China Tower Corp, the owner and operator and telecommunication tower network in China, listed on August 8th last year. Over the past six months, the stock has returned 35% with the addition of a number of global investors to its share registry.

As it heads into lock-up expiry in Feb, in this insight we would like to examine China Tower’s performance since listing.

We note that China Tower has delivered a decent set of results for 3Q2018 and it will be a key beneficiary of China’s push into 5G built-up with little uncertainty.

The current valuation of the company was still lower than international tower providers.

With the improving operating metrics and stable income, we believe there are still upsides for China Tower Corp post-lock-up expiry.

A set of generally solid Q3FY19 earnings results from Chinese e-commerce giant Alibaba Group Holding (BABA US) also yielded some interesting insights into the company’s two main logistics-related ventures (CaiNiao Network and on-demand food delivery specialist ele.me).

Unfortunately, the information we can glean from BABA’s Q3FY19 results suggests CaiNiao and ele.me are either growing slower or generating significant losses — or both.

In our view, the main logistics takeaways from BABA’s results are:

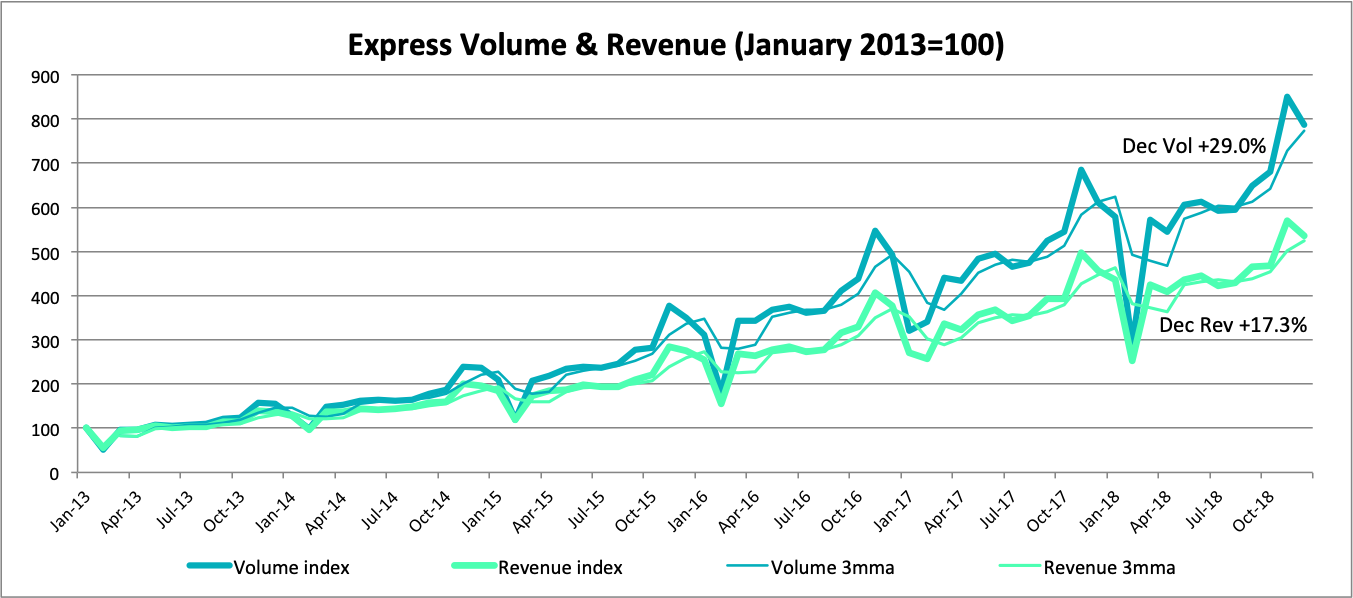

Alibaba’s ‘Core Commerce’ revenues continue to grow faster than express delivery. For the seventh consecutive quarter, Alibaba’s ‘core commerce’ grew much faster than China’s parcel delivery market, outgrowing parcel volume by 8% and parcel delivery revenue by almost 18%. At the margins, China’s express delivery firms are being bypassed by new modes of fulfillment, in our view.

CaiNiao Network’s 15% growth in Q3FY19 is disappointing. Revenue at Alibaba’s CaiNiao Network grew by just 15% Y/Y in the December quarter, to 4.5 bn RMB. In other words, CaiNiao grew even slower than overall Chinese express delivery revenue in the December quarter (+17% Y/Y). That’s disappointing for a company that enjoyed an equity valuation of US$20 bn when Alibaba upped its stake to 51% in late 2017.

The reporting segment that includes ele.me barely grew from Q2FY19 to Q3FY19. Alibaba’s ‘Local Consumer Services’ segment had revenue of 5.2 bn RMB in Q3FY19, representing Q/Q growth of just 2.7%. It’s unclear how much local services venture Koubei contributed to this, as Alibaba only began consolidating its revenues some time in December.

It looks like losses from CaiNiao & ele.me continued to pile up in Q3FY19. Although it’s not an ‘apples-to-apples’ comparison, EBITA losses from the group of companies that includes CaiNiao and ele.me expanded from 5.8 bn RMB in Q2FY19 to over 8.2 bn RMB in Q3FY19. This suggests the deep losses from this group (which were equivalent to about 15% of BABA’s core ‘marketplace’ EBITA in Q2FY19) aren’t going away soon.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

If you are a follower of the Asian stock markets, one of the “rules of thumb” is to carefully follow the investments trails of the “superman” Li Ka-Shing, who has recently publicly declared that he supports Bakkt. On December 31st, 2018, Bakkt raised $182.5 million from high profile investors including Li Ka-Shing backed Horizon Ventures, M12 (Microsoft’s venture capital arm), Intercontinental Exchange (owner of the New York Stock Exchange), Alan Howard, and the Boston Consulting Group.

Starbucks and Bakkt have yet to mention exactly when Starbucks will allow consumers to use Bitcoin to purchase coffee at their stores. In terms of timing, we believe that the probable time frame is likely to be sometime in 4Q 2019 to 2020 when Starbucks will start allowing their consumers to start using Bitcoin at some of their stores. This will represent a crucial positive tipping point for Bitcoin in the next two years.

We think the market is underestimating global LNG supply in the early to mid-2020s from current facilities: initially we look at Australia, which became the world’s largest LNG exporter on a monthly basis in November (~80mtpa or 25% of global supply). Our analysis of Australian LNG supply suggests that production in the early to mid-2020s will be much higher than market expectations of falling production, as fields move into decline. Overall we think this is negative longer-term for the LNG market as supply could supply to the upside but it is a relative positive for the Australian LNG companies.

