As the colder winter weather is felt and the icy blast of industry tariff cuts continues to chill sentiment, we seek some respite (at least mentally) in the warmer climes of Okinawa. Okinawa Cellular is a unique company. It’s a small cap telecom network operator in Japan with a focus on the sub-tropical islands of Okinawa Prefecture. As part of the KDDI group, the company benefits from its parent’s economies of scale, but with its local presence, it also benefits from being the hometown hero.

Because the stock is relatively small, from an investment perspective it runs into liquidity constraints that the other telcos do not have, so it’s a different type of investment but one that we think is worth looking at. Over the past 12 months Okinawa Cellular’s stock has fallen by 12.3%, but over the past year the stock has delivered a return in the middle of its peer group and has outperformed the broad TOPIX by about 5.5%. Like most telcos, Okinawa Cellular is also ramping its dividend payments, and the current yield is about 3.5%.

Low correlation to the Thai market, low correlation with Western stock markets, and cheap on a PE basis relative to its sector

Stable cash flow from new contract for FGEN’s San Gabriel plant to sell its entire capacity of 414 MW to Meralco Manila Electric Company (MER PM) until 2024

Geothermal-energy producer EDC has been delisted through a share buyback tender offer, FGEN to benefit from higher equity stake (47% vs 42%) and more control over the firm to implement longer-term strategies

Trades at discount to ASEAN Utilities at 19CE* 6.5x PE and offers much better EPS growth

Risks: Facility breakdowns, uncertainty regarding plans for LNG facility

Right before Christmas, the Ministry of Finance confirms that both Thanachart and KTB were in talks to merge with TMB. We note that:

Considering that KTB’s earlier courtship failed once, it is more likely, but by no means guaranteed, for the deal with Thanachart to happen.

A deal with Thanachart would leave TMB as the acquirer rather than the target. Thanachart’s management has better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than BAY and not really change the bank rankings, but it would give TMB a bigger presence in asset management and hire-purchase finance and an re-entry into the securities business.

FBN Holdings Plc (FBNH NL) is the oldest and second-largest bank in Nigeria with a market share of 14% of domestic loans.

FBN’s solid franchise provides robust revenue generation capacity (especially in e-business and insurance) plus a solid and cheap funding base complemented by a strong liquidity profile. The Group’s solid funding base of low cost retail deposits, mainly CASA, underpins one of the most competitive in the sector.

Under new management, FBN is focused on a legacy asset quality clean-up and enhancing risk controls. The franchise has exhibited resilience in the face of system-wide asset quality problems, related to some extent to the concentration of oil/gas exposures. Moving forward, profitability can strengthen with improving asset quality though the recent plunge in oil prices represents a threat to this de-risking process. A plus point is the vibrant income streams from e-business and insurance growth drivers.

The operating environment in Nigerian remains challenging: while the country has emerged from a recession, vulnerabilities remain. Lower oil prices, tighter external market conditions, heightened security issues, and delayed policy responses are the main downside risks. The recent fall in oil prices is a concern given Nigeria’s dependency on the commodity and its knock-on effect to the hydrocarbon-exposed Banking System. Although access to foreign currency has eased, due to FX reforms, many borrowers retain limited capacity to service obligations and there are modest opportunities for banks to grow their loan portfolios.

FBN is thus somewhat of a contrarian call given the weakness in the oil market. But one should buy a hydrocarbon “play” when prices are low, not high. Shares trade at a 60% discount to Book Value and stand on a low Mkt Cap./Deposits rating of 8%, far below the global and EM median. FBN commands a dividend-adjusted PEG of 1.3x. Dividend and earnings yields are 3.3% and 15%, respectively. A quintile 1 PH Score™ of 7.7 captures the valuation dynamic while metric change is satisfactory. Combining franchise valuation and PH Score™, FBN stands in the top quintile of opportunity globally. The asset quality position and interrelated lower profitability vis-a-vis peers is a reason behind FBN’s lower credit rating and relatively low valuation. We are somewhat sceptical that FBN’s underlying creditworthiness and valuation are efficiently evaluated versus more popular counterparts.

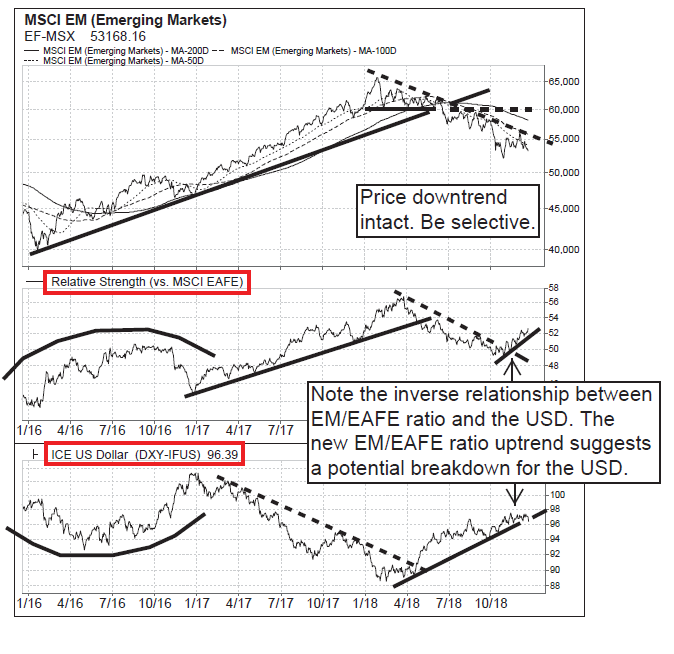

Relative strength for MSCI EM is bottoming vs. MSCI EAFE despite continued global equity market weakness. Although the MSCI EM’s price index remains in a downtrend, we are seeing signs of outperformance ona a relative strength basis and would add incremental exposure. In this report we highlight attractive and actionable themes within EM.

Tracking Traffic/Containers & Air Cargo is the hub for all of our research on container shipping and air cargo, featuring analysis of monthly industry data, notes from our conversations with industry participants, and links to recent company and thematic pieces.

Tracking Traffic/Containers & Air Cargo aims to highlight changes to existing trends, relationships, and views affecting the leading Asian companies in these two sectors. This month’s note includes data from about twenty different sources.

In this issue readers will find:

An analysis of November container shipping rates, which our index suggests increased by over 20% Y/Y. We concede that our index skews toward volatile spot rates rather than contract rates, but we suspect higher average container rates in Q418, combined with moderating fuel prices, will result in surprisingly strong earnings for the quarter.

A look at November air cargo activity and air cargo pricing, which diverged. The volume of air cargo handled by the five airlines we track declined slightly (-0.1% Y/Y) but some of those carriers reported sharply higher yields (circa +10% Y/Y), due to limited capacity expansion in the region.

Some good news: fuel prices have continued to moderate. Bunker climbed by just 5.1% Y/Y as of mid-December, and jet fuel prices have fallen about 11% Y/Y. Given firm container rates and air cargo pricing, the drop in fuel prices bodes well for Q418 margins, though it’s unclear whether such gains are sustainable.

Although slowing demand growth is unlikely to generate impressive top-line improvements, firmer pricing combined with lower fuel costs should support an ongoing improvement in profitability for container carriers and air cargo operations in the near-term. We believe many investors remain too pessimistic regarding near-term earnings for container carriers and airlines.

Tracking Traffic/Chinese Express & Logistics is the hub for our research on China’s express parcels and logistics sectors. Tracking Traffic/Chinese Express & Logistics features analysis of monthly Chinese express and logistics data, notes from our conversations with industry players, and links to company and thematic notes.

This month’s issue covers the following topics:

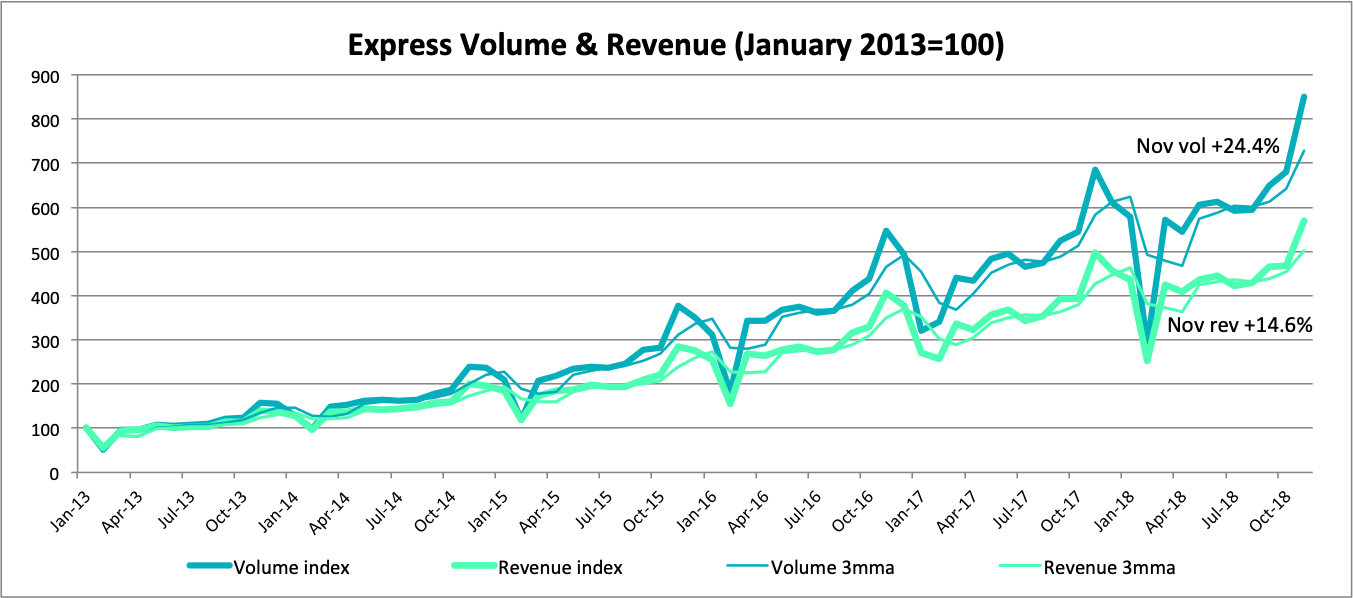

November express parcel pricing remained weak. Average pricing per express parcel fell by 7.8% Y/Y to just 11.06 RMB per piece. November’s average price represents a new all-time low for the industry, and November’s Y/Y decline was the steepest monthly decline in over two years (excluding Lunar New Year months, which tend to be distorted by the timing of the holiday).

Express parcel revenue growth dipped below 15% last month. Weak per-parcel pricing pulled express sector Y/Y revenue growth down to just 14.6% in November, the worst on record (again excluding distorted Lunar New Year comparisons). Chinese e-commerce demand has slowed and we suspect ‘O2O’ initiatives, under which online purchases are fulfilled via local stores, are also undermining express demand growth.

Intra-city pricing (ie, local delivery) remains firm relative to inter-city. Relative to weak inter-city express pricing (where ZTO Express (ZTO US) and the other listed express companies compete), pricing for local, intra-city express deliveries remained firm. In the first 11 months of 2018, express pricing rose 1.7% Y/Y versus a -2.9% decline in inter-city shipments (international pricing fell sharply, -14.5% Y/Y). Relatively firm pricing on local shipments may make it hard for local food delivery companies like Meituan Dianping (3690 HK) and Alibaba Group Holding (BABA US) ‘s ele.me to beat down unit operating costs.

Underlying domestic transport demand held up well again in November. Although demand for speedy, relatively expensive express service (and air freight) appears to be moderating, demand for rail and highway freight transport has held up well. The relative strength of rail and water transport (slow, cheap, industry-facing) versus express and air freight (fast, expensive, consumer-oriented) suggests a couple of things: a) upstream industrial activity is stronger than downstream retail activity and b) the people in charge of paying freight are shifting to cheaper modes of transport when possible.

We retain a negative view of China’s express industry’s fundamentals: demand growth is slowing and pricing appears to be falling faster than costs can be cut. Overall domestic transportation demand, however, remains solid and shows no signs of slowing.

Horiba combines high gearing to semiconductor capital spending with a large and growing automotive test business characterized by upward trending but uneven profitability. At ¥4,545 (Friday, December 21, closing price), its share price has dropped by 53% from an all-time high of ¥9,590 reached last May. Falling demand for semiconductor production equipment and a downward revision to FY Dec-18 sales and profit guidance announced in November appear to be largely in the price.

The downward revision, which cut projected full-year operating profit growth from 15.5% to 2.5%, followed a 22.2% year-on-year decline in operating profit in 3Q and implies a similar rate of decline in 4Q. The weakness is concentrated in Semiconductor Equipment and Automotive Test, the former due to a cyclical downturn in overall demand, the latter due to M&A-related and other one-time expenses. New Automotive Test orders continued to outpace sales, leading to a 9.5% increase in the order backlog during 3Q.

Automotive Test sales and profits should rise next year, while semiconductor equipment sales and profits seem likely to bottom out. In a report issued on December 17, SEMI (the semiconductor equipment and materials industry organization) forecasts a further decline in wafer fab equipment sales in 1H of 2019, followed by recovery in 2H. Other industry sources we talked to before the report was issued had similar views.

This scenario could fall apart due to general economic weakness, American attempts to stifle China’s semiconductor industry, or both. On December 21, Reuters reported that Foxconn “…is in the final stages of talks with the local government of the Chinese city of Zhuhai to build a chip plant there with a total investment of about $9 billion… most of which would be shouldered by the Zhuhai government through subsidies and tax breaks…” This looks like a perfect target for the Americans, but whether or not they will notice or care remains to be seen.

Horiba is now selling at 9.6x our EPS estimate for this fiscal year, 13.4x our estimate for next year and 12.1x our estimate for FY Dec-20. These and other projected valuations are near the bottom of their 5-year historical ranges. If the Semiconductor Equipment division does not recover in 2H of 2019, historical data suggest that its operating profit could drop by 70% rather than the 47% we are now forecasting, resulting in a P/E ratio of 17x. Nevertheless, it is time to start considering when and at what price to buy Horiba.

Horiba is a diversified Japanese maker of precision and analytical devices and systems with a significant presence in the global markets for automotive test, industrial process and environmental analysis, hematology, semiconductor production equipment and scientific instruments. It is by far the world’s leading producer of automotive emission measurement systems (EMS), having supplied about 80% of the installed base worldwide, and also the world’s top manufacturer of mass flow controllers for the semiconductor industry, with an estimated global market share of nearly 60%.

Relative strength for MSCI EM is bottoming vs. MSCI EAFE despite continued global equity market weakness. Although the MSCI EM’s price index remains in a downtrend, we are seeing signs of outperformance ona a relative strength basis and would add incremental exposure. In this report we highlight attractive and actionable themes within EM.

Improving asset turnover, good risk adjusted price momentum, and relatively strong analyst recommendations relative to its sector

Larger distribution channel through acquisition of DNA Retail Link to add 95 more stores to current 518 stores

New mobile product launches in 4Q18 and COM7’s focus on high margin products, such as Android smartphones, should support high earnings growth which was up 56% YoY in 3Q18

Attractive at a 19CE* PEG of 0.9 versus ASEAN sector at a PEG of 2.7

Risks: Lower-than-expected demand for new IT products, slower-than-expected store expansions

Tracking Traffic/Chinese Express & Logistics is the hub for our research on China’s express parcels and logistics sectors. Tracking Traffic/Chinese Express & Logistics features analysis of monthly Chinese express and logistics data, notes from our conversations with industry players, and links to company and thematic notes.

This month’s issue covers the following topics:

November express parcel pricing remained weak. Average pricing per express parcel fell by 7.8% Y/Y to just 11.06 RMB per piece. November’s average price represents a new all-time low for the industry, and November’s Y/Y decline was the steepest monthly decline in over two years (excluding Lunar New Year months, which tend to be distorted by the timing of the holiday).

Express parcel revenue growth dipped below 15% last month. Weak per-parcel pricing pulled express sector Y/Y revenue growth down to just 14.6% in November, the worst on record (again excluding distorted Lunar New Year comparisons). Chinese e-commerce demand has slowed and we suspect ‘O2O’ initiatives, under which online purchases are fulfilled via local stores, are also undermining express demand growth.

Intra-city pricing (ie, local delivery) remains firm relative to inter-city. Relative to weak inter-city express pricing (where ZTO Express (ZTO US) and the other listed express companies compete), pricing for local, intra-city express deliveries remained firm. In the first 11 months of 2018, express pricing rose 1.7% Y/Y versus a -2.9% decline in inter-city shipments (international pricing fell sharply, -14.5% Y/Y). Relatively firm pricing on local shipments may make it hard for local food delivery companies like Meituan Dianping (3690 HK) and Alibaba Group Holding (BABA US) ‘s ele.me to beat down unit operating costs.

Underlying domestic transport demand held up well again in November. Although demand for speedy, relatively expensive express service (and air freight) appears to be moderating, demand for rail and highway freight transport has held up well. The relative strength of rail and water transport (slow, cheap, industry-facing) versus express and air freight (fast, expensive, consumer-oriented) suggests a couple of things: a) upstream industrial activity is stronger than downstream retail activity and b) the people in charge of paying freight are shifting to cheaper modes of transport when possible.

We retain a negative view of China’s express industry’s fundamentals: demand growth is slowing and pricing appears to be falling faster than costs can be cut. Overall domestic transportation demand, however, remains solid and shows no signs of slowing.

