This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Intel CFO @ Citi’s 2025 Global TMT Conference: “We Will Use TSMC Forever”

- We will be putting products on TSMC you know, forever, really. TSMC is a great partner for us. Obviously everyone understands that their support and technology are great.

- 18A is actually a good node for us. We want to milk that node We won’t get peak volume on 18A until the 2030 timeframe.

- Kevork Kechichian joined Intel as head of the Data Center Group. He will lead Intel’s data center business across cloud and enterprise, including the Intel Xeon processor family

2. Synopsys Crashes On “Major Foundry Challenges”. Intel, What Have You Done?

- Last week, Synopsys reported Q325 results and guidance both well below expectations causing the share price to collapse over 34% in the immediate aftermath.

- The company revised down full year revenue targets, noting that “challenges at a major foundry customer are also having a sizeable impact on the year”

- That “major foundry customer” is likely Intel. Who’s next in line to face similar revenue impact from Intel’s challenges?

3. MediaTek: Satellite Connectivity the Next Strategic Battleground for Mobile SoCs (Structural Long)

- Starlink’s Direct-to-Phone Semiconductor Integration Push Signals a Major Shift Coming for Telecom

- Direct-To-Satellite Connectivity Could Become Critical for a Market-Competitive Smartphone SoC Design

- Leadership in Satellite Connectivity Will Soon Mean Leadership in Smartphone SoCs

4. NVIDIA Becomes The Latest To Back Intel’s GoFundMe Appeal

- NVIDIA will invest $5 billion in Intel’s common stock at a purchase price of $23.28 per share

- Intel will supply custom x86 server CPUs to NVIDIA, who in turn will sell RTX graphics cores to Intel to combine into an new type SOC for the PC market

- Under sustained questioning during the Q&A, Jensen did a remarkable marketing pitch for TSMC, drowning any hopes of a looming Intel Foundry deal for the foreseeable future

5. TSMC’s COUPE Signals Silicon Photonics Go-Time — Early Winners in Taiwan’s Listed Supply Chain

- Last week at SEMICON, TSMC unveiled COUPE, moving silicon photonics from lab demos into industrial-scale advanced packaging.

- Himax, ASE, Zhen Ding, GlobalWafers, ACON, and Accton form Taiwan’s listed ecosystem for silicon photonics adoption.

- As NVIDIA Corp (NVDA US)-driven AI clusters proliferate, the power and cost of moving data between chips have become as constraining as compute itself.

6. Taiwan Tech Weekly: Starlink Engaging Chipmakers in Direct-To-Phone Push; Intel’s TSMC Dependency

- Starlink Engaged with Chipmakers to Bring Satellite Connectivity Direct to Smartphones — Mediatek Well Placed to Benefit

- Intel CFO @ Citi’s 2025 Global TMT Conference: “We Will Use TSMC Forever”

- TSMC’s COUPE Signals Silicon Photonics Go-Time — Early Winners in Taiwan’s Listed Supply Chain

7. Intel (INTC.US): NVIDIA’s $5B Intel Stake — A Shift in Tech’s Competitive Landscape?

- NVIDIA Corp (NVDA US) surprised the market with its announcement of a $5 billion investment in Intel Corp (INTC US).

- The market seems to read this as the beginning of a deeper Intel–NVIDIA partnership in AI chips.

- We also note that Japan’s push to establish its own foundry industry through Rapidus deserves continued attention, as it could reshape the competitive map in the years ahead.

8. Memory Monitor: The Sticky Era — Memory’s Transition from Spot Pricing to Long-Cycle Commitments

- The Industry Is Moving From Cyclical Volatility Into a Sticky Pricing Era.

- Why Memory Pricing is Becoming Sticky. — HBM Memory is Hard to Swap Out Once Designed Into a GPU Product.

- Investment View: Entering Memory’s Sticky Pricing Era — Structurally Long Micron & SK Hynix; Underperform for Nanya Tech.

9. UK Sovereign AI Proudly Paid For & Made In The USA

- Microsoft CEO Satya Nadella announced his intention to spend $30 billion on AI infrastructure in the UK. NVIDIA, Coreweave, Alphabet and OpenAI are also ponying up further billions

- Jensen Huang declared the UK and AI powerhouse, third in line globally behind the US and China

- Is it really UK sovereign AI when it’s mostly paid for and made in the USA?

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. @Sama Says There’s An AI Bubble. What’s Going On?

- OpenAI CEO Sam Altman caused quite a stir with his recent comments about an AI bubble, people getting burned and someone on track to lose a phenomenal amount of money

- However, his message would appear to be directed at other AI startups, not OpenAI, which he says plans to spend trillions on data centers in the not very distant future

- Meta’s no-cost-spared talent grab & Palantir’s valuation are bubbly red flags but the AI infrastructure build out currently underway is real & rational, assuming the ROI can follow expeditiously

2. MIT Report Claims 95% of GenAI Projects Fail. How Is This Possible?

- Despite $30–40 billion in enterprise investment into GenAI, this report uncovers a surprising result in that 95% of organizations are getting zero return

- While employees are likely using LLMs in a personal capacity, this mostly isn’t feeding into the KPI’s that are being used to monitor the success of GenAI projects

- The harsh reality is that integrating GenAI tools into existing workflows is time consuming, needs careful planning and likely best done with help from the professionals.

3. Texas Instruments & KLA Signal Continued AI Strength, Foreshadow TSMC’s 2nm Breakout

- TI is experiencing 50%+ YoY growth in data center, showing no signs of AI server demand slowdown.

- KLA calls 2nm a “compelling” node, projecting it could be the industry’s largest over first three years.