We think production could grow to around 95mtpa by the mid-2020s due to substantial upside to the nameplate capacity on existing facilities, tie-backs and new developments keeping existing facilities full and utilizing new brownfield LNG trains. Australia’s key advantages versus LNG projects elsewhere are the low offshore upstream operating costs, cheap shipping costs to Asia, an investor friendly environment and having a huge installed base of LNG infrastructure and associated cashflows.

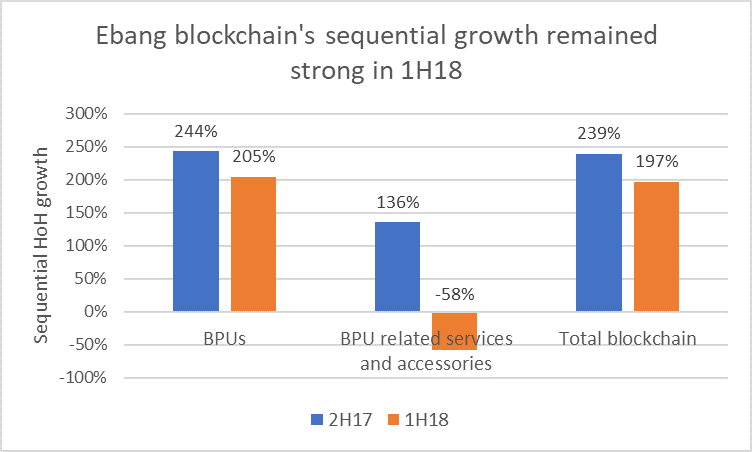

Ebang (EBANG HK) is a Chinese designer of bitcoin mining machines which are sold under the Ebit brand. Ebang refiled its draft prospectus with HKEX on 20 December 2018, but the IPO plans of cryptocurrency related companies are in a state of flux. Last week, the CEO of the Hong Kong Exchanges and Clearing, said that companies seeking to go public in Hong Kong should show consistency in their business models, in response to questions about the IPO applications of Bitmain Technologies Ltd (1374554D CH), Canaan Inc. (CANAAN HK) and Ebang.

While 1H18 results were strong, Ebang cautions that it experienced significant decreases in revenue and gross profit for 3Q18 compared to 2Q18. In the absence of any 3Q18 financial metrics, we scrutinised the financial accounts to find clues on the extent of the slowdown. Our analysis of the financial accounts’ leading indicators points to a rapid slowdown.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this week’s HK Connect Discovery, we highlight that CRRC’s outflow coincides with media reports that highlight the risks of China’s investment in high-speed railway. We also see a very substantial southbound flow into Car Inc.

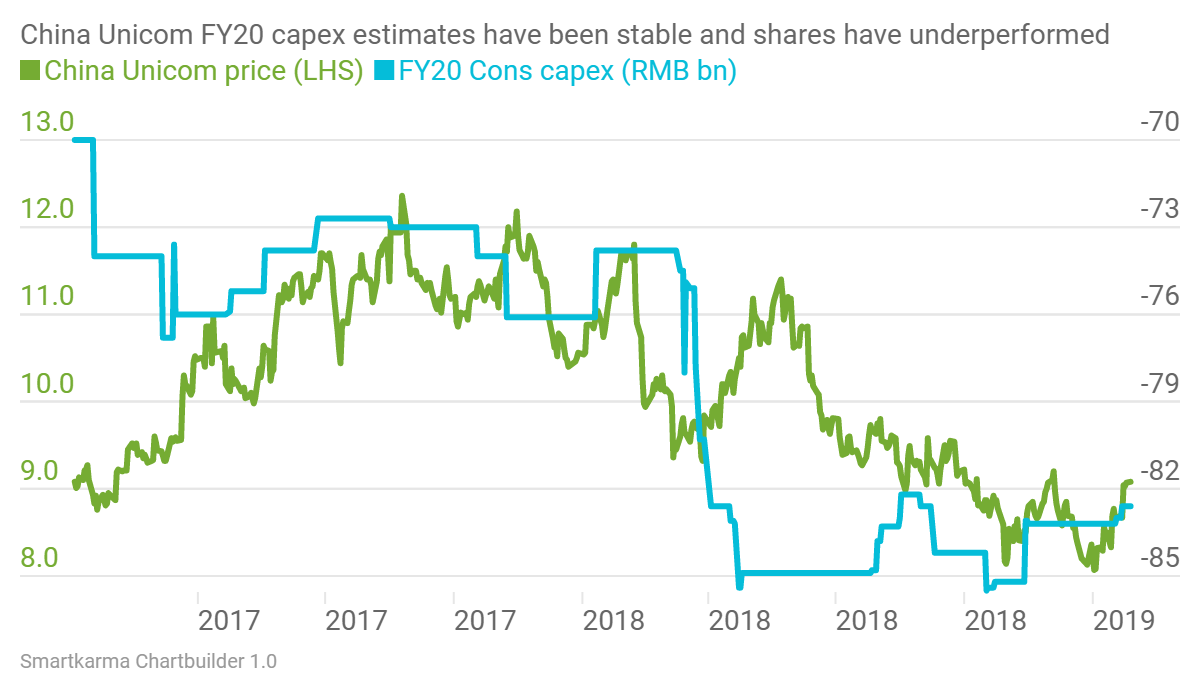

We have been positive on the Chinese telcos, in part due to our thesis that peak 5G capex expectations were too high for China Mobile. That has largely played out as capex expectations have come down and the stock has performed well. The telcos see a steady state approach to 5G capex as the best way forward given the lack of a current business case. However, there are larger forces at work which imply higher capex – the need to support Huawei/ZTE (763 HK) given the moves against Chinese equipment manufacturers internationally, and the likelihood of economic stimulus packages.

We have increased our 2020 capex expectations for Chinese Telcos. China Mobile most affected (RMB bn)

Source: New Street Research

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Trawling through >1500 global banks, based on the last quarter of reported Balance Sheets, we apply the discipline of the PH Score™ , a value-quality fundamental momentum screen, plus a low RSI screen, and a low Franchise Valuation (FV) screen to deliver our latest rankings for global banks.

While not all of top decile 1 scores are a buy – some are value traps while others maybe somewhat small and obscure and traded sparsely- the bottom decile names should awaken caution. We would be hard pressed to recommend some of the more popular and fashionable names from the bottom decile. Names such as ICICI Bank Ltd (ICICIBC IN) , Credicorp of Peru, Bank Central Asia (BBCA IJ) and Itau Unibanco Holding Sa (ITUB US) are EM favourites. Their share prices have performed well for an extended period and thus carry valuation risk. They represent pricey quality in some cases. They are not priced for disappointment but rather for hope. Are the constituents of the bottom decile not fertile grounds for short sellers?

