On Monday, Bilibili Inc (BILI US) unveiled plans to raise around $192 million (based on the closing price of $18.95 per ADS) through a public offering of 10.6 million ADS and a concurrent offering of $300 million convertible senior notes. Also, certain selling shareholders will offer 6.5 ADS in the offering.

We believe bilibili’s fundamentals are mixed as rapid monthly active users (MAUs) and non-mobile games growth is offset by a declining margin and higher cash burn. Overall, the proposed offering is unnecessary and highly opportunistic, and we would not participate in the offering.

Bilibili announced a USD 300 million share placement and a USD 300 million convertible note placement after market close on Monday. This is the first major placement since Bilibili’s IPO in March 2018. In this insight, we will provide our thoughts on the deal and score the deal in our ECM Framework.

CVC is looking to raise about US$353m through the sale of about 648m Map Aktif Adiperkasa PT (MAPA IJ) shares in the follow-on offering.

Map Aktif (MAPA) is a sports, leisure, and kids retailer in Indonesia. It is a subsidiary of Mitra Adiperkasa (MAPI IJ). The selldown might not be totally unexpected as CVC planned to exit its investment by 2020. However, post this selldown it will still have 192m share left.

In my previous insights I’ve covered the company background, its projected growth, compared it to its main listed peer and other yield assets in India:

In this insight, I will re-visit some of the deal dynamics, comment on share price drivers and provide a table with implied valuations.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Huya, a leading live streaming player in China, announced share placement of USD 550 million after market close on April 3rd. In this insight, we will look at recent developments of Huya and score the deal in our ECM Framework.

Naspers (NPN SJ) recently announced another attempt to reduce the holdco discount which has remained stubbornly high despite previous attempts by management to reduce it. Since the announcement there has been movement, so perhaps this time it really is different!

So what is being done? Naspers will spin off its international internet assets, which account for >99% of its value, into a newco. They will then list 25% of newco on the Euronext in Amsterdam by issuing these shares to Naspers’ shareholders. The intention is to create a vehicle which can attract increased foreign and tech investors without the complication of a South African listing. The company believes this has been a key factor behind the wide holdco discount. The move also reduces Naspers weighting in South African indices which is another contributing factor.

Alastair Jones sees the announcement as a positive, although there are still issues with the main listing being in South Africa. He still believes a buyback would be the most effective way to reduce the discount, but Naspers is also keen to keep investing.

The deal scores marginally positive on our framework owing to its decent track record, and price and earnings momentum.

Its past deals have done well in the long run. Even though it did not perform well over the one-month period, its first week returns have tend to hold up above the deal price.

Polycab India (POLY IN) plans to raise around US$190m in its IPO through a mix of selling primary and secondary shares. It is the largest manufacturer of wires and cables in India with a 12% market share, as per CRISIL research. The company also recently entered the consumer electrical segments.

In this insight, I’ll run the deal through our IPO framework, and comment on valuation and updates since the previous filing.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Studio City, a spin-off by MLCO US, was listed on October 18th, 2018 and its lock-up will expire next week on April 16th. The company raised USD 359 million in its IPO with the majority of the shares taken up by its shareholders.

In this insight, we will review the company’s operation, shares subject to lock-up expiry and its valuation vs peers.

Changliao Inc (CL HK) is looking to raise about US$100m in its upcoming IPO. The company just filed its draft prospectus with the HKEX last week.

Changliao is a fast-growing social networking entertainment platform. The business model of engaging and monetizing users through interactive games is interesting.

However, the need for an IPO is questionable since the company has a healthy net cash balance sheet and it had paid out dividends in the past two years. It can easily finance its growth through debt or operating cash flow.

Tencent is an investor in the firm, however, it had only invested RMB9m in the company in FY2016. There are no other notable investors despite several rounds of financing.

In this insight, we will look at the company’s business model, analyze its financial performance and operating metrics.

