In this briefing:

- Ten Years On – Asia Outperforms Advanced Economies

- Asian Credit Monitor: 2019 Portfolio Strategy, US Rate Trajectory, China Reform Pause

- TRACKING TRAFFIC/Chinese Tourism: Visits to Macau & HK Surge

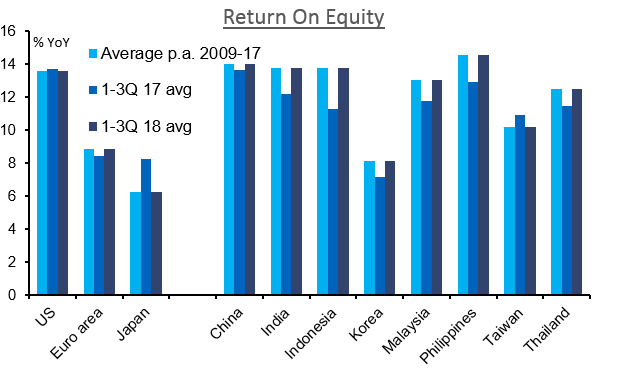

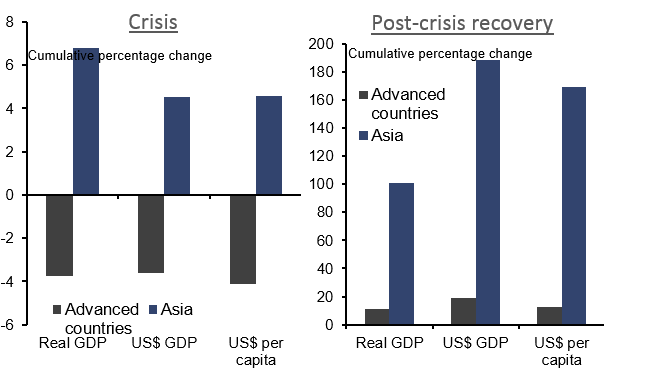

1. Ten Years On – Asia Outperforms Advanced Economies

You might be surprised to learn that in the ten years to 2017 Asia has outperformed advanced economies. Despite extraordinary monetary and fiscal stimulus and the damaging dollar-demand deflationary policies of the ECB, BoJ and BoE, the region is 188% larger in US dollar terms compared with 2007 while US dollar GDP per capita income is 170% higher. The parallel numbers for the advanced countries – the US, euro-area and Japan combined- are 19% and 13%. Asian stock markets have underperformed since 2010 but we believe that investors are still to fully acknowledge Asia’s strong growth fundamentals. Combined with cheap valuations there is significant upside for Asian equity markets.

2. Asian Credit Monitor: 2019 Portfolio Strategy, US Rate Trajectory, China Reform Pause

If we had to make a base observation for Asia credit markets over 2018, it was certainly caught “wrong-footed” like most of its other risky asset counterparts. The combination of a more hawkish Fed in 2018, global quantitative tightening, late-cycle economic conditions, volatility and a strong USD have all served to impact almost all the asset classes negatively. According to some asset allocators, the only asset class which returned positive in 2018 was cash, every other traditional asset class saw losses.

USD direction will further dictate the impact on overall Asian risk, in our view, with many undervalued Asian currencies following their sharp declines in 2018. One of our scenarios includes a range-bound USD in 1H19, followed by a possible reversal in 2H19 on any dovish Fed policy/US economic weakness. In this case, it has the potential to attract incremental portfolio inflows back into Asian risk. We expect a slightly tighter bias in monetary policy in most Asia ex-Japan nations which is supportive for their respective currencies.

In 2019, risk-reward dynamics have improved particularly for Asian investment grade (“IG”) where we see more limited MTM pressure. We expect a more defensive market at least in 1H19 which supports our heavier IG bias. We suspect larger investors would continue to reallocate depending on the outcomes of the China-US trade dispute and their view on US risk (arguably near its last late-cycle expansion legs). We continue to be extremely selective in Asian high yield (“HY”) which have been impacted by idiosyncratic situations including credit deterioration and rising defaults. Exogenous factors such as the potential for “fallen angel” risk (i.e. a migration from issuers on the cusp of IG, “BBB-” into HY) as well as net portfolio outflows from HY, EM and leveraged loan funds are ongoing concerns. Despite cheaper valuations in Asian HY, we still see skewed risk-reward (with larger potential risks).

In the US, our base case expects the Fed to hike 1-2 times (quarter point each) for 2019, premised on still below-trend inflation and external factors. We think it is near the tail-end of its current tightening cycle, but we would continue to monitor the US supply-side (labour markets, employment gaps, prices) for further clues. A sustained upshot to the previous factors may have the potential to prolong the Fed’s tightening cycle.

On China’s side, we have seen a critical reversal in policy towards selective expansion/accommodation again as economic reforms instituted 3 years ago have been reprioritized. China’s difficult task to balance growth targets and restructure its economy is a perennial issue. We would also expect defaults to remain elevated domestically/internationally as a new paradigm of credit investing takes root in China.

Finally, we would like to wish our readers luck in investing and trading in the year ahead.

3. TRACKING TRAFFIC/Chinese Tourism: Visits to Macau & HK Surge

A year ago we began publishing Tracking Traffic/Chinese Tourism as the hub for all of our research on China’s tourism sector. This monthly report features analysis of Chinese tourism data, notes from our conversations with industry participants, and links to recent company news and thematic pieces. Our aim is to highlight important trends in China’s tourism sector (and changes to those trends).