Why pay top dollar for a bank franchise given risks related to domestic (let alone global) politics and the economy? Some investors and analysts have expressed “inspiration” for developments in Brazil and Argentina. But Brazilian bonds are now trading as if the country is Investment Grade again. (This is relevant for banks especially). Guedes and co. may deliver on pension/social security reform. If so, prices will become even more inflated. But what happens if they don’t deliver on reform? Why pay top dollar for hope given the ramp up in prices already? Argentina is an even more fragile “hope narrative”. More of a “Hope take 2”. Similar to Brazil, bank Franchise Valuations are elevated. While the current account adjustment and easing inflation are to be expected, the political and social scene will be a challenge. LATAM seems to be “hot” again with investment bankers talking of resilience. But resilience is different from valuation. Banks from Chile, Peru, and Colombia feature in the bottom decile too. If an investor wants to be in these markets and desires bank exposure, surely it makes sense to look for the best value on offer. Grupo Aval Acciones y Valores (AVAL CB) may represent one such opportunity.

Our bottom decile rankings feature a great deal of banks from Indonesia. In a promising market such as Indonesia, given bank valuations, one needs to tread extremely carefully to not end up paying over the odds, to not pay for extrapolation. In addition, India is a susceptible jurisdiction for any bank operating there – no bank is “superhuman” and especially not at the prices on offer for the popular private sector “winners”. Saudi Arabia is another market that suddenly became popular last year. We are mindful of valuations and FX.

Does it not make more sense to look at opportunity in the top decile? While some of the names here will be too small or illiquid (mea culpa), there are genuine portfolio candidates. South Korea stands out in the rankings. Woori Bank (WF US) is top of the rankings after a share price plunge related to a stock overhang but this will pass. Hana Financial (086790 KS) , Industrial Bank of Korea (IBK LX) and DGB Financial Group (139130 KS) are portfolio candidates. Elsewhere, Russia and Vietnam rightly feature while Sri Lanka and Pakistan contribute some names despite very real political and macro risks. We would caution on some of the relatively small Chinese names but recommend the big 4 versus EM peers – they are not expensive. In fact some of the big 4 feature in decile 2 of our rankings. There are many Japanese banks here too. And many, like some Chinese lenders, are cheap for a reason. While the technical picture for Japanese banks is bearish, at some stage selective weeding out of opportunity within Japan’s banking sector may be rewarding. The megabanks are certainly not dear. Europe is another matter. Despite valuations, we are cautious on French lenders and on German consolidation narratives – did a merger of 2 weak banks ever deliver shareholder value? The inclusion of two Romanian banks in the top decile is somewhat of a headscratcher. These are perfectly investable opportunities but share prices have been poor of late.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Tracking Traffic/Chinese Express & Logistics is the hub for our research on China’s express parcels and logistics sectors. Tracking Traffic/Chinese Express & Logistics features analysis of monthly Chinese express and logistics data, notes from our conversations with industry players, and links to company and thematic notes.

This month’s issue covers the following topics:

December express parcel pricing fell by over 9% Y/Y. Average pricing per express parcel fell by 9.1% Y/Y, the worst decline since Q216 (excluding January/February figures distorted by the Lunar New Year holiday).

Express parcel revenue growth remained well below 20% last month. Weak pricing dragged sector revenue growth down to 17% in December, the 4th consecutive month of sub-20% growth.

Intra-city pricing (ie, local delivery) was strong in 2018. Relative to weak inter-city pricing (down 3.1% Y/Y in 2018), pricing for intra-city express shipments was firm, rising by 0.1% last year. In fact, average pricing for intra-city express shipments has risen in four of the last five years.

Underlying domestic transport demand remained firm in December. Although demand for inter-city express shipments appears to be moderating (from high levels), underlying transportation activity in December remained firm. The three modes of freight transport we track (rail, highway, air) in aggregate rose 6.6% Y/Y in December, even as the growth of air freight slowed.

We retain a negative view of China’s express industry’s fundamentals: demand growth is slowing and pricing for inter-city shipments appears to be falling faster than costs can be cut, leading to margin compression.

Galaxy Entertainment Group (27 HK) exhibits some valid chart support in the form of a key low at 61.8% retracement and physical price support at the 40 level. This low should stay in place for 2019.

Price and RSI wedge formations are building steam for an upside breakout. MACD bull divergence and the triangle breakout back in November will provide forward upside energy. MACD triangles are some of the most powerful chart set ups.

Currently at an attractive risk to reward support zone for an entry with a reasonably tight stop.

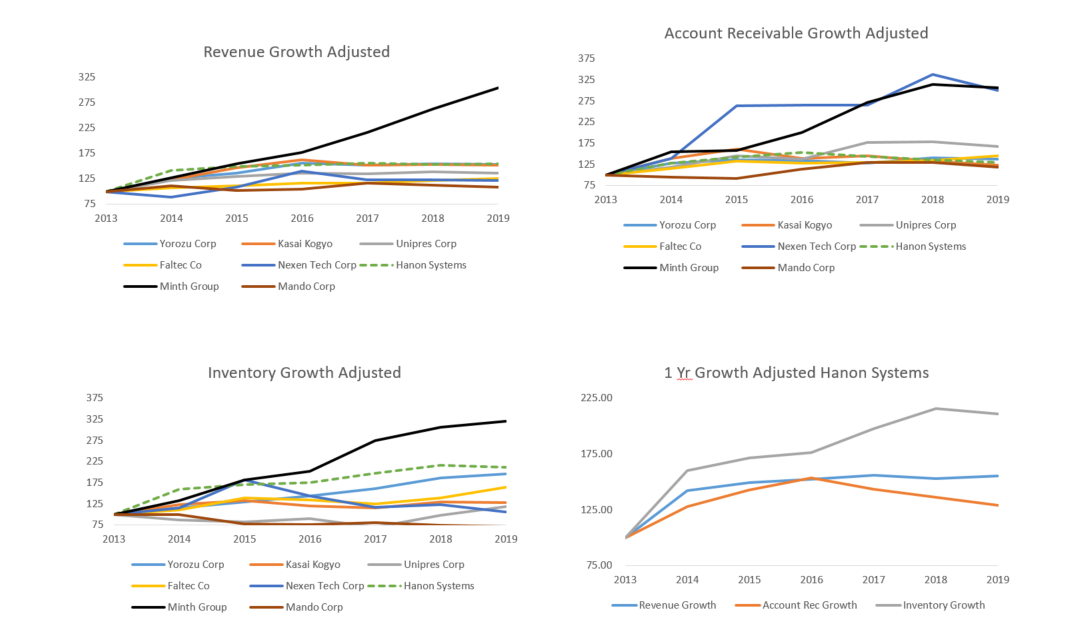

The recent negative sales in the Chinese auto industry and Nissan’s case of Carlos Ghosn removal could put additional pressure on the already thin margin of auto supplier industry. One of the Carlos Ghosn early contribution to Nissan was to cut cost and outsource the auto parts maker to a wide variety of suppliers including to Hanon Systems (018880 KS) . Nissan’s new management may want to undo some of Carlos Ghosn’ legacy including changing the selection criteria of parts supplier.