The company has been reporting flattish earnings for the past few years and remains well positioned in its main segments. HOLI is net cash, it has ample cash for that matter, and it has been generating operating cash flow consistently. It hasn’t provided any specific reasons for the capital raise. Which makes one wonder if this is just an opportunistic raise.

In my view, either the company needs to clearly disclose the intended use of capital or it needs to offer the deal at a very wide discount to where the shares are currently trading.

AGC Inc (5201 JP) plans to raise US$215m (including over allotment) via a secondary offering of share, this represents 2.9% of the outstanding shares.

The deal scores a mixed score on our framework, aided by its cheaper valuation while it scoring is hampered by its under performance versus it regional peers. However, the shares have been correcting since the deal was announced and the deal represents just a few days of ADV.

Almost 150 years ago in 1871, a modern postal service was established in Japan by the new Meiji government. The following year, a government-sponsored nationwide network of postal services was launched. Postal money orders started in 1875 and other money and payment services started in the following two decades. In the first decade of the 20th century, domestic money transfers and pension payment receipt were launched. In 1916 postal life insurance sales began. Life annuity sales began a decade later. The Japanese postal system of teigaku deposits started in 1941. In 1949, postal operations were established as the Ministry of Posts alongside the Ministry of Electric Communications (Telecommunications), and eventually both were subsumed into the Ministry of Posts & Telecommunications. In 2001, the business of the Japanese postal system was separated into the Japan Postal Agency, a short-lived entity set up under “central government restructuring” which took place that year. In 2003, the postal system was set up as the Japan Post Corporation under a law which established it as a statutory public corporation (in England, the Bank of England, the BBC, and the Civil Aviation Authority are such companies).

The issue of privatisation – i.e. making it responsible for its own accounts, which would take things one step further rather than being a government budget item – had long been mooted but constantly rejected because it might cost jobs and reduce services. Finally after several Lower House LDP politicians voted against Koizumi’s proposal to split the Japan Post Corporation into four parts in summer 2005 and the Upper House knocked it down, Koizumi dissolved both houses of the Diet and called a snap election saying that it was a referendum on postal privatization. He won easily and the bill was passed a month later. Things were iffy as a privatized company for a few years until after the 2011 Tohoku Earthquake, after which the government needed to find sources of extra funds to finance reconstruction. In 2012, the government announced it would sell shares to the public within three years.

Three years ago and change, the government of Japan launched the promised public offering for Japan Post Holdings (6178 JP) (“JPH”), which acted as a holding company for Japan Post Bank (7182 JP) (“JPB”), and affiliated insurance arm Japan Post Insurance (7181 JP) (“JPI”). At the time, the triple-IPO at ¥1.4 trillion was the largest one-day offering in almost two decades, and the situation created some significant and interesting short-term trading opportunities.

In the end, there was always going to be “overhang” because the explicit goal of the privatization policy was to get JPH’s ownership of JPB and JPI below 50%. In doing so, the bank and insurance operations could then go out and compete with other banks and insurers; currently they are to a large extent restricted from offering new products and entering new markets.

Japan Post Insurance announced on April 4th after the close that JPH would offer 168.1mm shares of Japan Post Insurance to the public, with another 16.9mm shares offered in an over-allotment. This is big news as it is almost 31% of the shares outstanding of Japan Post Insurance and will dramatically increase its float.

One can say it is a big deal – ¥450bn (~US$4bn) of stock and at announcement it was equivalent to the last 477 days of traded volume. More importantly, this ALMOST like an IPO in that the placement is almost 3x the original IPO size (66mm shares) and will get a lot of foreign investor attention.

In addition, JPI announced it would conduct a buyback for up to 50 million shares (with a spending limit of ¥100 billion) on the ToSTNeT-3 off-hours auction-like trading system on days between April 8th and April 12th.

JPH announced in its “Intention To Sell shares” announcement (end of section 1 on p2) that if it sold shares in the ToSTNeT-3 trade, it would likely reduce the number of shares it offered.

