In this briefing:

- Maoyan Entertainment (猫眼娱乐) IPO: Lackluster Demand but CNY Blockbusters Could Be a Catalyst

- Healthscope (HSO AU): Don’t Count on a Material Bump to Brookfield’s Binding Offer

- Last Week in Event SPACE: Toppan, Hyundai Heavy, Descente, Healthscope, Eclipx, Pioneer, Earthport

- ECM Weekly (2 February 2019) – Maoyan, China Tower, Dexin, Chalet Hotels, Bharat Hotels, Wingarc1st

- Netmarble Games + Tencent = The Most Likely Consortium to Acquire NXC Corp/Nexon?

1. Maoyan Entertainment (猫眼娱乐) IPO: Lackluster Demand but CNY Blockbusters Could Be a Catalyst

Maoyan Entertainment was priced at HKD 14.8/share and will start trading today. We summarize the latest information with updates on our valuation in this short note, prior to the trading debut. Our recent studies on the movies slotted to launch during the Chinese New Year period suggest that the box office during the CNY period could be a positive catalyst to Maoyan, which lists right before the CNY.

Our previous coverage on Maoyan Entertainment

2. Healthscope (HSO AU): Don’t Count on a Material Bump to Brookfield’s Binding Offer

Healthscope Ltd (HSO AU), Australia’s second-largest private hospital operator, finally received a firm but marginally lower offer from Brookfield Asset Management (BAM US) through a recommended implementation deed.

With Brookfield’s binding proposal providing a floor, the shares are viewed as attractive as BGH-AustralianSuper, a rival bidder could start a bidding war. However, we maintain our view that in the event AustralianSuper decides to stick with the consortium, BGH-AustralianSuper’s improved offer is unlikely to provide material upside.

3. Last Week in Event SPACE: Toppan, Hyundai Heavy, Descente, Healthscope, Eclipx, Pioneer, Earthport

Last Week in Event SPACE …

- Toppan Printing (7911 JP)‘s management prefers to run a long/short fund rather than support the company’s long-suffering shareholders.

Hyundai Heavy Industries Holdings (267250 KS) discount to NAV was all set to narrow after Aramco’s intention to acquire 19.9% in Hyundai Oilbank Co; then 31%-held Hyundai Heavy Industries (009540 KS) announced a multi-step split-off, payment in kind and rights issue.

Following Itochu Corp (8001 JP)‘s partial offer, Descente Ltd (8114 JP) has the ability to play dirty and investors and traders should be aware of that.

- Brookfield firms up a reduced offer for Healthscope Ltd (HSO AU), however the BGH-consortium is not out of the picture.

Mcmillan Shakespeare (MMS AU) pushes back on Eclipx (ECX AU)‘s first court date, but MACs have not been triggered.

Pioneer Corp (6773 JP)‘s shareholders vote to implement a self-imposed (self-inflicted?) equity “cramdown” of sorts.

- Bidding could still go crazily higher from here as Mastercard Inc Class A (MA US) and Visa Inc Class A Shares (V US) wrestle for Earthport plc (EPO LN).

- Plus CCASS movements and expected upcoming events for key M&A transactions.

(This insight covers specific insights & comments involving Stubs, Pairs, Arbitrage, share Classification and Events – or SPACE – in the past week)

EVENTS

Toppan Printing (7911 JP) (Mkt Cap: $5.3bn; Liquidity: $14mn)

Campbell Gunn tackled Toppan, whose market capitalisation has grown by only 2% per annum or just ¥34b since December 2013. From the recent peak in June 2017, Toppan shares have underperformed the market by 27% and, for the last year, have been at their most extreme value relative to TOPIX over the previous thirty years.

- Toppan’s investment portfolio (341 companies with an aggregate market value as of the last quarter of ¥498bn) has grown at a 39.1% compound annual growth rate (CAGR) over the last five years, outperforming Toppan’s core operations (6.4% CAGR) and the overall stock market (7.5% CAGR). The economic reality for Toppan is that the company’s investment business has far surpassed the core business in terms of ‘margins’ and contribution to Net Assets.

- The company has become more (relatively speaking) proactive in managing equity risk, and recently sold 10.5m shares in Recruit Holdings (6098 JP) (its largest investment holding) for approximately ¥31.5b, reducing Toppan’s holding in Japan’s leading listing employment services business from 6.57% to 6.05%. With this sale, Toppan’s liquid assets will now exceed US$3b or 58% of the current market capitalisation.