Hanon’s global peers also experienced a decrease in the inventory turnover and most of them have been priced at PER <10 but Hanon is still trading at 24x PER while its sales growth and profitability is still in low single digit? Facing the onset of the slowdown in the Chinese auto industry, won’t it be another headwind for Hanon Systems?

Trawling through >1500 global banks, based on the last quarter of reported Balance Sheets, we apply the discipline of the PH Score™ , a value-quality fundamental momentum screen, plus a low RSI screen, and a low Franchise Valuation (FV) screen to deliver our latest rankings for global banks.

While not all of top decile 1 scores are a buy – some are value traps while others maybe somewhat small and obscure and traded sparsely- the bottom decile names should awaken caution. We would be hard pressed to recommend some of the more popular and fashionable names from the bottom decile. Names such as ICICI Bank Ltd (ICICIBC IN) , Credicorp of Peru, Bank Central Asia (BBCA IJ) and Itau Unibanco Holding Sa (ITUB US) are EM favourites. Their share prices have performed well for an extended period and thus carry valuation risk. They represent pricey quality in some cases. They are not priced for disappointment but rather for hope. Are the constituents of the bottom decile not fertile grounds for short sellers?

Why pay top dollar for a bank franchise given risks related to domestic (let alone global) politics and the economy? Some investors and analysts have expressed “inspiration” for developments in Brazil and Argentina. But Brazilian bonds are now trading as if the country is Investment Grade again. (This is relevant for banks especially). Guedes and co. may deliver on pension/social security reform. If so, prices will become even more inflated. But what happens if they don’t deliver on reform? Why pay top dollar for hope given the ramp up in prices already? Argentina is an even more fragile “hope narrative”. More of a “Hope take 2”. Similar to Brazil, bank Franchise Valuations are elevated. While the current account adjustment and easing inflation are to be expected, the political and social scene will be a challenge. LATAM seems to be “hot” again with investment bankers talking of resilience. But resilience is different from valuation. Banks from Chile, Peru, and Colombia feature in the bottom decile too. If an investor wants to be in these markets and desires bank exposure, surely it makes sense to look for the best value on offer. Grupo Aval Acciones y Valores (AVAL CB) may represent one such opportunity.

Our bottom decile rankings feature a great deal of banks from Indonesia. In a promising market such as Indonesia, given bank valuations, one needs to tread extremely carefully to not end up paying over the odds, to not pay for extrapolation. In addition, India is a susceptible jurisdiction for any bank operating there – no bank is “superhuman” and especially not at the prices on offer for the popular private sector “winners”. Saudi Arabia is another market that suddenly became popular last year. We are mindful of valuations and FX.

Does it not make more sense to look at opportunity in the top decile? While some of the names here will be too small or illiquid (mea culpa), there are genuine portfolio candidates. South Korea stands out in the rankings. Woori Bank (WF US) is top of the rankings after a share price plunge related to a stock overhang but this will pass. Hana Financial (086790 KS) , Industrial Bank of Korea (IBK LX) and DGB Financial Group (139130 KS) are portfolio candidates. Elsewhere, Russia and Vietnam rightly feature while Sri Lanka and Pakistan contribute some names despite very real political and macro risks. We would caution on some of the relatively small Chinese names but recommend the big 4 versus EM peers – they are not expensive. In fact some of the big 4 feature in decile 2 of our rankings. There are many Japanese banks here too. And many, like some Chinese lenders, are cheap for a reason. While the technical picture for Japanese banks is bearish, at some stage selective weeding out of opportunity within Japan’s banking sector may be rewarding. The megabanks are certainly not dear. Europe is another matter. Despite valuations, we are cautious on French lenders and on German consolidation narratives – did a merger of 2 weak banks ever deliver shareholder value? The inclusion of two Romanian banks in the top decile is somewhat of a headscratcher. These are perfectly investable opportunities but share prices have been poor of late.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Ebang (EBANG HK) is a Chinese designer of bitcoin mining machines which are sold under the Ebit brand. Ebang refiled its draft prospectus with HKEX on 20 December 2018, but the IPO plans of cryptocurrency related companies are in a state of flux. Last week, the CEO of the Hong Kong Exchanges and Clearing, said that companies seeking to go public in Hong Kong should show consistency in their business models, in response to questions about the IPO applications of Bitmain Technologies Ltd (1374554D CH), Canaan Inc. (CANAAN HK) and Ebang.

While 1H18 results were strong, Ebang cautions that it experienced significant decreases in revenue and gross profit for 3Q18 compared to 2Q18. In the absence of any 3Q18 financial metrics, we scrutinised the financial accounts to find clues on the extent of the slowdown. Our analysis of the financial accounts’ leading indicators points to a rapid slowdown.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this week’s HK Connect Discovery, we highlight that CRRC’s outflow coincides with media reports that highlight the risks of China’s investment in high-speed railway. We also see a very substantial southbound flow into Car Inc.

We have been positive on the Chinese telcos, in part due to our thesis that peak 5G capex expectations were too high for China Mobile. That has largely played out as capex expectations have come down and the stock has performed well. The telcos see a steady state approach to 5G capex as the best way forward given the lack of a current business case. However, there are larger forces at work which imply higher capex – the need to support Huawei/ZTE (763 HK) given the moves against Chinese equipment manufacturers internationally, and the likelihood of economic stimulus packages.

Tracking Traffic/Containers & Air Cargo is the hub for all of our research on container shipping and air cargo, featuring analysis of monthly industry data, notes from our conversations with industry participants, and links to recent company and thematic pieces.

Tracking Traffic/Containers & Air Cargo aims to highlight changes to existing trends, relationships, and views affecting the leading Asian companies in these two sectors. This month’s note includes data from about twenty different sources.

In this issue readers will find:

An analysis of December container shipping rates: Our proprietary index suggests average container shipping rates firmed again in December. Firmer rates in Q418, combined with a moderation in fuel prices, probably lifted carrier margins in the period, and this improvement is likely to spill over into Q119.

A look at December air cargo activity, which slumped, again: The five Asia-based airlines we track reported a ~2% Y/Y decline in air cargo handled. After growing by a healthy +6.3% Y/Y in H118, air cargo demand at these five carriers has shown a consistent monthly decline, growing by just 1% in Q418 and shrinking slightly in November and December.

For container carriers and airlines, fuel price increases have continued to moderate. As of mid-January, the price of bunker fuel was up just 4% Y/Y, and the price of jet fuel had declined by around 7%. Throughout much of 2018, fuel prices had risen 20-40% Y/Y, or more.

