This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

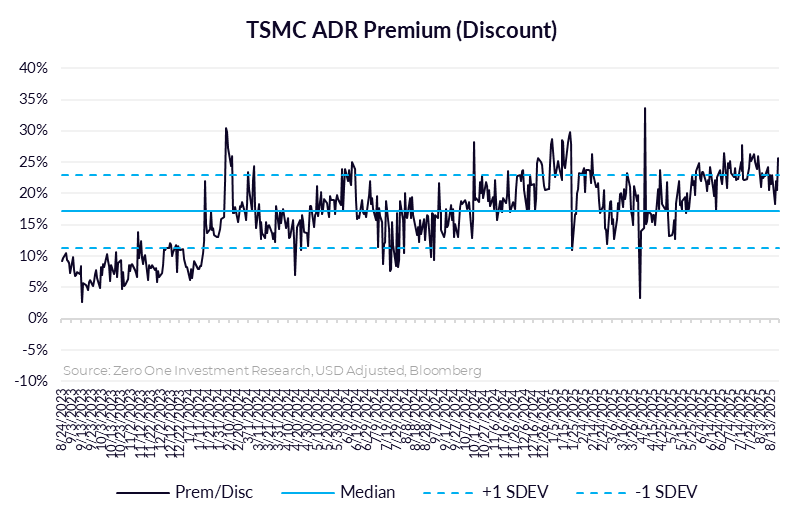

1. Taiwan Dual-Listings Monitor: TSMC Premium Spike Opportunity; ASE Hard Bounce to Prem from Discount

- TSMC: +25.6% Premium: Latest Spike is Opportunity to Short the ADR Spread

- UMC: +2.0% Premium; Near Level to Go Short the ADR Spread

- ASE: +5.1% Premium; Good Level to Take Profits on Previous Long Since Parity

2. Intel (INTC.US): Intel–U.S. Government Equity Deal: Implications and Industry Perspective

- Intel has reached an agreement with the U.S. government, under which Washington will invest $8.9bn for a 9.9% equity stake in the company.

- Intel benefits from the optics of government backing, which could help sentiment and prevent downside pressure on the stock in the short term, i.e. near-term optics positive, fundamentals unchanged.

- TSMC’s Japan and Germany fabs were structured through co-investments and partnerships, with equity involvement only when tied to technology access (e.g., Sony CMOS JV).

3. Taiwan Teck Weekly: Apple Snags Over Half of TSMC’s Best Chips; Long-Reasoning AI Will Surge Compute

- Apple Secures Over Half of TSMC’s Cutting-Edge 2nm Capacity; How TSMC Anchors Apple’s Product Leadership Strategy

- NVIDIA Results Key Take-Away: Long-Reasoning AI Models Driving Massive Compute Demand

- Intel (INTC.US): Intel–U.S. Government Equity Deal: Implications and Industry Perspective

4. Taiwan Dual-Listings Monitor: TSMC Premium Remains Elevated; ASE Drops Down to Near Parity

- TSMC: +21.8% Premium; Wait for Higher Premium Before Fresh Short of the Spread

- UMC: -0.6% Discount; Wait for More Extreme ADR Spread Level

- ASE: +0.4% Premium; Good Level to Go Long the ADR Spread

5. Silergy (6415.TT): 3Q25 Revenue Flat to Slightly Up QoQ; Annual Growth May Fall Short of 20%+.

- 3Q25: Revenue flat to slightly up QoQ; GM stable at 52–54%. FY25: Prior 20%+ growth target unlikely to be achieved; weaker demand due to trade war & customer conservatism.

- No evidence of significant market share loss; instead, delayed demand.

- Automotive Ssegment continues to trend upward with new EV-related products. Competition in China is intense, especially EVs, but pricing remains rational.