- Toppan’s business and investment portfolio should be radically pruned or eliminated. Such a transformation probably requires a change of management, the presence of an activist investor, or both. The latter is the more likely outcome.

(link to Campbell’s insight: Toppan Printing: Money for Nothing (& Your Clicks for Free)

Hyundai Heavy Industries (009540 KS) (HHIC) (Mkt Cap: $8.1bn; Liquidity: $37mn)

HHIC mainly comprises its own shipbuilding/marine plant business (75% of GAV) and 80.54% in Samho Heavy stake (15% of GAV), both unlisted. Samho Heavy owns a 42.40% stake in Hyundai Mipo Dockyard (010620 KS). HHIC announced it will split-off (no new shares issues) with the surviving company an intermediate holdco (same ticker, 009540) and new opco (unlisted) holding Samho Heavy and the in-house shipbuilding/marine plant business.

- Next the Korean Dev Bank will exchange its 55.7% stake in Daewoo Shipbuilding & Marine Engineering (042660 KS) (DSME) for 15.2mn shares in the intermediate holdco (21.5% of shares out) via a payment in kind.

- Following which, the intermediate holdco will do a ₩1.25tn rights offer to its shareholders, including Hyundai Heavy Industries Holdings (267250 KS).

- Next, DSME undertakes its own rights offer (39.9% of DSME’s shares), via a third party allocation to intermediate Holdco with a target value of ₩1.5tn, in an all cash deal. The intermediate holdco will ultimately hold a 68.3% stake in DSME. DSME will remain a listed company therefore no tender offer to the remaining shareholders is expected, according to Sanghyun Park. Details are not finalised and further information is expected on the 8 March.

links to:

Sanghyun’s insight: Hyundai Heavy/DSME Event – Comprehensive Summary

Douglas Kim‘s insight: Korea M&A Spotlight: KDB Is Ready to Sell Its Stake in DSME to Hyundai Heavy Industries Holdings.

Nexon Co Ltd (3659 JP) (Mkt Cap: $8.1bn; Liquidity: $37mn)

Netmarble Games (251270 KS) officially announced it is interested in buying Nexon/NXC Corp. At this point, it appears that a higher probability scenario is for Tencent Holdings (700 HK) to form a consortium with either Netmarble Games or Kakao Corp (035720 KS) in bidding for Nexon/NXC Corp. Douglas’ justification for this are:

- To avoid the cultural backlash from Korean gamers.

- Tencent is a minority investor of both Netmarble Games and Kakao. Tencent’s 17.7% stake in Netmarble Games is worth ₩1.6tn. Tencent’s 6.7% stake in Kakao which is worth ₩0.6tn.

- Netmarble Games is more focused on games and has a stronger balance sheet than Kakao Corp, which has also shown interest in acquiring NXC Corp/Nexon.

(link to Douglas’ insight: Netmarble Games + Tencent = The Most Likely Consortium to Acquire NXC Corp/Nexon?)

M&A – ASIA-PAC

Descente Ltd (8114 JP) (Mkt Cap: $1.9bn; Liquidity: $3mn)

Relationship problems started in 2013 when Itochu Corp (8001 JP) was pushed out of the leadership spot in Descente without any warning or even any face-saving honorary role for its outgoing leader. This was hostile and the frictions were laid bare for anyone who cared to see them. They got worse when Itochu bought shares last summer without telling Descente. They got even worse when Descente signed a deal which would effectively end in a merger with Wacoal without telling Itochu. So it should have been less of a surprise than it appeared when Itochu announced this past Thursday it would launch a Partial Tender Offer for 9.56% of the shares outstanding of Descente.

- Itochu’s Partial Tender is interesting, and there is a trade here if enough people are sceptical of Descente’s ability to play hardball. It is, however, not particularly cheap, and the shares were below ¥2,000/share last Wednesday for a reason.

- Because Itochu is putting itself in a place to not be able to win (i.e. not control the board post-tender, also knowing that Descente could dilute them at will), this is an invitation by Itochu to minority shareholders to make their opinions known, for the media and commentators to do so too, and for someone else to come in over the top.