- Taiwan Tech positioned to benefit via TSMC N2 ramp, CoWoS packaging, and ABF substrate expansion.

4. UMC (2303.TT; UMC.US): 4Q25 Revenue Is Projected to Decline 5–10% QoQ.

- United Microelectron Sp Adr (UMC US) – 2025 Full-Year and 4Q Outlook.

- The impact of U.S. recent restrictions on United Microelectron Sp Adr (UMC US) appears negligible.

- Customer demand trends are diverging in 2H25, and overall demand is expected to soften in 4Q25.

5. TSMC (2330.TT; TSM.US): TSMC Has Raised Wafer Prices; Rapidus Provides 2nm Milestone.

- Taiwan Semiconductor (TSMC) – ADR (TSM US) has raised wafer prices, with 2nm wafers expected to cost at least 50% more—exceeding USD 30,000 per wafer.

- Rapidus plans to begin 2nm engineering production in 1Q26 and target mass production by 2027, likely one node behind TSMC.

- Taiwan Semiconductor (TSMC) – ADR (TSM US) is expected to be ready for iPhone 17 production.

6. Taiwan Tech Weekly: SEMICON Taiwan Just Started; TSMC August Sales Soar; 2026 to Be Year of Edge AI?

- TSMC August Revenue +34% YoY: AI Demand Remains the Key Driver

- ARM Pushes Edge AI Forward with New “Lumex” Chip Designs — 2026 Could Be a Major Growth Year for Edge AI

- From AI Packaging to AI Edge: Listed Names to Watch at SEMICON Taiwan 2025 Starting Today

7. From AI Packaging to AI Edge: Listed Names to Watch at SEMICON Taiwan 2025 Starting Today

- Defining themes: Packaging, edge AI, and silicon photonics dominate SEMICON Taiwan 2025

- Global heavyweights Applied Materials, Lam, and TEL anchor this year’s industry sponsorship

- Taiwan’s next tier — Zhen Ding, ASE, Advantech, ASPEED, Egis — showcase critical AI enablers beyond TSMC

8. Hitachi Ltd. (6501 JP): Short and Long Term Benefit from New U.S. Investments

- More than $1 billion to be invested in electric power equipment and railway car production, plus a new automation center, to counter tariffs and support long-term expansion in the U.S.

- The rising share of sales accounted for by smart factory and other digital technologies should lead to higher profit margins and ROIC over the next several years.

- The share price has dropped 13% from its recent high to 26x EPS guidance for FY Mar-26. Buy on weakness for long-term growth. The main risk is a slowing economy.

9. Intel (INTC.US): Who Will Adopt Intel’s 14A Technology?

- Why does Intel Corp (INTC US)’s current CFO state “Intel will use TSMC basically forever”?

- From Taiwan Semiconductor (TSMC) – ADR (TSM US)’s perspective, they have always maintained a “no competition with customers” principle.

- Another question remains: who will adopt Intel’s 14A technology in 2027-28?

