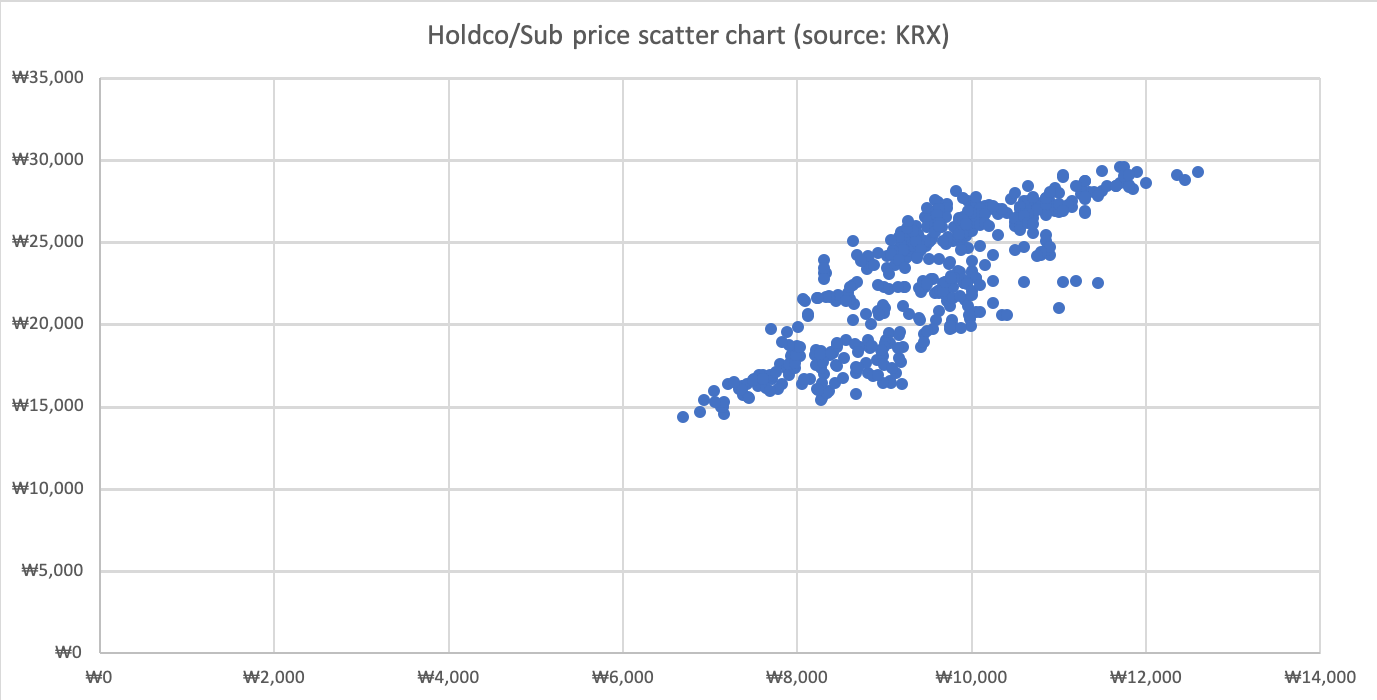

Hansae Yes24 Holdings Co, Ltd. (016450 KS) is a small cap holdco stock in Korea. Hansae Co Ltd (105630 KS) takes up half of Holdco NAV. Sub is Korea’s largest clothing OEM company. Holdco is currently at a 50% discount to NAV. This is the highest in 5 years. Discount was up nearly 10%p in the last 2 months.

Sub is taking a hit today. The share is down 5.56% now. Holdco is down only 1.21%. Macy’s unpleasant guidance revision is pulling down Sub price. We are now a little above -1 σ on a 20D MA. Sub shares have rebounded lately with the expectation on improving margins in the US. But weak holiday sales numbers in the US would be more than enough to kiss off this expectation.

I’d initiate a stub trade even though the duo has narrowed the gap today. It is still a long way to get reverted back to where they were two months ago.

Accordia Golf Trust (AGT SP) has not been a great success story since its IPO in August 2014. The stock went to market at a unit price of 0.97 SGD and was recently traded at 0.53 SGD. If we include the dividends received since the IPO (0.2387 SGD) the ‘real‘ adjusted price is still only 0.76 SGD.