- Travis Lundy thinks this goes to close to ¥2800 – and did close at ¥2,771 on Friday – because of expectations that Descente will find a white knight to pay more or that the family could launch an MBO. Anybody who wants Descente doesn’t want it for its Japan business. So paying a higher price than someone who wants to expand aggressively in China to allow entrenched management to not expand aggressively in China requires deeper pockets or a lot more patience.

links to:

Travis’ insight: No Détente for Descente: Itochu Launches Partial Tender

Michael Causton‘s insight: Wacoal and Descente Agree Partial Merger to Head Off Itochu

Healthscope Ltd (HSO AU) (Mkt Cap: $3.1bn; Liquidity: $25mn)

Healthscope has announced it has entered into an Implementation Deed with Brookfield, under which Brookfield seeks to acquire 100% of Healthscope by way of a scheme at A$2.50/share, and a simultaneous Off-market takeover Offer at $2.40/share, both inclusive of an interim dividend of $.035/share. The considerations under these proposals compare to the earlier indicative considerations of $2.585/share and $2.455/share respectively under the unsolicited conditional proposals announced back in November.

- HSO also announced that the BGH-led consortium, which holds a ~20% stake, said it could improve the terms of its previous offer of $2.36/share, provided it was given access to Healthscope’s data room.

- The 3.3% and 2.2% step down in Consideration under the Scheme and Off-market Offer compared to the earlier proposals underscores the uneasy backdrop to this Offer on account of various operational issues faced by Healthscope. It also underlines the fact that even provided due diligence, there can be no guarantee the BGH-led consortium will bump its initial bid.

- Shares are trading at a punchy $2.45/share, facing either the Scheme proposal or the possibility the BGH ups its offer, with or without due diligence. This is a mid-single-digits annualized return which assumes that either BGH will up, or will take the Scheme rather than see whether the Off-Market Takeover gets done. This is okay, but not great. I’d look to enter closer to the Off-market consideration level.

(link to my insight: BGH Lurks As Brookfield Firms Offer For Healthscope)

Clarion Co Ltd (6796 JP) (Mkt Cap: $1.3bn; Liquidity: $10mn)

On 26 October Hitachi Ltd (6501 JP) and Faurecia (EO FP) announced that Faurecia would take over Hitachi car audio and infotainment equipment subsidiary in Clarion a tender offer to be launched 3+ months hence. Clarion has now announced a forecast revision for the fiscal year to 31 March 2019 which involves a shortfall in revenue of 9.1%, a 16.7% drop in forecast Operating Profit, and a drop in Net Profit from ¥1.7bn to a loss of ¥500mn (a ¥2.2bn swing); fortunately Faurecia also announced it will go through with the deal with no changes (other than to extend the Tender Offer to 21 business days).

- This deal is quite straightforward. The deal is on schedule and coming through as planned.

- Travis expects this deal will end up with Faurecia owning over 90% and there will be a Demand For Shares as allowed to Special Controlling Shareholders (under Article 179, Paragraph 1 of the Companies Act) allowing them to force out minorities, potentially by the 3rd week of March 2019.

- At the current close of ¥2,496, it is offering <2% annualized return for slightly more than one-month of cash usage, and negligible risk this deal doesn’t go through. Tight, but to be expected.

(link to Travis’ insight: Faurecia Launches Tender Offer for Clarion)

Eclipx (ECX AU) (Mkt Cap: $520mn; Liquidity: $3mn)

Thirty minutes after Eclipx guided down its FY19 NPATA figure, Mcmillan Shakespeare (MMS AU) announced that the first court meeting to be held on the 1st February – which would consider the Scheme documents that are sent to ECX shareholders – will be rescheduled. No new date was announced.

- Taken purely on the guidance downgrade and the MAC’s described in the SIA, on balance, this deal still looks good to go. I don’t see a MAC being triggered here.

- But this new development could/should also be viewed in conjunction with the large step down in NPATA guidance for FY18 (announced on the 6 August 2018, and resulted in the large decline as seen in the chart below), where FY18 NPATA was guidance was reduced to A$77-$80mn (13-17% growth ) versus prior guidance of 27-30% growth. Perhaps MMS want ECX to come out and say their forecast for annual NPATA is down 10%.

- Still, at a 15% gross spread to terms and trading ~5% above its undisturbed price, prior to Sg Fleet (SGF AU)‘s August proposal – while ECX’s peer group is down 17% on average since SGF’s tilt – the negative news surrounding the NPATA guidance and the MACs appears fully priced in.

