This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

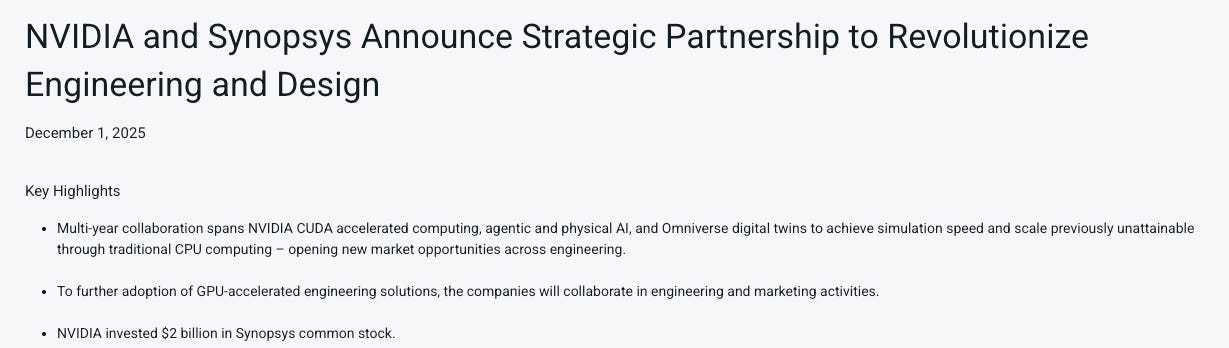

1. NVIDIA Invests $2 Billion In Synopsys. But Why?

- NVIDIA & Synopsys announced a new strategic partnership on Dec 1, mostly covering topics they were already strategically partnering on, with one exception, Cloud-Ready Solutions

- The partnership sees NVIDIA purchase $2 billion worth of Synopsys stock in a private placement. Other, recent, similar strategic partnerships e.g. Siemens & GM, involved no such investment

- They plan to start enabling cloud access for GPU-accelerated engineering solutions. Could this be where that $2 billion finds a home? Is this a new Neocloud in disguise? Let’s see

2. Intel (INTC.US): Apple M-Series in 2027; Intel 18A Is the Key.

- Apple (AAPL US) may outsource iPad CPU production to Intel in 2027.

- U.S. semiconductor reshoring faces fundamental structural barriers, and Trump is trying to blame this by pushing TSMC to move advanced manufacturing technology to the U.S.

- The key variable remains Intel’s 18A execution. However, Intel’s current CEO, Lip-Bu Tan, has not demonstrated an aggressive stance so far.

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. NVIDIA. Burry’s Claims Miss The Forest For The Trees. The Real Issues Are Structural, Not Legal

- After taking short positions against Palantir & NVIDIA, Michael Burry has closed his hedge fund and taken to substack to continue his assault on the AI bubble

- While he makes some valid points, these are mainly things everybody already knows and in the end he’s missing the forest for the trees

- There are key structural issues surrounding the AI Infrastructure build out (grid, foundry, memory capacity to mention a few). These will drive course corrections, all by themselves.

2. TSMC (2330.TT; TSM.US): Retired Sr. VP Joins Intel; U.S. Fab Impact; Arizona Earnings Decline.

- TSMC (Taiwan Semiconductor Manufacturing) – ADR (TSM US)’s retired Senior Vice President Dr. Wei-Jen Lo has taken a position at Intel.

- Trump has been in power for less than a year, and the U.S.’s measures have fully revealed its purpose of confrontation between China and the United States.

- TSMC’s Arizona fab profit dropped from NT$4.32 billion in 2Q25 to NT$410 million in 3Q25.

3. Did The Elon & Jensen Clown Show Just Crater The AI Narrative?

- Maybe it’s 10, 20 years something like that. For me that’s long term. Um my prediction is that work will be optional.

- The evidence speaks for itself uh but but but AI and humanoid robots will actually eliminate poverty and Tesla won’t be the only one that makes them.

- There will still be constraints on power like electricity. The fundamental physics elements will still be constraints. Um but um I think at some point uh currency becomes irrelevant.

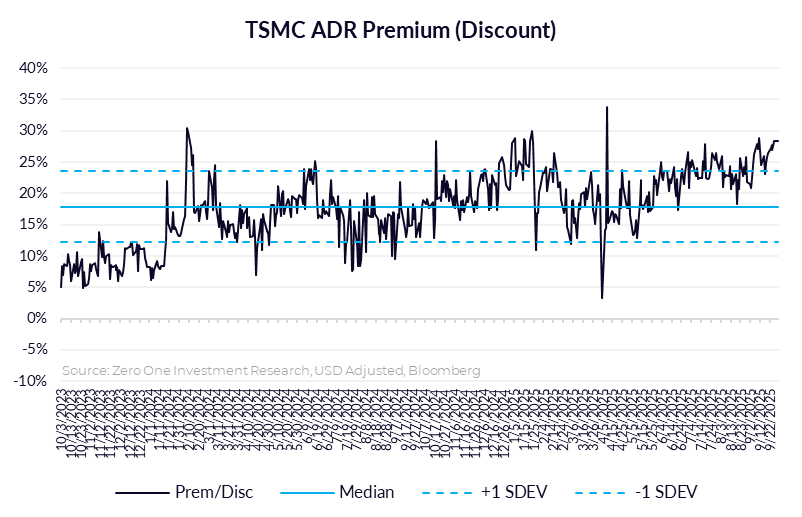

4. Taiwan Dual-Listings Monitor: TSMC Spread Back in Extreme Range, UMC Discount

- TSMC: +25.8% Premium; Rebounded to High End of Range, Good Level to Open a Short of the ADR Spread