In the past we have attended several management meetings and the 2017 company AGM but were disappointed on multiple occasions by management that either 1) did not care, 2) did not know how or 3) was held back by other corporate Japanese factors from creating shareholder value.

Over the last six months several new developments are potentially creating a cocktail that could finally create sustained value for AGT unitholders:

Appointment of new CFO who assures investors no repeat of “membership deposit debacle”

New five-year funding secured from two lenders

MBK Partners buys ORIX Golf Management

Value investor Hibiki Path Advisors buys 6.2% of the company

Clear focus on acquisitions and using its balance sheet strength

With its 2019 financial year ending in March, investors can be hopeful that its dividend in FY20 can grow to a minimum of 5 SGD cents suggesting a yield of 9.5%. If management injects assets a higher DPU is possible.

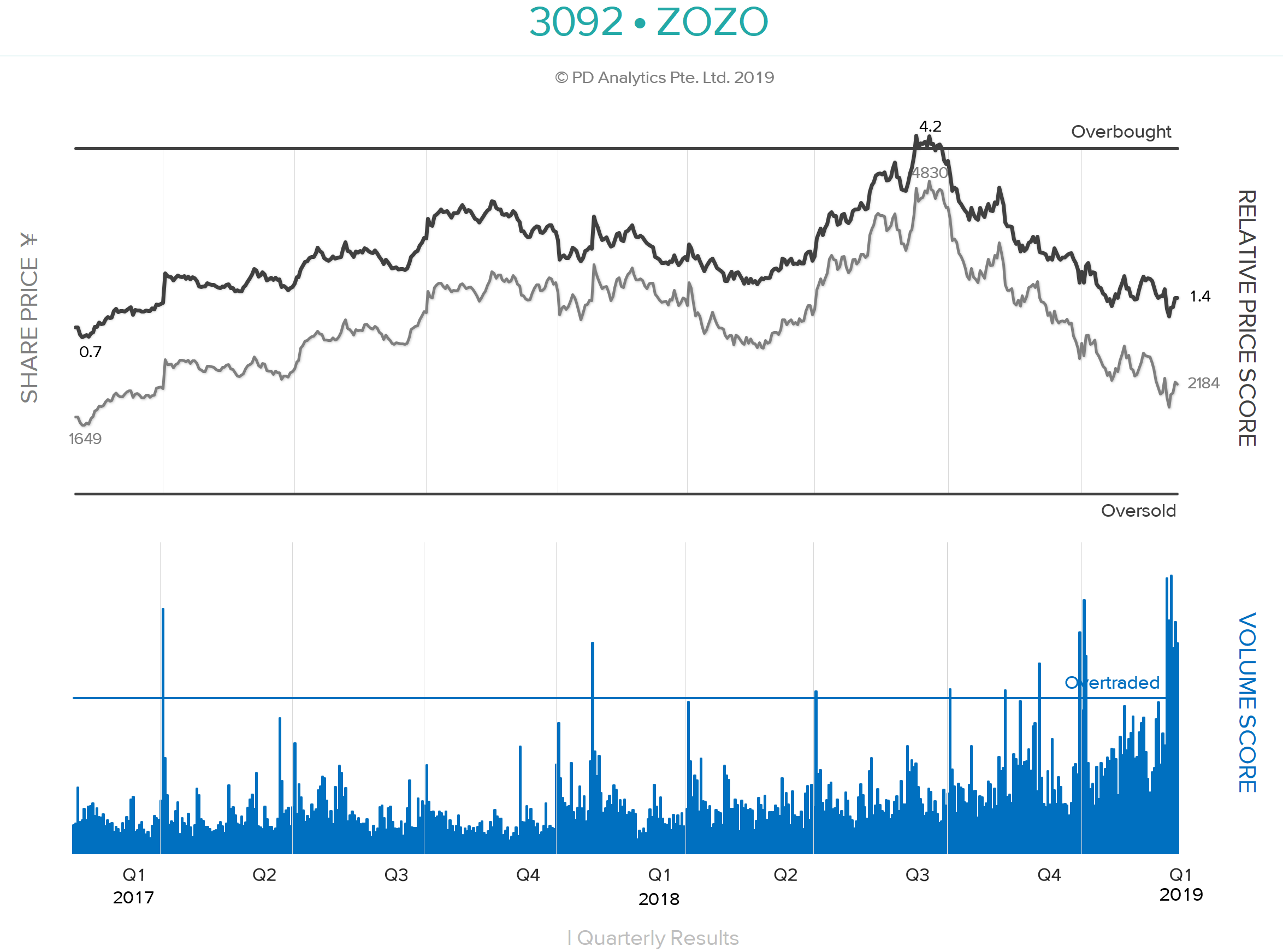

ONWARD AND OUT – ZOZO (3092 JP), formerly Start Today, has been the sixth-most-traded large capitalisation stock over the last ten trading days after Benefit One (2412 JP), Rizap (2928 JP), Takeda Pharmaceutical (4502 JP), Hoshizaki (6465 JP), and Workman Co Ltd (7564 JP). According to Nikkei XTECH, on 25th December apparel maker Onward (8016 JP) suspended selling of its products on ZOZOTOWN and will leave the platform altogether. Although Onward products are estimated to account for less than 3% of total transactions on the site, there are concerns that other apparel makers will follow suit as a result of the emerging direct competition on the site from ZOZO’s private label. Since reaching our 4.0 ‘Overbought’ threshold on 9th July 2018, ZOZO shares have corrected by 57% – the worst performance of any large cap from that date – as concerns mounted over the private brand strategy and the behaviour of CEO Yusaku Maezawa. Since bottoming on 4th January, the shares have risen by 18% following positive comments from the CEO about sales over the New Year holiday period.

