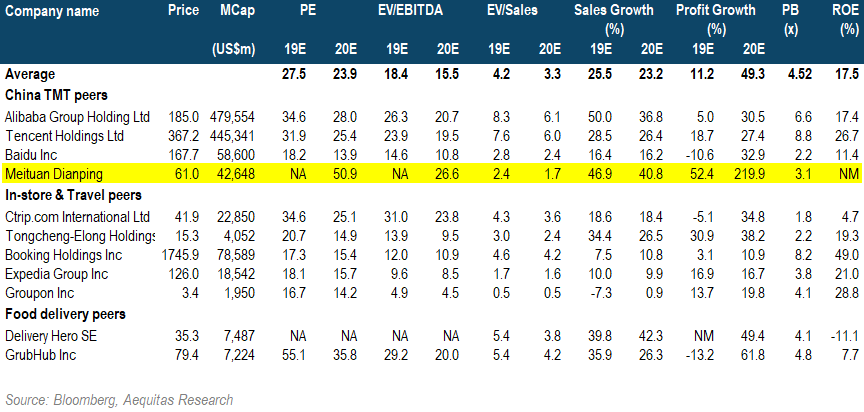

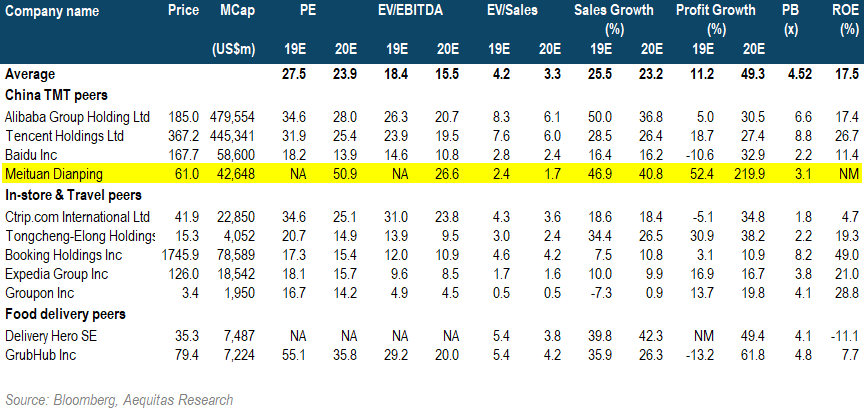

Meituan Dianping, the largest O2O platform in China, was listed on September 20th last year and lock-up expiry will be on March 20th. The stock has returned -13% since listing.

As it heads into lock-up expiry on March 20th, we will examine Meituan Dianping shareholder structure and potential shares up for sale.

Meituan was included by MSCI recently and will be eligible for the Hong Kong Connect soon thanks to rule amendment.

The company delivered a decent topline growth in 3Q2018 but its profit fell short of expectation. We highlight potentials from the food supply chain solution. We also discuss implication from MoBike acquisition.

We review our SOTP valuation of Meituan and believe there is an upside.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Meituan Dianping, the largest O2O platform in China, was listed on September 20th last year and lock-up expiry will be on March 20th. The stock has returned -13% since listing.

As it heads into lock-up expiry on March 20th, we will examine Meituan Dianping shareholder structure and potential shares up for sale.

Meituan was included by MSCI recently and will be eligible for the Hong Kong Connect soon thanks to rule amendment.

The company delivered a decent topline growth in 3Q2018 but its profit fell short of expectation. We highlight potentials from the food supply chain solution. We also discuss implication from MoBike acquisition.

We review our SOTP valuation of Meituan and believe there is an upside.