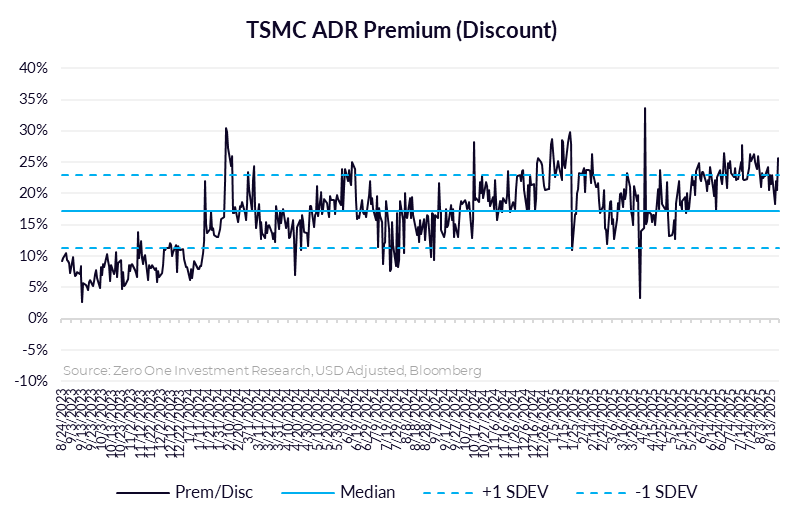

10. Taiwan Dual-Listings Monitor: TSMC Extreme Level; ASE Spread Hits Parity; ChipMOS Near Long Level

- TSMC: +24.4% Premium: Remains at Level to Short the ADR Spread

- ASE: 0.0% (Parity); Open Fresh Longs Here or at a Discount

- ChipMOS: -1.9% Discount; Near Level to Go Long the Spread

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

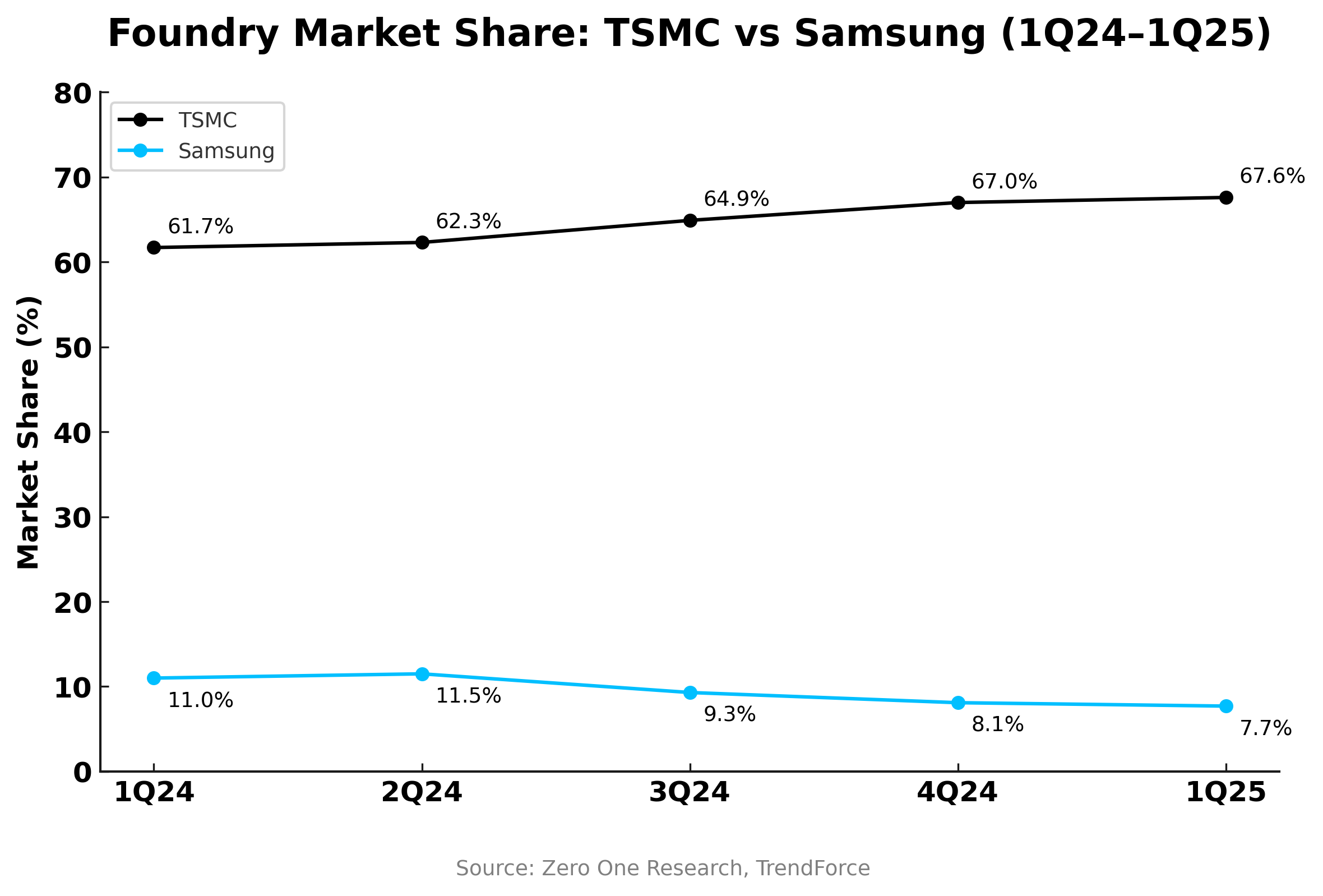

1. Samsung’s Intel Gambit: A Signal of TSMC’s Widening Lead

- Samsung’s potential Intel stake highlights need for packaging know-how, not customers, and provides a hedge if its 2nm yields or production slip.

- TSMC extends lead with stable N3, on-track N2, AI packaging dominance, and customer migrations, while Samsung’s foundry share declines below 8%.

- Implications: Positive for TSMC (2330 TT), negative signal for Samsung (005930 KS), validating for Intel (INTC US) though regulatory and governance constraints remain important.

2. Nidec (6594 JP): Wait for Hard Numbers

- Nidec dropped 22% on Thursday following management’s decision to establish an independent committee to investigate accounting irregularities. It bounced back nearly 5% on Friday, but finished the week down 20%.

- In June, the Company received approval to postpone submitting its FY Mar-25 securities report until September 26. In July, it released incomplete 1Q results while postponing full disclosure.

- Without correct numbers, we can only guess at the full impact of the accounting irregularities and their effect on management.

3. Intel (INTC.US): Qualcomm CEO Has Publicly Stated that Intel’s Technology Is Still Not Competitive.

- Intel Corp (INTC US) has not given up on Intel Foundry Service (IFS), even though it currently lacks any sizable clients.

- We are puzzled as to why Intel former CEO Pat Gelsinger insisted on entering the foundry market, which has so far weakened Intel’s financials without generating meaningful returns.

- Qualcomm Inc (QCOM US) CEO has publicly stated that Intel’s manufacturing technology is still not competitive.

4. Taiwan Dual-Listings Monitor: TSMC Premium at Historically Extreme Level; ASE Bounces Off Parity

- TSMC: 26.2% Premium; Historically Extreme Level to Open Fresh Short of the Spread

- UMC: +1.0% Premium: Wait for More Extreme Level Before Going Long or Short

- ASE: +2.7% Premium; Open Fresh Longs of ADR Spread Closer to Parity

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Taiwan Dual-Listings Monitor: TSMC Premium Spike Opportunity; ASE Hard Bounce to Prem from Discount

- TSMC: +25.6% Premium: Latest Spike is Opportunity to Short the ADR Spread

- UMC: +2.0% Premium; Near Level to Go Short the ADR Spread

- ASE: +5.1% Premium; Good Level to Take Profits on Previous Long Since Parity

2. Intel (INTC.US): Intel–U.S. Government Equity Deal: Implications and Industry Perspective

- Intel has reached an agreement with the U.S. government, under which Washington will invest $8.9bn for a 9.9% equity stake in the company.

- Intel benefits from the optics of government backing, which could help sentiment and prevent downside pressure on the stock in the short term, i.e. near-term optics positive, fundamentals unchanged.