The stock rallied very sharply Friday, rising 3% at the open and ending the morning session up 3% but rising much further in the afternoon to end up 9.9%.

After the close Friday, the company announced it would spend ¥100bn to buy up to 37.411mm shares pre-open on ToSTNeT-3 on Monday morning. That was 6.2% of shares outstanding.

The dynamics of this ToSTNeT-3 buyback were discussed in Japan Post Insurance – The ToSTNeT-3 Buyback. The ToSTNeT-3 buyback was, at its basest, an interesting garbitrage trade for a limited number of traders but the resulting dynamics are important. They influence the supply in the Offering, the dynamics of demand, and may influence trading patterns into pricing.

There are several things going on here. There is a huge offering, a buyback, earnings accretion, a float change, substantial sale to foreigners this time, and index changes. Sooner and later, it will mean a substantial move towards getting closer to 50%, and the fact that this is now investable for lots of institutional investors.

It is worth looking at these aspects independently to better understand demand for the offering as a whole.

Read on for more.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

I’ve covered some of the background and index weightage impact in my earlier insight: Japan Post Insurance Placement – 3x the IPO Size – Basics and Index Impact. For people interested in reading more about the history and background, I’ve covered the IPO and JPH sell down in the below series of insights:

Below is a recap of the key IPO/placement research produced by the Global Equity Research team. This week, we update on the bevvy of placements offered by various companies. After placements by Pinduoduo (PDD US) and Sea Ltd (SE US) , we saw more offerings from HUYA Inc (HUYA US) , Bilibili Inc (BILI US) and Qutoutiao Inc (QTT US). We update on these three offerings and perhaps big picture, this could reflect a signalling inflection point in these shares. More details below

In addition, we have provided an updated calendar of upcoming catalysts for EVENT driven names below.

Best of luck for the new week – Arun, Venkat and Rickin

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Placements activity picked up momentum this week as evidenced by the number of follow-on offerings launched by a handful of US-listed Chinese tech companies. It all started with Qutoutiao Inc (QTT US) ‘s follow-on offering, then followed by Bilibili Inc (BILI US)‘s equity + convertible note placement, and ending the week with HUYA Inc (HUYA US)‘s follow-on offering and Baozun Inc. (BZUN US)‘s convertible bond and placement.

On the other hand, Ruhnn Holding Ltd (RUHN US)‘s debut this week had been a total disaster. It closed 37% below its IPO price on the first day. This is the worst first-day performance among Chinese ADRs (deal size >US$100m) in the past six months.

Back in Hong Kong, Dongzheng Automotive Finance (2718 HK) also broke its IPO price on the first day after relaunching at a much lower price. As per our trading update note, considering that there will be greenshoe support, we thought that the risk to reward could be favorable for a trade (from its first day mid-day price of HK$2.57).

As for placements, Ronshine China Holdings (3301 HK) seems to have made its equity raise a yearly affair. The company is back to tap the equity market through a top-up placement and it has done the same in 2017 and 2018. The initial deal size was small, US$122m, but was upsized later on. The share price traded well post-placement, closing 9.5% above its deal price of HK$10.95 on Thursday.

Map Aktif Adiperkasa PT (MAPA IJ) will be closing its bookbuild for its follow-on offering next Tuesday (pricing on Wednesday). We heard that books are already covered as of Thursday.

Accuracy Rate:

Our overall accuracy rate is 72.4% for IPOs and 63.5% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

Changliao AKA 派派(Hong Kong, ~US$100m)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Yesterday, post-market close, Japan Post Holdings (6178 JP)(JPH) announced that it will sell 185m shares (including over-allotment) or 30.8% of Japan Post Insurance (7181 JP)(JPI) amounting to US$4bn. JPI plans to buy back up to 50m shares out of these, leaving around US$3.1bn worth of stock to be placed. Out of these 185m shares, 30% will be placed with foreigners.