- UMC: -2.2% Discount; Good Level to Open a Short of the ADR Spread

- ASE: +3.2% Premium; Wait for More Extreme Level Before Going Long or Short

5. PC Monitor: Dell/HP Results Support PC Up-Cycle Into 2026E

- AI PCs turning the PC refresh into a gradual, extended up-cycle

- Memory inflation is one of the major margin risks for PC makers in 2026

- Dell’s server business indicates AI factory build-outs becoming a multi-year investment cycle. Remain long Dell, Asustek, Acer.

6. Taiwan Tech Weekly: Rapidus Making Progress… TSMC Impact; Latest PC Results Support 2026E Up-Cycle

- Japan’s Rapidus Moves Ahead With 1.4nm Plans… TSMC Impact? — Latest and Past Analysis

- PC Monitor: Latest Dell/HP Results Support PC Up-Cycle Into 2026E

- TechChain Insights: Factory Visit with One of Taiwan’s Critical Battery Suppliers

7. TechChain Insights: Visit with Taiwan’s Critical Battery Supplier

- Factory visit to GUS Technology reveals Taiwan’s strategic position as a non-China battery supplier for defense and critical infrastructure applications.

- Proprietary pouch cell technology with patents in Taiwan and Japan addresses weight-sensitive applications including drones, underwater vehicles, and data center UPS systems.

- Dual product strategy (safety-focused Mettle Series and energy-dense Hyper Series) targets both commercial reliability and mission-critical performance markets.

8. Taiwan Dual-Listings Monitor: TSMC ADR Spread Deeper in Historically Rare Zone

- TSMC: +27.1% Premium; Increased to More Historically Extreme Level; Deeper in Short Range

- UMC: +2.3% Premium; Good Level to Open a Short of The Spread

- ASE: +2.3% Premium; Wait Better Long Opportunity Near Parity or Below

9. TSMC (2330.TT; TSM.US): Rapidus Plans to Build a Second Fab to Begin 1.4nm Volume Production in 2029

- Rapidus is currently moving in parallel with TSMC (Taiwan Semiconductor Manufacturing) – ADR (TSM US) in targeting the 2nm, and is regarded as Japan’s core force in the advanced-process arena.

- Rapidus plans to build a second fab in Hokkaido in FY2027. The facility is scheduled to begin 1.4nm volume production in 2029 to accelerate the catch-up with global leader TSMC.

- During its mid-October earnings briefing, TSMC stated that 2nm will enter volume production as scheduled in 4Q this year, and that it will begin 1.4nm mass production in 2028.

10. Silicon Motion (SIMO US): Multiple Growth Drivers Converging Into 2026E

- Four growth drivers ramping simultaneously: PCIe5 targeting 40% market share, NAND makers increased outsourcing of controller design, automotive segment approaching 10% of revenue, and datacenter products approaching 5-10% of revenue.

- Near-Term catalysts compelling as memory supply tightness drives controller outsourcing and gross margins approach 49-50%.

- 19x 2026E PER represents good value if company hits targets. While stock carries market pullback risk, we nevertheless maintain our Structural Long rating due to multi-year growth in view.

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. OpenAI. Is The Narrative Slowly Disintegrating ?

- Fresh on the heels of his podcast meltdown, Mr. Altman has had to scramble to walk back his CFO’s assertion that a potential federal bailout was on her agenda.

- One of Mr. Altman’s revenue generating ideas is to lease AI compute directly to others. Of course, that’s compute capacity he can’t afford to purchase in the first place.

- Mr. Altman wants OpenAI to be all things to all people all at once. That’s a strategy that rarely ends well. Let’s see..

2. Microsoft. Acting Like There’s An AI Bubble Without Saying There’s An AI Bubble

- Microsoft has significantly course corrected on their compute capacity build out, demurred on their right of first refusal for OpenAI compute demand and adopted a risk off “fungible” compute strategy

- Mr. Nadella thinks AGI as more hype than substance, “jagged” intelligence will remain problematic for a longer, and the true measure of AI success will be measured by GDP growth

- Microsoft stopped reporting AI-driven ARR when the number hit $13 billion six months ago, but why? Broadly deploying AI into productivity tools is a marathon not a sprint.