- TSMC’s Japan and Germany fabs were structured through co-investments and partnerships, with equity involvement only when tied to technology access (e.g., Sony CMOS JV).

3. Taiwan Teck Weekly: Apple Snags Over Half of TSMC’s Best Chips; Long-Reasoning AI Will Surge Compute

- Apple Secures Over Half of TSMC’s Cutting-Edge 2nm Capacity; How TSMC Anchors Apple’s Product Leadership Strategy

- NVIDIA Results Key Take-Away: Long-Reasoning AI Models Driving Massive Compute Demand

- Intel (INTC.US): Intel–U.S. Government Equity Deal: Implications and Industry Perspective

4. Taiwan Dual-Listings Monitor: TSMC Premium Remains Elevated; ASE Drops Down to Near Parity

- TSMC: +21.8% Premium; Wait for Higher Premium Before Fresh Short of the Spread

- UMC: -0.6% Discount; Wait for More Extreme ADR Spread Level

- ASE: +0.4% Premium; Good Level to Go Long the ADR Spread

5. Silergy (6415.TT): 3Q25 Revenue Flat to Slightly Up QoQ; Annual Growth May Fall Short of 20%+.

- 3Q25: Revenue flat to slightly up QoQ; GM stable at 52–54%. FY25: Prior 20%+ growth target unlikely to be achieved; weaker demand due to trade war & customer conservatism.

- No evidence of significant market share loss; instead, delayed demand.

- Automotive Ssegment continues to trend upward with new EV-related products. Competition in China is intense, especially EVs, but pricing remains rational.

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Intel Snags $2 Billion From SoftBank. What Now?

- Intel just announced that SoftBank has agreed to buy $2 billion worth of Intel stock, details here.

- The shares are likely newly issued, meaning dilution of existing shareholders. Markets didn’t care and shares rose >5% in after hours trading.

- $2 billion is a far cry from the $40 billion former CEO Craig Barrett thinks Intel needs. Could this be the first of similar deals with US semiconductor/technology companies?

2. CHIPS Act Money For Equity Stake, Pay For China Play? For Goodness Sake!

- US commerce secretary Howard Lutnick confirmed that the US Administration is pursuing a strategy of converting CHIPS Act funding into equity stakes with Intel acting as its guinea pig

- It seems clear that Mr. Lutnick is bent on applying the same formula with other beneficiaries of US CHIPs Act funding

- CHIPs Act Dollars for Equity, Pay For China Play may seem like innovative ideas but in reality they are a slippery slope to confusion & chaos. Who or what’s next?

3. Intel (INTC.US): SoftBank Buys $2bn of Intel Stock at $23; U.S. Government Considers Investment.

- Monetary support may temporarily ease Intel’s current financial difficulties, but the ultimate solution lies in securing technical support from manufacturing.

- We remain curious how the U.S. government will devise a solution for Intel if the company ultimately cannot provide the necessary support for U.S. Fabless players.

- We are bearish on Intel Corp (INTC US)’s current position and do not believe financial support alone can help the company overcome its challenges.

4. SUMCO Q225. Operating Profit Tanks As Depreciation Soars

- SUMCO reported Q225 revenues of ¥102.9 billion, flat sequentially and roughly 3% higher than guidance.

- Operating profit of ¥1.5 billion was also slightly better than the forecasted breakeven, but dramatically down from its peak of ¥30.2 billion in Q322.

- A projected further increase in depreciation charges for the current quarter is forecasted to drive operating profit to negative ¥3.5 billion. Yikes!

5. TSMC (2330.TT; TSM.US): 2nm Production Schedule in US Could Be One Year Ahead of Previous Schedule.

- TSMC Chairman C.C. Wei previously emphasized that customer demand for 2nm technology surpasses that for 3nm, and the company is actively working to expand production capacity.

- For 2nm technology, we expect production to take place at the Tainan fab, ahead of the U.S. Arizona fab and earlier than the previously anticipated 2028 timeline.

- Taiwan Semiconductor (TSMC) – ADR (TSM US)’s next generation 2nm development is actively progressing.

6. Intel’s Historic Agreement Or Moment Of Surrender?

- Intel has agreed to convert US CHIPs Act funding (past & future) & Secure Enclave contracts into a 10% equity stake for the US Administration.

- The equity stake will comprise 433.3 million primary shares of Intel common stock at a price of $20.47 per share, a roughly 16% discount to their market value yesterday

- In his commentary on the deal, President Trump referred to Intel CEO Lip-Bu Tan as a victim, stating he came to the White House to save his job. Wow!

7. A Defining Bet: Intel’s New Capital and the Case for Buying a Stake in Taiwan’s UMC

- A major Intel balance sheet boost, backed by SoftBank, the U.S. government, and leading institutions, would enhance the company’s capacity to make bold bets on regaining global chip manufacturing leadership.

- UMC’s market valuation is less than the capex for just one advanced fab. Intel would likely make a gain on its investment since it would cause UMC shares to rally.

- For less than the cost of a single advanced fab, a large company could acquire UMC and gain chipmaking expertise approaching TSMC’s level; boosting returns across an entire fab network.

8. Taiwan Tech Weekly: TSMC’s US Fabs On a Roll; Why Intel Should Invest in UMC; The Big SPE Reset

- TSMC’s Tale of Two Fabs: Arizona’s Surprise Upside vs. Kumamoto’s Challenges

- A Defining Bet: Intel’s New Capital and the Case for Buying a Stake in Taiwan’s UMC

- SPE – Semi Production Equipment: The Big Reset Is Happening. SPE Firms Expectations Is the Problem

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Intel CEO Heads To DC To Save His Job As Former CEO Calls His Leading Edge Strategy A Joke

- Intel CEO Lip Bu Tan is reportedly headed to Washington today to meet with the US Administration and clear up any misunderstandings about his past investments in China etc.