The selldown is part of the government’s plan for privatization under which JPH is supposed to reduce its stake in JPI and Japan Post Bank (7182 JP)(JPB) to around 50%. This was highlighted in the IPO of the three entities in 2015. Thus, the deal is not totally unexpected but the timing of it was never certain. For people interested in more about the history and background, we’ve covered the IPO and JPH sell down in the below series of insights:

Follow-on offerings by Chinese ADRs are the flavour of the day. Hot on the heels of Qutoutiao Inc (QTT US) and Bilibili Inc (BILI US), HUYA Inc (HUYA US) filed for a potential $550 million public offering without presenting any details on the new ADS being offered. Also, certain selling shareholders will offer shares in the offering.

Huya is one of the few recent Chinese “new-economy” IPOs which has lived up to the hype by delivering a creditable post-IPO financial performance. While Huya has proven to be a good IPO, we believe this follow-on offering is highly opportunistic and would be tempted to participate only at a large discount.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The Homeplus REIT IPO is surely a key landmark deal in the 20 year history of the Korean REIT market. We have a positive view on the Homeplus REIT IPO and believe it has a good chance of generating 6-9% return per year (including dividends and capital appreciation) in the next three years. The Homeplus REIT is geared towards the investors who are happy with 6-9% annual returns with relatively low downside risk. For the investors that are seeking 10%+ annual returns, this deal is probably not suitable for them.

The following are the five major factors why we believe the Homeplus REIT market will be a success:

Stable dividend yield of 6-7%.

Opportunity to get included in a global REIT index (such as EPRA Developed Asia Index).

Supermarkets related REITs are viewed safer than residential and commercial office building related REITs globally.

Global investors have wanted to invest in a big, liquid, safe retail REIT with stable dividends in Korea for a long time. The Homeplus REIT possesses many of these characteristics.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

GDS Holding, the largest carrier-neutral, cloud-neutral data centre operator in China, is raising USD 400 million from a private placement. The deal was launched last night (US time) post the company’s results announcement. In this insight, we will cover:

Keppel Infrastructure Trust (KIT SP) plans to raise US$450m via an equity placement and non-renounacable preferential offering. Its sponsor, Keppel Corp Ltd (KEP SP) will subscribe in the placement and the preferential offering to maintain its 18.2% stake.

KIT announced the acquisition of IXOM in Nov 2018 and has been talking about the need to issue equity ever since. Its earlier presentations seem to indicate a preference for raising a large sum via an equity issuance. Furthermore, despite the smaller raise the accretion to DPU is probably only marginal.

CanSino is a China-based biotechnology company with a focus on vaccine development. In our previous insight (link to Part 1 and Part 2), we have discussed CanSino’s drug pipeline, the competitive landscape, and the valuation.

As the company is starting pre-marketing, we will provide an updated valuation based on new information obtained from the approved application document. Our base case valuation for CanSino is USD 856 million on a pre-money basis. Majority of the rNPV based SOTP valuation still comes from its meningococcal conjugate vaccine (MCV2 and MCV4). Over the past few months, the company has completed Phase III for MCV4 and submitted NDA (new drug application) for MCV2 candidates.

Embassy Office Parks REIT (EOP IN) plans to raise around US$680m in its India IPO. Of this, it has already raised around US$125m from Capital Group, who came in as a strategic investor. EOP will primarily hold office assets in Bengaluru, Pune and Noida with a total portfolio size of around US$4.5bn.

In my previous insights I’ve covered the company background, its projected growth and compared it to its main listed peer and other yield assets in India:

In this insight, I’ll cover the deal dynamics, compare the revised forecast in the RHP with the earlier one from the DRHP, comment on the yield boost from the zero coupon debt and run the deal through our framework.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Ruhnn Holding Ltd (RUHN US) is an e-commerce platform which drives sales through KOLs (key opinion leaders). Ruhnn is the largest internet KOL facilitator in China as measured by revenue, the number of online stores and GMV in 2018 according to Frost & Sullivan. Ruhnn is backed by Alibaba Group Holding (BABA US), an 8.6% shareholder, and is seeking to raise $200 million through a Nasdaq IPO.