Japanese carriers’ December quarter earnings on the horizon: We will soon find out whether improving conditions in container shipping showed up in the carriers’ P&Ls, as the three major Japanese shipping companies are set to report December quarter results at the break on January 31.

Although slowing demand growth is unlikely to generate impressive top-line improvements, firmer pricing combined with lower fuel costs should support an ongoing improvement in profitability for container carriers in the near-term. Meanwhile, the slump in air cargo demand has not yet hit air cargo yields, but it’s becoming clearer that an economic slowdown is hurting demand for this relatively expensive mode of transport.

We run through our views on the main themes that will impact the oil and gas market in 2019 and the stocks to play these through. We outline the 10 key themes including oil demand, US oil supply growth, OPEC+ policy, base production decline rates, exploration potential and the outlook for new project final investment decisions. We also look at the refining market, LNG supply and demand, the M&A prospects and the impact of the energy transition. We outline 12 stocks (7 bullish and 5 bearish calls) that we think you can play the themes through.

We examine some of the key drivers of the oil price and on the whole we are relatively bullish as although we see some risk to demand growth forecasts in 2019, in the absence of a recession we think that supply has more room to surprise to the downside. Geopolitics and financial markets will play a huge role in prices. We think that US oil supply growth will be lower y/y in 2019, OPEC+ compliance with cuts will be high and maybe helped by unplanned disruptions and base production will decline more rapidly than forecast. Companies will accelerate the sanctioning of new projects in 2019 and also will increase exploration spending, despite a number of years of poor success rates – overall the trend should be positive for the offshore oil service companies. We expect strong LNG supply growth in 2019 to hit spot pricing but still expect a large number of projects to be sanctioned helping the LNG engineering and construction companies. It will be a very interesting year for the refining industry as new regulations limiting shipping sulphur emissions should lead to a spike in diesel and to some extent gasoline margins towards the end of the year, helping complex refiners. Major oil companies will continue to embrace renewables as investors continue to push for companies to plan for the energy transition.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

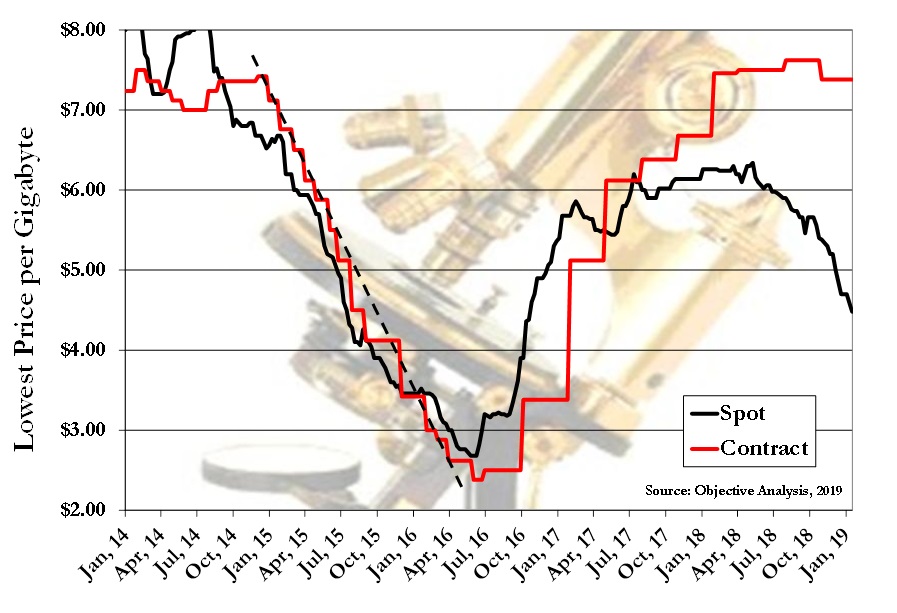

A very normal part of the semiconductor cycle is inventory clearance. DRAM makers are starting to discuss this in their earnings calls. What they are NOT telling their investors is how significant this is to the onset of a price collapse, perhaps because they don’t understand it themselves. This Insight will help readers to learn how and why an inventory clearance helps ratchet a budding oversupply into a full-blown glut.

The globe is facing more than an ordinary business cycle.

Joseph C. Sternberg, editorial-page editor and European political-economy columnist for the Wall Street Journal’s European edition, recently interviewed Claudio Borio, head of the Monetaryand Economic Department of the BIS. Mr. Borio said that politicians have relied far too much on central banks, which are constrained by economic theories that offer little meaningful guidance on how to sustain growth and financial stability. The only tool they have is an interest rate that can affect output in the short run but ends up affecting only inflation in the end.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainland investors in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: component stocks in the HSCEI index, stocks with a market capitalization between USD 1 billion and USD 5 billion, and stocks with a market capitalization between USD 500 million and USD 1 billion.

In this week’s HK Connect Discovery, we highlight that Tencent topped the weekly inflow by quantum and its shares held by mainland investors via Stock Connect is at one year low. Stocks exposed to mobile game sector experienced inflow too. In addition, we continue to observe that the mainland investors holding on Yichang HEC continue to rise.

Tracking Traffic/Chinese Express & Logistics is the hub for our research on China’s express parcels and logistics sectors. Tracking Traffic/Chinese Express & Logistics features analysis of monthly Chinese express and logistics data, notes from our conversations with industry players, and links to company and thematic notes.

This month’s issue covers the following topics:

December express parcel pricing fell by over 9% Y/Y. Average pricing per express parcel fell by 9.1% Y/Y, the worst decline since Q216 (excluding January/February figures distorted by the Lunar New Year holiday).

Express parcel revenue growth remained well below 20% last month. Weak pricing dragged sector revenue growth down to 17% in December, the 4th consecutive month of sub-20% growth.

Intra-city pricing (ie, local delivery) was strong in 2018. Relative to weak inter-city pricing (down 3.1% Y/Y in 2018), pricing for intra-city express shipments was firm, rising by 0.1% last year. In fact, average pricing for intra-city express shipments has risen in four of the last five years.

Underlying domestic transport demand remained firm in December. Although demand for inter-city express shipments appears to be moderating (from high levels), underlying transportation activity in December remained firm. The three modes of freight transport we track (rail, highway, air) in aggregate rose 6.6% Y/Y in December, even as the growth of air freight slowed.

We retain a negative view of China’s express industry’s fundamentals: demand growth is slowing and pricing for inter-city shipments appears to be falling faster than costs can be cut, leading to margin compression.

Galaxy Entertainment Group (27 HK) exhibits some valid chart support in the form of a key low at 61.8% retracement and physical price support at the 40 level. This low should stay in place for 2019.

Price and RSI wedge formations are building steam for an upside breakout. MACD bull divergence and the triangle breakout back in November will provide forward upside energy. MACD triangles are some of the most powerful chart set ups.