(link to my insight: McMillan’s Offer For Eclipx Wobbles)

Pioneer Corp (6773 JP) (Mkt Cap: $228mn; Liquidity: $3.7mn)

The deal is done. Shareholders approved the deal. Given where book value and market prices were on the day before the revised plan was announced on 7 December, Travis expects a spirited appraisal rights process.

- For those who are now looking at this as an arb situation, the return is quite decent if you buy on the bid and can get multiples of leverage and keep them after the shares have been delisted, while waiting for payment. If you can get multiples of leverage only while the shares are listed, it is still pretty OK. If you are an arb with no leverage, this is still OK for a Japanese deal.

(link to Travis’ insight: Pioneer Shareholders Approve Deal | What Next?)

Veriserve Corp (3724 JP) (Mkt Cap: $270mn; Liquidity: $1mn)

SCSK announced a Tender Offer to buy out minorities in Veriserve, in which it holds 55.59% of voting rights. The Tender Offer is at ¥6,700/share which is a 43.6% premium to the last traded price. The price does not seem egregiously unfair, but for investors who own it who think it has another double in it this year they might get upset. And the lack of good process here deserves attention.

- The lack of imagining a competing bid is not good governance. The lack of looking for one is not either. The lack of true fairness opinion is also not good governance.

- Still, it is at a 14+year high. It is a small cap. Not that many people will care. It is not cheap on a PER basis and not really inexpensive on an EV/EBITDA basis.

- There IS a chance, theoretically, that this does not go through. SCSK doesn’t have a super-majority, and if it does not get 11.1% of the shares outstanding, it will not be able to automatically squeeze out minorities. But Travis does not think it will be particularly difficult to get there.

(link to Travis’ insight: SCSK (9719 JP) Launches Buyout of Subsidiary VeriServe (3724 JP))

Jiec Co Ltd (4291 JP) (Mkt Cap: $147mn; Liquidity: $.03mn)

Sumitomo Corp (8053 JP) consolidated subsidiary SCSK Corp (9719 JP) announced a Tender Offer to buy out minorities in JIEC at ¥2,750/share, in which it has 69.52% of voting rights. This deal is a worthwhile example of some of the weaknesses in the execution of the current Corporate Governance Code and the “fairness” of M&A in Japan.

- The lack of a competing bid and true fairness opinion are not good governance. The fact that the bid is 1.4% above the bottom of the Target’s own Advisor’s fair value DCF valuation range while the top of the range is 61.3% higher is disappointing.

- But what are you gonna do? SCSK has a super-majority. The stock is super-duper illiquid. The Offer is a 31% premium to the highest price ever paid for the stock. There is no minimum to the tender so it will be “successful” if no one tenders.

- So you suck it up and buy and tender, or tender what you own. And then you write a public comment to the METI Fair M&A process.

(link to Travis’ insight: SCSK (9719 JP) Launches Buyout of Subsidiary JIEC)

M&A – Europe/UK

Earthport plc (EPO LN) (Mkt Cap: $304mn; Liquidity: $2mn)

Mastercard Inc Class A (MA US) has made a £233mn Offer (£0.33/share) to take over cross-border payments firm Earthport, trumping Visa Inc Class A Shares (V US)‘s offer late December by 10%. The Offer is conditional on 75% of EPO’s shareholders accepting with 13.08% of shares outstanding in the bag. EPO’s shares increased to £0.282 following Visa’s offer, but currently trade at £0.37.50, ~14% above the latest offer, suggesting a higher bid is likely, or at least expected.

- For EPO shareholders, who watched their shares erase 70% of their value over the last 2 years and trade around £0.05 earlier this month, this is a fantastic result. Mastercard’s bid also comes at a 65% premium to the placement at £0.20/share on 4 October 2017.

- A (significantly) higher offer price is plausible. EPO can be seen as a disruptor to these card giants. Instantaneous bank-to-bank transfers and the increase in mobile payments are a threat to their traditional business models as they eliminate payment cards from the transaction loop. Both Visa and Mastercard have deep pockets and EPO would help both Visa and Mastercard expand their product offering.