PRIVATE-LABEL STRETCH GOALS– The ‘teething problems’ of ZOZO entering the private-label apparel business have been well-documented by Michael Causton in a recent Insight on Smartkarma. Michael rightly questions the feasibility of the company scaling a ¥200b apparel business within the next three years while targeting an additional incremental ¥400b in e-commerce revenue, particularly as it has taken ZOZO twenty years to reach the first ¥100b in annual revenues. In the DETAIL section below, we shall examine ZOZO’s current and possible future financial condition as it strives to become one of the top-ten global fashion retailers.

‘ZOSO’ & THE STAIRWAY TO HEAVEN – In addition to some notable purchases of modern art at record-breaking prices, CEO Maezawa also last year booked himself on Space X’s first flight to the moon. With apologies, the lyrics of the peerless song from Led Zeppelin’s untitled fourth album – known by fans as ‘Zoso’ after the symbol designed by Jimmy Page for the inner sleeve – come to mind:-

There’s a lad(y) who’s sure All that glitters is gold And (s)he’s buying a stairway to heaven When(s)he gets there (s)he knows If the stores are all closed With a word (s)he can get what (s)he came for.

We have received requests to provide a calendar of upcoming catalysts for near-term M&A, stubs and erstwhile event-driven names. Below is a list of catalysts over the near-term for such names as below. If you are interested in importing this directly into Outlook or have any further requests, please let us know.

Shares of E Mart Inc (139480 KS) are down 40% from their highs in March 2018 and we think this decline has been excessive. We believe the stock has bottomed and we expect a 20-30% upside on this stock over the next six months to one year (current share price is 193,500 won). At end of 3Q18, the company had 157 Emart hypermarkets and Traders warehouse supermarkets, of which 90% of their assets were owned by the company and 10% were leased. The company has the highest number of hypermarkets and warehouse supermarkets in Korea. The following are the major catalysts that could boost Emart shares by 20-30%+ in the next 6-12 months.