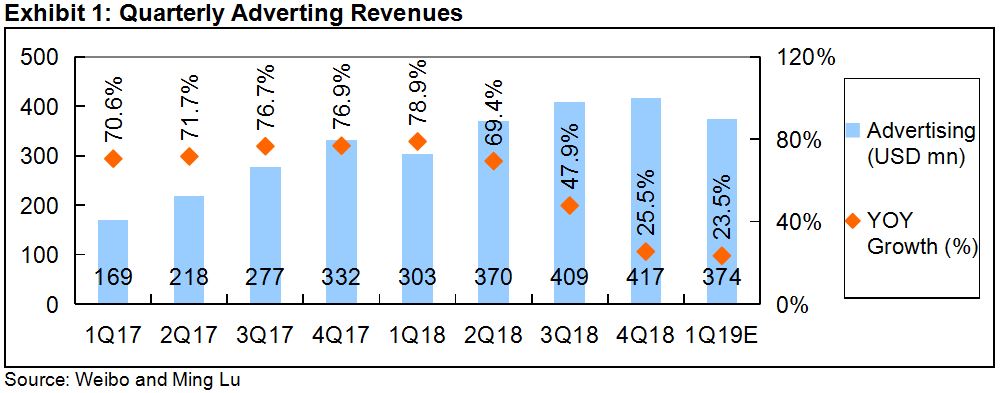

The advertising revenues slowed down significantly in 4Q2018.

We believe the content transition from politics to entertainment was not as good as the management expected.

We believe WB will not defeat Tencent’s WeChat.

We believe the stock price has downside of 9%.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

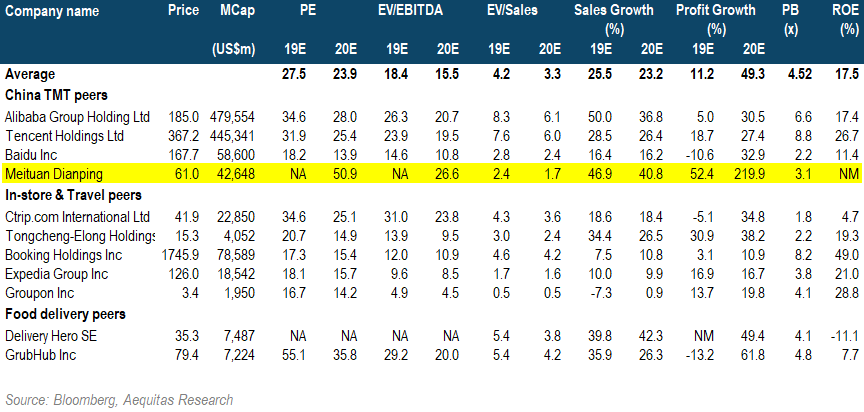

Naspers (NPN SJ) recently announced another attempt to reduce the holdco discount which has remained stubbornly high despite previous attempts by management to reduce it. Since the announcement there has been movement, so perhaps this time it really is different!

So what is being done? Naspers will spin off its international internet assets, which account for >99% of its value, into a newco. They will then list 25% of newco on the Euronext in Amsterdam by issuing these shares to Naspers’ shareholders. The intention is to create a vehicle which can attract increased foreign and tech investors without the complication of a South African listing. The company believes this has been a key factor behind the wide holdco discount. The move also reduces Naspers weighting in South African indices which is another contributing factor.

Alastair Jones sees the announcement as a positive, although there are still issues with the main listing being in South Africa. He still believes a buyback would be the most effective way to reduce the discount, but Naspers is also keen to keep investing.

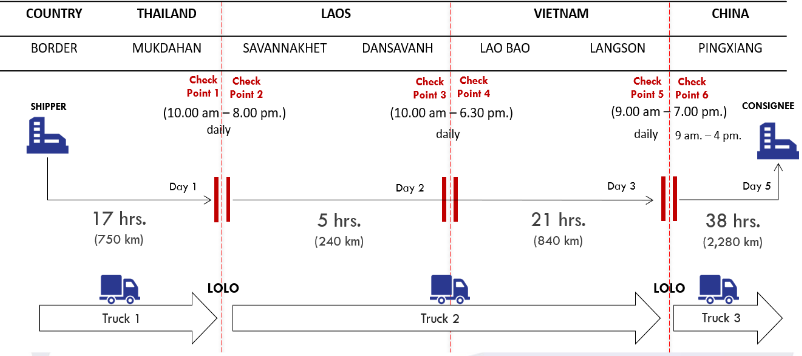

We maintain BUY rating for WICE with a new target price of Bt5.20 (previous target price: 7.50), based on 29xPE’19E, its one year average trading range or 20% discount to Thai transportation sector.