3. NVIDIA Results: Taiwan Take-Aways — Demand Visibility Implies Strength for Key Suppliers

- NVIDIA’s AI Factory Buildout Signals Multi-Year Demand for Taiwan’s Supply Chain

- TSMC’s Growth Outlook De-Risked by NVIDIA’s Smooth Transition to GB300

- NVIDIA’s Networking Segment Surge Expands System-Level Product Integration Opportunity for Taiwan Ecosystem

4. Taiwan Tech Weekly: NVDA Results- Taiwan Supplier Winners; Silicon Valley’s Substrate- TSMC Slayer?

- NVIDIA Results: Taiwan Take-Aways — Demand Visibility Implies Strength for Key Suppliers

- NVDA Strong Quarter, Strong Guidance, Consensus ~20% Too Low, Stock Is Not Expensive

- Silicon Valley’s Substrate — ASML, TSMC Slayer Or Ideological Pipe Dream?

5. Taiwan Dual-Listings Monitor: TSMC and ASE Premiums Near Spead Short Levels

- TSMC: 24.5% Premium; Near Level to Open Fresh Short of ADR Spread

- ASE: +5.7% Premium; Good Level to Short the ADR Spread

- ChipMOS: -1.7% Discount; Near Discount Level to Go Long the ADR Spread

6. IHI (7013 JP): Orders and Profits Headed Up, Share Price Down

- Sales and operating profit declined YoY in 1H, but new orders were up 17.5% and the book-to-bill ratio rose from 1.00 to 1.25. anagement has raised full-year guidance.

- Aerospace & Defense continue to lead growth, with nuclear energy and Asian EPC making significant contributions to new orders and the restructuring of Industrial Systems & Machinery boosting operating profit.

- Share price down 15% in two weeks to 23x FY Mar-26 EPS guidance. Once again a reasonably valued investment in Japan’s rising defense budget and corporate restructuring.

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Taiwan Tech Weekly: Nvidia Asking TSMC for More Capacity; Apple to Disintermediate Telcos?

- Nvidia Pushes TSMC for More Capacity as AI Chip Demand Surges

- Apple Expands Its Satellite Ambitions for iPhones Beyond Just Emergencies — A Step Towards Disintermediating Telcos?

- Nvidia’s International HQ in Taipei Deal Clears Final Hurdle — Boost for Taiwan 2026E-2027E

2. Substrate. ASML, TSMC Slayer Or Ideological Pipe Dream?

- Silicon valley startup Substrate made waves two weeks ago when they emerged from stealth mode to announce a revolutionary new tool they claim will rival ASML’s EUV lithography capability

- Substrate simultaneously plans to build next-generation semiconductor fabs to return America to dominance in semiconductor production and will use their technology—a new form of advanced X-ray lithography—to power them.

- For a three year old startup, whos CEO has zero documented experience of semiconductors or lithography, these are bold claims indeed. This should be interesting!

3. Humanoid Robots Won’t Take Your Job, We’ve Just Decided Not To Give You The Job In The First Place.

- Jensen Huang claims that the world is running out of workers & there will be a shortage of 50 million workers by the end of the decade. Enter humanoid robots.

- Elon Musk claims that AI and robots will take all our jobs, working will be optional and we can grow vegetables while he’s on his way to becoming a trillionaire

- Technology and society are rapidly approaching a critical decision point. Jobs for robots or for humans?

4. SMIC (981.HK): Although GM May Decline Slightly, Revenue Is Expected to Continue Growing in 4Q25.

- Revenue in 3Q25 was 7.8% higher than in 2Q25, in line with stronger seasonal demand. GM: 22.0% in 3Q25, compared with 20.4% in 2Q25 and 20.5% in 3Q24.

- The Company expects: Revenue Flat to up 2% quarter-over-quarter (QoQ). Gross Margin: Between 18% and 20%.

- SMIC’s stock price has risen 160.7% year-to-date in 2025, outperforming Taiwan Semiconductor (TSMC) – ADR (TSM US) at 44.2% and United Microelectron Sp Adr (UMC US) at 10.8%.

5. Hamamatsu Photonics (6965 JP): Capex Peaking, Profits to Rebound

- Announced last Friday, FY Sep-25 sales and net profit were in line with guidance, but operating profit fell short. On Monday, the shares dropped 4.5%, wiping out a month’s gains.

- Looking ahead, management expects three years of sales and profit growth as capex declines, depreciation and R&D level off, and the NKT Photonics acquisition approaches breakeven.

- In this scenario, semiconductor, bio-medical, defense and quantum computing applications should drive 3-year sales growth of 24% and a 71% increase in net profit, bringing the P/E down to 20X.

6. Silergy (6415.TT): 4Q25 Flat or Slightly Upside; Early Gen4 Yields Remain Non-Comparable.

- 4Q25 seasonal outlook? Silergy expects flat to slightly up QoQ, similar to past years.

- Silergy does see consolidation, and given its stronger financials, product breadth, and R&D capabilities, the company remains a top supplier and will continue to gain share.

- Will 1H next year be better than 2H this year?Hard to say because of Chinese New Year seasonality.We expect YoY growth, but not strong yet.

7. TechChain Insights: ChipMOS Indicates Memory Industry Surge into 2026E; Smartphones Currently Soft

- This assembly and testing leader provides fresh insight into the state of display, memory, consumer, enterprise, and industrial end markets.

- ChipMOS: Memory Industry Strength Offsets Display Industry Weakness. Memory strength seen into 2026E. Company noted soft smartphone industry panel demand currently.