- Meanwhile, former CEO Craig Barrett published his third opinion piece about Intel’s future and calls LBT’s strategy of not investing further in 14A without customer support a joke

- It’s challenging to deal with the US Administration from a position of strength. It’s a whole different ball game when both the CEO & the company are in crisis mode…

2. Taiwan Dual-Listings Monitor: TSMC Spread Remains Extreme; UMC ADR Short Interest Falling

- TSMC: +22.8% Premium; ADR Spread Remains at Historically Extreme Levels

- UMC: -0.8% Discount; Wait for More Extreme Levels; Short Interest in ADRs Falling

- ASE: -0.1% Discount; Continued Opportunity to Go Long the ADR Spread

3. Taiwan Tech Weekly: Foxconn US$1bn USA Robotics Push; Samsung Doubles Down on US Fabs; Intel Crisis

- Foxconn Tech invests US$1bn in U.S. robotics, AI, and smart manufacturing over 10 years, expanding into service robotics via RoboTemi stake.

- Samsung to surpass US$50bn in U.S. chip investments, adding US$7bn for advanced packaging to compete with TSMC and capture AI/HPC integration opportunities.

- Intel faces leadership crisis as CEO Lip Bu Tan’s strategy is criticized; U.S. policy and competitive pressures may accelerate market gains for TSMC and Samsung.

4. TSMC (2330.TT; TSM.US): Board Meeting Resolutions; 2nm Technology Information Leakage Issue.

- Taiwan Semiconductor (TSMC) – ADR (TSM US) disclosed Board of Directors meeting resolutions today.

- Taiwan Semiconductor (TSMC) – ADR (TSM US) 2nm technology manufacturing information leakage issue.

- Currently, only TSMC, Samsung, and Intel have achieved trial production at the 2nm node.

5. Apple. A Master Class On How To Win Friends & Influence People

- Apple CEO Tim Cook visited the White House announcing an additional $100 billion investment in the US over the next four years, on top of the $500 billion already committed.

- He launched the American Manufacturing Program with nine initial members seven of which are already long terms partners and two of which have no direct relationship with Apple at all

- Samsung with its image sensor deal (presumably) and MP Materials with its rare earth magnets deal are two clear winners from the Apple announcement. Overall, successful mission by Mr. Cook.

6. Nanya July Revenue Soars 31% MoM As Micron Revises Current Quarter Guide Up >5%

- Nanya last week announced that revenues for the month of July amounted to NT$5.3 billion, an increase of 31.4% MoM, and an increase of 95% YoY,

- Micron this week revised upwards its guidance for the current quarter with a roughly $500 million increase in revenue, attributable primarily price increases for DDR5

- Customisation of Micron’s HBM4E base logic die is transforming their key customer relationships from commodity vendor to strategic ASIC design-like partner. That’s good for Micron…

7. AMAT Q325. Tanking On Tepid Leading Edge Outlook & China Woes

- AMAT reported FY Q325 revenues of $7.3 billion, up 3% QoQ, up 8% YoY and ~$100 million above the midpoint of the guided range

- Looking ahead, AMAT forecasted current quarter revenues of $6.7 billion at the midpoint, down 8.3% QoQ and down 4.9% YoY

- The China slump was not unexpected, but the leading edge logic drop was definitely a surprise

8. PC Monitor: ASUS’s Gaming & Commercial Strength Signal AI PC Cycle; Positive Read for Dell, HP

- ASUS experienced record 2Q25 revenue driven by 30–40% YoY growth in gaming and commercial PCs, supported by a new GPU sales strength and enterprise market expansion.

- AI servers held mid-teens revenue share for ASUS; margin pressure from tariffs and FX expected to ease after 3Q.

- Strong gaming and commercial PC momentum could signal PC upgrade activity in response to AI PCs, offering positive read-through for Dell and HPQ’s upcoming results end-August.

9. Taiwan Dual-Listings Monitor: TSMC ADR Premium Sees Small Breakdown; ASE Discount Long Opportunity

- TSMC: +21.5% Premium; Historically High Short Interest in the Local Begins to Drop?

- ASE: -0.4% Discount; Opportunity to Go Long the ADR Premium

- UMC: +0.2% Premium; Wait for More Extreme Levels Before Going Long or Short the Spread

10. Himax (HIMX US) – Share Drop: Near-Term Weakness Offset by Structural Automotive & AI Growth Drivers

- 2Q25 beat on margins, in-line on profit; automotive and non-driver ICs resilient despite macro headwinds; guidance points to weaker 3Q25 from seasonal bonus costs and softer demand.

- Automotive, OLED, WiseEye AI, and WLO/CPO remain multi-year growth drivers; CPO mass production targeted for 2026 with early-stage annualized revenue potential above US$100m.

- Shares likely fell on weak near-term outlook, but structural leadership in automotive display ICs, AI sensing, and optical technologies underpins long-term growth runway through 2028.

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Taiwan Dual-Listings Monitor: TSMC Spread Short Setup, ASE ADR at Historically Rare Discount

- TSMC: +23.9% Premium; Continued Opportunity to Short the ADR Premium

- UMC: -0.4% Discount; Wait for More Extreme Levels Before Going Long or Short

- ASE: -1.5% Discount; Historically Rare Discount Presents Opportunity to Long the ADR Spread

2. TechChain Insights: Taiwan’s Battery Cell Moment? USA & EU Supply Chain Under Strategic Pressure

- Battery cells are the new chokepoint in the global clean energy supply chain, with China still controlling 75%+ of global capacity and exporting under increasingly restrictive terms.