Currently at an attractive risk to reward support zone for an entry with a reasonably tight stop.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

The recent negative sales in the Chinese auto industry and Nissan’s case of Carlos Ghosn removal could put additional pressure on the already thin margin of auto supplier industry. One of the Carlos Ghosn early contribution to Nissan was to cut cost and outsource the auto parts maker to a wide variety of suppliers including to Hanon Systems (018880 KS) . Nissan’s new management may want to undo some of Carlos Ghosn’ legacy including changing the selection criteria of parts supplier.

Hanon’s global peers also experienced a decrease in the inventory turnover and most of them have been priced at PER <10 but Hanon is still trading at 24x PER while its sales growth and profitability is still in low single digit? Facing the onset of the slowdown in the Chinese auto industry, won’t it be another headwind for Hanon Systems?

Trawling through >1500 global banks, based on the last quarter of reported Balance Sheets, we apply the discipline of the PH Score™ , a value-quality fundamental momentum screen, plus a low RSI screen, and a low Franchise Valuation (FV) screen to deliver our latest rankings for global banks.

While not all of top decile 1 scores are a buy – some are value traps while others maybe somewhat small and obscure and traded sparsely- the bottom decile names should awaken caution. We would be hard pressed to recommend some of the more popular and fashionable names from the bottom decile. Names such as ICICI Bank Ltd (ICICIBC IN) , Credicorp of Peru, Bank Central Asia (BBCA IJ) and Itau Unibanco Holding Sa (ITUB US) are EM favourites. Their share prices have performed well for an extended period and thus carry valuation risk. They represent pricey quality in some cases. They are not priced for disappointment but rather for hope. Are the constituents of the bottom decile not fertile grounds for short sellers?

Why pay top dollar for a bank franchise given risks related to domestic (let alone global) politics and the economy? Some investors and analysts have expressed “inspiration” for developments in Brazil and Argentina. But Brazilian bonds are now trading as if the country is Investment Grade again. (This is relevant for banks especially). Guedes and co. may deliver on pension/social security reform. If so, prices will become even more inflated. But what happens if they don’t deliver on reform? Why pay top dollar for hope given the ramp up in prices already? Argentina is an even more fragile “hope narrative”. More of a “Hope take 2”. Similar to Brazil, bank Franchise Valuations are elevated. While the current account adjustment and easing inflation are to be expected, the political and social scene will be a challenge. LATAM seems to be “hot” again with investment bankers talking of resilience. But resilience is different from valuation. Banks from Chile, Peru, and Colombia feature in the bottom decile too. If an investor wants to be in these markets and desires bank exposure, surely it makes sense to look for the best value on offer. Grupo Aval Acciones y Valores (AVAL CB) may represent one such opportunity.

Our bottom decile rankings feature a great deal of banks from Indonesia. In a promising market such as Indonesia, given bank valuations, one needs to tread extremely carefully to not end up paying over the odds, to not pay for extrapolation. In addition, India is a susceptible jurisdiction for any bank operating there – no bank is “superhuman” and especially not at the prices on offer for the popular private sector “winners”. Saudi Arabia is another market that suddenly became popular last year. We are mindful of valuations and FX.

Does it not make more sense to look at opportunity in the top decile? While some of the names here will be too small or illiquid (mea culpa), there are genuine portfolio candidates. South Korea stands out in the rankings. Woori Bank (WF US) is top of the rankings after a share price plunge related to a stock overhang but this will pass. Hana Financial (086790 KS) , Industrial Bank of Korea (IBK LX) and DGB Financial Group (139130 KS) are portfolio candidates. Elsewhere, Russia and Vietnam rightly feature while Sri Lanka and Pakistan contribute some names despite very real political and macro risks. We would caution on some of the relatively small Chinese names but recommend the big 4 versus EM peers – they are not expensive. In fact some of the big 4 feature in decile 2 of our rankings. There are many Japanese banks here too. And many, like some Chinese lenders, are cheap for a reason. While the technical picture for Japanese banks is bearish, at some stage selective weeding out of opportunity within Japan’s banking sector may be rewarding. The megabanks are certainly not dear. Europe is another matter. Despite valuations, we are cautious on French lenders and on German consolidation narratives – did a merger of 2 weak banks ever deliver shareholder value? The inclusion of two Romanian banks in the top decile is somewhat of a headscratcher. These are perfectly investable opportunities but share prices have been poor of late.

Uzbekistan’s economy is a frontier market stand out and has a large number of attractive characteristics:

Uzbekistan’s stock market trades at a substantial discount to other frontier markets, though the extremely illiquid nature of the market makes it hard to trade. However, there still is foreign interest in the market.

The IMF projects that the economy will grow by 5% during 2018 and 2019, and eventually reach 6% by 2022, though this is still below its historical high.

Market reforms were spearheaded in December 2016 when the newly elected president, Shavkat Mirziyoyev decided to transition towards a market- oriented economy led by private sector growth, as the public sector was unable to create enough jobs. This represents a significant shift given that Uzbekistan had been a closed, centrally planned economy until 2016.

Tourist arrivals grew by 91.6% during H1 2018, and this is poised to improve greater in the future due to the impact of the visa liberalization measures.

Twin deficits have remained under control and Uzbekistan is one of few current account surplus frontier markets.

Uzbekistan is also very attractive compared to other markets in the frontier space given that its minimum wage is only US$24/month, compared to around $70-75/month in Kyrgyzstan and Kazakhstan.

The market reforms that the country recently implemented will be a major catalyst for future economic growth and makes investment in this market appealing. Apart from strong growth, the market is also appealing due to its high foreign exchange reserves ( nearly 2 years of import cover), consistent CA surplus, and stable currency. My latest frontier and emerging market recap highlights the appeals of markets such as Bangladesh, Vietnam, and Egypt, while expressing concerns for markets such as Sri Lanka and Pakistan. Uzbekistan is a suitable addition given its stable macro/political picture, and the main negative factor of this market is the highly inaccessible nature of the equity market. The ADTV is less than $100,000, which is a far cry from other frontier markets like Romania, Sri Lanka and Kenya.

Highlights of significant recent happenings include:

Substantive Deep Dive – Canada’s BlackBerry Ltd (BB CN) seeks to be the go-to provider of web Security: Why we believe investors should look at Blackberry as a way to hedge their exposures to the increasing list of companies who are susceptible to adverse impact from security breaches.

Feeding the Dragon – Chinese buying of US firms brakes abruptly, obliterating the long-term trend, and now Japan has become the second-largest market for outbound M&A globally. Also, South Korean food giant Cj Cheiljedang (097950 KS) is continuing its aggressive expansion into the U.S. market

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

On the back of a growing LNG global trade volume, LNG producers have outperformed the US market and their E&P peers including the oil majors over the last two years. As global LNG production reaches a record 316m tonnes in 2018, a 9.6% increase year on year, new capacity additions set to come online in the next three years will be dominated by the US. This insight will examine how the recent entry of US LNG in the market is transforming the LNG industry and which emerging players are driving the change.

