This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

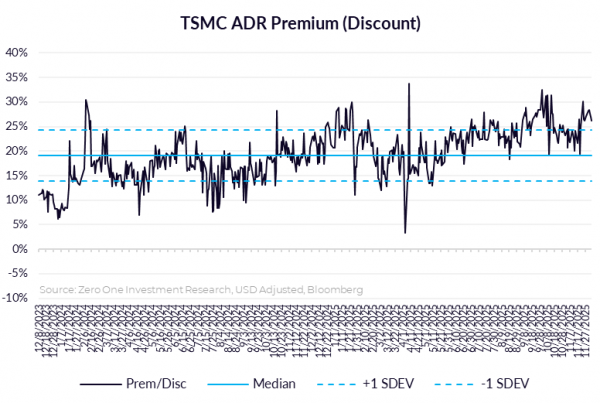

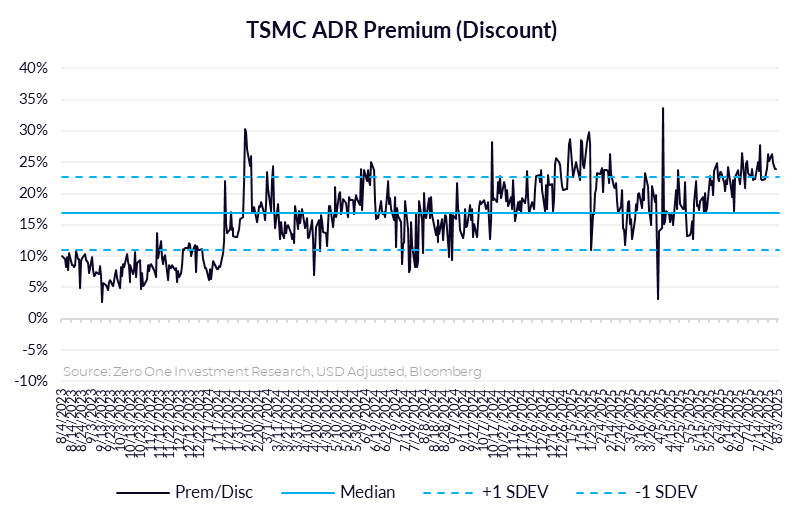

1. Taiwan Dual-Listings Monitor: TSMC Spread Short Setup, ASE ADR at Historically Rare Discount

- TSMC: +23.9% Premium; Continued Opportunity to Short the ADR Premium

- UMC: -0.4% Discount; Wait for More Extreme Levels Before Going Long or Short

- ASE: -1.5% Discount; Historically Rare Discount Presents Opportunity to Long the ADR Spread

2. TechChain Insights: Taiwan’s Battery Cell Moment? USA & EU Supply Chain Under Strategic Pressure

- Battery cells are the new chokepoint in the global clean energy supply chain, with China still controlling 75%+ of global capacity and exporting under increasingly restrictive terms.

- Taiwan is emerging as a high-trust, high-precision hub for advanced cell manufacturing, applying its semiconductor model to batteries.

- With pouch cells gaining traction across drones, robotics, and compact mobility, Taiwan’s lab-to-fab advantage positions it as a future anchor of the U.S. and European energy ecosystems.

3. Intel. Was Tesla’s Deal With Samsung The Death Knell For IFS?

- Tesla & Samsung just inked an eight year, $16.5 billion foundry deal set to run from July 24, 2025 through December 31, 2033.

- Had Intel snagged this deal, it would have been a lifesaver for the company. Not getting it likely triggered the updated “Risk Factors” section in their latest 10K.

- This isn’t Intel playing politics, there’s no point. It’s LBT laying it on the line for investors. Continued investment in 14A is no longer a given. It’s that simple…

4. Taiwan Tech Weekly: TSMC’s Arizona Surprise – 2nm by 2026?; Signs of Hyperscaler Growth Acceleration

- U.S. 2nm Production May Begin Sooner Than Expected — Is TSMC Responding to Unprecedented N2 Demand?

- Hyperscalers 2Q25: Revenue Growth Accelerates, Cloud Revenues Accelerate, Capex Higher

- TechChain Insights: Taiwan’s Battery Cell Moment? USA & EU Supply Chain Under Strategic Pressure

5. Intel. Crisis Mode All Over Again

- President Trump wants Intel CEO Lip Bu Tan to resign immediately because he claims that he is “highly CONFLICTED”

- The President’s concerns likely relate to a recent DoJ case against Cadence as well an investigation by the Select Committee on the CCP into Walden International’s Chinese investments

- That both these topics weren’t comprehensively addressed and mitigated prior to Mr. Tan’s appointment beggars belief. Where was the due diligence Mr. Yeary?

6. Intel (INTC.US): Changing the CEO Could Save This Company? Probably the Wrong Direction.

- US President Trump urged Intel Corp (INTC US) yesterday to replace its current CEO, Mr. Lip-Bu Tan.

- We believe Intel Foundry Services (IFS) could be a highly challenging — or even misguided — strategy

- Intel Corp’s share price has declined about 23% since Mr. Lip-Pu Tan took office.

7. SMIC (981.HK): 2Q25 Results in Line; 3Q25 May Offer Mild Upside, but GM Is Expected to Be Flattish.

- Semiconductor Manufacturing International Corp (SMIC) (981 HK) reported in-line 2Q25 results, while its 3Q25 guidance appears somewhat cautious, particularly in terms of gross margin.

- The Americas continued to contribute a low-teens percentage to revenue, accounting for 12.9% in 2Q25, while China and Eurasia comprised the remaining majority.

- Our top questions for the upcoming SMIC’s 3Q25 earnings conference call.

8. Novatek (3034.TT): 3Q25 Outlook Is Expected; Weaker Demand from China Due to Subsidy Tapering.

- 3Q25 Outlook & Guidance- Revenue: NT$23.7–24.7bn( down 9.5~5.7% QoQ); Gross Margin: 34–37%; Operating Margin: 15–18%; USD/TWD Assumption: 29.5

- Weaker demand from China due to subsidy tapering in 3Q25, but seasonal stocking in non-China markets.

- 2025 foldable penetration estimated at ~1.6% (~19mn units); Large foldables: higher internal display resolution and ASP; OLED TDDI advantage: fewer components, more space-efficient, enabling thinner phones.

9. Novatek (3034.TT): FX Impact Persists; 3Q25 May Be a Down Quarter.

- We expect Novatek Microelectronics Corp (3034 TT)‘s 3Q25 might be decline 5-10% QoQ, reflecting 2H25 US tariffs impacts and Chinese opponent’s competition.

- The Foldable handset may be indicated a new era to come, and we believe Novatek Microelectronics Corp (3034 TT) shall be one of the DDIC winners.

- The stock price of Novatek Microelectronics Corp (3034 TT) is long staying with NT$450~650 since the beginning of 2024, and the current price is at the relative low point.