Renewed focus on the company’s real estate value

Upcoming IPO of Homeplus REIT in 2019

Push back against a steep increase in minimum wages

Success of Pierrot Shopping and a gradual reduction of unprofitable hypermarkets

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

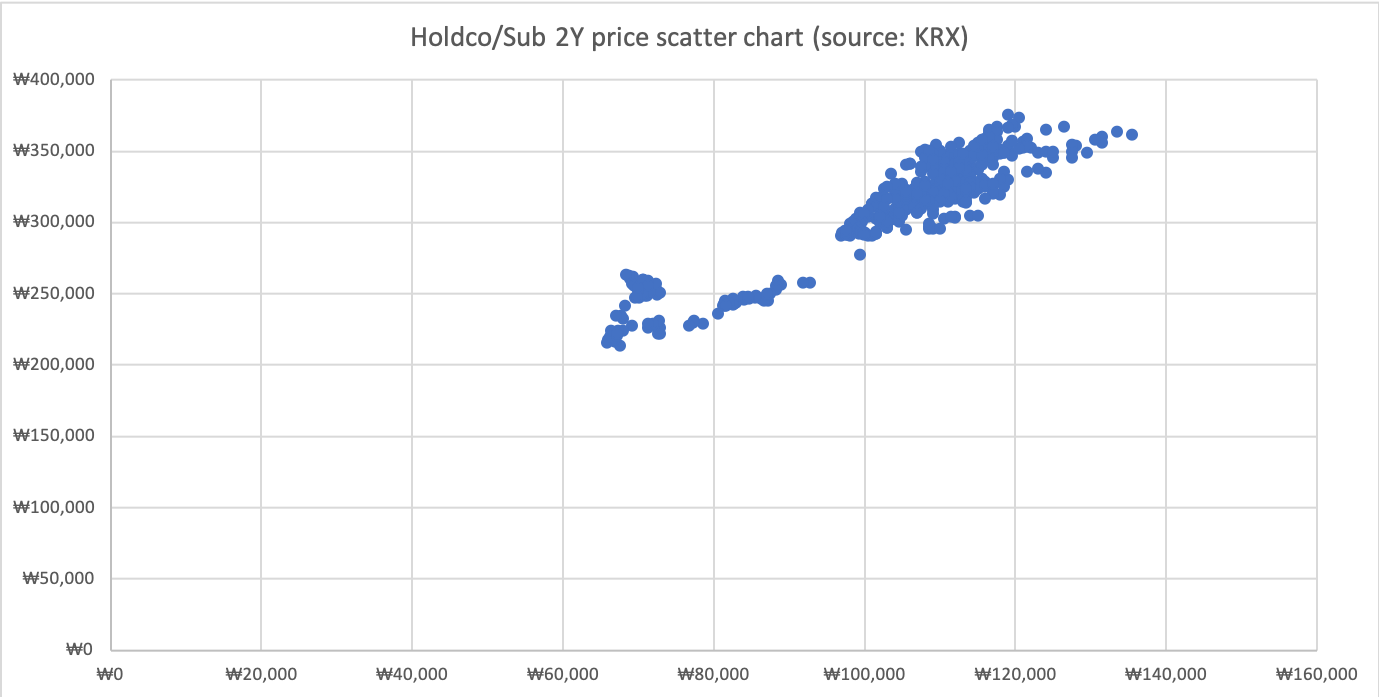

Thanks to improved Korea-China relation, Opco (004320 KS) shares have nicely rebounded lately. Nongshim Holdco hasn’t caught up. This created the highest price ratio gap in 2 years. On a 20D MA, they are close to the mean. But on a 2 year mean, Holdco is currently and still severely undervalued.

Liquidity has played a major role in the recent price gap widening. At a rebounding cycle like this, liquidity must have been a huge factor. But it shouldn’t be too long until Holdco catches up. Opco has kinda drifted sideways for a while now. This should be time for Holdco to begin a catchup.

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of fully-diluted shares (current shares out + 26.826mm Options + ~2.1mm Award shares).

The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The other terms and conditions of this deal will be set out in the offer document which is expected to be despatched in mid-January 2019 (14-21 days from 28 December).

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.10 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

With the fourth quarter just a few hours from closing, CEO Elon Musk says he is keeping Tesla Motors (TSLA US) stores open until midnight so buyers can still get the coveted $7,500 tax credit on a new car before it gets cut in half January 1st.

This is interesting since Tesla started warning months ago that buyers need to order by October to be guaranteed delivery by December 31st since said demand was purportedly so hot the company couldn’t make its cars fast enough. It remains to be seen how many early birds rushed in, because as time passed that deadline has been extended through November and then December. I snapped this from Tesla’s website yesterday:

Tesla web site, December 30th

The takeaway here is that despite months of extraordianary sales efforts, price erosion, and declining production, Tesla’s inventory remains troublingly bloated, conditions I warned about in the third quarter as accelerating threats for the fourth quartert and likely through 2019 (see my report “Great Magic Trick Tesla; Now Do It Again,” 11/29/18).

Monthly sales trends for October and November also signalled that Tesla needs strong December performance if it still hopes to meet ambitious guidance for profits and free cash flow the company desparately needs to generate sufficiently sustainable cash flow to support operations plus hefty nearterm debt maturities, much less its burgeoning R&D and capex obligations where it’s already fallen behind.