- Management signals sustained memory upcycle; disciplined capex to serve multi-year AI and datacenter growth. We rate ChipMOS shares as a Structural Long.

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Microsoft’s OpenAI Conundrum

- In Q126, Microsoft recorded $4.1 billion in net losses from investments in OpenAI, up from $688 million in the year ago quarter.

- The newly updated partnership between Microsoft and OpenAI has many clauses contingent on when (not if) AGI gets declared. Since AGI has no actual definition, an expert panel will decide.

- Sam Altman dreams of an OpenAI IPO so that detractors can be lured into shorting the stock and getting burned in the process. Revenue growth is a touchy subject, apparently

2. Taiwan Tech Weekly: Mediatek’s Power Move for 2nm Chips; Yet More TSMC Pricing Power

- TSMC Sets Sights on 3-10% Price Rises for Advanced Nodes

- MediaTek’s Leap Into the 2nm Era — Leading Edge Node Signals Market Leadership Ambitions

- Mediatek 3Q25: Good News (ASIC Revenue) But Weak Margins Getting Weaker. Stock Not Attractive.

3. NEC (6701 JP): Tie-Up with Siemens Adds to Growth Potential

- NEC and Siemens plan to develop an automated robot teaching system for faster set-up and more efficient operation of production lines incorporating multiple robots.

- NEC’s FY Mar-26 guidance raised on strong 1H results. BluStellar, which includes digital twins for robot teaching, grew faster than expected.

- Aerospace/Defense led sales growth and followed BluStellar in operating profit. Improving product mix and rising Japanese defense budget point to growing long-term potential.

4. Novatek (3034.TT): 4Q25 Decline; AI-Integrated Products Currently ~20% of SoC Revenue and Growing.

- 4Q25 Guidance: Revenue NT$22–23bn (declined 4.9% QQ); Entering traditional low season. Gross Margin: 35–38%; Operating Margin: 14.5–17.5%.

- AI-Integrated products currently ~20% of SoC revenue and growing. Image SoC / New Camera Trends: New AI Vlog cameras seeing positive demand.

- Key 2026 factors: FX, gold price, raw materials (KGD, substrate) supply.

5. Yageo 3Q25 Take-Aways: Passive Components Leader Benefitting from AI Applications Demand

- Strong AI Demand Sustains Revenue Growth Despite the Seasonal Headwinds

- Recent Shibaura Acquisition Enhances Yageo’s Strategic Positioning in Specialty Components

- We rate Yageo as a Structural Long – AI Content Cycle Should Drive Sustainable Mix Improvement

6. Vanguard (5347.TT): 3Q25 EPS Missed Expectations; 4Q25 and 1Q26 Decline Milder Than Seasonal Trend

- Management expects 4Q25 wafer shipments to decline 6–8% QoQ, while ASP should rise 4–6% QoQ, mainly due to lower DDI shipments.

- The AI revenue share has risen from a low-single-digit percentage in 2024 to a high-single-digit level in 2025.

- The worst phase of mature-node overcapacity has passed, and pricing pressure should ease entering 2026.

7. Taiwan Dual-Listings Monitor: TSMC Premium Eases Down; UMC & CHT Opportunity Levels

- TSMC: +21.8% Premium; Wait for Lower Premium Before Fresh Long

- UMC: +2.2% Premium; Good Level to Short the ADR Premium

- CHT: -2.0% Discount; Near Level to Go Long the ADR Spread

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Taiwan Dual-Listings Monitor: TSMC Near Fresh Spread Short Level; ChipMOS Rare Discount

- TSMC: +23.4% Premium; Near Levels to Open Fresh ADR Spread Short

- ASE: +0.3% Premium; Good Level to Long the ADR Spread

- ChipMOS: -7.5% Discount; Local Shares Rally Makes ADR Deeply Discounted

2. Taiwan Tech Weekly: Apple’s Macbook Windfall; Yageo’s Rally; TSMC’s Massive Rare Earth Stockpile

- Windows 10’s End-of-Life Becomes Apple’s Windfall as Second Fastest Growing Computer Brand

- Eyes on Yageo Results Coming October 30 After 35% 1-Week Surge

- China Tightens Rare Earth Grip: TSMC Says It’s Prepared with Inventory

3. SK Hynix Q325. HBM, DRAM, NAND All Sold Out Through 2026

- SK Hynix reported Q325 revenues of ₩34.45 trillion, up +10% QoQ and up 39% YoY representing an all time quarterly revenue record

- Now given the customers demand and the company’s capacity for next year not only HBM but DRAM and NAND capacity has essentially been sold out.

- DRAM margin could rise closer to HBM but the company does not plan to immediately adjust the capacity mix based on what can be a short-lived change in profitability

4. MediaTek (2454.TT): 4Q25 GM Eases on Mix; 2025 Record Revenue; 2026 AI Upswing Begins

- 4Q25 Guidance: Revenue is NT$142.1 – 150.1 bn (+0 – 6% QoQ, +3 – 9% YoY); Gross margin is 46% ± 1.5ppt; Opex ratio is 31% ± 2ppt.