- There is no clear or discernible pricing methodology to exact where a bidding war will send the share price. But it could get (unsurprisingly) crazier from here. I think a £0.40/share offer is not unreasonable or out of the question, and is a level where shares often found support for a year and half back in 2014 and 2015.

(link to my insight: Earthport the Winner as Mastercard/Visa Jostle For Position)

Ceva Logistics AG (CEVA SW) (Mkt Cap: $1.7bn; Liquidity: $13mn)

CMA CGM SA (144898Z FP) has published its prospectus for what is evidently a heavily orchestrated Public Tender Offer for CEVA. Ceva’s Board has concluded that offer is fair & reasonable but does not recommend shareholders tender. CMA CGM added that “the recommendation to shareholders from the CEVA board not to tender shares in exchange for cash is done in perfect agreement with CMA CGM“.

- CMA CGM currently holds 50.6% of CEVA, via a 33% direct stake with the remainder in derivatives. After a 10-trading day cooling off period, the offer will be open for acceptances between February 12 to March 12, unless extended. It is the intention of CMA CGM to maintain CEVA’s listing.

(link to my insight: CEVA’s Fair & Reasonable Offer; But Please Don’t Tender)

M&A ROUND-UP

For the month of January, seventeen new deals were discussed on Smartkarma with an overall deal size of US$91bn. This number does not include rumours on Nexon Gt Co Ltd (041140 KS) and Capitaland Ltd (CAPL SP)‘s acquisition of Ascendas-Singbridge. The average transaction premium was 43%, or 26% if ignoring Earthport plc (EPO LN)‘s offer. This insight provides a summary of ongoing M&A situations and a recap of news associated with each event situation in January.

(link to my insight: M&A: A Round-Up of Deals in January 2019)

STUBS & HOLDCOS

Hyundai Heavy Industries Holdings (267250 KS)/Hyundai Heavy Industries (009540 KS)

As widely reported in the press and discussed by Douglas Kim (Korea M&A Spotlight: Saudi Aramco Plans to Buy Up To 19.9% Stake in Hyundai Oilbank) and Sanghyun Park (Hyundai Heavy Holdco Trade: Long Holdco / Short HHI (30%) & SKI (70%) On Aramco Deal), Aramco announced an intention to acquire a 19.9% equity investment in Hyundai Oilbank Co (HOC) for US$1.6bn. This places an overall value for HOC at ₩8.98tn (the media is reporting that Aramco plans to value HOC at ₩10tn) or ₩8.2tn for HHI’s current 91.13% stake. This is HHI’s largest investment, accounting for 83%/67% of NAV/GAV.

- HOC initially targeted an IPO in 2018 with an expected market cap and an enterprise value of ~₩8tn and ₩10tn respectively, as discussed by Sanghyun in an earlier insight (Hyundai Oilbank IPO Update: Timeline & Valuation). The IPO was postponed after the regulator picked over the balance sheet; and probably just as well, as falling refining margins resulted in HOC’s operating profit declining 42% to ₩661bn last year. The sale to Aramco is expected to push the IPO back to later this year.

- Prior to Aramco’s involvement, HHI was (and effectively is) a weakish stub with the 31% stake in HHIC accounting for just 32%/26% of NAV/GAV; the unlisted operations and the future earnings of those investments were more critical to understanding HHI’s valuation. This investment by Aramco quantifies the valuation for the majority (~95%) of HHI’s unlisted investments, reinforcing the already somewhat prevalent view that HHI’s discount to NAV was excessively wide.

- But HHI/HHIC weren’t done yet. Just when the NAV was expected to narrow further – especially as additional newsflow filters in on the outcome of the board meetings, the expected timeline to completion, and the possibility of HOC’s IPO later this year – HHIC announced a split-off, a PIK and rights issue. Please refer to this development in the “Events” section above.

(link to my insight: StubWorld: Aramco’s Stake Reaffirms Hyundai Heavy’s NAV; Rusal Gains After Sanctions Lifted)

United Co Rusal (486 HK)/Mmc Norilsk Nickel Pjsc (Adr) (MNOD LI)

The U.S. Treasury (OFAC) has lifted sanctions imposed on En+ Group plc, UC Rusal plc, and JSC EuroSibEnergo. The key to lifting these sanctions was Oleg Deripaska reducing his direct and indirect shareholding stake in these companies and severing his control. All sanctions on Deripaska continue in force.