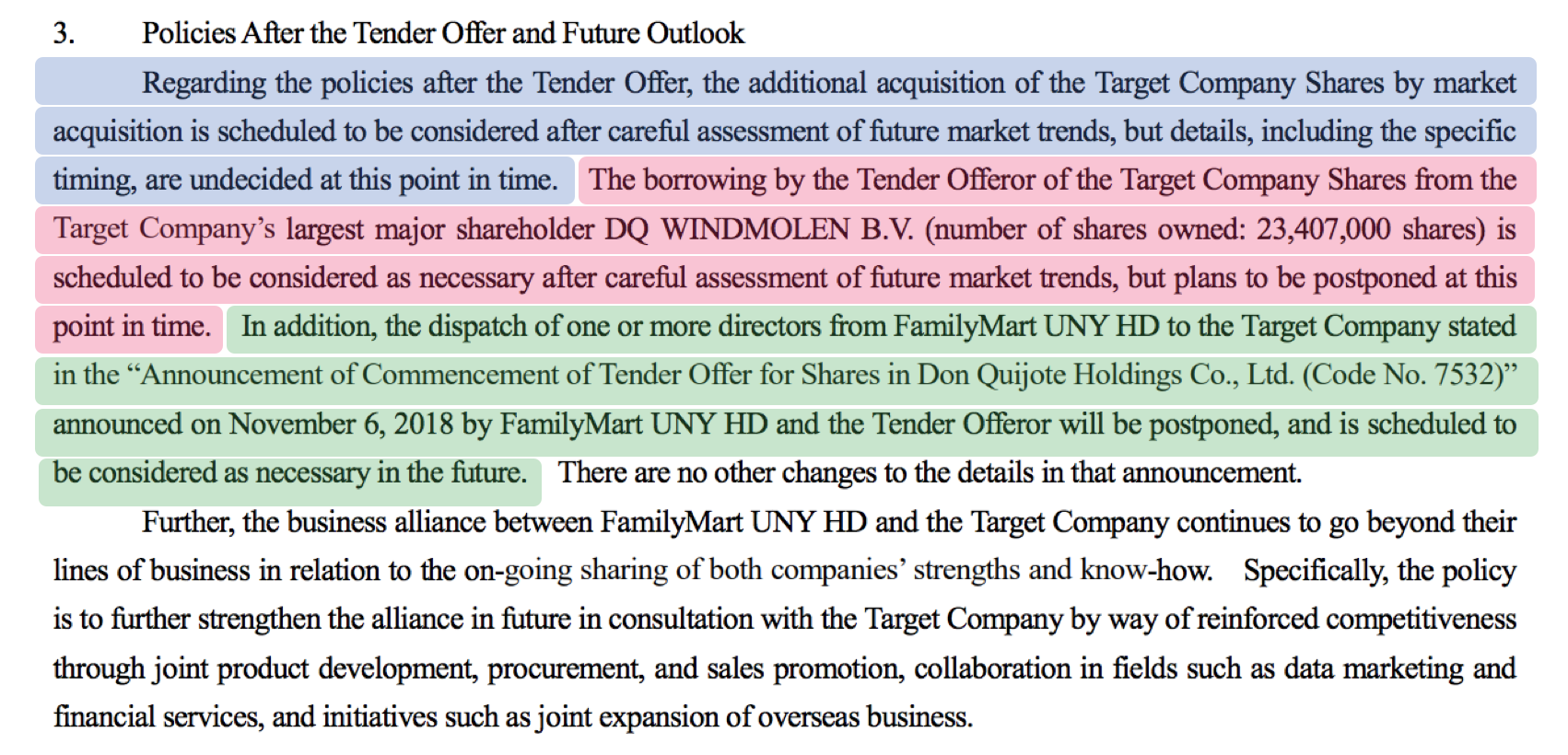

Recapping the original plan: when Familymart Uny Holdings (8028 JP)(“FM”) sold the remaining 60% of UNY to Don Quijote Holdings (7532 JP) (DQ), it entered into an agreement to buy 20+% in DQ, for one of two reasons; 1) a company wants to prove to the employees of a division being sold that they are maintaining a watchful eye over them, or (as is now evident) 2) the buyer wants to gain an equity method affiliate and the income from it (including the placeholder for frontrunner status to future capital events).

FM launched a Partial Tender Offer at a 20% premium to last in order to buy these shares, and in the MOU to launch the tender offer there was a clause which said that if FM did not reach the full 20%, it had made arrangements to borrow shares in order to get to 20% of the voting rights. And if FM did not manage to get to the full 20%, there was an agreement between DQ which allowed FM to buy shares in the market to get to a 20% (but not larger) position.

If FM managed to get the shares, it was going to buy from the weak hands. Growth stock managers don’t like selling growth stocks until the growth stops growing. DQ is still growing, and with UNY, DQ may grow faster than previously expected. The upshot is that everyone decided they’d stand pat – FM got nothing in the tender (0.08% of the total desired).

Shares in DQ could fall because of a lack of hard strategy announced by FM to buy all the shares at a higher price immediately. That shouldn’t be a big worry – it wasn’t going to happen.

Travis Lundy sees DQ having a performance skew which includes a “cushion of sorts” in the ¥5500-6600/share zone where he would expect FM to acquire shares. He does not see a cushion for the shares of FM, and expects them to be volatile.

It is possible this suspension is not in relation to a takeover, but a major sale of assets, for example, from the parent to the sub. This would make sense given the recent share purchase by HEC (completed in January this year), and the fact HE is playing catch-up to Dongfang Electric Corporation (1072 HK)& Shanghai Electric Group Company (2727 HK). Arguably, launching a takeover shortly after subscribing for more shares is unusual. Then again, when the two SOE railway behemoths CNR and CSR merged in 2015, a merger was disputed (at the time) when both were suspended on account of the fact CNR was only listed (on the HK exchange) in 2Q14.

HE has perennially traded at discount to net cash. As at its last traded price, the discount to net cash (using the 2018 interim figure of HK$12.4bn, or HK$7.27/share) was 65%.

“Fair” pricing to me would be something like the distribution of net cash to zero then taking over the company on PER. I simply don’t see this happening. And if it doesn’t, the fiduciary duty of independent directors will be tested/scrutinised if they recommend an offer to shareholders at any price less than the net cash/share of the company.

Reportedly Motherson has entered merger/acquisition talks withLeoni AG (LEO GR), a leading provider of cables and cable systems for the automotive sector and other industries. Motherson has made four acquisitions so far in this business segment with the latest being PKC in 2017.

Motherson has always aimed at strengthening this business area internationally, therefore the news about a merger with Leoni comes as no surprise and was mentioned as a potential acquisition target in LightStream Research‘s earlier insight Two More Acquisitions on the Way for Motherson Sumi.

Motherson has a strong balance sheet that could support this acquisition, although its ability to make further acquisitions in the short-to-medium term may be hampered – Leoni would be at the higher end of the price range for recent acquisitions. Should the acquisition go through, the company will be very well positioned to reach its US$18bn revenue target by 2020E, given that the combined revenue for FY2017 alone is ~US$13bn.

Currently, Motherson is trading at an FY1 EV/EBITDA of 10x, slightly above peers such as Mahindra Cie Automotive (MACA IN)(9x) and below peers such as Bosch Ltd (BOS IN) (25x). If the deal goes through, Motherson’s FY1 EV/EBITDA of ~12x would be at a slight premium to local players, but still reasonable compared to international players.

Kohlberg Kravis Roberts reduced its indicative offer to $3.40 from $3.77 on Thursday after sifting through MYOB’s books, with MYOB announcing:

Following completion of due diligence and finalisation of debt funding commitments, KKR has revised the offer price to $3.40 per share. … The board has informed KKR that it is not in a position to recommend the revised proposal, however it remains in discussions with KKR regarding its proposal. (my emphasis)

KKR’s revised non-binding proposal expired at 5pm on Friday, which came and went without any ASX announcement. Presumably, an announcement will be made before the market opens tomorrow (rendering this commentary redundant) with either MYOB grudgingly accepting the lower offer, or MYOB rejecting and KKR walking away (for now), or going hostile.

The Nikkei carried an article noting that the Japanese government’s FY2019 budget currently being formed proposes a sale of ¥160bn of shares in NTT to help fund any revenue impact from the upcoming consumption tax rate hike from 8% to 10% next October. The article helpfully notes that they plan on selling when NTT is buying back shares. One of the longstanding features of buybacks for NTT is that NTT is subject to the NTT Law which requires (for the moment) that the government hold at least one-third of the shares outstanding in NTT.

Travis estimates NTT has ~1.95bn shares outstanding, or ~1.917bn shares outstanding ex-Treasury shares, after recent buybacks. If NTT cancelled the shares it has bought back prior to buying back shares from the government, this would allow NTT to buy back 59mm shares from the government (assuming those shares are also cancelled). If it did not, it would mean NTT could only buy back about 42-43mm shares. 59mm shares backs out ¥250bn; 43mm shares at a 10% discount would be ¥180bn. That means there is about 10% leeway in stock price to buy ¥160bn from the government IF shares repurchased under the current buyback are not cancelled.

But that also means that there would be no more buybacks from the government after that until the company buys back more shares from the market. If the company wanted to buy back another ¥200bn from the government, ceteris paribus it would have to buy back something like ¥400-450bn first from the market in order to reduce the denominator. Travis concludes there is still more on-market buying to do.

At an NTT/ NTT Docomo Inc (9437 JP) ratio of 1.80x, buybacks coming, expected ongoing strong dividend policy (and lots of headroom to do so, unlike perhaps Softbank Corp (9434 JP)), and investor suspicion of what comes next for Docomo, NTT is the home of the cashflow.