The story:

Cross broader business plays the key growth driver in 2019

We revised down earnings in 2019-21E due to lower-than-expected margins

Risks:

Stronger Baht vs major foreign currencies such as US dollar causes lower income in Baht terms as the main reporting currency is Baht

Higher than expected in fluctuation in freight rates

Intensity of freight forwarding businesses in both domestic and overseas

This article is a round up of the key takeaways from our recent meeting with Sony’s IR team. Our main focus was on the PlayStation and subsequent hardware and software developments, the company’s mobile phones business unit, the pictures unit as well as the semiconductor business.

In the gaming segment, Sony doesn’t see Stadia as a threat since Sony mainly caters to the core gaming segment. Sony does not expect cloud gaming to offer the same quality that consoles offer to core gamers anytime soon. For the time being, Stadia will most likely appeal to casual gamers.

In the pictures segment, Sony is developing a Spider-Verse sequel. A definite release date is yet to be confirmed, however, looking at the first movie’s success, we can expect a similar result for the sequel upon release.

The company also plans to hold onto its mobile communications segment even though it is expected to make losses in FY03/19 as well. For Sony, this segment is crucial in developing 5G technologies.

In the semiconductors segment, Sony expects a demand hike from the number of cameras used per phone. This is in spite of the mobile phone market itself slowing down. Sony expects to increase the ASPs of these sensors going forward as well.

We selectively visited a dozen companies in March and were most impressed with three of them (two of which we happily own):

SISB, Thailand’s only listed education stock, whose market cap has increased more than 30% since its IPO. The future potential growth they are currently working on in Cambodia and China will show up here and spruce the company’s already strong growth. Working in a favorable environment (Thailand’s affluent class is growing) also helps.

MINT, the country’s hotel chain giant and 20th largest chain in the world, sees great growth potential in Europe, where things are slowly turning around after they made two big acquisitions (NH Hotels and Tivoli). Synergies are also materializing with co-marketing and re-branding efforts.

After You, arguably the dessert chain with the highest margin in Thailand. No longer a newbie IPO stock, these guys boast collaboration with global giant Starbucks and branching out into new channels such as After You Durian.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Yesterday, post-market close, Japan Post Holdings (6178 JP)(JPH) announced that it will sell 185m shares (including over-allotment) or 30.8% of Japan Post Insurance (7181 JP)(JPI) amounting to US$4bn. JPI plans to buy back up to 50m shares out of these, leaving around US$3.1bn worth of stock to be placed. Out of these 185m shares, 30% will be placed with foreigners.

The selldown is part of the government’s plan for privatization under which JPH is supposed to reduce its stake in JPI and Japan Post Bank (7182 JP)(JPB) to around 50%. This was highlighted in the IPO of the three entities in 2015. Thus, the deal is not totally unexpected but the timing of it was never certain. For people interested in more about the history and background, we’ve covered the IPO and JPH sell down in the below series of insights:

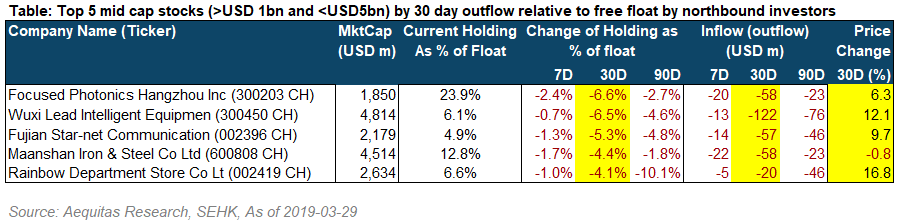

In our Discover SZ/SH Connect series, we aim to help our investors understand the flow of northbound trades via the Shanghai Connect and Shenzhen Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by offshore investors in the past seven days.

We split the stocks eligible for the northbound trade into three groups: those with a market capitalization of above USD 5 billion, and those with a market capitalization between USD 1 billion and USD 5 billion.

We note that in March, northbound inflows turned more cautious vs strong inflows in February (link to our Feb note) and January (link to our Jan note). Nevertheless we see strong inflows into Healthcare sector, led by Jiangsu Hengrui Medicine Co., (600276 CH). We also highlight Universal Scientific Industrial Shanghai (601231 CH 环旭电子) in the mid cap space that attracted strong northbound inflows.