- Taiwan is emerging as a high-trust, high-precision hub for advanced cell manufacturing, applying its semiconductor model to batteries.

- With pouch cells gaining traction across drones, robotics, and compact mobility, Taiwan’s lab-to-fab advantage positions it as a future anchor of the U.S. and European energy ecosystems.

3. Intel. Was Tesla’s Deal With Samsung The Death Knell For IFS?

- Tesla & Samsung just inked an eight year, $16.5 billion foundry deal set to run from July 24, 2025 through December 31, 2033.

- Had Intel snagged this deal, it would have been a lifesaver for the company. Not getting it likely triggered the updated “Risk Factors” section in their latest 10K.

- This isn’t Intel playing politics, there’s no point. It’s LBT laying it on the line for investors. Continued investment in 14A is no longer a given. It’s that simple…

4. Taiwan Tech Weekly: TSMC’s Arizona Surprise – 2nm by 2026?; Signs of Hyperscaler Growth Acceleration

- U.S. 2nm Production May Begin Sooner Than Expected — Is TSMC Responding to Unprecedented N2 Demand?

- Hyperscalers 2Q25: Revenue Growth Accelerates, Cloud Revenues Accelerate, Capex Higher

- TechChain Insights: Taiwan’s Battery Cell Moment? USA & EU Supply Chain Under Strategic Pressure

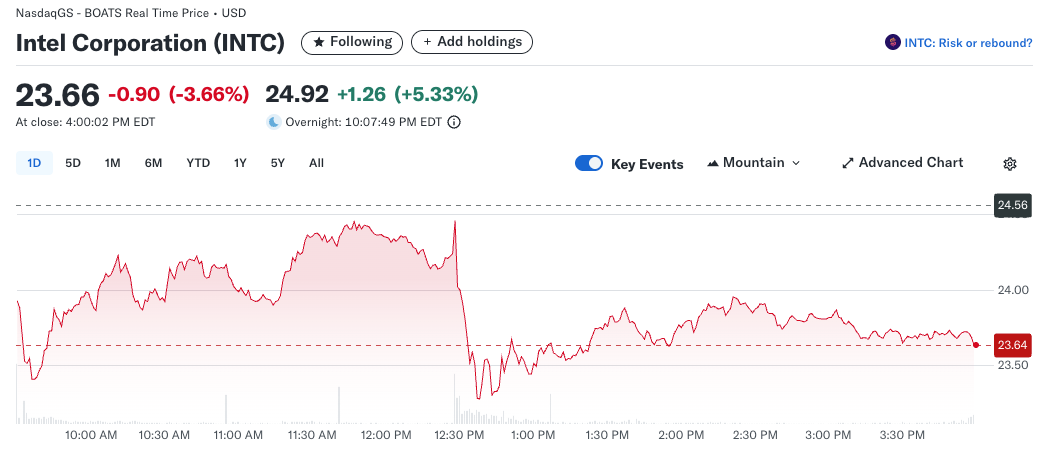

5. Intel. Crisis Mode All Over Again

- President Trump wants Intel CEO Lip Bu Tan to resign immediately because he claims that he is “highly CONFLICTED”

- The President’s concerns likely relate to a recent DoJ case against Cadence as well an investigation by the Select Committee on the CCP into Walden International’s Chinese investments

- That both these topics weren’t comprehensively addressed and mitigated prior to Mr. Tan’s appointment beggars belief. Where was the due diligence Mr. Yeary?

6. Intel (INTC.US): Changing the CEO Could Save This Company? Probably the Wrong Direction.

- US President Trump urged Intel Corp (INTC US) yesterday to replace its current CEO, Mr. Lip-Bu Tan.

- We believe Intel Foundry Services (IFS) could be a highly challenging — or even misguided — strategy

- Intel Corp’s share price has declined about 23% since Mr. Lip-Pu Tan took office.

7. SMIC (981.HK): 2Q25 Results in Line; 3Q25 May Offer Mild Upside, but GM Is Expected to Be Flattish.

- Semiconductor Manufacturing International Corp (SMIC) (981 HK) reported in-line 2Q25 results, while its 3Q25 guidance appears somewhat cautious, particularly in terms of gross margin.

- The Americas continued to contribute a low-teens percentage to revenue, accounting for 12.9% in 2Q25, while China and Eurasia comprised the remaining majority.

- Our top questions for the upcoming SMIC’s 3Q25 earnings conference call.

8. Novatek (3034.TT): 3Q25 Outlook Is Expected; Weaker Demand from China Due to Subsidy Tapering.

- 3Q25 Outlook & Guidance- Revenue: NT$23.7–24.7bn( down 9.5~5.7% QoQ); Gross Margin: 34–37%; Operating Margin: 15–18%; USD/TWD Assumption: 29.5

- Weaker demand from China due to subsidy tapering in 3Q25, but seasonal stocking in non-China markets.

- 2025 foldable penetration estimated at ~1.6% (~19mn units); Large foldables: higher internal display resolution and ASP; OLED TDDI advantage: fewer components, more space-efficient, enabling thinner phones.

9. Novatek (3034.TT): FX Impact Persists; 3Q25 May Be a Down Quarter.

- We expect Novatek Microelectronics Corp (3034 TT)‘s 3Q25 might be decline 5-10% QoQ, reflecting 2H25 US tariffs impacts and Chinese opponent’s competition.

- The Foldable handset may be indicated a new era to come, and we believe Novatek Microelectronics Corp (3034 TT) shall be one of the DDIC winners.

