Mobvista (1860 HK)‘s IPO was priced just above the low-end at HKD4/share, the retail tranche was 1.8x covered while the institutional tranche was moderately oversubscribed. I have covered most aspects of the deal in my earlier insights:

In this insight, I’ll provide an update on the deal dynamics, valuations and provide a table with the implied valuations at different share price levels.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

IPO listings this week have mostly been within our expectation. Mobvista (1860 HK), Natural Food International H (1837 HK), and Fosun Tourism (1992 HK) have all struggled to hold on to their IPO price on the first day of trading. Unfortunately, WuXi AppTec Co (2359 HK) has also struggled on this first day despite our expectation that the company should be trading at a relatively smaller 19% A-H premium which would imply about 11% upside based on Ke Yan, CFA, FRM‘s sensitivity analysis and Wuxi Apptec’s A share Friday close price.

In the US, Tencent Music Entertainment (TME US) performed well within our expectation. The company’s share price opened about 9% above IPO price. As Sumeet Singh has mentioned in his insight, Tencent Music IPO – Firework – Trading Strategies, this is unlikely going to be a bumper IPO and short-term investors could take profit at high single-digit to low double-digit returns on debut. Indeed, after a decent debut, TME has collapsed below its IPO price, probably due to investors taking profit as the broad market traded poorly on Friday.

Next week, all eyes will be on Softbank Corp (9434 JP)‘s debut and Mio Kato, CFA summarised in his note some of the reasons why Softbank Corp could perform poorly in the near term. Bookbuild results have been mixed. Bloomberg report suggested that Softbank’s international bookbuild was 2-3x oversubscribed while retail offering was at almost 2x. However, Nikkei Asian Review’s article reported that it has been a struggle to sell the IPO shares to retail investors. In any case, we will put out a note next week on our thoughts on bookbuild, updated valuation of peers, and how we think the IPO will likely trade after the recent series of events.

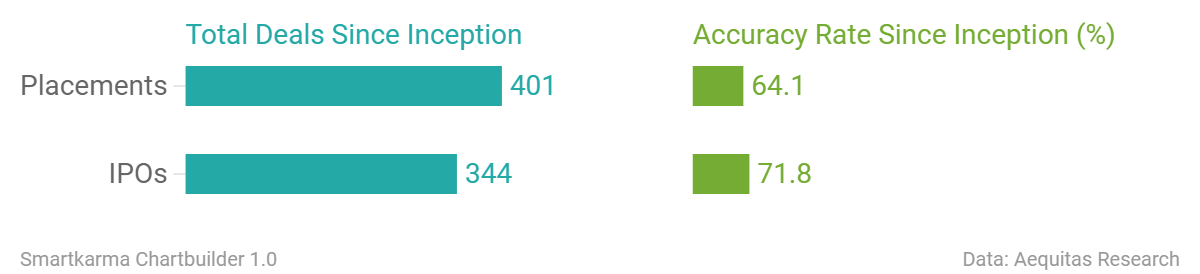

Our overall accuracy rate is 72% for IPOs and 64% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings this week

Shanghai Henlius Biotech (Hong Kong, ~US$500m)

Ingrid Millet (Hong Kong, re-filed)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

New industry data this week, plus take-aways from our latest discussions with company managements, all confirm that the likely trend in the industrial segment of the global real estate industry is for rental rates to rise.

The growth in e-commerce is continuing to accelerate globally. In some key market, this is “triggering a land grab for distribution space that experts say is accelerating”.

Therefore, the increasing scarcity value of well situated industrial real estate in high demand markets is likely to continue to push up rental rates to higher and higher levels.

Given our expectation that fundamentals driving the growing demand for Last Mile Industrial real estate are likely to persist, we continue to expect this segment to outperform the broader Real Estate sector for the foreseeable future.

Fosun Tourism (1992 HK)‘s IPO was priced at the low-end, HKD15.60/share. The retail tranche was undersubscribed while the institutional tranche was said to be moderately over-subscribed. I have covered most aspects of the deal in my earlier insights:

In this insight, I’ll provide an update on the deal dynamics, valuations and provide a table with the implied valuations at different share price levels.

This share class monitor provides a snapshot of the premium/discounts for various share classifications around the region, and comprises four sets of data:

Alpha Smart (ALS HK), the parent of Chinese menswear fashion retailer GXG, plans to raise US$300m in its Hong Kong IPO. L Catterton, LVMH’s investment arm, along with another PE investor, owns a 73% stake in the company.

Earnings have been consistently growing with the highest contribution still coming from its flagship brand “GXG”. The recent expansion of the online channel has further aided sales growth, with ASL claiming to be the largest menswear retailer in terms of online sales.

Apart from a large dividend payout which covered half of the acquisition costs for L Capital, nothing much seems to have changed recently. In addition, operating cash flow has not kept pace with earnings due to a consistent increase in inventory. To add to that there are a few related party issues as well including some stores being run by former employees.