Huya, a leading live streaming player in China, announced share placement of USD 550 million after market close on April 3rd. In this insight, we will look at recent developments of Huya and score the deal in our ECM Framework.

In this insight, we will update on the deal dynamics, implied valuation, and include a valuation sensitivity table.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Meituan Dianping, the largest O2O platform in China, was listed on September 20th last year and lock-up expiry will be on March 20th. The stock has returned -13% since listing.

As it heads into lock-up expiry on March 20th, we will examine Meituan Dianping shareholder structure and potential shares up for sale.

Meituan was included by MSCI recently and will be eligible for the Hong Kong Connect soon thanks to rule amendment.

The company delivered a decent topline growth in 3Q2018 but its profit fell short of expectation. We highlight potentials from the food supply chain solution. We also discuss implication from MoBike acquisition.

We review our SOTP valuation of Meituan and believe there is an upside.

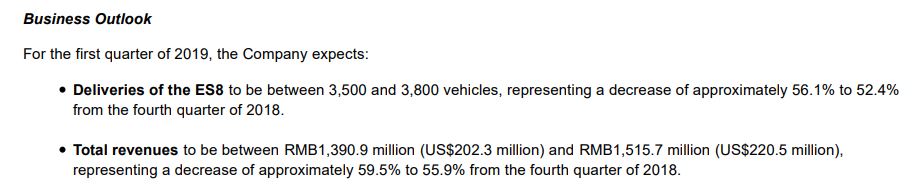

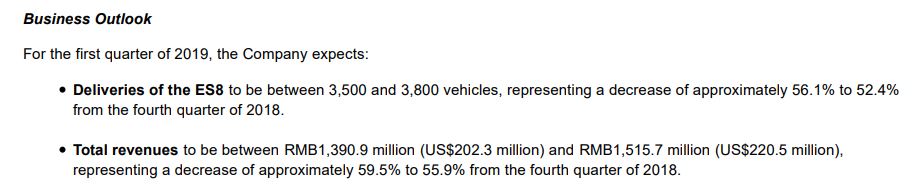

NIO Inc (NIO US) fell 17% in its after-hour trading session post announcement of its Q4 results. The company turned a gross profit in Q4 while the number of cars delivered in the full year 2018 was 11,348 has beaten their own 10,000 cars target. The company is currently trading 62% above its IPO price.

However, the worrying part lies in its guidance which could mean that pre-IPO investors have more compelling reasons to lock-in some profits upon lock-up expiry.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

NIO Inc (NIO US) fell 17% in its after-hour trading session post announcement of its Q4 results. The company turned a gross profit in Q4 while the number of cars delivered in the full year 2018 was 11,348 has beaten their own 10,000 cars target. The company is currently trading 62% above its IPO price.

However, the worrying part lies in its guidance which could mean that pre-IPO investors have more compelling reasons to lock-in some profits upon lock-up expiry.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We maintain BUY rating for WICE with a new target price of Bt5.20 (previous target price: 7.50), based on 29xPE’19E, its one year average trading range or 20% discount to Thai transportation sector.

The story:

Cross broader business plays the key growth driver in 2019

We revised down earnings in 2019-21E due to lower-than-expected margins

Risks:

Stronger Baht vs major foreign currencies such as US dollar causes lower income in Baht terms as the main reporting currency is Baht

Higher than expected in fluctuation in freight rates

Intensity of freight forwarding businesses in both domestic and overseas

This article is a round up of the key takeaways from our recent meeting with Sony’s IR team. Our main focus was on the PlayStation and subsequent hardware and software developments, the company’s mobile phones business unit, the pictures unit as well as the semiconductor business.

In the gaming segment, Sony doesn’t see Stadia as a threat since Sony mainly caters to the core gaming segment. Sony does not expect cloud gaming to offer the same quality that consoles offer to core gamers anytime soon. For the time being, Stadia will most likely appeal to casual gamers.

In the pictures segment, Sony is developing a Spider-Verse sequel. A definite release date is yet to be confirmed, however, looking at the first movie’s success, we can expect a similar result for the sequel upon release.

