This weekly newsletter pulls together summaries of the top ten most-read Insights across Macro and Cross Asset Strategy on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Agentic Finance: Building AI Analysts for the Debasement Trade Era — with Vlad Stanev of Quantly

- CEO of Quantly discusses market updates, geopolitical landscape, and trends in safe havens

- Focus on innovation and tech, AI, and bitcoin in the digital market

- Analysis of one year trends in safe havens, bitcoin, gold, and the impact of tariffs on the market.

This content is sourced through publicly available sources and has been machine generated. Information displayed is for general informational purposes only.

2. HEM: Nov-25 Views & Challenges

- Pushback by Powell and peers trimmed some excessively dovish pricing, but the BoE converged down on poor data.

- The BoE should also resist pressure as underlying issues are unbroken by relatively marginal recent payback.

- We now see markets overpricing easing most in the UK. More weakness is needed to signal a threatening trend.

3. BoE: Hawkish Surprise Set For November

- Markets have erroneously repriced a BoE rate cut as potentially imminent and repeated. Policymakers are tending to surprise hawkishly in the UK and elsewhere recently.

- Downside news on excess inflation is mild, while the activity data have, if anything, exceeded BoE forecasts. Pay growth signals remain strong, not disappointing the BoE.

- Six MPC members have favoured slower easing, inconsistent with a November cut. Fiscal consolidation is unlikely to frontload a shock large enough for the MPC to accommodate.

4. BoE: Bailey Leans Over December Fence

- Another 5:4 vote split broke the BoE’s run of quarterly rate cuts. Governor Bailey is revealed to be the pivotal member, with the others worried about inflation persistence.

- Bailey endorsed market pricing and a forward-looking Taylor Rule path that includes a cut this quarter. His verbal comments imply a presumption in favour of cutting then.

- Upside news over the next two monthly release cycles would be needed to block that December cut. Resistance to cutting should only grow stronger as time passes.

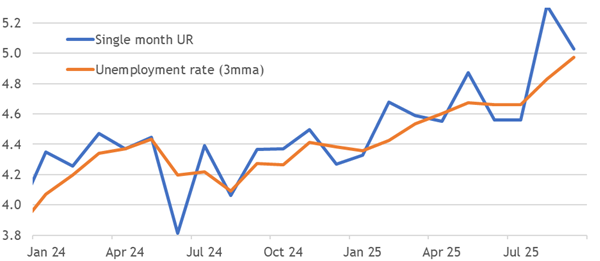

5. Rebound To Resilience

- The diverging services PMI and ISM resolved bullishly in October, with activity broadly back to 2024 averages. The ISM headline still looks lower because it is a composite.

- Price balances remain extremely elevated while employment’s weakness has become less acute, skewing the trade-off more hawkishly for any policymaker’s preferences.

- The broader global deterioration in PMIs and unemployment last month also recovered in the latest round of releases. These data are not screaming for any more easing.

6. HONG KONG ALPHA PORTFOLIO: (October 2025)

- The Hong Kong Alpha portfolio’s performance was -2.01% in October versus returns of -0.81 for the benchmark and -3.53 to -8.62 for Hong Kong indexes.

- The Hong Kong Alpha portfolio has captured most of the market gains and minimized drawdowns since inception. The portfolio’s outperformance is more than 40% since inception in October 2024.

- At month-end, we reduced materials and healthcare exposure. We had already reduced the tech exposure earlier in the month. We established positions in the utility, textile, and battery sectors.

7. Making Sense of the Gold Price Retreat

- We offer a plausible scenario that explains the recent surge and correction in gold.

- The market misinterpreted the “Liberation Day” USD decline as a “Sell America” trade instead of a “Hedge America” trade and panicked out of USD and rushed into gold.

- We expect a bottom in gold in Q4 or Q1 as the new Fed Chair pivots monetary policy in a more expansionary manner.

8. HEW: Caution Echoes Outside the BoE

- The BoE resisted cavalier calls for a rate cut this week, but it is much less cautious than we expected. A December rate cut is now likely, absent significant upside surprises.

- All other central bank announcements this week fit the trend, with cautious holds in Australia, Sweden, Norway, Malaysia and Brazil, and a more careful cut in Mexico.

- Next week’s UK labour market (and GDP) data are one of the few things that could clear the evidential hurdle to block a cut, although we doubt good news will extend that far.

9. The Art of the Trade War: HE SAID, XI SAID….. WHAT WAS AGREED?

- The meeting in Busan between Presidents Trump and Xi reduced the tension between the two countries, but the detente may only be temporary and confusion on details persist.

- Tariffs were immediately reduced and potential future increases delayed by a year. President Trump offered to reduce the fentanyl tariff further to 0% after the meeting.

- The most critical issues of export restrictions on chips and Rare Earth Elements were dialed back with recent threatened restrictions delayed by a year.

10. Prepare for the Year-End Rally!

- A review of our Trend Asset Allocation Model reveals a broadly based momentum-driven global bull.

- The S&P 500 is also entering a period of positive year-end seasonality.

- In light of the bullish support provided by the intermediate trend, investors should be positioning for a rally into year-end.