Otherwise Tesla is likely to get really creative, again, with accounting and cash managment strategies to keep up the illusion of progress and stability.

Read more as Bond Angle Analysis continues.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

We recently visited Prataap Snacks (DIAMOND IN) in Indore, Madhya Pradesh. Our objective of interaction was to get some clarifications on standalone financials of the company. As of FY 2018, standalone revenue was at 10,309 mn vs 10,377 mn for consolidated entity. Contrary to management’s suggestion to look at consolidated financials, we prefer to look at standalone financials, since the parent company contributes to 99% of Sales as 100% of the assets. Some of the issues that warrant attention are highlighted in this insight. Consensus financial data indicate an expectation of 44% growth in EPS for FY 2020. Our checks indicate an increasing competitive environment where both regional and national (MNC brands) are fighting for market share. The company is entering new product categories like sweet snacks. However, looking at growth expectations and cost structures discussed in this insight, investors would be better off looking for an alternative which is leaner.

A recent meeting with Bank Mandiri Persero (BMRI IJ) in Jakarta confirmed a positive outlook for loan growth and net interest margins for 2019, with continuing incremental improvements to credit quality, especially in the MidCap and SME space.

The bank is optimistic about loan growth in 2019 but with a shift in the shape of growth, with Midcap and SME loans moving into positive territory, a slight tempering of growth from large corporates.

Microlending continues to be a significant growth driver, especially salary-based loans, which have huge potential and are relatively low risk.

Mandiri is switching its focus on smaller sized mortgages and is even offering products specifically targeting millennials. It is also training staff in its branches to promote both mortgages and auto loans, which should help to boost growth in consumer loans.

The bank is investing heavily in growing both Mandiri Online mobile banking, as well as working closely with the major e-commerce players in Indonesia.

Management is optimistic about the outlook for net interest margins and comfortable with its funding requirements, with good visibility on credit quality.

Bank Mandiri Persero (BMRI IJ) remains a key proxy for the Indonesian banking sector, with an increasingly well-diversified portfolio and growing exposure to the potentially higher growth areas of microlending and consumer loans. The bank has fully embraced modern day banking with strong growth in Mandiri Online, which should help the bank grow its transactional business and its current and savings accounts (CASA). Its push to grow salary-based loans is another business with huge potential, given the low penetration of its corporate pay-roll accounts. According to Cap IQ consensus estimates, the bank trades on 12.5x FY19E PER and 11.0x FY20E PER, with forecast EPS growth of +16.5% and +11.8% for FY19E and FY20E. The bank trades on 1.9x FY18E PBV with an FY18E ROE of 13.9%, which is forecast to rise to 15.5% by FY20E. Given its higher growth profile and rising ROE, the bank looks relatively attractive compared to peers.

The Education Ministry of China promulgated Burden Relief Measures for Students in Primary and Secondary Schools (中小学生减负措施).

The market is concerned about “Article 15” on the educator license.

We note that a large number of teachers in part-time schools took the educator exam in November 2018.

We expect that the incremental passers of the educator exam will be many more than the number of EDU’s vacancies, and that most of the passers will prefer to work for giants such as EDU or TAL (TAL) as opposed to other part-time schools.

Over 2017-18, the Australian Securities & Investments Commission (ASIC) undertook a review of allocation in equity raising transactions. The review involved large and mid-sized licensees (brokers), Issuers, International investors and other international regulators. The results of the review were published by ASIC in Dec 2018. This insight highlights some of the key findings.

It’s good to see that some of the standard practices of banks allocating more to existing clients and participants of earlier deals have at least been acknowledged. Even though some institutional investors have outright labelled the allocation process as a “black box”, ASIC doesn’t seem to want to do much about it.

The area where ASIC is more concerned is the messaging to investors which highlights the different definitions of “well-covered” across banks. Although, the banks seem to have mislead the regulator on interpretation of “real-demand” with ECM bankers saying that all orders are taken at face-value. That raises a whole new level of questions on the messaging around demand for the deal.

Kingboard Chemical (148 HK)gets a boost after buying properties from its major shareholder, however, the implied yield is uninspiring.

Preceding my comments on BGF and KBC are the weekly setup/unwind tables for Asia-Pacific Holdcos.