- Rusal announced that En+ had entered into a securities exchange agreement with Glencore, pursuant to which Glencore shall transfer 8.75% of Rusal’s shares to En+ in consideration for En+ issuing new GDRs to Glencore representing approximately 10.55% of the enlarged share capital of En+.

- The transfer will be done in two stages: 2% to be transferred following the removal of Rusal and EN+ from the SDN list; and 6.75% 12 months later. This two-stage process appears geared to circumvent a mandatory takeover by En+. Hong Kong employs a “creeper” speed limit, where shareholders (holding between 30-50%) can creep their shareholding upwards by 2% in a 12-month period (Rule 26.1 (c)).

- As an aside, after sanctions were lifted, En+ announced seven new directors, including Christopher Bancroft Burnham, who served as Under Secretary-General for Management of the United Nations (alongside John Bolton, Trump’s current national security adviser). Burnham was also on Trump’s Presidential Transition Team

- Rusal’s NAV discount has narrowed to 68.5% from 71% the previous Friday. This compares to the 45-50% discount range prior to the sanctions being imposed. This should narrow further.

(link to my insight: StubWorld: Aramco’s Stake Reaffirms Hyundai Heavy’s NAV; Rusal Gains After Sanctions Lifted

SHARE CLASSIFICATIONS

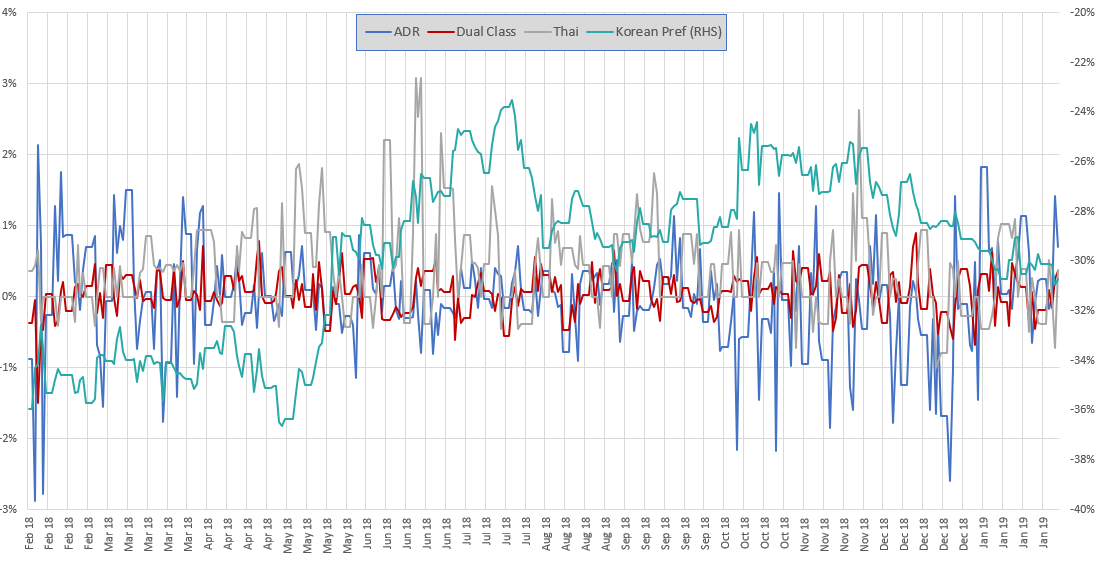

I issued a month-end share class summary, a companion insight to Travis’ H/A Spread & Southbound Monitors and Ke Yan‘s HK Connect Discovery Weeklies. This share class monitor provides a snapshot of the premium/discounts for 215 share classifications (ADRs, Koran prefs, Dual-class, Thai foreign/local Thai) around the region.

The average premium/discount for each set over a one-year period is graphed below.

(link to my insight: Share Classifications: Jan 2019 Month-End Snapshot)

Briefly …

- Sanghyun recommended a long Common and short 1P, after LG Chem Ltd (051910 KS) Common/1P is touched levels last seen in mid October last year. LG Chem Share Class: Common Discount to 1P Should Be Reverted at This Point.

TOPIX & JPX NIKKEI INDEX CHANGES

By Travis’ calcs, there was something on the order of ¥630-650bn of shares of several names to buy on the close this past Wednesday. There was also, therefore, something like ¥630-650bn of TOPIX and JPX Nikkei 400 (almost all TOPIX) to sell on the close of Wednesday.