- The stock price of Novatek Microelectronics Corp (3034 TT) is long staying with NT$450~650 since the beginning of 2024, and the current price is at the relative low point.

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

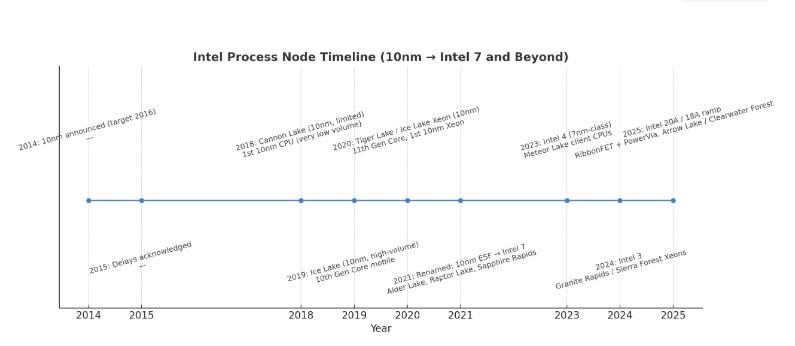

1. Intel (INTC.US): 18A May Have Been Too Rushed; Now All Hopes Rest on 14A.

- On July 24, chip giant Intel announced that its latest 18A advanced process is progressing smoothly. However, the next-generation 14A process will be developed “based on confirmed customer commitments.”

- Apple (AAPL US) adopt Intel’s 14A process for its future M-series chips, while NVIDIA Corp (NVDA US) is expected to use the same process for its entry-level gaming GPUs.

- U.S. President Trump is imposing tariffs on countries around the world, which is indirectly pressuring some manufacturers to accelerate the establishment of U.S.-based production facilities.

2. Taiwan Dual-Listings Monitor: TSMC ADR Premium Remaining Unusually High; UMC & ASE Headroom Changes

- TSMC: +26.3% Premium; Opportunity to Go Short the ADR Premium

- UMC: -1.2% Discount; ADR Headroom Falls Yet Again by a Significant Amount

- ASE: +0.7% Premium; Opportunity to Go Long the ADR Premium — ADR Headroom Has First Change in a Long Time

3. Microsoft FYQ425. Who Says Elephants Can’t Dance?

- Q425 revenues of $76.4 billion, up 5.5% QoQ, 18% YoY and handily beating guidance of $73.8 billion.

- Azure surpassed $75 billion in revenue in FY25, up 34% YoY, driven by growth across all workloads.

- Contracted backlog grew by $53 billion QoQ to reach $368 billion. Wow!

4. Yageo’s AI-Driven Momentum and Strategic Expansion Through Shibaura Acquisition

- 2Q25 Results Summary: Reports Broad-Based Growth with Specialty Margin Strength

- Yageo Inventory Recovery Marks a Demand-Led Inflection for Hardware Components

- Update on Shibaura Acquisition: Still on Track, Strategic Synergy in Focus

5. Taiwan Tech Weekly: Mediatek Reportedly Bests Broadcom for Meta Custom Chip Win; Semi Key Indicators

- MediaTek Reportedly Wins Meta’s 2nm AI Chip Order Over Broadcom

- Memory Monitor: SK Hynix Vs. Micron — Different Speeds & Focus, Same Structural Shift

- Semi Key Indicators Q2 2025: PC, Smartphone Unit Shipments, Global Semi & WFE Sales All Looking Good

6. Intel Q225. GM Obfuscation, Red Flags & 14A Now Officially A Risk Factor

- Intel reported Q225 revenues of $12.9 billion, up $200 million QoQ, flat YoY but $1.1 billion above the guided midpoint. After that revenue beat, things went downhill from there.

- CEO Lip Bu Tan said he will review and approve all future company product designs prior to tape out. Sounds like a vote of no confidence in the design team.

- Intel’s 10 Q now lists the possibility of pausing or abandoning 14A as a risk factor with doomsday details about the implications for the company

7. ASEH (3711.TT): FX Impact; AI Gains Attention; 3Q25 Grows, but GM and OPM Decline QoQ.

- 3Q25 guidance (Assuming US$1 = NT$29.2.): Consolidated US$ revenue: +12-14% QoQ; NT$ revenue: +6-8% QoQ; Gross margin: -1 to -1.2ppts QoQ; OPM: -0.1 to -0.3ppts QoQ.

- Still keep US$1bn advanced packaging guidance despite AI boom (TSMC revised up).

- Long-Term success definition for ASE: Transition from OSAT model to foundry-aligned scale.

8. Vanguard (5347.TT): FX Impact; Mild Recovery, Slightly Better Than 3Q25 Preview.

- 3Q25 Outlook (based on USD/TWD = 28.7): Wafer Shipments: +7–9% QoQ; ASP: +1–3% QoQ; Gross Margin: 25–27%.

- Revenue Mix (Industrial, Auto, 3C): Industrial + Automotive: 40%+ (majority industrial; automotive in teens) ; Communication & Computing: 20%+ each ; Consumer: 10%+.

- 2025 Dividend Policy : Will maintains NT$4.5 per share dividend.

9. Hon Hai(2317.TT): Form Strategic Alliance Via Share Swap with TECO (1504) For Global AI Data Center

- Hon Hai Precision Industry (2317 TT) and Teco Electric & Machinery (1504 TT) held a joint press conference this afternoon to announce the formation of alliance through a share swap.

- Teco (1504) TT and Hon Hai (2317 TT) stated their target markets extend beyond Taiwan and Asia, to include substantial business opportunities in the U.S. and the Middle East.