The IPO of Softbank Corp and the Merger of Takeda and Shire Pharmaceuticals create significant changes in TOPIX, MSCI, and FTSE because of the addition of roughly ¥5tn of “new” market capitalization in major Japan indices. Pure passive investors have something like ¥1.35tn of Softbank Corp and Takeda Pharmaceutical to buy.

However, after Travis’ initial note (Softbank Corp, Takeda, and Newton’s Three Laws of Motion), TSE unhelpfully changed their mind on timing (for Takeda) based on an unhelpful change by the LSE. With the changes at FTSE and now TOPIX and JPX Nikkei 400, we no longer have quite the same clarity of forces on the bodies, and therefore less clarity on the resulting motion. The LSE’s announced market change appears to have led the MSCI to change its deletion date for Shire as well, now also (along with FTSE) deleting Shire at the close of the 21st. The new schedule is:

Index Deletion

Shire (shs mm)

Index Inclusion

Takeda (shs mm)

Index Effect (US$ bn)

Net Delta (US$bn)

21 Dec

MSCI

-50

MSCI JP

+75

– $0.3bn

+$1.3bn

21 Dec

FTSE UK, All-Share,

-100-130

FTSE JP

+15

-$5.2bn+

– $2.1bn

rest of December – end of a pretty bad year for hedge funds, but illiquid

all of January

30 Jan

TOPIX

-$1.9bn

TOPIX, JPXN400

+60

+$2.1bn

+$2.1bn

30 Jan

TOPIX

-$3.5bn

TOPIX

Softbank

+$3.5bn

+$3.5bn

all of February

27 Feb

TOPIX, JPXN400

+60

+$2.1bn

+$2.1bn

It doesn’t change the amounts but a lot more time allows for more risk and preparation and there will no longer be any potential settlement issues on the TOPIX side. There is still the same amount of Takeda to buy in TOPIX and JPX Nikkei 400.

In principle, Travis would want to be long Takeda at the close of the year of 2018, but given the LSE and TSE changes there is less support to give and the payoff is substantially more distant.

Speciality steel maker Nisshin Steel (5413 JP)is slated to merge with parent company Nippon Steel & Sumitomo Metal (5401 JP)as of January 1, 2019. For that, Nisshin Steel will be delisted on December 26th (i.e. the last day of trading is the 25th) and that means the Nikkei Inc was obliged to choose a replacement for Nisshin Steel in the Nikkei 225 and other indices. On December 11th, the Nikkei Inc announcedItoham Yonekyu Holdings Inc (2296 JP) would take Nisshin’s place in the Nikkei 500 Index; announced that Japan Post Holdings (6178 JP) would join the Nikkei 300 Index; and announced thatDic Corp (4631 JP)would replace Nisshin Steel in the Nikkei Stock Average, better known as the Nikkei 225.

Nisshin Steel’s deletion is a nothing-burger.

The possibility of a DIC addition was well-flagged as early as May when sell-side brokers started compiling Annual and Ad Hoc Review lists for the Nikkei 225 changes to come in September and as a result of the Nisshin Steel merger. Travis would rather be long DIC than short DIC through the close of December 21st or probably December 25th.

YP appeared “cheap” back in April when I last discussed this Holdco, and is now cheaper, with its holding in KZ accounting for near-on 200% of its market cap. I can’t think of any other parent/subsidiary relationship – one which is essentially a single stock structure – with such a deep discount. Especially one where the stub ops operate in a similar space to that of the listed holding.

On the negative front, an investigation into YP’s Seokpo zinc smelter remains ongoing on account of perceived environmental transgressions. The Seokpo smelter is located in a national park on the Nakdong river. Wastewater containing above-legal limits of certain chemicals (fluoride and selenium) allegedly flowed downstream to residents, who are heavily reliant on this water.

YP’s stub and KZ are in the same business, but there are differences. YP does not have a balanced product mix as KZ does, with around 84% of its revenue coming from zinc-related production (for the 9M18 period), compared to 42.5% (on a revenue basis) for KZ, followed by lead (20.4%), silver (20.2%), and gold (7.6%).

However, YP and KZ remain inextricably intertwined and the current discount is unjustifiably steep. Just that YP’s liquidity, uncertainty on Seokpo, and lack of a near-term catalyst make for a difficult stub set-up.

A forgettable trading debut for Japan’s largest-ever IPO, with Softbank Corp,closing at ¥1,282/share, down from the IPO price of ¥1,500, and closing at ¥1,316/share on Friday, the same day as its FTSE inclusion.

At around 22% of NAV and 16% of GAV – by my calcs – Corp is a material % of Softbank Group (9984 JP). However as repeatedly seen when a conglomerate adds yet another listco to its stable (in Hong Kong, Wheelock & (20 HK)and Great Eagle Holdings (41 HK) spring to mind), a sustained narrowing in the holdco discount is often not the end result. Nor should it be. Softbank is effectively swapping shares for cash.

With seven stocks promoted/reassigned from TSE2, MOTHERS, and JASDAQ in November 2018 leading to the same seven stocks being included in TOPIX at the end of December, Travis tested 340+ TOPIX inclusions over the past five years to see what really happens around TOPIX inclusions?

If you own all but the smallest stocks (with a market cap of less than ¥15bn), odds are that, ON AVERAGE, they will underperform TOPIX from inclusion date or the day after, for many months.

The larger the market cap, the more marked the AVERAGE underperformance immediately following inclusion.

For names in the ¥25-50bn sweet spot of “large enough to be “small cap” with somebody paying attention to it”, outperformance vs underperformance in the next 10 days is a 47/53 proposition. That is a bigger risk. It may be data-idiosyncratic, but it is not clear.

In the case of the 7 names going into TOPIX at month-end this month, the averages would suggest one could still be long the four largest (at the time of Travis’ insight), but one would not want to be long the others; and one could sell long positions in all the names as of the close of the 27th or 28th and have it be an ex-ante expected net positive outcome vs TOPIX over the following 10-60 trading days.

CJ Corp (001040 KS) announced both Common and Pref will get 0.15 class B pref shares for each share they already own. This new class B pref is convertible to Common with a 10-year duration, and it provides an extra 2% of the face value to what Common gets. Price ratio wise, 1P is currently close to the 2Y mean. This stock dividend should push 1P up, as should CJ’s announcement it would pay a cash dividend. The current div yield difference is a historic high at 1.53%. (link to Sanghyun Park ‘s insight: CJ Corp Share Class: Huge Net Gain Difference Between Common & Pref from Stock Dividend)

LCY Chemical Corp (1704 TT). MOEA (Ministry of Economic Affairs) approval has now been received and LCY has applied for the delisting from the TWSE. The last trading day is the 23 Jan 2019 and the stock delists on the 30 Jan. The settlement is expected to take place mid-Feb.

Healthscope Ltd (HSO AU). In an ASX announcement on Friday Brookfield said: “based on its enquiries and financing discussions to date, it has no reason to believe it will not be willing and able to proceed with the proposal“. The exclusivity provisions have been extended to 18 January. Separately, Healthscope has also received correspondence from the BGH-AustralianSuper Consortium that it has indicated it is able to commence due diligence immediately. HSO’s board stated it will consider the correspondence. These are both positive developments.

CCASS

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Relative strength for MSCI EM is bottoming vs. MSCI EAFE despite continued global equity market weakness. Although the MSCI EM’s price index remains in a downtrend, we are seeing signs of outperformance ona a relative strength basis and would add incremental exposure. In this report we highlight attractive and actionable themes within EM.

Right before Christmas, the Ministry of Finance confirms that both Thanachart and KTB were in talks to merge with TMB. We note that:

Considering that KTB’s earlier courtship failed once, it is more likely, but by no means guaranteed, for the deal with Thanachart to happen.

A deal with Thanachart would leave TMB as the acquirer rather than the target. Thanachart’s management has better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than BAY and not really change the bank rankings, but it would give TMB a bigger presence in asset management and hire-purchase finance and an re-entry into the securities business.

In October, the Nikkei leaked and Familymart Uny Holdings (8028 JP) immediately thereafter announced that Familymart would sell the rest of its GMS (and financing) subsidiary UNY to Don Quijote Holdings (7532 JP) (which bought 40% of the company in 2017) and would conduct a Tender Offer later in 2018 at a 20% premium to the then-current price to buy a stake in Don Quijote of just over 20%. The Tender Offer was announced November 6th. Familymart had arranged to borrow shares it did not manage to buy in the tender so that at the next record date it will have 20% of the voting rights by hook or by crook.

Don Quijote shares jumped to the Tender Offer price the same day and then spent a day there before investors decided that the news and structure of the deal was better news for Don Quijote than Familymart had priced in.

Results of the Tender Offer have just been announced. Familymart had been trying to buy 32,108,700 shares for JPY 212 billion. They just missed. They got 0.08% of the total desired, or 24,721 shares for just over JPY 163 million.

THEY GOT NOTHING.

I expect Familymart had zero idea this would happen. I expect their bankers are surprised as well. They should not have been. They analysed this badly. There was a decent chance they would find it difficult to dislodge shares from owners.

“I couldn’t think of selling that stock.” “You couldn’t?” asked Elmer, beginning to look doubtful himself. It is a habit with most tip givers to be tip takers. “Why not?” And Elmer drew nearer. “Why, this is a bull market!” The old fellow said it as though he had given a long and detailed explanation.