These relationships trade with a minimum liquidity threshold of US$1mn on a 90-day moving average, and a % market capitalisation threshold – the $ value of the holding/opco held, over the parent’s market capitalisation, expressed as a % – of at least 20%.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

M1 Ltd (M1 SP), the third largest telecom operator in Singapore, is subject to a bid. On 7 January 2019, Konnectivity launched a voluntary conditional offer (VGO) at S$2.06 cash per share. Konnectivity is jointly owned by Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP).

M1’s shares are trading a touch above the VGO price of S$2.06 per share as the market is betting that Axiata Group (AXIATA MK) may ride in with its competing offer. However, we believe that shareholders should accept the offer as Axiata is unlikely to engage in a bidding war due to several factors.

While most news coverage is intensely focused on former Chairman Carlos Ghosn’s first public statements, defence strategy and Japan’s rather arcane justice system, we believe that news regarding the sudden “leave” of two Nissan executives is worth paying attention to as it may have ramifications for the fate of the alliance overall. We discuss the details below.

China Xinhua Education (2779 HK) listed in Q1 of 2018 and we wrote in our insight that the founder had vocational schools that have been separated from China Xinhua that seemed to be his prized asset. Fast forward to December 2018, the prized asset has finally filed its draft prospectus under the entity China East Education (CEE HK) and it is looking to raise US$400m in its IPO.

In this insight, we will analyze the company’s financial and operating performance, compare it to listed education companies, and provide some questions we have for management.

The Japanese telecom market was more volatile in 2018 than anticipated. However, Chris Hoare remains broadly positive on the sector for 2019. While pressure on the revenue line is intensifying, we do do not expect a price war to break out. In fact, we look for volatility to ease as the year progresses. Operators point to opex reductions and handset subsidy reductions to offset revenue weakness. We think that earnings are likely to surprise on to the upside. Over time we also look for dividend payout ratios to gradually rise, with the Softbank Corp (9434 JP) (KK) listing the long term catalyst. For Softbank Group (9984 JP) (SB) we look for market confidence to improve on the Vision Fund strategy, as profitable exits/up-valuations of assets such as Uber are announced.

The sector is recovering from NTT Docomo’s (9437 JP) price cut announcements but we don’t think they will slash prices (cuts will be selective). Our top pick is now KDDI (9433 JP) which could actually benefit from Rakuten’s (4755 JP) entry (as the roaming partner). DoCoMo is most affected but there are plenty of cost cutting opportunities. NTT (Nippon Telegraph & Telephone) (9432 JP) has optimistic guidance with substantial opex and capex cost cuts planned. Our order of preference for the stocks is now: KDDI (Buy), followed in order by NTT (Buy), SB Group (Buy), DoCoMo (Buy) and SB Corp (Neutral). We do not currently cover Rakuten.

In our Discover HK Connect series, we aim to help our investors understand the flow of southbound trades via the Hong Kong Connect, as analyzed by our proprietary data engine. We will discuss the stocks that experienced the most inflow and outflow by mainlanders in the past seven days.

We split the stocks eligible for the Hong Kong Connect trade into three groups: those with a market capitalization of above USD 5 billion, those with a market capitalization between USD 1 billion and USD 5 billion, and those with a market capitalization between USD 500 million and USD 1 billion.

In the past week, there were only three and a half days trading on the Hong Kong Stock Exchange last week. Hence the flow numbers were not as significant as a typical 5 trading day week. Having said that, we find it interesting that the Chinese were buying China Resources Beer Holdin (291 HK), Great Wall Motor Company (H) (2333 HK). In addition, Yichang Hec Changjiang Pharm (1558 HK) is a rare health care stock that experienced inflow last week despite overall poor sector performance last week.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