- Cloud ASIC TAM: Raised from US$40bn → ≥ US$50bn by 2028; MediaTek targeting ≥ 10–15% share; Gross Margin: 4Q dip from mix; 2026 to benefit from repricing + high-value allocation

- MediaTek continues to execute on a dual-engine AI strategy. Despite near-term margin pressure from mix and FX, the company is building a foundation for sustainable profit growth.

5. Realtek Results Readthrough: Normalization Marks Pause Before Next PC Wave

- PC upgrade mini-cycle front-loaded: Realtek 3Q25 results reflected normalization after Windows 10-related demand pulled forward into 1H25, with revenue and margins easing sequentially but remaining solid.

- Diversification offsets softness: Communications infrastructure and automotive Ethernet continued to expand, with stronger growth outside China and resilient contribution from next-gen connectivity and Wi-Fi 7 adoption.

- Cautious near term, constructive on 2026E: Inventory build and tariff uncertainty temper 4Q outlook, but management expects a strong 1Q26 rebound as PC inventories normalize and AI-driven peripherals lift ASPs.

6. UMC (UMC US / 2303 TT): Adeptly Navigating Foundry Industry Transition From Scale to Specialization

- UMC’s 3Q25 results reaffirm its strategic shift toward specialty foundry leadership.

- Revenue was stable at NT$59.13bn with improving utilization and 22nm technology now contributing over 10% of sales. Gross margins remain robust.

- UMC’s growing 22/28nm portfolio, Intel partnership in Arizona, and focus on power-efficient packaging highlight how the maturing foundry sector is moving away from pure node competition and towards application-specific differentiation.

7. ASEH (3711.TT; ASX.US): 3Q25 ATM Record High; 4Q25 Modest Growth; 2025 ATM Revenue +20% YoY (USD)

- 4Q25 Outlook: Revenue is expected to grow by 1% to 2% QoQ. Both of GM and OPM are projected to increase by 0.70 to 1 percent QoQ.

- Growth continues to be driven by AI and HPC demand, with testing revenue exceeding expectations and offsetting minor shortfalls in packaging due to geopolitical uncertainties.

- With 2025 test revenue expected to grow at roughly twice the pace of packaging revenue. Investment priorities are focused on wafer probing capacity for both AI and non-AI devices

8. UMC (2303.TT; UMC.US): 4Q25 Upbeat; 1Q26 May Be a Challenging Quarter Due to Expected Seasonality.

- 4Q25 Guidance: Wafer shipment will remain flat. ASP in US dollars will remain firm. Gross margin will be approximately in the high 20% range.

- Expect interposer technology capabilities to serve the market when volume comes in late 2026 or sometime in 2027.

- 12nm PDK is expected to be ready for the first wave of customers in January 2026. Customer product takeout is expected at the beginning of 2027.

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. TSMC Q325. Today, The Numbers Are Insane

- Q3 2025 revenues of $33.1 billion, slightly exceeding the upper end of the guided range, up 10.1% QoQ and up 40.8% YoY.

- On track for 35% YoY revenue growth in 2025, with revenue likely to exceed $120 billion

- No QoQ revenue growth this quarter suggests either AI demand growth has stalled or TMSC is maxed out at the leading edge. Methinks it’s the latter..

2. Taiwan Dual-Listings Monitor: TSMC Spread Sinks Sharply; ASE Near Parity Again

- TSMC: +22.1% Premium; Continue to View 24% or Higher as Level to Short From

- UMC: +0.4% Premium; Results Coming… Wait for More Extreme Spread Levels

- ASE: +0.4% Premium; Near Good Level to Go Long the ADR Spread

3. Intel Q325. Solid Quarter But Still No Coherent AI Strategy & 18A Yields Won’t Mature Until 2027

- Intel announced Q325 revenues of $13.7 billion, above the high end of the guided range, up 6% QoQ and up 2.8% YoY

- Intel forecasted current quarter revenues of $13.3 billion at the midpoint, down $1 billion YoY and down $400 million QoQ

- 18A yields are not where we need them to be, by the end 2026 they probably will be, and they should be “industry acceptable” by 2027

4. Taiwan Tech Weekly: Mediatek & Nvidia Announce GB10 Partnership; TSMC’s Prices Spur Samsung Interest

- MediaTek Joins Forces with NVIDIA on the GB10 Superchip — Locally-Run AI Models Are Coming to Your Desktop

- TSMC’s 2nm Price Hike Spurs Interest in Samsung, But Underscores Its Strength

- Latest for Smartphone Demand 3Q25: A Little Bit Better, Just a Little

5. Intel (INTC.US): 3Q25 Results Slightly Beat; Emphasized AI Importance; Seeking New Foundry Clients.

- Intel Corp (INTC US) 3Q25 slightly exceeded consensus estimates in both revenue and EPS.

- CEO Lip-Bu Tan emphasized the growing importance of AI, while CFO David Zinsner highlighted the accelerated funding from the U.S. government and strategic investments from NVIDIA and SoftBank

- Intel’s foundry business still relies primarily on internal orders and continues to seek external customers.

