding worries about a December cut, the interest rate trajectory remains resolutely downwards. Asian disinflation offers several central banks further room for monetary easing.

- AI capex monetization worries will wax and wane. But Asian AI enablers’ cash flows seem safe and valuations inexpensive. Corporate earnings environment is solid in US and recovering in Asia.

9. Asian Equities: Policy Focus Reflected in Sector-Wise IPO Revival in Leading Markets

- Asian IPOs’ spike in 2025 (21% higher till October) has been driven primarily by HK/China. Indian IPOs are almost at the same level as in a very strong 2024.

- Policy thrust for “New Productive Forces” are driving capital raising from industrials, materials, technology and utilities and shall continue to do so. Healthcare should also be a buoyant capital raiser.

- India’s policy focus on manufacturing and listing of PE-funded companies should drive IPOs from industrials, materials and consumer discretionary. Financials shall also remain a large issuer sector.

10. Walker’s Weekly: Dr. Jim’s Summary of Key Global Macro Developments – 21 Nov 2025

U.S. data releases are expected to clarify economic conditions while political pressure complicates monetary policy sentiment.

Japan’s new leadership has escalated geopolitical tensions with China through unnecessary provocative statements.

Asian growth remains mixed but resilient, led by strong performances in Vietnam, India, Taiwan, and Malaysia.