However, Ruhnn’s rhetoric does not match its financial performance. On balance, we are inclined to give this IPO a pass.

DAF is a fast growing auto finance company which acquires customers through a network of dealership around China. Its net interest income grew by 66% CAGR from FY2016 to FY2018 while net fees/comms income and profit grew by 39.6% and 61% CAGR over the same period.

However, most of its growth originated from ZhengTong dealers and joint promotion arrangement. Excluding loans from joint promotion arrangement, gross outstanding loan had only grown by 12% CAGR.

In this insight, we will look at the company’s business, analyze the competitive landscape, provide thoughts on valuation, and some questions for management.

Haidilao International, the largest Chinese cuisine player by valuation, was listed on September 26th last year and lock-up expiry will be on March 26th. The stock has returned 24% since listing.

As it heads into lock-up expiry, we will examine Haidilao’s shareholder structure and potential shares up for sale.

Haidilao was included in the Hong Kong Connect Scheme on December 10th, 2018 and shares held by mainland investors have been consistently increasing.

But we think Haidilao’s valuation has built in a perfect growth scenario.

Risk of de-rating for Haidilao warrants a short position.

Futu Holdings Ltd (FHL US)‘s IPO was priced at the top-end at US$12/ADS raising a total of US$160m, including the US$70m raised from General Atlantic via a concurrent private placement.

In my earlier insights, I looked at the company’s background, past financial performance, scored the deal on our IPO framework and compared it to Tiger Brokers:

In this insight, I will re-visit some of the deal dynamics, comment on share price drivers and provide a table with implied valuations.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Last Friday, Gds Holdings (Adr) (GDS US), the largest third-party data centre operator in China, announced the placing price of its public offering of 11.9 million ADS. At the placing price of $33.50 per share, GDS will raise net proceeds of $385.5 million which will be used for the development and acquisition of new data centres.

We are positive on GDS as the business remains in rude health due to strong revenue growth, rising margins and high revenue visibility. Overall, we would participate in the public offering at the placing price.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Starting with bad news in Korea, Homeplus REIT (HREIT KS)‘s IPO was pulled on the 14th of March which when it was supposed to price. The reason cited was weak demand which stemmed from growth concerns and difficulty in valuing this business.

On the other hand, Hong Kong’s IPO market is getting busier. This week alone, we had Dongzheng Automotive Finance (2718 HK) and Koolearn (1797 HK) that have already opened for bookbuilding and will price next week. We also heard that Sun Car Insurance is already started pre-marketing and it will likely open its books next week. The company had only just re-filed their draft prospectus last week.

In India, the focus is on Embassy Office Parks REIT (EOP IN) as this is the country’s first ever REIT IPO. It is also the first time there is a strategic tranche in an Indian IPO which has been taken up by Capital Group. Sumeet Singh has pointed out in his insight that with cost of debt of the REIT being at 9 – 9.25%, it is hard to fathom buying equity at a FY2020E dividend yield of 8.25%. This yield had already been inflated by the lack of interest payments. For detailed explanation, read his insight, Embassy Office Parks REIT IPO – FY19 Revised Down, Yield Propped up by Zero Coupon Bond.

In other countries, we heard that Leong Hup International (LEHUP MK) is aiming to pre-market next month whereas, in Australia, there had been chatter that Prospa Advance Pty (PGL AU) may be back for an IPO again after it had beaten its own estimates from the IPO prospectus.