6. LRCX Q325. Solid Results, Outlook But China Exposure Is A Glaring Red Flag

- LRCX reported September 2025 quarter revenues of $5.32 billion, marginally above the guided midpoint, up 3% QoQ and up 27.7% YoY.

- LRCX is forecasting current quarter revenues of $5.2 billion at the midpoint, slightly down sequentially, but up 18% YoY. In other words, the AI boost is coming, just not yet.

- The elephant in the room was once again revenue mix from China which accounted for a whopping 43% of sales, up from 35% in the prior quarter. Oh my!

7. IHI (7013 JP): SAR Satellite Deal Adds to Takaichi Trade

- New Japanese Prime Minister Sanae Takaichi aims to raise defense spending to 2% of GDP this fiscal year, two years ahead of the original schedule.

- Takaichi also wants to accelerate investment in advanced defense technologies. IHI, which recently signed an agreement with ICEYE to build earth observations satellites, should be among the beneficiaries.

- IHI’s sales and profit comparisons should turn positive during FY Mar-26. A 7-for-1 stock split effective October 1, 2025, makes the shares more attractive to retail investors.

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. TSMC (2330.TT; TSM.US): U.S. Stocks Plunged on October 10 Under Heavy Selling Pressure.

- U.S. President Donald Trump announced a 100% tariff on China.

- Facing the escalation of the U.S.–China tariff war, U.S. stocks plunged on October 10 under heavy selling pressure.

- Facing the escalation of the U.S.–China tariff war, U.S. stocks plunged on October 10 under heavy selling pressure.

2. Taiwan Dual-Listings Monitor: TSMC Set Up Opportunity During Taiwan Sesssion Ahead of Results Today

- TSMC: +27.3% Premium; Opportunity to Set Up ADR Spread Short During Taiwan Session

- UMC: +2.0% Premium; Wait for Slightly Higher Premium Before Opening Spread Short

- ASE: +2.6% Premium; Wait for More Extreme Swing Before Going Long or Short

3. Nvidia (NVDA.US): Problems Encountered in Land Acquisition to Establish Offshore Headquarters.

- NVIDIA Corp (NVDA US) is setting up an offshore headquarters in Taipei, and is currently in the process of acquiring land.

- Taiwan’s central government is currently ruled by the Democratic Progressive Party (DPP), while Taipei City is governed by a mayor from the Kuomintang (KMT), creating political complications.

- Politics often takes precedence over economics, yet in a democracy, politics is driven by competing parties—inevitably leading to conflicts of interest.

4. TSMC (2330.TT; TSM.US): 4Q25 Outlook Slightly Softer; US Fab to Dilute GM; AI Remains Key Driver.

- For 4Q25, revenue guidance is US$32.2–33.4 billion, equivalent to NT$985.3–1,022.0 billion (based on an assumed FX rate of 30.6).

- N2 will begin mass production later this quarter with good yields, and volume will ramp in 2026 driven by both smartphone and HPC/AI applications

- Smartphone inventory has returned to seasonally healthy levels, with no signs of early pull-ins.

5. Why TSMC 3Q25 Indicates Strong AI Accelerator Demand Through 2029E; Maintain Structural Long Rating

- TSMC 3Q25: Margins Surge as Pricing Power Strengthens Ahead of 2nm Ramp

- AI Megatrend Continues to Reshape Demand – 40% CAGR Expected for AI Accelerators Through 2029

- Maintain Structural Long Rating — TSMC Remains Inexpensive vs. Tech Companies Highly Dependent on It

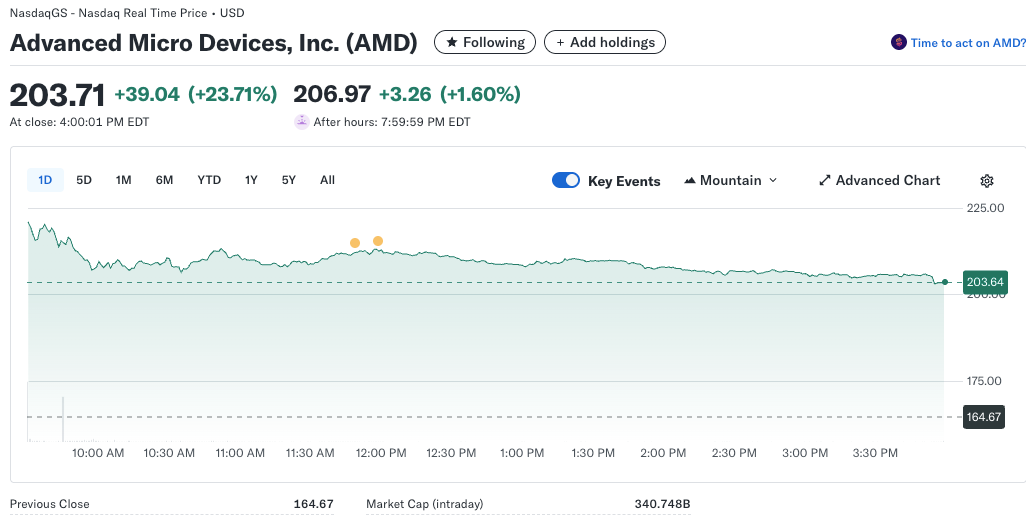

6. First AMD, Now Broadcom. How OpenAI Is Ruining NVIDIA’s Party

- OpenAI just signed a deal with Broadcom to deploy ten gigawatts of OpenAI designed AI accelerators targeted to start in H2 2026, and to complete by end of 2029.