- Foxconn Chairman Mr. Young Liu also noted that as AI data centers scale up rapidly and demand surges, modular design is increasingly favored.

10. Tokyo Electron (8035 JP): Why the Big Downward Revision?

- Tokyo Electron’s share price dropped 18% on Friday following the announcement of weak Q1 results and a huge downward revision to H2 FY Mar-26 guidance.

- Push-Outs and/or cancellations of orders due to the uncertainty caused by President Trump apparently caught managment by surprise. Costs also rising as management ramps up capex and R&D.

- Impact of Trump’s yet-to-be-announced tariffs on semiconductors is still unknown, but 15% base rate on Japan already a negative.

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Taiwan Tech Weekly: TSMC Preparing 5x 2nm Ramp into 2027; Altman ‘Jokes’ About Buying 100x More GPUs

- TSMC’s Most Advanced Node — 5x Growth to 200K Wafers a Month? Upcoming 2nm Node Capacity Ramp Could Be Much Bigger Than Many Think

- OpenAI’s Sam Altman ‘Jokes’ About Owning US$3 Trillion Worth of GPUs One Day…

- AI PC Delay — Nvidia-MediaTek Push AI PC Chip Launch to 2026

2. Semi Key Indicators Q2 2025: PC, Smartphone Unit Shipments, Global Semi & WFE Sales All Looking Good

- According to Gartner, PC unit shipments increased 4.1% YoY in Q225 to reach 63.2 million

- According to IDC, smartphone unit shipments grew 1% YoY in the second quarter, reaching 295.2 million units

- Global semi sales were up 20% YoY in May while SEMI now expects YoY growth in WFE spending of 7.5% in 2025 and a further 10% in 2026

This weekly newsletter pulls together summaries of the top ten most-read Insights across Tech Hardware and Semiconductor on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. TSMC Q225. Surfing The AI Tidal Wave With Style

- TSMC reported Q225 revenues of $30.1 billion, up 44% YoY, up 17.8% QoQ and handily beating the high end of the $29.2 billion guidance.

- Full year 2025 guidance raised to 30% YoY growth, and that may still not be enough

- Resumption of H20 sales to China not yet baked into forecast, an army of ex Intel employees coming on the job market & potential Fx reversal are all possible tailwinds

2. TSMC 2Q25 Takeways: Undervalued Op Leverage and Capacity Strain Setting Up 2026 N2 Growth Suprise

- TSMC Beats, Raises, and Confirms AI Ramp Is Real, Despite FX Drag

- Conclusion — Maintain Structural Long View, 2026 Growth Likely Underappreciated

- TSMC ADR Premium Rebounds to 23.6% — US Investor Positioning Skewed Toward TSMC’s Unique AI Exposure

3. TSMC (2330.TT; TSM.US): FX Could Make an Impact; Full Year USD Revenue Raised to ~30% YoY.

- 3Q25 Guidance: Revenue: US$31.8–33.0 billion (approx. 8% QoQ growth); Gross Margin: 55.5–57.5%; Operating Margin: 45.5–47.5%.

- Despite FX headwinds, TSMC aims to maintain gross margin ≥ 53%

- Driven by strong demand in AI (including sovereign AI) and HPC; Full-year USD revenue growth outlook raised to ~30% YoY.

4. Taiwan Dual-Listings Monitor: TSMC Results Ahead; ASE Historically Rare Discount

- TSMC: +20.6% Premium; FY2Q25 Results This Week a Key Catalyst

- UMC: 0.0% Premium (Parity); Wait for More Extreme Levels Before Going Long or Short

- ASE: -0.8% Discount; Historically Rare Discount, Long the ADR Spread

5. ASML Q225 Earnings. Solid Results, Forecasting 15% Growth In 2025, Down 7% In Pre Market. But Why?

- ASML today reported second quarter revenues of €7.7 billion, bang at the top of the guided range, flat QoQ and up 23% YoY

- Guided 2025 at 15% growth (~€35 billion), a big step up in confidence from the €30-€35 billion range given last quarter

- Comments regarding uncertainty about 2026 outlook and tariff impacts likely led to the >7% sell off currently happening in pre-market trading.

6. Taiwan Tech Weekly: Intel Tapes Out New Chips at TSMC – What It Means; PC Demand Growth in Focus

- Intel Tapes Out New PC Chips on TSMC 2nm — Dual-Node Nova Lake Strategy Shows Dependence on TSMC… and Value of UMC for INTC in the Long-Term

- DRAM Memory Outlook — Nanya Results See Non-AI DRAM Demand Rebound; DDR4 Shortage Tightens, Expects Continued Strength in 2H25

- PC 2Q25: 6-7% Unit Growth YoY Is Pretty Good. 2025 Looks like a 5-6% Growth Year

7. Intel Layoffs Finally Kick Off With A Chaotic Start In Oregon

- Despite initially WARNing of 529 job cuts in Oregon, the actual number turned out to be 2,392

- Only 9% of the Oregon cuts are in management positions

- Huge cuts in technical employees across the board with a total of thirty Principal Engineers losing their jobs in Oregon alone.

8. TechChain Insights: Kinik – The Hidden Enabler Behind TSMC’s Sub-2nm Push

- We Engaged with Kinik Recently to Get Insight on Activity Strength for TSMC’s Expansion into Nodes 2nm and Below

- Diamond Tooling: Quietly Powering Advanced Logic; Kinik Recently Running at Max Capacity for Key DBU Business Segment… also at 100% for SBU Segment

- Takeaways — Kinik as a Concentrated Play on Advanced Node Transitions… Also, We Believe Signs Remain Positive for TSMC’s Recent Activity Momentum