This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Intel (INTC.US): 18A May Have Been Too Rushed; Now All Hopes Rest on 14A.

- On July 24, chip giant Intel announced that its latest 18A advanced process is progressing smoothly. However, the next-generation 14A process will be developed “based on confirmed customer commitments.”

- Apple (AAPL US) adopt Intel’s 14A process for its future M-series chips, while NVIDIA Corp (NVDA US) is expected to use the same process for its entry-level gaming GPUs.

- U.S. President Trump is imposing tariffs on countries around the world, which is indirectly pressuring some manufacturers to accelerate the establishment of U.S.-based production facilities.

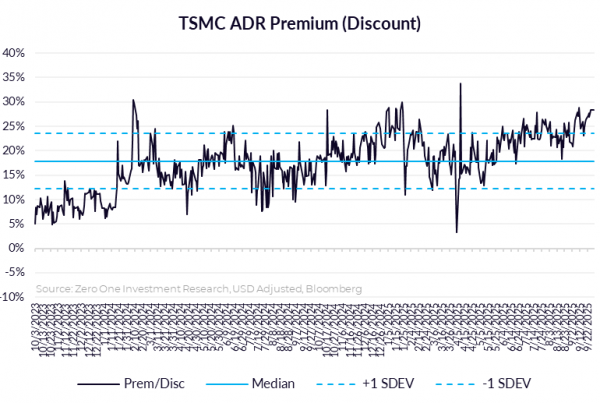

2. Taiwan Dual-Listings Monitor: TSMC ADR Premium Remaining Unusually High; UMC & ASE Headroom Changes

- TSMC: +26.3% Premium; Opportunity to Go Short the ADR Premium

- UMC: -1.2% Discount; ADR Headroom Falls Yet Again by a Significant Amount

- ASE: +0.7% Premium; Opportunity to Go Long the ADR Premium — ADR Headroom Has First Change in a Long Time

3. Microsoft FYQ425. Who Says Elephants Can’t Dance?

- Q425 revenues of $76.4 billion, up 5.5% QoQ, 18% YoY and handily beating guidance of $73.8 billion.

- Azure surpassed $75 billion in revenue in FY25, up 34% YoY, driven by growth across all workloads.

- Contracted backlog grew by $53 billion QoQ to reach $368 billion. Wow!

4. Yageo’s AI-Driven Momentum and Strategic Expansion Through Shibaura Acquisition

- 2Q25 Results Summary: Reports Broad-Based Growth with Specialty Margin Strength

- Yageo Inventory Recovery Marks a Demand-Led Inflection for Hardware Components

- Update on Shibaura Acquisition: Still on Track, Strategic Synergy in Focus

5. Taiwan Tech Weekly: Mediatek Reportedly Bests Broadcom for Meta Custom Chip Win; Semi Key Indicators

- MediaTek Reportedly Wins Meta’s 2nm AI Chip Order Over Broadcom

- Memory Monitor: SK Hynix Vs. Micron — Different Speeds & Focus, Same Structural Shift

- Semi Key Indicators Q2 2025: PC, Smartphone Unit Shipments, Global Semi & WFE Sales All Looking Good

6. Intel Q225. GM Obfuscation, Red Flags & 14A Now Officially A Risk Factor

- Intel reported Q225 revenues of $12.9 billion, up $200 million QoQ, flat YoY but $1.1 billion above the guided midpoint. After that revenue beat, things went downhill from there.

- CEO Lip Bu Tan said he will review and approve all future company product designs prior to tape out. Sounds like a vote of no confidence in the design team.

- Intel’s 10 Q now lists the possibility of pausing or abandoning 14A as a risk factor with doomsday details about the implications for the company

7. ASEH (3711.TT): FX Impact; AI Gains Attention; 3Q25 Grows, but GM and OPM Decline QoQ.

- 3Q25 guidance (Assuming US$1 = NT$29.2.): Consolidated US$ revenue: +12-14% QoQ; NT$ revenue: +6-8% QoQ; Gross margin: -1 to -1.2ppts QoQ; OPM: -0.1 to -0.3ppts QoQ.

- Still keep US$1bn advanced packaging guidance despite AI boom (TSMC revised up).

- Long-Term success definition for ASE: Transition from OSAT model to foundry-aligned scale.

8. Vanguard (5347.TT): FX Impact; Mild Recovery, Slightly Better Than 3Q25 Preview.

- 3Q25 Outlook (based on USD/TWD = 28.7): Wafer Shipments: +7–9% QoQ; ASP: +1–3% QoQ; Gross Margin: 25–27%.

- Revenue Mix (Industrial, Auto, 3C): Industrial + Automotive: 40%+ (majority industrial; automotive in teens) ; Communication & Computing: 20%+ each ; Consumer: 10%+.

- 2025 Dividend Policy : Will maintains NT$4.5 per share dividend.

9. Hon Hai(2317.TT): Form Strategic Alliance Via Share Swap with TECO (1504) For Global AI Data Center

- Hon Hai Precision Industry (2317 TT) and Teco Electric & Machinery (1504 TT) held a joint press conference this afternoon to announce the formation of alliance through a share swap.

- Teco (1504) TT and Hon Hai (2317 TT) stated their target markets extend beyond Taiwan and Asia, to include substantial business opportunities in the U.S. and the Middle East.

- Foxconn Chairman Mr. Young Liu also noted that as AI data centers scale up rapidly and demand surges, modular design is increasingly favored.

10. Tokyo Electron (8035 JP): Why the Big Downward Revision?

- Tokyo Electron’s share price dropped 18% on Friday following the announcement of weak Q1 results and a huge downward revision to H2 FY Mar-26 guidance.

- Push-Outs and/or cancellations of orders due to the uncertainty caused by President Trump apparently caught managment by surprise. Costs also rising as management ramps up capex and R&D.

- Impact of Trump’s yet-to-be-announced tariffs on semiconductors is still unknown, but 15% base rate on Japan already a negative.