In this issue readers can find:

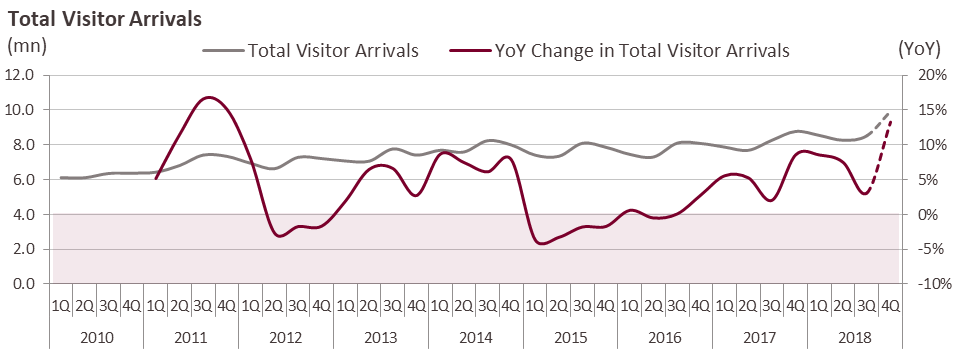

- A review of China’s outbound tourist traffic in November, which strengthened: Lifted by extraordinarily strong growth in visits to Hong Kong and, to a lesser extent, Macau, Chinese outbound travel demand rebounded strongly in the seven regional destinations we track. But the fact that November’s growth was led overwhelmingly by Hong Kong and Macau — destinations close enough for weekend or day trips from population centers in Southern China — suggests Chinese tourists’ purse strings are still tight.

- An analysis of November domestic Chinese travel activity, which turned weaker: November data from China’s three leading airlines and the Ministry of Transport show moderating domestic travel demand. For combined rail, highway, and air travel, November demand grew by less than 3% Y/Y. Along with the change in destination mix for outbound travel (that favors ‘nearby’ destinations), it now appears domestic demand has weakened, too.

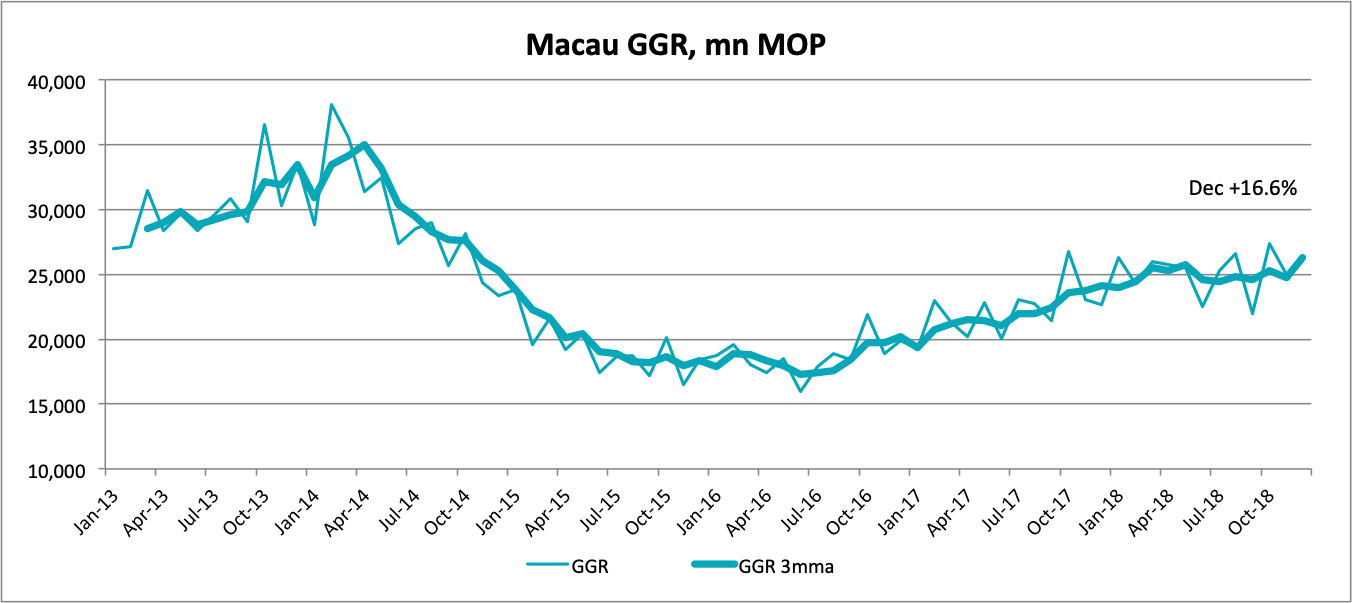

- Links to other recent news & research on Chinese tourism: Readers can check out our quick takes on Macau’s December GGR figure, preliminary GTV and revenue figures released by Ctrip.Com International (Adr) (CTRP US), declining US visa issuance to Chinese tourists, and Qatar Airways’ new investment in a leading Chinese airline.

Although we remain positive on the long-term growth of Chinese tourism, it’s clear that near-term demand has weakened substantially. We continue to take a negative view of travel intermediaries like Ctrip, which face intensifying competition from many sources. We are more positive on the prospects of actual owners of Chinese travel and tourism assets, like hotel chain Huazhu Group (HTHT US) and Air China Ltd (H) (753 HK).

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.