Exhibit 1: LNG Producers Outperform the US Market

Source: Capital IQ. Prices as of 22 of January. Un-weighted indexed composites. Oil Majors: Exxon, Chevron, Shell, BP, Total and ENI. Australia LNG: Woodside Energy, Santos, Oil Search. independent E&Ps: oil and gas upstream companies with market value greater than $300m as of 18 April 2018.

My colleagues strive to cover M&A transactions in Asia-Pac – and further afield – with a market cap >US$100mn and/or when liquidity or the backdrop story warrant comment. This insight is no exception.

In the past two weeks, two companies who form part of the Huarong-CMB network (HCN), as discussed by David Webb, and one company enmeshed in the Enigma network, have received official offers or are have made announcements pursuant to the Hong Kong Code on Takeovers and Mergers.

Below are brief comments on all three situations. In the case of New Sports, it is a very real deal, with financing in place for the cash option.

It is arguable whether the tanking in CSST shares yesterday after the resumption of trading, increases or lessens the chances of an official Offer unfolding.

LVS shot at Japan license enhanced by his role in lobbying US Justice Department’s reverse opinion on online gambling published last week. Read why in this insight.

Owning Sands China makes a strong case based on an ROCE analysis vs. the hospitality sector.

Owning both at current trade is one of the screaming bargains in the entire sector

Maoyan Entertainment (EPLUS HK) is the largest online movie ticketing service provider in China. The mid-point of Maoyan’s IPO price range of HK$14.8-20.4 per share implies a market value of $2.5 billion (HK$19.8 billion). Five cornerstone investors have agreed to buy $30 million or 10% of the offering at the IPO mid-point. The cornerstone investors are Imax China Holding (1970 HK), Hylink Digital Solutions, Prestige of The Sun, Welight Capital and Xiaomi Corp (1810 HK).

Our analysis suggests Maoyan is being offered at a material premium to a peer group of major Chinese internet companies. Due to challenging prospects faced by Maoyan as outlined in our previous research, we believe a premium rating is unwarranted. Consequently, we are inclined to sit out this IPO.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We have been positive on the Chinese telcos, in part due to our thesis that peak 5G capex expectations were too high for China Mobile. That has largely played out as capex expectations have come down and the stock has performed well. The telcos see a steady state approach to 5G capex as the best way forward given the lack of a current business case. However, there are larger forces at work which imply higher capex – the need to support Huawei/ZTE (763 HK) given the moves against Chinese equipment manufacturers internationally, and the likelihood of economic stimulus packages.

Tracking Traffic/Containers & Air Cargo is the hub for all of our research on container shipping and air cargo, featuring analysis of monthly industry data, notes from our conversations with industry participants, and links to recent company and thematic pieces.

Tracking Traffic/Containers & Air Cargo aims to highlight changes to existing trends, relationships, and views affecting the leading Asian companies in these two sectors. This month’s note includes data from about twenty different sources.

In this issue readers will find:

An analysis of December container shipping rates: Our proprietary index suggests average container shipping rates firmed again in December. Firmer rates in Q418, combined with a moderation in fuel prices, probably lifted carrier margins in the period, and this improvement is likely to spill over into Q119.

A look at December air cargo activity, which slumped, again: The five Asia-based airlines we track reported a ~2% Y/Y decline in air cargo handled. After growing by a healthy +6.3% Y/Y in H118, air cargo demand at these five carriers has shown a consistent monthly decline, growing by just 1% in Q418 and shrinking slightly in November and December.

For container carriers and airlines, fuel price increases have continued to moderate. As of mid-January, the price of bunker fuel was up just 4% Y/Y, and the price of jet fuel had declined by around 7%. Throughout much of 2018, fuel prices had risen 20-40% Y/Y, or more.

Japanese carriers’ December quarter earnings on the horizon: We will soon find out whether improving conditions in container shipping showed up in the carriers’ P&Ls, as the three major Japanese shipping companies are set to report December quarter results at the break on January 31.

Although slowing demand growth is unlikely to generate impressive top-line improvements, firmer pricing combined with lower fuel costs should support an ongoing improvement in profitability for container carriers in the near-term. Meanwhile, the slump in air cargo demand has not yet hit air cargo yields, but it’s becoming clearer that an economic slowdown is hurting demand for this relatively expensive mode of transport.

We run through our views on the main themes that will impact the oil and gas market in 2019 and the stocks to play these through. We outline the 10 key themes including oil demand, US oil supply growth, OPEC+ policy, base production decline rates, exploration potential and the outlook for new project final investment decisions. We also look at the refining market, LNG supply and demand, the M&A prospects and the impact of the energy transition. We outline 12 stocks (7 bullish and 5 bearish calls) that we think you can play the themes through.

We examine some of the key drivers of the oil price and on the whole we are relatively bullish as although we see some risk to demand growth forecasts in 2019, in the absence of a recession we think that supply has more room to surprise to the downside. Geopolitics and financial markets will play a huge role in prices. We think that US oil supply growth will be lower y/y in 2019, OPEC+ compliance with cuts will be high and maybe helped by unplanned disruptions and base production will decline more rapidly than forecast. Companies will accelerate the sanctioning of new projects in 2019 and also will increase exploration spending, despite a number of years of poor success rates – overall the trend should be positive for the offshore oil service companies. We expect strong LNG supply growth in 2019 to hit spot pricing but still expect a large number of projects to be sanctioned helping the LNG engineering and construction companies. It will be a very interesting year for the refining industry as new regulations limiting shipping sulphur emissions should lead to a spike in diesel and to some extent gasoline margins towards the end of the year, helping complex refiners. Major oil companies will continue to embrace renewables as investors continue to push for companies to plan for the energy transition.

In our base case, we do not expect the trade war between the US and China to end soon. The next bilateral meeting between Liu He and US Trade Representative Robert Lighthizer is scheduled at the end of this month. If the Chinese side is hoping to placate the US with promises to purchase US commodities, this is unlikely to be sufficient to achieve a lasting improvement in the relationship. We are sceptical that the Chinese leadership will agree to launch structural reforms under pressure from the US.

Elsewhere, we are concerned with growing geopolitical and security risks in Nigeria where both presidential and parliamentary elections are scheduled in February. The relations between Turkey and the US have also soured ahead of the Turkish local elections. In Poland, the assassination of the Gdansk mayor put the polarisation of the society into the spotlight ahead of the parliamentary elections due this autumn. There are signs that the US is about to ramp up pressure on Russia after newly elected Democratic House members filled their seats earlier this month.