- OpenAI’s AMD & Broadcom deals undermine the credibility of the NVIDIA deal. Where exactly is all the money going to come from?

- In partnering with AMD and Broadcom, OpenAI has given huge credibility to AMD as a GPU competitor and Broadcom as a custom accelerator competitor. Two big headaches for NVIDIA. Ouch!

7. Memory Monitor: Nanya Tech Indicates DRAM Price Spike to Persist Longer; SK Hynix Relative Trade

- Nanya Tech 3Q25: Rebounds to Profit Thanks to DDR4 Price Surge Windfall… But Underlying Structural Drivers Remain Unsteady

- The World’s DDR4 Shortage to Extends Pricing Spike Through 4Q25

- Nanya Technology vs SK Hynix — We Expect Relative Strength Ahead for SK Hynix Over Nanya Tech

8. Taiwan Tech Weekly: TSMC’s Market Share Keeps Rising; Semi Revenues Show AI the Only Pillar; AI PCs

- TSMC’s Grip Tightens: 2Q25 Market Share Hits New Heights; September Revenue Implies Even More Taken

- TSMC (2330.TT; TSM.US): U.S. Stocks Plunged on October 10 Under Heavy Selling Pressure.

- PC Monitor: Dell Doubles Multi-Year Forecasts; AI PC Up-Cycle, Art Thou Finally Here?

9. MediaTek (2454.TT): 4Q25 Expected to Be Flat QoQ; D9600 Mass Production Scheduled for Late 2026.

- Mediatek Inc (2454 TT)’s 4Q25 performance is expected to remain roughly flat QoQ, compared with 3Q25.

- Based on the product launch cycles of major smartphone manufacturers, by the end of 2026, the 2nm process will be adopted in multiple flagship chips

- At the China Mobile Global Partner Conference on October 10, MediaTek showcased a range of its latest products

10. Semiconductor WFE. China Retains #1 Spending Slot In Q225, US Mulls Yet Further Sweeping Sanctions

- Q225 WFE billing amounted to $33 billion, up 24% YoY and up 3% QoQ. China was the biggest spender with billings of $11.36 billion, +11% QoQ, albeit down 7% YoY

- A US select committee on China WFE spending, published on October 7 last, highlights multiple gaps with existing US restrictions on China WFE and proposes nine separate remedies

- Remedies include sweeping China country-wide bans, bans on related components, consumables & deploying “incentives & leverage” with allies so they follow suit. Still wondering about China’s surprise rare earth move?

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. OpenAI, AMD Enter Into Strategic Partnership. Guys, This Is Getting Ridiculous!

- OpenAI agrees to deploy 6 gigawatts of AMD GPUs based on a multi-year, multi-generation agreement. The deal could be worth upwards of $100 billion to AMD through 2030

- AMD issued OpenAI a warrant for up to 160 million shares of AMD common stock, structured to vest as specific milestones are achieved, including AMD share price appreciation to $600

- Could a strategic partnership with Intel now also be on the cards? After all, OpenAI needs CPUs as well as GPUs, especially as they ramp into enterprise. Just saying…

2. Hitachi Ltd. (6501 JP): Tie-Up with OpenAI Opens the Flood Gates

- An agreement to supply OpenAI with energy-saving electric power equipment should be accretive to Hitachi’s sales and profits as long as the AI boom continues.

- Hitachi is also building an “AI Factory” based on Nvidia technology. This should accelerate the growth of Hitachi’s Lumada digital services platform, also boosting sales and profits.

- Hitachi’s share price jumped 10.3% on the OpenAI news. Data center news flow and AI sentiment now drive the share price.

3. Intel (INTC.US): AMD to Submit Foundry Orders to Intel? We Think It’s Highly Unlikely.

- What is happening with Advanced Micro Devices (AMD US) and Intel Corp (INTC US)?

- Intel’s stock price has risen about 50% from its April 8 low. However, we have yet to see any tangible progress in its manufacturing technology.

- Intel’s stock price has risen about 50% from its April 8 low. However, we have yet to see any tangible progress in its manufacturing technology.

4. Astroscale (186A.T-JP/ASTRO): The Small-Cap Takaichi Defense Trade

- After months of going nowhere, Astroscale shot up more than 20% in the two trading days following the election of defense hawk Sanae Takaichi as president of the LDP.

- Astroscale made a small gross profit last quarter, but needs a rising flow of contracts and subsidies in order to turn profitable at the operating and net levels.

- At ¥825, the stock price is 38% below the ¥1,326 high reached just over a year ago. If Takaichi becomes prime minister, the chances of regaining that high would improve.

5. Taiwan Tech Weekly: Why Many Tech Companies Could Soon See Their Chip Costs Rise Substantially

- As Chips Move to 3nm and 2nm Designs, Tech Companies Could See a Sharp Increase in Their Chip Manufacturing Cost

- Intel (INTC.US): AMD to Submit Foundry Orders to Intel? We Think It’s Highly Unlikely.

