This weekly newsletter pulls together summaries of the top ten most-read Insights across Event-Driven and Index Rebalance on Smartkarma.

Receive this weekly newsletter keeping 45k+ investors in the loop

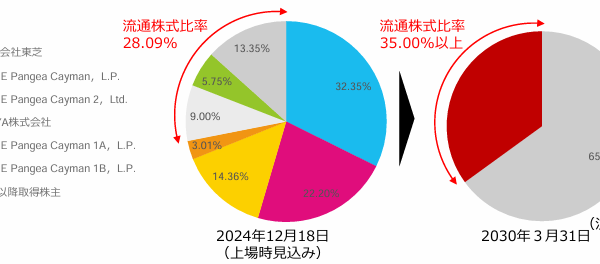

1. Index Treatment of Sony (6758 JP)’s Spinoff of the Financial Services Business

- For each share of Sony Corp (6758 JP), shareholders will receive 1 share of Sony Financial Group. Ex-date for the dividend in-kind is 29 September.

- The Nikkei has started a market consultation on treatment of the spinoff in the Nikkei225 and that means the dividend in-kind will not be included in the Dividend Point Index.

- There will be some selling in SFGI from passive trackers and the company will buy back some stock following listing. Details of the buyback have not been announced yet.

2. Foshan Haitian Flavouring & Food (3288 HK): Offering Details & Index Inclusion

- Foshan Haitian Flavouring & Food (603288 CH)‘s global offering opens today and the raise could reach up to US$1.5bn if the offer-size adjustment option and the overallotment option are exercised.

- There is a large allocation to cornerstone investors. The discount of around 22% to the A-shares is attractive given the recent trend for Midea (300 HK) and CATL (3750 HK).

- The H-shares could be added to a global index and the FXI ETF in December. Inclusion in the HSCI should be in September and Southbound Stock Connect in July.

3. [Japan M&A] Carlyle Deal for TRYT (9164) – Great Exit for Speculators as HR Co Targets Are Desirable

- In early February, articles suggesting the PE owner of TRYT (9164 JP) wanted to cash out. Performance post-IPO had been bad. Catching up to the IPO price would be tough.

- But a second round of bidding came about, so the stock went limit up. Then it settled in the ¥480 range for three weeks. Then started to climb.

- Now the company and its PE firm owner have announced a sale to a new PE Firm at ¥880/share. This is below IPO Price but it will get done.

4. Toyota Industries (6201 JP): Thoughts on Intrinsic Value

- Several investors have sharply criticised Toyota Industries (6201 JP)’s preconditional tender offer from Toyota Fudosan. Oasis is pushing for a higher offer.

- The offer has several issues that are detrimental to minorities’ interests. The key grievance is that it is below TICO’s intrinsic value.

- Due to TICO’s varied business units, SoTP valuation is the most appropriate methodology. My analysis suggests a base case intrinsic value of around JPY19,000.

5. [Japan M&A] Private Co Takeout of Fuji Corp (7605 JP) – A Done Deal

- The long-term major owner now chairman is getting out. The company was shopped. And bought. And this is the deal. ¥2,830 which is about 5.7x this year’s EBITDA.

- It could have been done a bit better, but irrevocables are 48.5% out of the 50.01% minimum and other directors get this past the minimum hurdle.

- Transparency is lacking but it is an all-time high and you can’t do much about it.

6. Virgin Australia (VGN AU): Touch & Go for Index Inclusion

- Virgin Australia Holdings (VGN AU) is looking to raise A$685m in a secondary offering, valuing the company at A$2.27bn. The stock is expected to start trading on 24 June.

- Bain Capital and management are escrowed on their shares till early 2026. There is no escrow for Qatar Airways, but they have indicated that their shareholding is strategic.

- Virgin Australia Holdings (VGN AU) could be added to the S&P/ASX 300 Index in September and there could be global index inclusions in November and December.

7. Zhejiang Sanhua Intelligent Controls (2050 HK): Big Raise Supported by Cornerstones

- Zhejiang Sanhua Intellignt Controls Co. (002050 CH)‘s global offering opens today and the raise could reach up to US$1.4bn if the offer-size adjustment option and the overallotment option are exercised.

- There is a large allocation to cornerstone investors. The discount of around 22.7% to the A-shares is attractive given the recent trend for Midea (300 HK) and CATL (3750 HK).

- The H-shares should be added to Southbound Stock Connect in July, to the HSCI in September, and to a global index in December.

8. Merger Arb Mondays (09 June) – Mayne, Tam Jai, OneConnect, Toyota Industries, Makino, Fuji Corp

- We summarise the latest spreads and newsflow of merger arb situations we cover across Hong Kong, Australia, New Zealand, Singapore, Japan, Indonesia, Malaysia, Philippines, Thailand and Chinese ADRs.

- Highest spreads: Mayne Pharma (MYX AU), Insignia Financial (IFL AU), Fuji Corp (7605 JP), ENN Energy (2688 HK), Smartpay Holdings (SPY NZ), Seven & I Holdings (3382 JP).

- Lowest spreads: Bright Smart Securities And (1428 HK), Toyota Industries (6201 JP), Dada Nexus (DADA US), Avjennings Ltd (AVJ AU), Nissin Corp (9066 JP), Torii Pharmaceutical (4551 JP).

9. [Japan M&A] Hino & Mitsubishi-Fuso Truck to Join; Bagholding Ugly for Minorities, and a Re-IPO

- On the 10th of June, Toyota Motor (7203 JP) subsidiary Hino Motors Ltd (7205 JP) and Mitsubishi-Fuso Truck & Bus Company announced their long-awaited integration plans. We have a deal.

- An agreement was signed in 2023, but Hino got in big trouble for falsifying testing data on gasoline engine emissions/efficiency. Hino took a hit in 2023, then 2025. Talks advanced.

- The deal announced suggests Toyota has thrown itself and Hino minorities under the proverbial Fuso bus. It’s VERY odd. But… it deserves a look because 2026 will see a re-IPO.

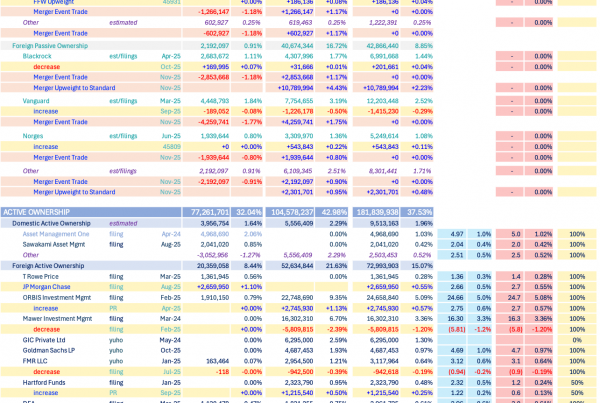

10. A/H Premium Tracker (To 6 June 2025): Narrow Premia Hs Worst Performers, BYD Relents

- AH spreads are slightly narrower. BANKS, INSURERS, BROKERS, INDUSTRIALS, PHARMA and UTILITIES see significant H-share outperformance vs their A pairs. TECH, CONSUMER, ENERGY mixed to worse.

- Ongoing skew on H-vs-A performance this week. Those trading AH Premium <20% saw H outperform sharply but those with H Premia contracted. Quiddity Portfolio alpha trending strongly.

- The data tables below update on a daily basis in the Tools section of Smartkarma. The SOUTHBOUND Flow Monitor and AH Monitor are both there free for SK readers.