Growth stock managers don’t like selling growth stocks until the growth stops growing. Don Quijote is still growing. And with UNY, Don Quijote may grow faster than previously expected.

The announcement at the end of the Tender Offer Results announcement is also VERY telling. There was a plan to make Don Quijote an equity-method affiliate by buying in the Tender Offer, buying in the market, or borrowing lots of shares. There was a plan for Familymart to appoint directors to DQ.

There was a clearly-available trading strategy based on that.

The new announcement puts that strategy into question. And Mr. Partridge might not be so inclined to call it a bull market. Since the launch of the deal, the markets have started the trip to Gehenna in a trug. From the one-month average prior to the Familymart bid news, Don Quijote is up 25%. Familymart is up 40%, the Nikkei 225 is down 10.7%, the TOPIX retail sector is down 5.5% but Familymart and Don Quijote have influenced that performance (without those two names, average performance is worse).

CJ Corp (001040 KS) announced a 0.15 stock dividend. CJ will issue a new class B pref. Both Common and Pref will get 0.15 class B pref shares for each share they already own. This new class B pref is convertible to Common with a 10 year duration. It gives an extra 2% of the face value to what Common gets. A total 4,226,513 new class B prefs will be issued.

CJ previously had two class B prefs. Based on the historic discount % of these two, 2P’s discount to Common on the listing day is estimated at 33%. There will be nearly 10% price dilution in both Common and 1P. There will be a 10+%p difference in gain per share. 1P’s dilution-adjusted net gain per share stands at 13.61%, whereas Common is only 0.66%.

Price ratio wise, 1P is in an undervalued territory. On a longer horizon, it is currently close to the 2Y mean. This stock dividend should push 1P further upward above the 2Y mean. CJ also said that it would give cash dividend. Current div yield difference is a historic high at 1.53%p. This should be another reason to push up 1P. I’d go long 1P and short Common at this point.

Just how will Harbin Electric Co Ltd H (1133 HK)‘s independent directors justify recommending an Offer to shareholders at a price which gave cash less cavalier than cash?

MYOB Group Ltd (MYO AU)‘s directors grudgingly yet understandably enter an agreed deal with KKR.

As previously discussed in Harbin Electric Expected To Be Privatised, Harbin Electric (HE) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption. The Offer price of $4.56/share, an 82.4% premium to last close, is bang in line with that paid by HEC in January this year for new domestic shares. The Offer price has been declared final.

Of note, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors (and the IFA) can justify recommending an Offer to shareholders at any price below the net cash/share, especially when the underlying business is profit-generating.

Dissension rights are available, however, there is no administrative guidance on the substantive as well as procedural rules as to how the “fair price” will be determined under PRC and HK Law.

Trading at a gross/annualised spread of 15%/28% assuming end-July completion, based on the average timeline for merger by absorption precedents. As HEC is only waiting for approval from independent H-shareholders suggests this transaction may complete earlier than precedents.

KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal. The Offer price assumes no full-year dividend is paid.

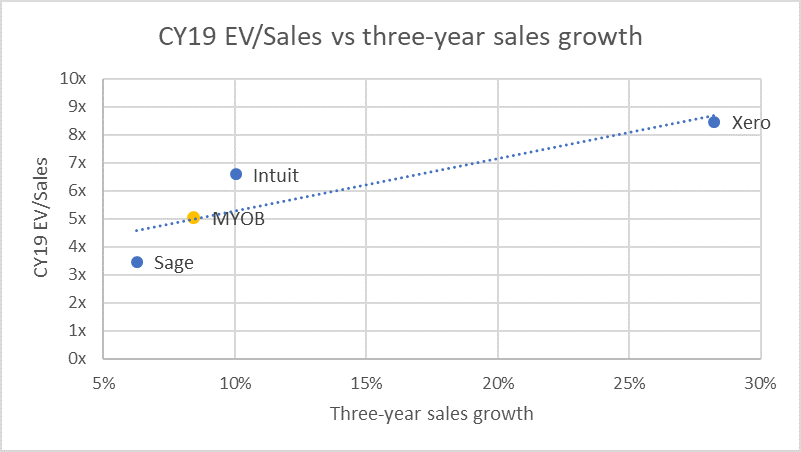

On balance, MYOB’s board has made the right decision to accept KKR’s reduced Offer. The argument that MYOB is a “known turnaround story” is challenged as cloud-based accounting software providers Xero Ltd (XRO AU)and Intuit Inc (INTU US) grab market share. This is also reflected in MYOB’s forecast 7% revenue growth in FY18 and follows a 10% decline in first-half profit, despite a 61% jump in online subscribers.

And there is justification for KKR’s lowering the Offer price: the ASX is down 10% since KKR’s initial tilt, the ASX technology index is off by ~14%, a basket of listed Aussie peers are down 17%, while Xero, the most comparable peer, is down ~20%. The Scheme Offer is at a ~27% premium to the estimated adjusted (for the ASX index) downside price of $2.68/share.

Bain was okay selling at $3.15/share to KKR and will be fine selling its remaining ~6.5% stake at $3.40. Presumably, MYOB sounded out the other major shareholders such as Fidelity, Yarra Funds Management, Vanguard etc as to their read on the revised $3.40 offer, before agreeing to the SIA with KKR.

If the markets avoid further declines, this deal will probably get up. If the markets rebound, the outcome is less assured. This Tuesday marks the beginning of a new year and a renewed mandate for investors to take risk, especially an agreed deal; but the current 5.3% annualised spread is tight.

The Ministry of Finance, the major shareholder of TMB, confirmed that both Krung Thai Bank Pub (KTB TB)and Thanachart Capital (TCAP TB)had engaged in merger talks with TMB. Considering an earlier KTB/TMB courtship failed, it is more likely, but by no means guaranteed, that the deal with Thanachart will happen. Bloomberg is also reporting that Thanachart and TMB want to do a deal before the next elections, which is less than two months away.

TMB is much bigger than Thanachart and therefore it may boil down to whether TMB wants to be the target or acquirer. In Athaporn Arayasantiparb, CFA‘s view, a deal with Thanachart would leave TMB as the acquirer rather than the target. But Thanachart’s management has a better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than Bank Of Ayudhya (BAY TB) and would not change the bank rankings; but it would give TMB a bigger presence in asset management, hire-purchase finance and a re-entry into the securities business.

Mando accounts for 45% of Halla’s NAV, which is currently trading at a 50% discount. Sanghyun Park believes the recent narrowing in the discount may be due to the hype attached to Mando-Hella Elec, which he believes is overdone; and recommends a short Holdco and long Mando. Using Sanghyun’s figures, I see the discount to NAV at 51%, 2STD above the 12-month average of ~47%.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

The accounting fraud issue had hammered the Celltrion duo nearly equally up until Dec 26. But last two days were different. Healthcare got hurt much more deeply. Celltrion fell only 2.41%, but Healthcare fell 11.52%.

The accounting issue is supposed to be equal to both. KOSPI move and merger are still alive to push up Healthcare. Local institutions and foreigners have bashed both pretty much equally in the last two days. This is another sign that it was more of a price divergence than a mean reversion.

The duo is now at 20D MA and also the yearly mean. I expect it to go substantially below the yearly mean on KOSPI move and merger expectations. A powerful downwardly mean adjusting force still seems to be in action. I’d long Healthcare and short Celltrion to exploit the latest price divergence.

Halla Holdings is falling nearly 5% today. Holdco said it’d give a ₩2,000 div per share. This is about 4.5% div yield at yesterday’s closing price. 5% drop today shouldn’t be much as an ex-dividend date price drop. Mando fell 5%. Mando was oversold relative to the other local auto stocks, particularly to Halla Holdings. They are still close to +1 σ on a 20D MA.

Mando-Hella Elec has been another reason behind Holdco’s valuation divergence against Mando lately. I believe Mando-Hella is being overhyped. Mando-Hella-caused divergence should no longer be effective. I expect ‘downwardly’ mean reversion from now on. I’d go short Holdco and long Mando at this point.

The Offer price of $4.56/share, an 82.4% premium to last close, has been declared final. The price corresponds to the subscription of 329mn domestic shares (~47.16% of the existing issued domestic shares and ~24.02% of the existing total issued shares) @$4.56/share by HEC in January this year.

Of greater significance, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors can justify recommending an Offer to shareholders at any price which gave cash less cavalier than cash.

Dissension rights are available, however, what constitutes a “fair price” under those rights, and the timing of the settlement under such rights, are not evident.

As all PRC approvals have been obtained, this transaction may complete earlier than prior mergers by absorption, which have taken 6-8 months from the initial announcement.

On 24 December, MYOB Group Ltd (MYO AU) announced that it entered into a scheme implementation agreement under which KKR will acquire MYOB at $3.40 per share, which is 10% lower than 2 November offer price of A$3.77. MYOB claims its decision to recommend KKR’s lower offer was based on current market uncertainty, long-term nature of its strategic growth plans and the go-shop provisions of the deal.

