This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

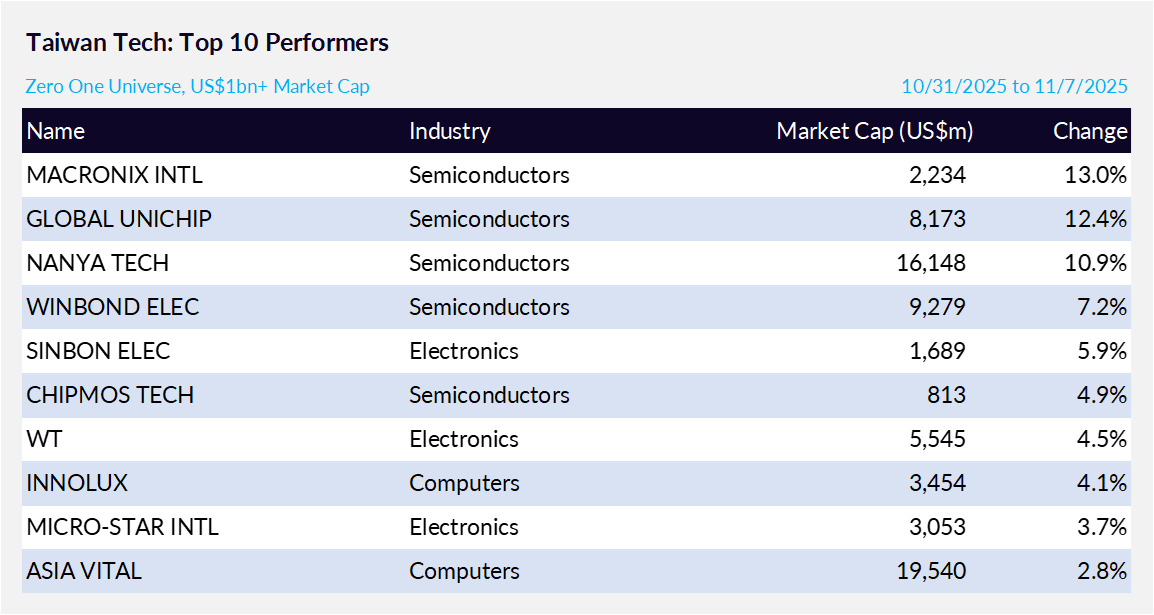

1. Taiwan Tech Weekly: Nvidia Asking TSMC for More Capacity; Apple to Disintermediate Telcos?

- Nvidia Pushes TSMC for More Capacity as AI Chip Demand Surges

- Apple Expands Its Satellite Ambitions for iPhones Beyond Just Emergencies — A Step Towards Disintermediating Telcos?

- Nvidia’s International HQ in Taipei Deal Clears Final Hurdle — Boost for Taiwan 2026E-2027E

2. Substrate. ASML, TSMC Slayer Or Ideological Pipe Dream?

- Silicon valley startup Substrate made waves two weeks ago when they emerged from stealth mode to announce a revolutionary new tool they claim will rival ASML’s EUV lithography capability

- Substrate simultaneously plans to build next-generation semiconductor fabs to return America to dominance in semiconductor production and will use their technology—a new form of advanced X-ray lithography—to power them.

- For a three year old startup, whos CEO has zero documented experience of semiconductors or lithography, these are bold claims indeed. This should be interesting!

3. Humanoid Robots Won’t Take Your Job, We’ve Just Decided Not To Give You The Job In The First Place.

- Jensen Huang claims that the world is running out of workers & there will be a shortage of 50 million workers by the end of the decade. Enter humanoid robots.

- Elon Musk claims that AI and robots will take all our jobs, working will be optional and we can grow vegetables while he’s on his way to becoming a trillionaire

- Technology and society are rapidly approaching a critical decision point. Jobs for robots or for humans?

4. SMIC (981.HK): Although GM May Decline Slightly, Revenue Is Expected to Continue Growing in 4Q25.

- Revenue in 3Q25 was 7.8% higher than in 2Q25, in line with stronger seasonal demand. GM: 22.0% in 3Q25, compared with 20.4% in 2Q25 and 20.5% in 3Q24.

- The Company expects: Revenue Flat to up 2% quarter-over-quarter (QoQ). Gross Margin: Between 18% and 20%.

- SMIC’s stock price has risen 160.7% year-to-date in 2025, outperforming Taiwan Semiconductor (TSMC) – ADR (TSM US) at 44.2% and United Microelectron Sp Adr (UMC US) at 10.8%.

5. Hamamatsu Photonics (6965 JP): Capex Peaking, Profits to Rebound

- Announced last Friday, FY Sep-25 sales and net profit were in line with guidance, but operating profit fell short. On Monday, the shares dropped 4.5%, wiping out a month’s gains.

- Looking ahead, management expects three years of sales and profit growth as capex declines, depreciation and R&D level off, and the NKT Photonics acquisition approaches breakeven.

- In this scenario, semiconductor, bio-medical, defense and quantum computing applications should drive 3-year sales growth of 24% and a 71% increase in net profit, bringing the P/E down to 20X.

6. Silergy (6415.TT): 4Q25 Flat or Slightly Upside; Early Gen4 Yields Remain Non-Comparable.

- 4Q25 seasonal outlook? Silergy expects flat to slightly up QoQ, similar to past years.

- Silergy does see consolidation, and given its stronger financials, product breadth, and R&D capabilities, the company remains a top supplier and will continue to gain share.

- Will 1H next year be better than 2H this year?Hard to say because of Chinese New Year seasonality.We expect YoY growth, but not strong yet.

7. TechChain Insights: ChipMOS Indicates Memory Industry Surge into 2026E; Smartphones Currently Soft

- This assembly and testing leader provides fresh insight into the state of display, memory, consumer, enterprise, and industrial end markets.

- ChipMOS: Memory Industry Strength Offsets Display Industry Weakness. Memory strength seen into 2026E. Company noted soft smartphone industry panel demand currently.

- Management signals sustained memory upcycle; disciplined capex to serve multi-year AI and datacenter growth. We rate ChipMOS shares as a Structural Long.