This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Fermi America’s Unfathomable Progress

- On October 1, Texas-based startup Fermi raised $682.5 million through the sale of 32.5 million shares at $21/share in a remarkable dual listing on both the NASDAQ and LSE

- The company claimed to have a prospective first tenant who had already “put down” a $150 million prepayment

- On December 12, Fermi issued a SEC filing clarifying that no money had been drawn down and the the prospective tenant had terminated their agreement. Currently trading @ ~$9/share

2. TSMC: A Resilient Long Holding Insulated From an AI Slowdown

- Strong Signals TSMC’s 2nm Node Will Take the Company to New Heights

- Apple Anchors 2nm Volumes — Insulates from Potential AI Capex Slowdown

- TSMC Inexpensive and Resilient to Any Potential AI Capex Slowdown

3. Hamamatsu Photonics (6965 JP): The Opportunity in Lasers

- Demand from the semiconductor, medical, quantum computing and defense industries is turning the Laser segment into Hamamatsu Photonics’s new growth driver.

- The acquisition of NKT Photonics brings defense and other technologies, Rheinmetall as a customer in Europe, and potential for greater defense-related sales in Japan.

- Selling at 20x net profit guidance for FY Sep-28, near the bottom of its 10-year P/E range.

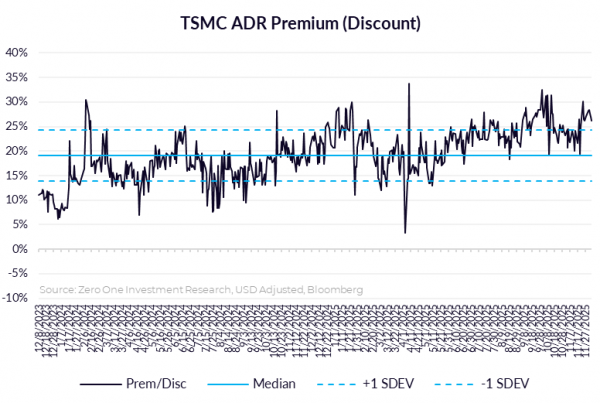

4. Taiwan Tech Weekly: TSMC’s Next Node Already Sold Out Before Any Mass Production

- TSMC’s 2nm Node Is Already Sold Out Through 2026E… And Hasn’t Even Started Production Yet

- Taiwan Dual-Listings Monitor: TSMC Historically High Premium Cracks; ChipMOS & CHT Opportunities

- Micron: Nov-25 Beat by 30%, Feb-26 Guidance 80% Above Consensus

5. Pharma Foods International (2929 JP): 1Q Loss from Up-Front Advertising Expenses

- After dropping to a 52-week low on operating and net 1Q losses, the share price has recovered to 20x EPS guidance for FY July 2026.

- The gross margin remains near 80%, but a large increase in advertising expenses put the company into the red. It also boosted sales as planned.

- Management plans to cut back on advertising, aiming for break-even in 2Q and profits in 2H. The dividend yield is now 3.6%. The long-term investment story remains intact.