- Softbank Corp (9434 JP) was expected to see total buying of ¥340bn or so; and Takeda Pharmaceutical (4502 JP) buying of ¥260-280bn at the close. (Both names did trade a very large amount off-market.) A number of other names see TOPIX inclusions because of them listing on TSE1 in December or because of share count increasing because of merger (like LIFULL (2120 JP)) or because of offerings.

- A VERY significant amount of both names were purchased in “guaranteed close” trades where indexers actually paid close-plus pricing until the very end of the day because of fears that the actual market might not close. This meant that on-market volume for Takeda and Softbank was a fraction of what might be expected. The risk was transferred but to get in the flow you had to trade off-market.

(link to Travis’ insight: 31 January TOPIX & JPX Nikkei 400 Major Index Changes)

OTHER M&A UPDATES

The Greencross Ltd (GXL AU)/TPG transaction has now received FIRB approval. The scheme meeting is scheduled for the 6 Feb.

- The Bank Tabungan Pensiunan Nasional (BTPN IJ) deal with Sumitomo Mitsui Financial (8316 JP) went through. SMFG paid IDR 4,282 and almost all BTPN shareholders took them up on it.

- The Centuria Capital (CNI AU) resolution has passed. This resolution was not a vote to decide on tendering the shares held by CNI in Propertylink Group (PLG AU) into ESR’s offer; but to give CNI’s board the authorisation to tender (or not to tender) those PLG shares.

- Minebea Co Ltd (6479 JP) announced that it had received all relevant anti-trust approvals but would not start the Tender Offer for U Shin Ltd (6985 JP) until the start of February (the original announcement had said the Tender would commence at the end of January).

- The interesting path of the Mobius strip of connections that is the HCN continues: China Goldjoy (1282 HK)‘s chairman Yao Jianhui (& others) have pledged 12.14% of China Goldjoy to Huarong Investments (2277HK). Goldjoy is the Offeror for New Sports Group (299 HK).

CCASS

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Name | % change | Into | Out of | Comment |

19.82% | Citi | Outside CCASS | ||

16.19% | HSBC | MS | ||

52.50% | China Yinsheng | Emperor |

UPCOMING M&A EVENTS

Country | Target | Deal | Event | |

| Aus | Greencross | Scheme | 6-Feb | Target Shareholder Approval |

| Aus | Stanmore Coal | Off Mkt | 12-Feb | Settlement date |

| Aus | GrainCorp | Scheme | 20-Feb | Annual General Meeting |

| Aus | Propertylink | Off Mkt | 28-Feb | Close of offer |

| Aus | Healthscope | Scheme | February | Binding Offer to be submitted |

| Aus | Sigma | Scheme | February | Binding Offer to be Announced |

| Aus | Eclipx Group | Scheme | February | First Court Hearing |

| Aus | MYOB Group | Scheme | 11-Mar | First Court Hearing Date |

| HK | Harbin Electric | Scheme | 22-Feb | Despatch of Composite Document |

| HK | Hopewell | Scheme | 28-Feb | Despatch of Scheme Document |

| India | Bharat Financial | Scheme | 28-Feb | Transaction close date |

| India | GlaxoSmithKline | Scheme | 9-Apr | Target Shareholder Decision Date |

| Japan | Pioneer | Off Mkt | 1-Mar | Designation of Common Stock as Securities To Be Delisted by TSE |

| Japan | Showa Shell | Scheme | 1-Apr | Close of offer |

| NZ | Trade Me Group | Scheme | 14-Feb | Approval of Scheme Booklet by Takeovers Panel and NZX |

| Singapore | Courts Asia | Scheme | 1-8-Feb | Despatch of offer document |

| Singapore | M1 Limited | Off Mkt | 18-Feb | Closing date of offer |

| Singapore | PCI Limited | Scheme | February | Release of Scheme Booklet |

| Thailand | Delta | Off Mkt | Feb-April | SAMR of China Approval |

| Finland | Amer Sports | Off Mkt | 28-Feb | Offer Period Expires |

| Norway | Oslo Børs VPS | Off Mkt | 4-Feb | Offer Document to be published |

| Switzerland | Panalpina | Off Mkt | 27-Feb | Binding offer to be announced |

| US | Red Hat, Inc. | Scheme | March/April | Deal lodged for approval with EU Regulators |

4. ECM Weekly (2 February 2019) – Maoyan, China Tower, Dexin, Chalet Hotels, Bharat Hotels, Wingarc1st

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

Happy Lunar New Year to everyone from Aequitas Research!