We believe that KKR’s revised offer is opportunistic, but MYOB’s shareholders are caught between a rock and a hard place. Shareholders can take a short-term view and grudgingly accept the revised offer. Alternatively, shareholders can take a long-term view by rejecting the offer and hope MYOB’s strategic growth plans and a market recovery can reverse the inevitable share price collapse.

Just how will Harbin Electric Co Ltd H (1133 HK)‘s independent directors justify recommending an Offer to shareholders at a price which gave cash less cavalier than cash?

MYOB Group Ltd (MYO AU)‘s directors grudgingly yet understandably enter an agreed deal with KKR.

As previously discussed in Harbin Electric Expected To Be Privatised, Harbin Electric (HE) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption. The Offer price of $4.56/share, an 82.4% premium to last close, is bang in line with that paid by HEC in January this year for new domestic shares. The Offer price has been declared final.

Of note, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors (and the IFA) can justify recommending an Offer to shareholders at any price below the net cash/share, especially when the underlying business is profit-generating.

Dissension rights are available, however, there is no administrative guidance on the substantive as well as procedural rules as to how the “fair price” will be determined under PRC and HK Law.

Trading at a gross/annualised spread of 15%/28% assuming end-July completion, based on the average timeline for merger by absorption precedents. As HEC is only waiting for approval from independent H-shareholders suggests this transaction may complete earlier than precedents.

KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal. The Offer price assumes no full-year dividend is paid.

On balance, MYOB’s board has made the right decision to accept KKR’s reduced Offer. The argument that MYOB is a “known turnaround story” is challenged as cloud-based accounting software providers Xero Ltd (XRO AU)and Intuit Inc (INTU US) grab market share. This is also reflected in MYOB’s forecast 7% revenue growth in FY18 and follows a 10% decline in first-half profit, despite a 61% jump in online subscribers.

And there is justification for KKR’s lowering the Offer price: the ASX is down 10% since KKR’s initial tilt, the ASX technology index is off by ~14%, a basket of listed Aussie peers are down 17%, while Xero, the most comparable peer, is down ~20%. The Scheme Offer is at a ~27% premium to the estimated adjusted (for the ASX index) downside price of $2.68/share.

Bain was okay selling at $3.15/share to KKR and will be fine selling its remaining ~6.5% stake at $3.40. Presumably, MYOB sounded out the other major shareholders such as Fidelity, Yarra Funds Management, Vanguard etc as to their read on the revised $3.40 offer, before agreeing to the SIA with KKR.

If the markets avoid further declines, this deal will probably get up. If the markets rebound, the outcome is less assured. This Tuesday marks the beginning of a new year and a renewed mandate for investors to take risk, especially an agreed deal; but the current 5.3% annualised spread is tight.

The Ministry of Finance, the major shareholder of TMB, confirmed that both Krung Thai Bank Pub (KTB TB)and Thanachart Capital (TCAP TB)had engaged in merger talks with TMB. Considering an earlier KTB/TMB courtship failed, it is more likely, but by no means guaranteed, that the deal with Thanachart will happen. Bloomberg is also reporting that Thanachart and TMB want to do a deal before the next elections, which is less than two months away.

TMB is much bigger than Thanachart and therefore it may boil down to whether TMB wants to be the target or acquirer. In Athaporn Arayasantiparb, CFA‘s view, a deal with Thanachart would leave TMB as the acquirer rather than the target. But Thanachart’s management has a better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than Bank Of Ayudhya (BAY TB) and would not change the bank rankings; but it would give TMB a bigger presence in asset management, hire-purchase finance and a re-entry into the securities business.

Mando accounts for 45% of Halla’s NAV, which is currently trading at a 50% discount. Sanghyun Park believes the recent narrowing in the discount may be due to the hype attached to Mando-Hella Elec, which he believes is overdone; and recommends a short Holdco and long Mando. Using Sanghyun’s figures, I see the discount to NAV at 51%, 2STD above the 12-month average of ~47%.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

As the colder winter weather is felt and the icy blast of industry tariff cuts continues to chill sentiment, we seek some respite (at least mentally) in the warmer climes of Okinawa. Okinawa Cellular is a unique company. It’s a small cap telecom network operator in Japan with a focus on the sub-tropical islands of Okinawa Prefecture. As part of the KDDI group, the company benefits from its parent’s economies of scale, but with its local presence, it also benefits from being the hometown hero.

Because the stock is relatively small, from an investment perspective it runs into liquidity constraints that the other telcos do not have, so it’s a different type of investment but one that we think is worth looking at. Over the past 12 months Okinawa Cellular’s stock has fallen by 12.3%, but over the past year the stock has delivered a return in the middle of its peer group and has outperformed the broad TOPIX by about 5.5%. Like most telcos, Okinawa Cellular is also ramping its dividend payments, and the current yield is about 3.5%.

THE GMO INTERNET (9449 JP) STORY – GMO internet (GMO-i) has attracted much attention in the last eighteen months from an unusual trinity of value, activist and ‘cryptocurrency’ equity investors.

VALUE– Many traditional, but mostly foreign, value investors have seen the persistent negative difference between GMO-i’s market capitalisation and the value of the company’s holdings in its eight listed consolidated subsidiaries as an opportunity to invest in GMO-i with a considerable ‘margin of safety’.

ACTIVIST – Since July 2017, the activist investor, Oasis, has waged a so-far-unsuccessful campaign with the aim of improving GMO’s corporate governance, removing takeover defences, addressing a ‘secularly undervalued stock price we are not able to tolerate’ (sic), and redefining the role and influence of the company’s Chairman, President, Representative Director and largest shareholder, Masatoshi Kumagai.

‘CRYPTO!’ – In December 2017, GMO-i committed to spending more than ¥35b or 10% of non-current assets. The aim was threefold: to set up a bitcoin ‘mining’ headquarters in Switzerland (with the ‘mining’ operations being carried out at an undisclosed location in Scandinavia), to develop proprietary state-of-the-art 7nm-node ‘mining chips’, and, in due course, to sell GMO-branded and developed ‘mining’ machines. The move was hailed in the ‘crypto’ fraternity as GMO-i became the largest non-Chinese and the first well-established Internet conglomerate to make a major investment in ‘cryptocurrency’ infrastructure.

OUTSTANDING – Following the December 2017 announcement, trading volumes spiked into ‘Overtraded’ territory – as measured by our Volume Score. Many investors saw GMO-i shares as a safer way of gaining exposure to ‘cryptocurrencies’, even as the price of bitcoin began to subside. By early June 2018, GMO-i’s shares had reached a closing price of ¥3,020: up 157% from the low of the prior year and outperforming TOPIX by 135%. Whatever the primary driver of this outstanding performance, each of our trio of investor groups no doubt felt vindicated in their approach to the stock.

CRYPTO CLOSURE – On December 25th 2018, GMO-i’s shares reached a new 52-week low of ¥1,325, a decline of 56% from the June high. Year to date, GMO-i shares have now declined by 31%, underperforming TOPIX by nine percentage points. On the same day, GMO-i announced that the company would post an extraordinary ¥35.5b loss for the fourth quarter, incurring an impairment loss of ¥11.5b in relation to the closure of the Swiss ‘mining’ headquarters and a loss of ¥24b to cover the closure of the ‘mining chip’ and ‘mining machine’ development, manufacturing and sales businesses. GMO-i will continue to ‘mine’ bitcoin from its Tokyo headquarters and intends to relocate the ‘mining’ centre from Scandinavia to (sic) ‘a region that will allow us to secure cleaner and less expensive power supply, but we have not yet decided the details’. Unlisted subsidiary GMO Coin’s ‘cryptocurrency’ exchange will also continue to operate, and the previously-announced plans to launch a ¥-based ‘stablecoin’ in 2019 will proceed. In the two trading days following this announcement, the shares have recovered 13% to ¥1,505.

RAIDING THE LISTCO PIGGY BANK – As we shall relate, this is the second time since listing that GMO-i has written off a significant new business venture which the company had commenced only a short time before. In both cases, the company was forced to sell stakes in its listed consolidated subsidiaries to offset the resulting losses. On this occasion, the sale of shares in GMO Financial (7177 JP) (GMO-F) on September 25 2018, and GMO Payment Gateway (3769 JP) (GMO-PG) on December 17 2018, raised a combined ¥55.6b and, after the deduction of the yet-to-be-determined tax on the realised gains, should more than offset the ‘crypto’ losses. According to CFO Yasuda, any surplus from this exercise will be used to pay down debt. Also discussed below and in keeping with this GMO-i ‘MO’, in 2015, the company twice sold shares in its listed subsidiaries to ‘smooth out’ less-than-desirable operating results.