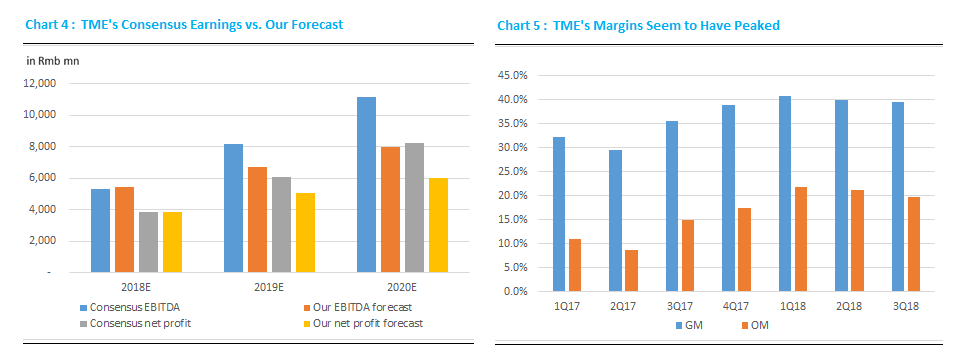

Tencent Music Entertainment (TME US)‘s social entertainment services (discretionary consumption in nature) face more headwinds due to ongoing China (macro) consumption slowdown.

Moreover, high consensus earnings expectation would make material earnings downgrade a major narrative for TME throughout 2019, in our opinion.

We initiative coverage on TME with Short/Sell recommendation, with 12-mo PT of US$9.80/ADR (representing a 25% downside potential).

Geely announced its Dec 2018 car sales volume at 93,333 units (down 39% yoy) and its FY2018 sales volume at 1.5mn units, 6% lower than our estimate of 1.59mn units.

Meanwhile management sets its FY2019 sales target at 1.51mn units, which surprised the market as the market consensus stood at around 1.8mn units. The stock price corrected by 11.3% on Jan 8th, right after the announcement.

In our view, it is reasonable for the management to give a cautious guidance for 2019E. After all, 2019E China’s auto sales volume might drop by 8% yoy.( China Auto Outlook 2019 – Keep Warm, Winter Is Here! )

However, would Geely’s aggressive new model launches sales offset the weak demand on existing models in 2019E? If not how bad it could be? In this report, we have done a scenario analysis. Our analysis shows that the possibility that Geely missing its 2019E guidance is low. Even assuming our worst case scenario, the stock would be at 7.1x P/E and no medium term downside from current levels.

A combination of, optimism surrounding U.S.-China trade talks, and Fed Chairman Powell’s comments have led to a continuation of the oversold bounce which began on 12/26, and the S&P 500 is now trading just below the 12/19 pre-Fed rate hike area. ~2,350 on the S&P 500 remains the support level to monitor. A retest of this low remains the most likely scenario, though it is far from a guarantee due to the potential for a “V” reversal. We examine an array of factors leading to our intact cautious outlook, and highlight attractive set-ups within Consumer Discretionary and Health Care Sectors.

China Tobacco International (GHALPZ CH) is a subsidiary and offshore unit of China National Tobacco Corp., a state-owned enterprise (SOE). The company procures tobacco leaves from regions around the world and exports tobacco leaf products and branded cigarettes to the duty-free outlets outside China’s customs area and in Southeast Asia.

The IPO is expected to raise US$100M and the company expects to use the proceeds to expand market share, acquire new cigarette brands, working capital, and other corporate purposes.

In this report, we provide an analysis of our pair trade idea between BGF Co Ltd (027410 KS) and Bgf Retail (282330 KS). Our strategy will be to be long BGF Co & Short BGF Retail. BGF Co Ltd (027410 KS)‘s share price plummeted by 48% in the past year while Bgf Retail (282330 KS) had a tiny gain of 0.7% in the same period. In the past year, BGF Co was down versus BGF Retail for pretty much the entire year. The BGF/BGF Retail share price ratio has been trending downwards since March 23rd, 2018. The current ratio is 0.037 and it is now close to approaching two σ.

The following are the major catalysts that could boost BGF Co shares higher than BGF Retail shares within the next six months.

Temporary relief from big market fears, seasonality, & trading volume

Market’s concerns about the size of tender offer rather than the value of BGF Co post tender offer in 2018

NAV discount to its intrinsic value at an all-time high – Our NAV analysis of BGF Co suggests that it is trading at a 51% discount to its NAV, which is close to its all time highest discount. Typically, the Korean holdcos trade at a 20-40% discount to their intrinsic value so it is unusual for the holdco to trade with so much discount.

Government is likely to slow down the minimum wage hikes

Potential increases in brand usage fees

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Hyosung Corporation (004800 KS) had fallen 16% just in two days. Holdco is now at a 50% discount to NAV. This is a 10%p drop from 10 days ago (Dec 19). Holdco price must have been overly corrected. The ongoing police investigation on Cho Hyun-joon’s alleged crime won’t lead to a delisting. 10%p drop in discount to NAV must be a price divergence, not a sensible price correction.