On January 24’th 2019, SEMI announced that Wafer Fab Equipment (WFE) billings for North America-based manufacturers of semiconductor equipment amounted to $2.11 billion worldwide in December 2018. This represents an 8.5% MoM increase, although still lower YoY by 12.1%. December’s data marks the reversal of a six month long downtrend in monthly billings, a bullish signal that the WFE segment has bottomed and better times lie ahead.

This latest billings data coincides with WFE bellwether Lam Research (LRCX US)‘s latest earnings report which slightly exceeded guidance with revenues of $2.5 billion, up 8.7% sequentially. On the call, company executives stated that first quarter CY 2019 would mark the trough from a gross margin perspective, strongly implying that it would be the same for revenues.

LRCX shares surged 15.7% in overnight trading triggering a rising tide that lifted large swathes of semiconductor stocks, particularly those within the WFE sector. Two swallows don’t necessarily mean it’s Spring, but for now, the markets are betting that it does.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Trawling through >1500 global banks, based on the last quarter of reported Balance Sheets, we apply the discipline of the PH Score™ , a value-quality fundamental momentum screen, plus a low RSI screen, and a low Franchise Valuation (FV) screen to deliver our latest rankings for global banks.

While not all of top decile 1 scores are a buy – some are value traps while others maybe somewhat small and obscure and traded sparsely- the bottom decile names should awaken caution. We would be hard pressed to recommend some of the more popular and fashionable names from the bottom decile. Names such as ICICI Bank Ltd (ICICIBC IN) , Credicorp of Peru, Bank Central Asia (BBCA IJ) and Itau Unibanco Holding Sa (ITUB US) are EM favourites. Their share prices have performed well for an extended period and thus carry valuation risk. They represent pricey quality in some cases. They are not priced for disappointment but rather for hope. Are the constituents of the bottom decile not fertile grounds for short sellers?

Why pay top dollar for a bank franchise given risks related to domestic (let alone global) politics and the economy? Some investors and analysts have expressed “inspiration” for developments in Brazil and Argentina. But Brazilian bonds are now trading as if the country is Investment Grade again. (This is relevant for banks especially). Guedes and co. may deliver on pension/social security reform. If so, prices will become even more inflated. But what happens if they don’t deliver on reform? Why pay top dollar for hope given the ramp up in prices already? Argentina is an even more fragile “hope narrative”. More of a “Hope take 2”. Similar to Brazil, bank Franchise Valuations are elevated. While the current account adjustment and easing inflation are to be expected, the political and social scene will be a challenge. LATAM seems to be “hot” again with investment bankers talking of resilience. But resilience is different from valuation. Banks from Chile, Peru, and Colombia feature in the bottom decile too. If an investor wants to be in these markets and desires bank exposure, surely it makes sense to look for the best value on offer. Grupo Aval Acciones y Valores (AVAL CB) may represent one such opportunity.

Our bottom decile rankings feature a great deal of banks from Indonesia. In a promising market such as Indonesia, given bank valuations, one needs to tread extremely carefully to not end up paying over the odds, to not pay for extrapolation. In addition, India is a susceptible jurisdiction for any bank operating there – no bank is “superhuman” and especially not at the prices on offer for the popular private sector “winners”. Saudi Arabia is another market that suddenly became popular last year. We are mindful of valuations and FX.

Does it not make more sense to look at opportunity in the top decile? While some of the names here will be too small or illiquid (mea culpa), there are genuine portfolio candidates. South Korea stands out in the rankings. Woori Bank (WF US) is top of the rankings after a share price plunge related to a stock overhang but this will pass. Hana Financial (086790 KS) , Industrial Bank of Korea (IBK LX) and DGB Financial Group (139130 KS) are portfolio candidates. Elsewhere, Russia and Vietnam rightly feature while Sri Lanka and Pakistan contribute some names despite very real political and macro risks. We would caution on some of the relatively small Chinese names but recommend the big 4 versus EM peers – they are not expensive. In fact some of the big 4 feature in decile 2 of our rankings. There are many Japanese banks here too. And many, like some Chinese lenders, are cheap for a reason. While the technical picture for Japanese banks is bearish, at some stage selective weeding out of opportunity within Japan’s banking sector may be rewarding. The megabanks are certainly not dear. Europe is another matter. Despite valuations, we are cautious on French lenders and on German consolidation narratives – did a merger of 2 weak banks ever deliver shareholder value? The inclusion of two Romanian banks in the top decile is somewhat of a headscratcher. These are perfectly investable opportunities but share prices have been poor of late.

Uzbekistan’s economy is a frontier market stand out and has a large number of attractive characteristics:

Uzbekistan’s stock market trades at a substantial discount to other frontier markets, though the extremely illiquid nature of the market makes it hard to trade. However, there still is foreign interest in the market.

The IMF projects that the economy will grow by 5% during 2018 and 2019, and eventually reach 6% by 2022, though this is still below its historical high.

Market reforms were spearheaded in December 2016 when the newly elected president, Shavkat Mirziyoyev decided to transition towards a market- oriented economy led by private sector growth, as the public sector was unable to create enough jobs. This represents a significant shift given that Uzbekistan had been a closed, centrally planned economy until 2016.

Tourist arrivals grew by 91.6% during H1 2018, and this is poised to improve greater in the future due to the impact of the visa liberalization measures.

Twin deficits have remained under control and Uzbekistan is one of few current account surplus frontier markets.

Uzbekistan is also very attractive compared to other markets in the frontier space given that its minimum wage is only US$24/month, compared to around $70-75/month in Kyrgyzstan and Kazakhstan.

The market reforms that the country recently implemented will be a major catalyst for future economic growth and makes investment in this market appealing. Apart from strong growth, the market is also appealing due to its high foreign exchange reserves ( nearly 2 years of import cover), consistent CA surplus, and stable currency. My latest frontier and emerging market recap highlights the appeals of markets such as Bangladesh, Vietnam, and Egypt, while expressing concerns for markets such as Sri Lanka and Pakistan. Uzbekistan is a suitable addition given its stable macro/political picture, and the main negative factor of this market is the highly inaccessible nature of the equity market. The ADTV is less than $100,000, which is a far cry from other frontier markets like Romania, Sri Lanka and Kenya.

Highlights of significant recent happenings include:

Substantive Deep Dive – Canada’s BlackBerry Ltd (BB CN) seeks to be the go-to provider of web Security: Why we believe investors should look at Blackberry as a way to hedge their exposures to the increasing list of companies who are susceptible to adverse impact from security breaches.

Feeding the Dragon – Chinese buying of US firms brakes abruptly, obliterating the long-term trend, and now Japan has become the second-largest market for outbound M&A globally. Also, South Korean food giant Cj Cheiljedang (097950 KS) is continuing its aggressive expansion into the U.S. market

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.