- HBM Stocks Will Keep Running (Micron, SK Hynix), It’s Just the Beginning

6. PC Monitor: Dell Doubles Multi-Year Forecasts; AI PC Up-Cycle, Art Thou Finally Here?

- Dell doubles long-term growth outlook to 7–9% revenue and 15%+ EPS CAGR through FY30, led by AI infrastructure.

- AI PCs emerge as Dell’s next growth engine; global refresh cycle could finally kickstart long-awaited PC upturn.

- Taiwan makers Asus, Acer, Quanta, and Wistron positioned to benefit as AI PC and server demand scales together.

7. Taiwan Dual-Listings Monitor: Weak US Friday Session Opens Up Wide Opportunities Across the Board

- TSMC: +19% Premium; Good Level to Close Out for Those Short the ADR Spread

- UMC: -3.9% Discount; Rare Deep Discount Good Level to Long the ADR Spread

- ASE: -5.5% Discount; Any Spread Below Parity a Good Level to Long the ADR Spread

8. Sovereign AI. National Strategic Imperative, FOMO Or Both?

- If all of the publicly announced sovereign AI initiatives come to pass, they could account for upwards of $1 trillion in AI infrastructure spending through 2030

- For now, “sovereign” AI means mostly means made in the USA. However, there a growing demand for “sovereign” AI from China, particularly among countries disillusioned by the US trade wars

- In general AI infrastructure, the US is outspending China six to one in 2025. Could one be spending too much and the other spending too little? Let’s see…

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Taiwan Dual-Listings Monitor: TSMC & UMC Spreads Higher After Taiwan Market Holiday

- TSMC: +28.3 Premium; Historically Extreme Level, Can Short the ADR Premium

- UMC: +3.3% Premium; Historically Extreme Level, Short the ADR Premium

- CHT: -0.7% Discount; Near Lower Bound, Consider Going Long the Spread

2. TSMC: New Signals Underscore N2’s Rise as a Blockbuster Node

- Latest Signals Continue to Indicate N2 Is Emerging as TSMC’s Blockbuster Node

- N2 Commercialization Timing Aligns With Major AI HPC Platform Roadmaps

- TSMC Market Share Over 70%… Could N2 Drive This Number Even Higher? Maintain Our Structural Long Rating for TSMC

3. PC Monitor: Nvidia GB10 PCs Poised to Redefine the AI PC Category

- GB10 Brings Nvidia AI Performance From Data Center to the Desktop

- GB10 PCs Will Be “True” AI PCs, Their Capabilities Will Be More Evident

- From Niche to Market Driver; Maintain Structural Long for Mediatek, Asustek, Acer

4. TSMC (2330.TT; TSM.US): Is It Possible TSMC’ Output Reach a 50:50 Ratio Between the U.S. And Taiwan?

- The U.S. Secretary of Commerce, Howard Lutnick, has requested that Taiwan Semiconductor (TSMC) – ADR (TSM US)’s production output reach a 50:50 ratio between the U.S. and Taiwan.

- By contrast, TSMC’s fab construction also requires strong supplier coordination, and in the case of its U.S. fabs, there are numerous regulatory hurdles to overcome.

- Meanwhile, Semiconductor Manufacturing International Corp (SMIC) (981 HK)’s share price in Hong Kong has surged this year (+209.14%), significantly outperforming TSMC’s share price increase (+28.15%).

5. It’s Official, OpenAI Is Becoming A Multi-Trillion Dollar Hyperscaler

- Inference compute is going increase by a factor of one billion. It’s already gone up at least 2x in the past twelve months

- OpenAI will become the next multi-trillion dollar hyperscaler. NVIDIA is going to make sure this happens

- AI-Related revenues have already reached $1 trillion since all hypercaler revenues are now AI related according to Jensen. Problem solved!

6. Taiwan Tech Weekly: OpenAI to Consume Nearly Half of Global DRAM; Why TSMC 2nm Will Be A Blockbuster

- OpenAI, Samsung & SK Hynix Lock In Memory Pact — Taiwan Next Stop

- MediaTek’s Major ASIC Ambitions Face Delays from Some Key Clients

- TSMC: New Signals Underscore N2’s Rise as a Blockbuster Node

7. Intel (INTC.US): Seeking Investment from TSMC?

- NVIDIA Corp (NVDA US)’s investment is focused on joint AI development.

- Intel Corp (INTC US) may seek to invite Taiwan Semiconductor (TSMC) – ADR (TSM US) to join its investment initiative.

- Meanwhile, Intel Corp (INTC US)’s stock price has risen about 50.2% from its recent low.

8. Taiwan Dual-Listings Monitor: TSMC Premium Remains High Ahead of 3Q Results; CHT Rare ADR Discount

- TSMC: +26.8% Premium; Remains at Historical Extreme; Earnings Release Ahead

- ChipMOS: +1.3% Premium; Wait for Higher Level Before Shorting the Spread

- CHT: -1.0% Discount; Good Level to Go Long the ADR Spread