This weekly newsletter pulls together summaries of the top ten most-read Insights across Event-Driven and Index Rebalance on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Toyota Industries (6201) – SURPRISE! It’s a TOYODA Takeover Proposal (Good Governance May Not Win)

- On Friday after the close, media reports surfaced that Toyota Motor (7203 JP) Group chairman and founding family member had put forth a take-private proposal to Toyota Industries (6201 JP).

- The number quoted was ¥6trln market cap (most) or EV (FT), financed by personal funds, 3 megabanks, and reportedly some group companies.

- ¥6trln market cap would be +50%. ¥6trln EV +16%. Simultaneously shocking but somehow not surprising. Opportunistic, and surprisingly elegant as a family/group/cultural solution. More below.

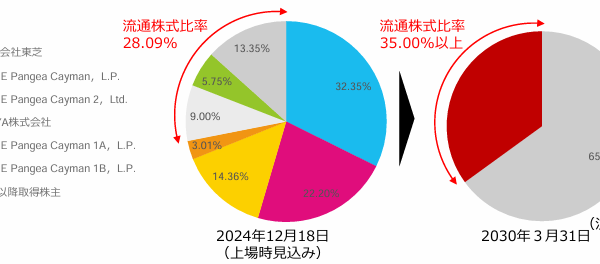

2. Toyota Industries (6201) – Thinking About How To Value a ¥6trln Bid

- Toyota Industries is a relatively complicated business. It owns lots of shares of Toyota and other companies. It has a financing business, and runs ¥500+bn of EBITDA.

- As of 31 March 2025, the “Enterprise Value” of the Operating and Financing Business together was about ¥2.2trln. The “Asset Ownership Business” was at ¥2.8trln (1yr ago it was ¥4trln).

- If you think buying the Operating Business at 6x EBITDA is appropriate, that means the Asset Ownership Business block buy gets done at 31-March-2025 prices. Worth thinking about.

3. Toyota Industries (6201 JP): A Rumoured Privatisation with Several Unknowns

- Toyota Industries (6201 JP) shares were set to hit the daily upper limit of JPY16,225 due to press reports of a privatisation bid valuing it at JPY6 trillion.

- Toyota Industries confirmed receiving a going-private proposal from a special purpose company, while Toyota Motor (7203 JP) said it is considering all possibilities, including a partial investment.

- There are still several unknowns, including the price, the identity of the offeror, potential irrevocable commitments, the financing structure, and the timeline.

4. Hanwha Ocean (042660 KS) Placement: Index Implications; Stock Appears Wildly Overvalued

- Korea Development Bank is looking to sell 13m shares of Hanwha Ocean (042660 KS). That is US$740m at the top end of the marketed range and 4x ADV.

- Following the sale, Korea Development Bank will still own over 15% of the company and that will be an overhang for the stock. Plus the stock appears wildly overvalued.

- There will be limited buying from passive trackers at the time of the placement with bigger passive flows coming through in June and August.

5. Ather Energy IPO: Expensive and No Immediate Index Inclusion

- Ather Energy is looking to raise INR 30bn (US$349m) in its IPO, valuing the company at INR 120bn (US$1.4bn). The company appears to be expensive compared to peers.

- Ather Energy could be added to one global smallcap index in August/November and to another in December/March. Small Cap classification for AMFI and no major local index inclusion.

- The continued selloff in Ola Electric will give investors pause, especially given Ather Energy‘s stagnant market share and continued losses. There is supply in Ola Electric with PE/VC investors selling.

6. Shibaura Elec (6957) – Minebea Overbids Yageo’s Overbid of Minebea’s Overbid of Yageo – ¥5,500

- A Nikkei article today suggested Minebea Mitsumi (6479 JP) would overbid Yageo’s dramatic 20% overbid of Minebea’s early ¥4,500 overbid of Yageo’s initial ¥4,300 bid for Shibaura Electronics (6957 JP).

- Now the news is out. MinebeaMitsumi has bid ¥5,500. Shibaura Electronics has endorsed. This is bang-in-line with the expected path. The question is now YAGEO’s overbid, expected 7 May.

- If I were YAGEO, I would wait for Shibaura’s earnings a couple of days later, then overbid by ¥100-150 and go for 35 days. There’s optionality there.

7. Poon’s Underpriced Takeover. Minorities Deserve Better

- Dickson Concepts (113 HK) (DC)’s Chairman, Dickson Poon (& relatives), holding 61.98%, have tabled an Offer by way of a Scheme for shares not held, at HK$7.20/share (best & final).

- That compares to DC’s net cash (as at 30 Sept 2024) of HK$7.44/share. Plus financial assets comprise an additional ~HK$2.16/share.

- The IFA will cite liquidity and DC’s historical discount to NAV, and opine “reasonable”, and perhaps even “fair”. It is neither. Minorities should vote this down. But probably won’t …

8. Merger Arb Mondays (28 Apr) – Seven & I, Shibaura, Makino, Bright Smart, ENN Energy, Tam Jai

- We summarise the latest spreads and newsflow of merger arb situations we cover across Hong Kong, Australia, New Zealand, Singapore, Japan, Indonesia, Malaysia, Philippines, Thailand and Chinese ADRs.

- Highest spreads: Oneconnect Financial Technology (6638 HK), Insignia Financial (IFL AU), ENN Energy (2688 HK), Seven & I Holdings (3382 JP), Smart Share Global (EM US).

- Lowest spreads: Shibaura Electronics (6957 JP), Makino Milling Machine Co (6135 JP), Sinarmas Land (SML SP), Millennium & Copthorne Hotels Nz (MCK NZ).

9. Meilan Airport (357 HK): Possible Unconditional MGO at HK$10.62

- Haikou Meilan International Airport Company entered an SPA with Hainan Island Construction (600515 CH) to sell its Hainan Meilan International Airport (357 HK) 50.19% stake at RMB9.85 per share (HK$10.62).

- The SPA completion requires several regulatory approvals, which are low-risk, particularly as Hainan SASAC is the largest shareholder of the offeror and the seller.

- Under Rule 26.1 of the Takeovers Code, upon completion, the offeror will be required to make an unconditional mandatory cash offer at HK$10.62 per share. The MGO price is final.

10. Dickson Concepts (113 HK): Sir Poon’s Scheme Offer Below Net Cash

- Dickson Concepts Intl (113 HK) disclosed a Bermuda scheme offer from the controlling shareholder (Sir Poon) at HK$7.20, a 50.6% premium to the last close price.

- The offer is final. While the offer represents an all-time high and is attractive compared to historical trading ranges, it is below net cash.

- No disinterested shareholder holds a blocking stake, and retail seems supportive (lowering the risk of the headcount test). The offer, while light, will likely succeed.