The company also plans to hold onto its mobile communications segment even though it is expected to make losses in FY03/19 as well. For Sony, this segment is crucial in developing 5G technologies.

In the semiconductors segment, Sony expects a demand hike from the number of cameras used per phone. This is in spite of the mobile phone market itself slowing down. Sony expects to increase the ASPs of these sensors going forward as well.

We selectively visited a dozen companies in March and were most impressed with three of them (two of which we happily own):

SISB, Thailand’s only listed education stock, whose market cap has increased more than 30% since its IPO. The future potential growth they are currently working on in Cambodia and China will show up here and spruce the company’s already strong growth. Working in a favorable environment (Thailand’s affluent class is growing) also helps.

MINT, the country’s hotel chain giant and 20th largest chain in the world, sees great growth potential in Europe, where things are slowly turning around after they made two big acquisitions (NH Hotels and Tivoli). Synergies are also materializing with co-marketing and re-branding efforts.

After You, arguably the dessert chain with the highest margin in Thailand. No longer a newbie IPO stock, these guys boast collaboration with global giant Starbucks and branching out into new channels such as After You Durian.

The deal scores marginally positive on our framework owing to its decent track record, and price and earnings momentum.

Its past deals have done well in the long run. Even though it did not perform well over the one-month period, its first week returns have tend to hold up above the deal price.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In our Discover SZ/SH Connect series, we aim to help our investors understand the flow of northbound trades via the Shanghai Connect and Shenzhen Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by offshore investors in the past seven days.

We split the stocks eligible for the northbound trade into three groups: those with a market capitalization of above USD 5 billion, and those with a market capitalization between USD 1 billion and USD 5 billion.

We note that in March, northbound inflows turned more cautious vs strong inflows in February (link to our Feb note) and January (link to our Jan note). Nevertheless we see strong inflows into Healthcare sector, led by Jiangsu Hengrui Medicine Co., (600276 CH). We also highlight Universal Scientific Industrial Shanghai (601231 CH 环旭电子) in the mid cap space that attracted strong northbound inflows.

Huya, a leading live streaming player in China, announced share placement of USD 550 million after market close on April 3rd. In this insight, we will look at recent developments of Huya and score the deal in our ECM Framework.

Naspers (NPN SJ) recently announced another attempt to reduce the holdco discount which has remained stubbornly high despite previous attempts by management to reduce it. Since the announcement there has been movement, so perhaps this time it really is different!

So what is being done? Naspers will spin off its international internet assets, which account for >99% of its value, into a newco. They will then list 25% of newco on the Euronext in Amsterdam by issuing these shares to Naspers’ shareholders. The intention is to create a vehicle which can attract increased foreign and tech investors without the complication of a South African listing. The company believes this has been a key factor behind the wide holdco discount. The move also reduces Naspers weighting in South African indices which is another contributing factor.

Alastair Jones sees the announcement as a positive, although there are still issues with the main listing being in South Africa. He still believes a buyback would be the most effective way to reduce the discount, but Naspers is also keen to keep investing.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

NIO Inc (NIO US) fell 17% in its after-hour trading session post announcement of its Q4 results. The company turned a gross profit in Q4 while the number of cars delivered in the full year 2018 was 11,348 has beaten their own 10,000 cars target. The company is currently trading 62% above its IPO price.

However, the worrying part lies in its guidance which could mean that pre-IPO investors have more compelling reasons to lock-in some profits upon lock-up expiry.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

NIO Inc (NIO US) fell 17% in its after-hour trading session post announcement of its Q4 results. The company turned a gross profit in Q4 while the number of cars delivered in the full year 2018 was 11,348 has beaten their own 10,000 cars target. The company is currently trading 62% above its IPO price.

However, the worrying part lies in its guidance which could mean that pre-IPO investors have more compelling reasons to lock-in some profits upon lock-up expiry.

* The recovery in 4Q2018 shows that CTRP has already survived the new law and the new competitor in 2018. * We believe EPS will grow 12% in 2019. * However, we believe the market has already over-reacted to the news last November that CTRP became the largest online travel agency. * We set a target price of USD23.80, which is 32% below the market price.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.