Accuracy Rate:

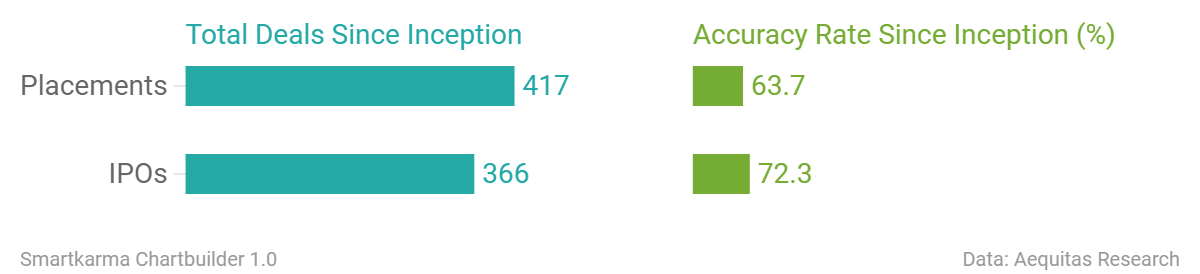

Our overall accuracy rate is 72.4% for IPOs and 63.7% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

FriendTimes Inc. (Hong Kong, >US$100m)

Frontage (Hong Kong, re-filed)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Embassy Office Parks REIT (EOP IN) boasts an impressive portfolio of office assets with adequate geographic diversification, strong client relationships and sound reputation.

Constructing/acquiring new office area is an integral part of Embassy’s growth strategy.

This requires massive capex (e.g. Embassy’s last 3 year’s capex is Rs32bn). Since it pledges to distribute 100% of its EBITDA to unit holders, it will have no cash left for capex or making interest payments.

Hence, post the IPO borrowings will increase to fund the capex. The interest expenses will lower the NDCF and in turn Dividend per unit.

Embassy may choose to issue fresh units to fund part of the capex in the future. This will also result in lower Dividend per unit.

Ascendas India Trust (AIT SP) shows us why you should be conservative while building in capital appreciation of REIT units. Despite revenues growing 3.18x over FY08-18, Ascendas’ Dividend per unit is flat over the period as its borrowings growth (29% Cagr) far outdid its revenue growth (12.3% Cagr). It also diluted equity to the tune of 37% over the period. Its units have seen no capital appreciation over the last decade.

Embassy’s effective yield (adjusted for interest outgo notwithstanding its proposed workaround) works out to 6.4%- unattractive in our view.

In this insight, we will look at the updates on financials and operating metrics, compare it to other listed online education companies, and run the deal through our framework.

The increase in spending on marketing has not yielded the intended results as the growth rates of student enrollment and gross billings slowing down. Furthermore, aggressive spending behavior is similar to that of STG and LAIX and both companies did not perform well post listing.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Subscription rate is 797 to 1. Offer price was fixed at ₩48,000, substantially higher than the upper end. Deal size is now ₩168.5bil. Company value is put at slightly higher than ₩1tril. Demands are spread out pretty well between long-term funds and hot money and local and foreign investors as well. All of the orders are universally placed at 75% of upper end or higher.

Local street is betting on Autoever/Glovis merger not long after this IPO. That is, HMG is still wanting the initial Glovis/Mobis merger plan. To better manage to win shareholder support, they must be thinking that bigger Glovis can be an answer. This means HMG should do whatever it takes to make Autoever bigger in the immediate future.

This is what local street is betting on and why they went really aggressive on this IPO. As witnessed in the bookbuilding results, this street mentalitywon’t be changed any time soon. We should expect even stronger prices after new shares are listed on Mar 28.

In this report, we provide a trading strategy for Hyundai Autoever Corp (0978519D KS) IPO, which is expected to start trading on March 28th. The IPO price has been finalized at 48,000 won, which is 9% higher than the high-end of the original IPOprice of 44,000 won. The institutional investors’ demand for the Hyundai Autoever IPO was very strong at 797 to 1.

Given the very strong institutional demand for this IPO, it appears that our base case valuation (59,454 won), which is 24% higher than the IPO price, may be too conservative. A more likely scenario now is that the stock reaches about 60,000 won to 65,000 won in the first few hours of trading on the first day, overshooting its intrinsic value and sells off a bit for a few days/weeks, enters a consolidation phase and then resumes its higher share price again.

