This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Why HBM is the Hottest Thing in Memory

Investing in semiconductors can be pretty simple if you let it be.

At a high level, I believe you want to invest in the secular at a decent price or invest in places where there are unwarranted dislocations.

Sometimes the entire ecosystem says one thing and the stocks say another. Usually, the ecosystem is right.

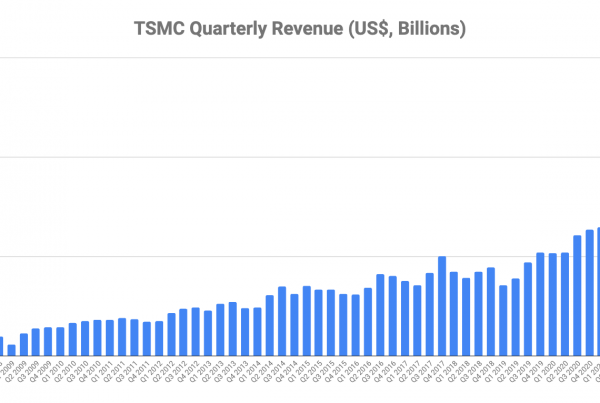

2. TSMC (2330.TT; TSM.US): Sales Should Be Gradually Increasing QoQ in 2024F; IPhone 16 Is on Schedule.

- Taiwan Semiconductor (TSMC) (2330 TT) is ramping up its CoWoS capacity, with the aim of increasing new capacity by 32k wafer/month in the end of 2024F.

- In the second half of 2024F, the Apple (AAPL US) iPhone 16 will contribute to revenue from shipments.

- The semiconductor industry is expected to rebound in 2024F, with TSMC being one of the leaders.

3. Global Semi Sales Decline 2.3% MoM In January

- It’s the first MoM decline in semi sales since February 2023, but it’s a seasonal thing & YoY comparisons continue to grow stronger.

- Forecasting 10% YoY growth in 2024 semiconductor sales, in line with TSMC’s outlook

- $1 trillion in annual semiconductor sales will likely happen in 2032 based on a 7.7% CAGR over the coming decade.

4. Taiwan Dual-Listings Monitor: Long TSMC Taiwan Shares Vs. ADR on Historically High Spread; UMC, ASE

- TSMC: +22.9% ADR Premium is Near an All-Time High; Long Taiwan Shares vs. Short the ADR

- UMC: 2.2% Premium; Flipped Positive From a Discount; Likely to Contract

- ASE: +13.3%; Short the Historically High Spread at the Current Level

5. GlobalWafers (6488.TT): 1Q24F Is a Down Quarter; Anticipating a Much Better Growth Rate in 2025F.

- The sales in January 2024 were the lowest during the period of 2022-2024, indicating a likely downtrend for the first quarter of 2024.

- Demand is expected to be flat or slightly increase in 2Q24F for GlobalWafers, which is encouraging.

- The market for 12″ raw wafers is expected to have a more stable demand-supply balance, while raw wafers of 8” and smaller sizes could experience reduced demand in 1H24F.

6. Silicon Wafers Area Shipments Decline 14.3% YoY in 2023

- Silicon wafers area shipments (in MSI) declined by 14.3% YoY in 2023

- Wafer revenues also declined by 10.9% to $12.3 billion over the same period

- We expect Q124 revenues to be down ~20% QoQ and anticipate a further 5% YoY decline in full year 2024 shipments

7. PC Monitor: Long Dell Vs. Short Acer Update; Dell & HPQ Results Indicate Opportunity in Asus

- Dell has outperformed Acer and other Taiwan PC names Asus and MSI by a wide margin. Close Long Dell vs. Short Acer. Dell’s value gap has dissipated.

- Latest indications from Dell and HP highlight that the AI PC’s will drive upgrades from customers, but the PC recovery remains soft. AI PC impact only in 2025E.

- Dell and HPQ’s recent results provide positive color for upcoming Asus, Acer, and MSI results. Trade: Long Asus into its upcoming earnings results.