This weekly newsletter pulls together summaries of the top ten most-read Insights across Event-Driven and Index Rebalance on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. FEFTA Classification Changes Summer 2025

- The Ministry of Finance has published an updated “FEFTA List” of classifications of listed companies as of July 15, 2025.

- 50 names lowered their ranks from the most “core” Type 3 to Type 2(20), or Type 1(30). 104 names raised from Type 1(51) or Type 2(53) to Type 3.

- Smartkarma readers may want to peruse the lists and details to see if they think companies are trying to protect themselves (from threats as yet not known by the public).

2. Merger Arb Mondays (18 Aug) – Santos, Shibaura, ENN Energy, Kangji, OneConnect, Smart Share

- I summarise the latest spreads and newsflow of merger arb situations we cover across Hong Kong, Australia, New Zealand, Singapore, Japan, Indonesia, Malaysia, Philippines, Thailand and Chinese ADRs.

- Highest spreads: Smart Share Global (EM US), Mayne Pharma (MYX AU), ENN Energy (2688 HK), Santos Ltd (STO AU), Joy City Property (207 HK), Oneconnect Financial Technology (6638 HK).

- Lowest spreads: Bright Smart Securities (1428 HK), Pacific Industrial (7250 JP), Shibaura Electronics (6957 JP), Ci Medical (3540 JP), Soft99 Corp (4464 JP), Ainsworth Game Technology (AGI AU).

3. Smart Share Global (EM US): Hillhouse Crashes The Party. And Rightfully So

- Nearly seven months after receiving a preliminary non-binding proposal, Smart Share Global (EM US) announced on the 1st August a firm Offer had been entered into.

- The Offeror consortium, led by Mars Guangyuan Cai, Chairman and CEO, made an Offer of US$1.25/ADS, a 74.8% premium to last close; but ~20% below net cash + short-term investments.

- Now Hillhouse has thrown its hat into the ring with a US$1.77/ADS NBIO. Smart Share’s special committee of independent directors should engage.

4. Today’s HMM Tender Follow-Up Disclosure and Hedge Ratio Setup

- KOBC’s core mission hinges on HMM; without it, no real mandate. Structural incentive to hold remains, so its active tender participation is still questionable.

- Still, max proration risk seems base case, with weak Q2, soft Q3 freight outlook, and post-tender skew pointing bearish for HMM.

- Spread >10% makes this too good to pass, but should also watch policy risk — better to lock futures hedge early as flows show players scrambling for cover.

5. HMM Tender Side Play: Targeting a Basis Squeeze Ahead of Sep Expiry

- Most traders are starting in September, rolling into October. Sep/Oct spread volume has picked up unusually fast, clearly reflecting hedge demand linked to the tender

- As September expiry approaches, basis-squeeze risk rises, likely pushing September cheap and October expensive, widening the spread — creating a clear side trade opportunity.

- With a basis squeeze expected near September expiry, we could enter a Sep/Oct spread (short Sep, long Oct) and also watch for spot-futures decoupling to play the cash-futures spread.

6. Hanon Systems Announces a Major Potential Rights Offering

- On 14 August, Hanon Systems (018880 KS) announced a potential rights offering capital raise. The exact amount will be finalized at the EGM next month.

- The significant size of the rights offering is expected to burden its largest shareholder Hankook Tire & Technology (161390 KS) which owns a 54.8% stake in Hanon Systems.

- We believe the potential rights offering is likely to continue to negatively impact Hanon Systems by diluting its existing shareholders.

7. Krungthai Card (KTC TB): Still A Buy As Pledged Shares Further Decline

- Back in May this year, shares in Krungthai Card (KTC TB), XSpring (XPG TB), BEC World Public (BEC TB), and The Practical Solution (TPS TB) all went limit down. Twice.

- This situation was discussed in Krungthai Card (KTC TB): Buying Opportunity After Margin Call. Reportedly Mongkol Prakitchaiwattana had pledged his shares in all four companies, leading to margin calls.

- On the 16th August, the SET released an updated list of securities pledged, with pledged shares in KTC now at 2.3% of shares outstanding, down from 16.3% in May.

8. Curator’s Cut: Singapore Unlocks Value, India’s Jewellery Caution & Taiwan’s Top ETF’s Rebalance

- Welcome to Curator’s Cut, a fortnightly roundup of standout themes from the 1,200+ Insights published over the past two weeks on Smartkarma

- In this cut, we review value-unlocking moves by Singapore-listed companies, take stock of India’s jewellery retail market, and track how Taiwan’s largest ETF drives flows for its adds and deletes

- Want to dig deeper? Comment or message with the themes you’d like to see highlighted next

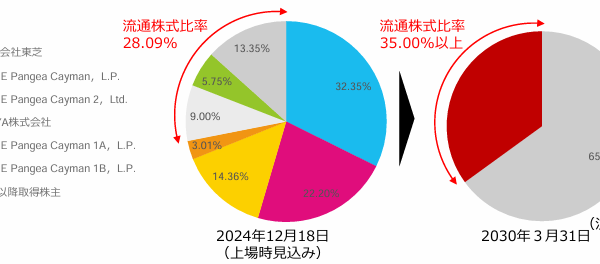

9. [Japan M&A] Minebea Forces a Game of Regulatory Chicken on Shibaura (6957 JP)

- Minebea Mitsumi (6479 JP) has bid ¥6,200/share for Shibaura Electronics (6957 JP). The tender ends 28 August. YAGEO has over bid now to ¥6,635/share.

- YAGEO’s regulatory clearance decision may not arrive before 1 September, after the Minebea tender closes. Minebea now says they will neither bump nor extend.

- Minebea is hoping people will throw in the towel and tender because if their tender ends and Yageo’s fails, it might a long way down. There are possibilities but… scary.

10. US Government May Acquire Equity Stakes in Samsung Electronics and TSMC

- According to Reuters, the US government may be interested in acquiring equity stakes in Samsung Electronics and TSMC in exchange for CHIPS and Science Act grants.

- The US government is exploring ways to take equity stakes in these two Asian tech giants that have been expanding their semiconductor facilities in the United States.

- If the US government decides to invest $10 billion each in Samsung Electronics and TSMC, they would represent about 3% and 1% of Samsung Electronics and TSMC’s market caps, respectively.