Of the 913 institutional investors that participated in the Hyundai Autoever IPO survey, 89% of them thought that the intrinsic value of the company should be more than the high end of the IPO price range (44,400 won), which provides a strong vote of confidence that this IPO should do well once it starts trading.

CanSino Biologics started its book building today to raise up to USD 160 million to list in Hong Kong. In our previous insights (links provided below), we provided a detailed analysis of the company’s core drug candidates, its shareholders and our thoughts on valuation. In this insight, we will cover the following topics:

ESR Cayman (ESR HK) aims to raise up to US$1.5bn in its planned Hong Kong listing, as per media reports. The company is backed by Warburg Pincus and counts APG, the Netherlands’ largest pension provider, as one of its main investors.

PagerDuty Inc (PD US)is a US based software company which is ready to complete its IPO in the next several weeks. Founded in 2009, PagerDuty helps companies to respond quickly when their websites go down. PagerDuty’s software helps companies to respond to items such as customer complaints and helps companies to spot problems. The company is known for capitalizing on its AI (Artificial Intelligence) models to quickly solve problems of why websites go down.

The company has an excellent, diversified base of more than 10,000 customers in 90 countries including IBM, The World Bank, Airbnb, Netflix, GE, and Gap. One of the strong points of PagerDuty is the fact that it has gathered massive amounts of data from its more than 10,000 customers. The company also boasts a very high customer retention rate (139% net retention rate). A combination of the company’s strong AI capability coupled with the increasing amounts of Big Data provide a strong competitive advantage for the company since its AI capability may improve and get smarter with additional Big Data and continuous problem solving of why websites go down.

PagerDuty was most recently valued at $1.3 billion in September 2018 in a private market valuation (led by T.Rowe Price Group investing $90 million in the company), representing 16x the company’s annual revenue of $79.6 million as of 12 months ending January 2018.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

In my earlier insights, I looked at the company’s background, past financial performance, scored the deal on our IPO framework and compared it to Futu Holdings Ltd (FHL US):

Biologics holdings is looking to raise upto US$517m by selling a 4.2% stake in Wuxi Biologics (Cayman) Inc (2269 HK). This will be fourth placement by the company since it listed less than two years ago. Below is a link to our coverage of the listing and the earlier placement:

Each of the past placement has been of a similar size and has generally done well. The company recently reported results which were ahead of street estimates. The deal scores a marginal positive score on our framework but there is still a lot more selling left once the 90-day lock-up expires.

The company is an internet key opinion leader (KOL) incubator in China. Revenue and GMV grew at impressive rates of 63% and 57% YoY in FY2018, respectively.

The idea of being able to leverage on KOLs influence over consumers to understand demand and retain consumers is interesting but Ruhnn has yet to demonstrate that it has a sustainable business model.

Gross margin has deteriorated and losses widened as a percentage of revenue. Service fee paid to KOLs as a percentage of revenue has increased and showed little improvement in 9M FY2019. The company depends heavily on the top KOL, Zhang Dayi, to generate revenue, almost half of the company’s GMV and revenue is generated from her.

Frontage Holding, a contract research organization subsidiary of A-share listed Hangzhou Tigermed Consulting (300347 CH), re-filed to list on the Hong Kong Stock Exchange recently. We have covered the company’s fundamentals in our previous insight here. In this insight, we will provide an updated analysis based on new data available from the new prospectus, as well as our thoughts on valuation.

Tencent Music Entertainment (TME US) reported its full year results today, post US market close. Revenue growth was slightly ahead of estimates as paying ratio continue to improve for both online music (subscription revenue) and social entertainment (live streaming). Growth for the latter continued to be driven more by ARPU rather than user growth.

The concerning bit in the results was the decline in gross margins as the company continues to invest in more content.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.