In the DETAIL section below we will cover the following topics:-

I: THE GMO-i TRACK RECORD – TOP-DOWN v. BOTTOM UP

BOTTOM LINE No. 1: NET INCOME

BOTTOM LINE No.2 – COMPREHENSIVE INCOME

II: THE GMO-i BUSINESS MODEL – THROWING JELLY AT THE WALL

III: THE GMO-i BALANCE SHEET – NOT SO HAPPY RETURNS

IV: THE GMO-i CASH FLOW – DEBT-FUNDED CASH PILE

V: THE GMO-i VALUATION – TWO METHODS > SAME RESULT

VALUATION METHOD No.1 – THE ‘LISTCO DISCOUNT’

VALUATION METHOD No.2 – RESIDUAL INCOME

CONCLUSION – For those unable or unwilling to read further, we conclude that GMO-i ‘rump’ is a grossly-overrated business. Despite having started and spun off several valuable GMO Group entities, CEO Kumagai bears responsibility for two decades of serial and very poorly-timed ‘mal-investments’. As a result, the stock market has, except for the ‘cryptocurrency’-induced frenzy of the first six months of 2018, historically not accorded GMO-i any premium for future growth, and has correctly looked beyond the ‘siren song’ of the ‘HoldCo discount’. According to the two valuation methodologies described below, the company is, however, fairly valued at the current share price of ¥1,460. Investors looking for a return to the market-implied 3% perpetual growth rate of mid–2018 are likely to be as disappointed as those wishing for BTC to triple from here.

Lic Housing Finance (LICHF IN), founded by Life Insurance Corporation of India, is the 2nd largest Housing Finance Company (HFC) in India with a total outstanding loan book portfolio of Rs 1,759 bn as of 2QFY19. 94% of the company’s loans were to retail customers as home loans & Loan Against Properties (LAP) and the balance 6% were to project developers as of 2QFY19.

We like the business of LICHF for following reasons:

LICHF focuses on the salaried segment. 86% of the customers as of 2QFY19 were from the salaried class. This provides the company with stability in earnings and better asset quality. We expect the NIMs & Spreads to be stable at 2.4% & 1.2% respectively for the period of FY18-21E.

We expect LICHF’s total loan book to grow at a CAGR of 16% over the period of FY18-21E. This growth will be supported by LAP and Developer loans. We expect the retail home loan portfolio to grow at a CAGR of 11% over the same period.

As the company focuses on LAP & developer segment to grow the total loan book, we expect this to affect the asset quality adversely. We expect the Gross Non-Performing Assets (GNPA) & Net Non-Performing Assets (NNPA) to increase to 1.3% (from 1.2% as of Sept-18) & 0.5% (from 0.4% as of Sept-18) respectively.

We initiate coverage on LICHF with a fair value estimate of Rs 570/- over the next 12 months. This implies a potential upside of 19% from the closing market price of Rs 481 as on 20th December 2018. This is arrived by applying P/ABV (Price to Adjusted Book Value) multiple of 1.7X to our Adjusted Book Value Estimate of Rs 337 per share for the period ending Sept-20E.

Particulars

FY18

FY19E

FY20E

FY21E

P/ABV (X)

2.1

1.7

1.5

1.3

ROE (%)

17.3

15.5

14.5

15.1

ROA (%)

1.3

1.2

1.2

1.2

Source: Trivikram Consultants Research as of 20th December 2018

Short press below S&P 2,600 working well but the pace of the decline warns of a bigger macro bear cycle ahead in 2019.

Near term we are moving into oversold territory in core sectors featured in this webcast as the S&P approaches our first key target near 2,350. Given risk of a bounce post Christmas we are placing a tactical reversal target above this level.

Support levels to work into are outlined as well as tactical bounce targets. Given key support breaks that macro picture continues to favor shorting rally attempts as our cycle work suggests we see more pain after the New Year.

EEM outperform versus the S&P is gaining traction and with a USD roll would see additional fuel.

MSCI Asia x Japan perform call over US equities is also taking shape. Buy support targets outlined. If one intends to trade a year-end would licking bounce then Asia/EM’s is the space to participate.

Strong net profit momentum and more attractive to analysts relative to its sector

Higher power demand trend from new industrial consumers should continue supporting electricity sales, revenue rose 31% YoY in 3Q18

Large capacity expansion from Xayaburi hydroelectric power plant in Laos with expected commercial operation date (COD) in 4Q19 to more than double CKP’s current effective capacity

Trades above ASEAN Utilities at 19CE* 45.1x PE but offers great EPS growth in a sector that is expected to remain flattish

Risk: Delays for new plants, change in government regulation

During this quarter, we visited 13 companies and have to admit the average quality has improved. Amongst these, there were four stocks that impressed us the most, and the Oscars go to…

SSP acheiving profit growth in excess of 20% in the backdrop of Thai economic headwinds and Trumpian trade wars by expanding into countries unaffected by both issues.

Amata VN capitalizing on the shift from locations with rising labor costs (eg Thailand, China) to Vietnam, which has more than a few geographic and demographic advantages.

Gunkul, arguably Thailand’s hottest renewable play at the moment delivering outsized long-term growth in solar/wind space as well as a promising solar roof game plan.

TIGER, an aggressive and small construction company that has only IPO’d for less than a quarter and is already highlighting aggressive growth plans.

The Islami Bank Bangladesh (ISLAMI BD) narrative is underpinned by a quintile 1 global PH Score™ and a lowly franchise valuation by global standards.

ISLAMIBANK is a Shariah-centric entity, basing its operations on partnership, profit-sharing, a principal-agent/ lessee-lessor relationship, and trading via traditional concepts of Murabaha, Mudaraba, Musharakah, Muajjal, Ijarah, Ujarah, and Wadiah. The bank’s asset-base is dominated by “investments” relating to Bai-Murabaha (asset financing with a mark-up) and hire purchase under Shirkatul Melk with modest exposure to Bai-Muajjal, Quard, Bai-Salam, Mudaraba and Musharaka. More than 50% of “Investments” relate to the industrial space, in particular to textiles (spinning/weaving/dyeing), to agriculture, to garments and accessories, and to steel (re-rolling and engineering). About 90% of “investments” stem from urban areas. There is a focus on Dhaka and Ctittagong opportunity. Source of Funding is based on Mudarabah.

While the economy is in a relatively stable state, the Banking Sector presents a highly mixed picture. Funding and liquidity are adequate in the Banking System. At the main listed entities, ROA and ROE stand at around 1% and 12%. Capitalisation targets are moving in the right direction though there is a shortfall at a number of lenders. The sector is weighed down by SOCB asset quality and poor governance which needs to be addressed as it exerts a distortionary impact across the system. SOCB NPL ratio stands at around 30% and is probably worse than this versus around 10% for the system in general. The system stressed loan/investment ratio is probably double this level. Worryingly, private sector bank defaults are rising at a fast clip too.

Shares of ISLAMIBANK stand on an Earnings Yield of 13.5%, a P/B of 0.7x, and a FV at 5%, well below EM and global medians. Shares yield 4.3%. A quintile 1 PH Score™ of 8.2 captures value-quality attributes. Combining franchise valuation and PH Score™, ISLAMIBANK stands in the top decile of opportunity globally. Shares seem to discount any good news.

Bank St Petersburg PJSC (BSPB RM) benefits from an entrenched market position and strong brand recognition in its home market of City of St. Petersburg –represented by sectors such as pharmaceuticals, medical materials, motor vehicles, trailers/semi-trailers, food products, textiles, and rubber /plastic goods- as well as Kaliningrad and Leningrad.

BSPB’s asset base is a quite diversified. While management focuses on relatively low-risk and hence low-yielding loans to core large corporates and mortgages, the consumer credit segment and autos are a fast-growing area.

Top Russian banks tend to have a technological edge vis-a-vis other EMs. BSPB‘s Internet Bank ( i.bspb.ru) remains one of the best in Russia exhibiting a 25% growth in retail customers to 960k last year. A recent innovation was the launch of a mobile website which was created as part of the integrated environment based on BSPB Mobile banking apps for iOS, Android, and WindowsMobile . The e-banking system is currently used by more than 95% of the corporate customers of BSPB with 99% of payments and FX transactions being made online. BSPB cards support all the cutting-edge mobile payment technologies offered by Apple Pay, Samsung Pay and Android Pay.

A key of BSPB’s strategic plan is to achieve a sustained ROAE of 15%+. The bank also vows to remain among the top 20 Russian banks by assets and to increase transaction revenues by 50% over 2018-20. In order to achieve these goals, management is committed to expand the low-risk transaction business and bolster corporate lending by introducing industry expertise and specialisation and a segmental approach matching customer demand with high quality services and products.

Independent directors make up at least 1/3 of the Supervisory Board.

BSPB stands out trading at a 70% discount to Book Value and lies on a low Mkt Cap./Deposits rating of 6%, far below the global and EM median. BSPB commands a huge dividend-adjusted PEG of 5x with expected growth more than 3x its PER. Shares yield 3.5%. A quintile 1 PH Score™ of 9.4 captures the valuation dynamic while metric change is satisfactory. Combining franchise valuation and PH Score™, BSPB stands in the top decile of opportunity globally.

In October, the Nikkei leaked and Familymart Uny Holdings (8028 JP) immediately thereafter announced that Familymart would sell the rest of its GMS (and financing) subsidiary UNY to Don Quijote Holdings (7532 JP) (which bought 40% of the company in 2017) and would conduct a Tender Offer later in 2018 at a 20% premium to the then-current price to buy a stake in Don Quijote of just over 20%. The Tender Offer was announced November 6th. Familymart had arranged to borrow shares it did not manage to buy in the tender so that at the next record date it will have 20% of the voting rights by hook or by crook.