It has been a fairly quiet week leading up to Chinese New Year but it is not stopping Maoyan Entertainment (1896 HK) from listing on Monday. The IPO was priced at the bottom end of its offering range. The last we checked, it traded up 3% in the grey market on Friday. Ke Yan, CFA, FRM will follow up with a short note of his thoughts on post-IPO trading dynamics and bookbuild subscription levels.

Other updates on IPO in Hong Kong include Sinochem Energy allowing its IPO application to lapse while Koolearn (1373356D HK) and Shangde Qizhi Education re-filed for IPO. Edvantage, another new education IPO (and likely to be borderline US$100m deal size) filed for Hong Kong listing this week as well.

China Tower (788 HK)‘s lock-up will be expiring on the 8th of February and Ke Yan, CFA, FRM mentioned in his insight that any potential placement will be a good opportunity to accumulate the stock. Placements from cornerstone investors will likely be a liquidity event.

In India, Chalet Hotels Limited (CHALET IN) closed its bookbuild with a tepid overall demand of 1.57x. The silver lining for the IPO is that the institutional tranche saw a healthy 4.6x demand, similar to that of Lemon Tree Hotels (LEMONTRE IN) in terms of weak overall but strong institutional demand, which ended up performing well in its IPO.

Other upcoming India IPOs include Mazagon Dock Shipbuilders Ltd (9155507Z IN) and Embassy REIT which were said to be seeking listing towards the end of February. Sterling and Wilson is also looking to file its INR50bn IPO with the Sebi soon.

In Japan, Wingarc1st announced its IPO bookbuild to start on the 25th of February and will be listing in March. It is estimated to be raising about US$380m.

Accuracy Rate:

Our overall accuracy rate is 72% for IPOs and 63.8% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings

- Edvantage Group (Hong Kong, ~US$100m)

- Koolearn (Hong Kong, re-filed)

- Shangde Qizhi Education Group (Hong Kong, re-filed)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

News on Upcoming IPOs

- China’s Sinochem Energy lets Hong Kong IPO application lapse

- India’s Cleartrip eyes IPO as it plans Gulf expansion

- Blackstone set to IPO inaugural $1 billion Reit before March

- Bursa Malaysia’s outgoing CEO says IPO pipeline for 2019 looks strong

- China to Scrap Price, Debut Gain Limits to Entice Tech IPOs

Smartkarma Community’s this week Analysis on Upcoming IPO

- Ebang IPO Preview: Balance Sheet Indicators Point to a Significant Slowdown

- Chalet Hotels IPO Review – Backed up into a Corner

- CStone Pharma IPO Preview: Mixed Prospects of Late-Stage Clinical Drug Candidates

- IPO Radar: KTB Securities, the Only Korean Broker in Thailand

- Shanghai Henlius (复宏汉霖) IPO: Not an Impressive Biosimilar Portfolio

- Dreamtech: Trying for an IPO Again at a Lower Price

- Bharat Hotels Pre-IPO – Catching up with Peers

- China Tower Corp: Trading Idea Before Lock-Up Expiry

- Dexin China (德信中国) Pre-IPO – Related Party Transactions and Partial Asset Listing

List of pre-IPO Coverage on Smartkarma

5. Netmarble Games + Tencent = The Most Likely Consortium to Acquire NXC Corp/Nexon?

Netmarble Games (251270 KS) officially announced on January 31st that it is interested in buying Nexon/NXC Corp. We believe that there is a growing likelihood of a potential consortium which includes Tencent and Netmarble Games to acquire NXC Corp/Nexon. Three major reasons why Tencent may want to partner with Netmarble Games to acquire NXC Corp/Nexon include the following:

- Avoid the cultural backlash from Korean gamers

- Among all the companies that Tencent has invested in Korea, Netmarble Games has become the biggest in amount.

- Netmarble Games is more focused on games and has a stronger balance sheet than Kakao Corp, which has also shown interest in acquiring NXC Corp/Nexon.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.