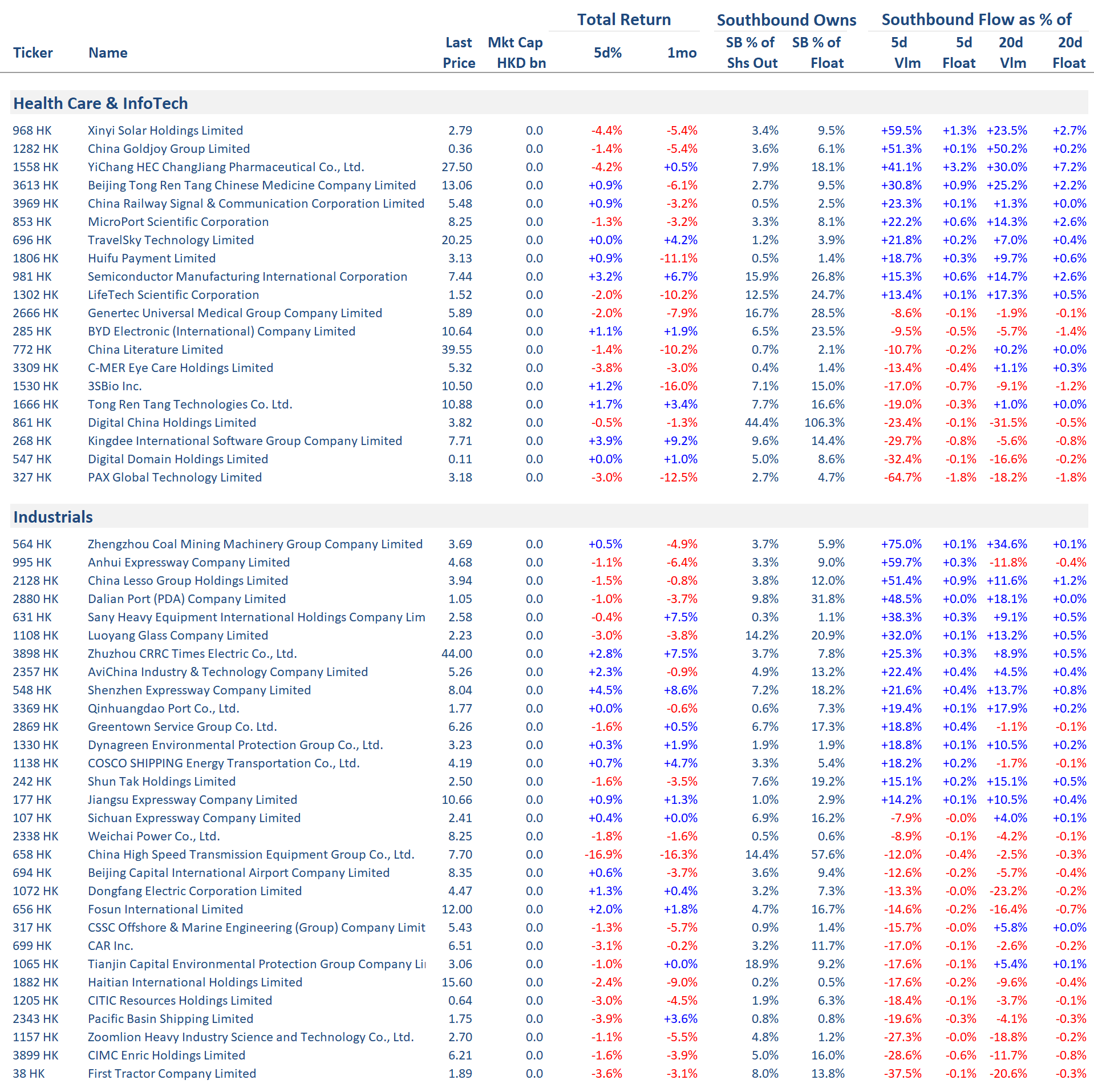

An H/A Spread Monitor Project offering a brief look at recent changes in H-Share and A-Share spreads, Southbound flow and impact, and where the spreads are trading within their own historical ranges.

The Nitty-Gritty Details Follow

There are five sets of data for now: 1. HK-Shanghai Connect Southbound Turnover and Net Buying vs Indices and HKEx Turnover 2. Top 20 Net Southbound buys and sells over the last 5 days 3. H-Share/A-Share Discounts, Changes in Discount over 1 and 4 wks, Changes in Southbound Flow 4. Southbound Flow as a % of Volume and Float on All Eligible Stocks 5. H-Share/A-Share Sector Discount Ranges and Averages Charted Over the Last 12 months

Historical Southbound Flows: Outright & vs HKEx Turnover

Net Southbound flows continue to be somewhat lacklustre. November was negative after a couple of positive months. December so far is very mildly positive. Northbound had been strongly positive for months, but say RMB 5.8bn of outflows in October only to rebound to RMB +32.5bn in November. So far this month, NB is positive too.

data source: capitalIQ, HKEx, calculations Travis Lundy

Xinyi Energy Holdings Ltd (1671746D HK) is a solar farm operator seeking a listing on Hongkong stock exchange raising up to US$680M (including Greenshoe). The company announced a price range of HK$1.89/share to HK$2.42/share valuing the company between HK$12.5B to HK$16B. The company is issuing 1.9B shares and 282M shares of Greenshoe as part of the IPO. The offer price will be announced on 13th December. The shares are expected to trade on Hongkong Stock Exchange on the 21st December.

Based on GER’s analysis valuations appear rich and the investors should avoid the IPO which are priced at a significant premium at the lower end of offer price compared to its peers.

At the time of the IPO we were quite negative on China Tower (788 HK) prospects. However, in recent calls and meetings our view has changed and become more constructive. Chris Hoare now believes that China Tower is managing to generate co-location growth outside the Master Services Agreement (MSA) and at a much lower level of capital intensity (perhaps up to 50%) than indicated in the IPO. Management has also proven to be more open to shareholders than expected and with lower capex, higher FCF generation we upgrade to a BUY with a HK$1.60 target price. The stock has started to move as the market has begun to understand the more positive outlook. It will be interesting to see if China Tower is allowed to retain these benefits long term.

Natural Food International H (1837 HK)‘s IPO was priced at the low-end at HKD1.62/share. The retail tranche was 1.4x covered and the institutional tranche was said to be moderately over-subscribed. I have covered most aspects of the deal in my earlier insight,

In this insight, I’ll provide an update on the deal dynamics, valuations and provide a table with the implied valuations at different share price levels.