Don Quijote shares jumped to the Tender Offer price the same day and then spent a day there before investors decided that the news and structure of the deal was better news for Don Quijote than Familymart had priced in.

Results of the Tender Offer have just been announced. Familymart had been trying to buy 32,108,700 shares for JPY 212 billion. They just missed. They got 0.08% of the total desired, or 24,721 shares for just over JPY 163 million.

THEY GOT NOTHING.

I expect Familymart had zero idea this would happen. I expect their bankers are surprised as well. They should not have been. They analysed this badly. There was a decent chance they would find it difficult to dislodge shares from owners.

“I couldn’t think of selling that stock.” “You couldn’t?” asked Elmer, beginning to look doubtful himself. It is a habit with most tip givers to be tip takers. “Why not?” And Elmer drew nearer. “Why, this is a bull market!” The old fellow said it as though he had given a long and detailed explanation.

Growth stock managers don’t like selling growth stocks until the growth stops growing. Don Quijote is still growing. And with UNY, Don Quijote may grow faster than previously expected.

The announcement at the end of the Tender Offer Results announcement is also VERY telling. There was a plan to make Don Quijote an equity-method affiliate by buying in the Tender Offer, buying in the market, or borrowing lots of shares. There was a plan for Familymart to appoint directors to DQ.

There was a clearly-available trading strategy based on that.

The new announcement puts that strategy into question. And Mr. Partridge might not be so inclined to call it a bull market. Since the launch of the deal, the markets have started the trip to Gehenna in a trug. From the one-month average prior to the Familymart bid news, Don Quijote is up 25%. Familymart is up 40%, the Nikkei 225 is down 10.7%, the TOPIX retail sector is down 5.5% but Familymart and Don Quijote have influenced that performance (without those two names, average performance is worse).

Just how will Harbin Electric Co Ltd H (1133 HK)‘s independent directors justify recommending an Offer to shareholders at a price which gave cash less cavalier than cash?

MYOB Group Ltd (MYO AU)‘s directors grudgingly yet understandably enter an agreed deal with KKR.

As previously discussed in Harbin Electric Expected To Be Privatised, Harbin Electric (HE) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption. The Offer price of $4.56/share, an 82.4% premium to last close, is bang in line with that paid by HEC in January this year for new domestic shares. The Offer price has been declared final.

Of note, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors (and the IFA) can justify recommending an Offer to shareholders at any price below the net cash/share, especially when the underlying business is profit-generating.

Dissension rights are available, however, there is no administrative guidance on the substantive as well as procedural rules as to how the “fair price” will be determined under PRC and HK Law.

Trading at a gross/annualised spread of 15%/28% assuming end-July completion, based on the average timeline for merger by absorption precedents. As HEC is only waiting for approval from independent H-shareholders suggests this transaction may complete earlier than precedents.

KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal. The Offer price assumes no full-year dividend is paid.

On balance, MYOB’s board has made the right decision to accept KKR’s reduced Offer. The argument that MYOB is a “known turnaround story” is challenged as cloud-based accounting software providers Xero Ltd (XRO AU)and Intuit Inc (INTU US) grab market share. This is also reflected in MYOB’s forecast 7% revenue growth in FY18 and follows a 10% decline in first-half profit, despite a 61% jump in online subscribers.

And there is justification for KKR’s lowering the Offer price: the ASX is down 10% since KKR’s initial tilt, the ASX technology index is off by ~14%, a basket of listed Aussie peers are down 17%, while Xero, the most comparable peer, is down ~20%. The Scheme Offer is at a ~27% premium to the estimated adjusted (for the ASX index) downside price of $2.68/share.

Bain was okay selling at $3.15/share to KKR and will be fine selling its remaining ~6.5% stake at $3.40. Presumably, MYOB sounded out the other major shareholders such as Fidelity, Yarra Funds Management, Vanguard etc as to their read on the revised $3.40 offer, before agreeing to the SIA with KKR.

If the markets avoid further declines, this deal will probably get up. If the markets rebound, the outcome is less assured. This Tuesday marks the beginning of a new year and a renewed mandate for investors to take risk, especially an agreed deal; but the current 5.3% annualised spread is tight.

The Ministry of Finance, the major shareholder of TMB, confirmed that both Krung Thai Bank Pub (KTB TB)and Thanachart Capital (TCAP TB)had engaged in merger talks with TMB. Considering an earlier KTB/TMB courtship failed, it is more likely, but by no means guaranteed, that the deal with Thanachart will happen. Bloomberg is also reporting that Thanachart and TMB want to do a deal before the next elections, which is less than two months away.

TMB is much bigger than Thanachart and therefore it may boil down to whether TMB wants to be the target or acquirer. In Athaporn Arayasantiparb, CFA‘s view, a deal with Thanachart would leave TMB as the acquirer rather than the target. But Thanachart’s management has a better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than Bank Of Ayudhya (BAY TB) and would not change the bank rankings; but it would give TMB a bigger presence in asset management, hire-purchase finance and a re-entry into the securities business.

Mando accounts for 45% of Halla’s NAV, which is currently trading at a 50% discount. Sanghyun Park believes the recent narrowing in the discount may be due to the hype attached to Mando-Hella Elec, which he believes is overdone; and recommends a short Holdco and long Mando. Using Sanghyun’s figures, I see the discount to NAV at 51%, 2STD above the 12-month average of ~47%.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Hotel Properties (HPL SP) (“HPL”) announced on Friday evening a significant change in its shareholdings relating to the HPL shares owned by 68 Holdings Pte Ltd.

The restructuring of shareholding did not come as a surprise and was within expectations.

Now, Wheelock holds only a significant minority interest of 22.53% and without a board seat in HPL. Wheelock’s influence in HPL has been reduced significantly. Without control, Wheelock’s investment in HPL is as good as any other non-strategic investment in quoted securities.

In the event that Wheelock Properties decides to sell its HPL shares, Mr Ong will be a likely buyer of the HPL shares. This will present a very good opportunity for Mr Ong to successfully privatise and delist HPL.

Prabhat Dairy Ltd’s quarterly result is in line with our expectation. In Q2 FY19, the company registered a growth of 8.53% YoY, EBITDA margin was 9.4% improving by 119 bps since the same period last year, EBITDA grew by 24.2% YOY; the profit margin was at 2.95% improving by 60 bps YoY, Net Income grew by 35.86% YOY. For more details about the company, please refer to our initiation report Prabhat Dairy Ltd – An Emerging Star in the Indian Milky Way. B2B business contributed to 70% of revenue and the remaining 30% was driven by B2C business. Value Added Products contributed to 25% of revenue in Q2FY19.

The stock is trading at 16.3x its TTM EPS, 13.8x its FY19F EPS. Margins have improved over the past quarters due to lower cost of raw materials, we expect raw materials to continue to be lower than their historic average in short term. Lower cost of raw material along with the improving contribution from B2C will lead to higher margins in medium to long term. The company also wants to increase its B2C contribution aggressively from the current 30% to 50% by 2020.

We will monitor the stock closely to firm up our views further, albeit we remain positive on the long-term prospects of the company.

Swaraj Engines (SWE IN) (SEL)is primarily manufacturing diesel engines for fitment into Swaraj tractors manufactured by Mahindra & Mahindra Ltd. (M&M). The Company is also supplying engine components to SML Isuzu Ltd used in the assembly of commercial vehicle engines. SEL was started as a joint venture between Punjab Tractor Ltd (now acquired by M&M Ltd) and Kirloskar Oil Engines Ltd. M&M holds 33.3% stake in SEL and is its key client.

We are positive about the business because:

SEL’s growth is correlated with M&M’s tractor business growth. SEL supplies engines to the Swaraj division of M&M. M&M expects tractor growth to be around 12% YoY in FY19E. We forecast SEL’s tractor engine volumes will grow at a CAGR of 12% for FY18-21E.

The growth of the company is dependent on the monsoon and rural sentiments. We expect the profitability to improve with normal rainfall and government initiatives towards the rural sector. We expect the revenue/ EBITDA/ PAT CAGR for FY18-21E to be 14%/ 15%/ 14% respectively.

SEL is debt free and a cash generating company. It has a healthy and stable ROCE and ROE. SEL has increased its capacity from 75,000 engines in FY16 to 120,000 engines in FY18. We expect the capacity utilisation to reach 97% by FY20E from 90% in 1HFY19. SEL funds its capex through internal accruals. We forecast a capex of Rs 600 mn for FY19E to FY21E considering the requirement of the additional capacity, R&D and testing costs for new and higher HP engines & for upgradation of engines according to the TREM IV emission norms for >50 HP engines.

We initiate coverage on SEL with a fair value objective of Rs 1,655/- over the next 12 months. This represents a potential upside of 15% from the closing price of Rs 1,435/- (as on 26-12-2018). We arrive at the fair value by applying PE multiple of 18x to EPS of Rs 87/- to the year ending December-20E and add cash of Rs 82/- per share. While the business outlook is good, we think the upside in the share price is limited due to rich valuation.

Particulars (Rs mn) (Y/E March)

FY18

FY19E

FY20E

FY21E

Revenue

7,712

9,210

10,478