Trade volume remained steady. Local hedge funds led the selling on Dec 27. Even they changed their position the following day. No short selling spike has been seen either. Hyosung is one of the highest yielding div holdco stocks. Hyosung Capital liquidation and Anyang Plant revaluation would be another short-term plus.

I’d exploit this price divergence. It would soon revert to the Dec 19 discount level. It should at least stay at the peer average.

Just how will Harbin Electric Co Ltd H (1133 HK)‘s independent directors justify recommending an Offer to shareholders at a price which gave cash less cavalier than cash?

MYOB Group Ltd (MYO AU)‘s directors grudgingly yet understandably enter an agreed deal with KKR.

As previously discussed in Harbin Electric Expected To Be Privatised, Harbin Electric (HE) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption. The Offer price of $4.56/share, an 82.4% premium to last close, is bang in line with that paid by HEC in January this year for new domestic shares. The Offer price has been declared final.

Of note, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors (and the IFA) can justify recommending an Offer to shareholders at any price below the net cash/share, especially when the underlying business is profit-generating.

Dissension rights are available, however, there is no administrative guidance on the substantive as well as procedural rules as to how the “fair price” will be determined under PRC and HK Law.

Trading at a gross/annualised spread of 15%/28% assuming end-July completion, based on the average timeline for merger by absorption precedents. As HEC is only waiting for approval from independent H-shareholders suggests this transaction may complete earlier than precedents.

KKR and MYOB entered into Scheme Implementation Agreement (SIA) at $3.40/share, valuing MYOB, on a market cap basis, at A$2bn. MYOB’s board unanimously recommends shareholders to vote in favour of the Offer, in the absence of a superior proposal. The Offer price assumes no full-year dividend is paid.

On balance, MYOB’s board has made the right decision to accept KKR’s reduced Offer. The argument that MYOB is a “known turnaround story” is challenged as cloud-based accounting software providers Xero Ltd (XRO AU)and Intuit Inc (INTU US) grab market share. This is also reflected in MYOB’s forecast 7% revenue growth in FY18 and follows a 10% decline in first-half profit, despite a 61% jump in online subscribers.

And there is justification for KKR’s lowering the Offer price: the ASX is down 10% since KKR’s initial tilt, the ASX technology index is off by ~14%, a basket of listed Aussie peers are down 17%, while Xero, the most comparable peer, is down ~20%. The Scheme Offer is at a ~27% premium to the estimated adjusted (for the ASX index) downside price of $2.68/share.

Bain was okay selling at $3.15/share to KKR and will be fine selling its remaining ~6.5% stake at $3.40. Presumably, MYOB sounded out the other major shareholders such as Fidelity, Yarra Funds Management, Vanguard etc as to their read on the revised $3.40 offer, before agreeing to the SIA with KKR.

If the markets avoid further declines, this deal will probably get up. If the markets rebound, the outcome is less assured. This Tuesday marks the beginning of a new year and a renewed mandate for investors to take risk, especially an agreed deal; but the current 5.3% annualised spread is tight.

The Ministry of Finance, the major shareholder of TMB, confirmed that both Krung Thai Bank Pub (KTB TB)and Thanachart Capital (TCAP TB)had engaged in merger talks with TMB. Considering an earlier KTB/TMB courtship failed, it is more likely, but by no means guaranteed, that the deal with Thanachart will happen. Bloomberg is also reporting that Thanachart and TMB want to do a deal before the next elections, which is less than two months away.

TMB is much bigger than Thanachart and therefore it may boil down to whether TMB wants to be the target or acquirer. In Athaporn Arayasantiparb, CFA‘s view, a deal with Thanachart would leave TMB as the acquirer rather than the target. But Thanachart’s management has a better track record than TMB.

Both banks have undergone extensive deals before this one: 1) TMB acquired DBS Thai Danu and IFCT; and 2) Thanachart engineered an acquisition of the much bigger, but struggling, SCIB.

A merger between the two would still leave them smaller than Bank Of Ayudhya (BAY TB) and would not change the bank rankings; but it would give TMB a bigger presence in asset management, hire-purchase finance and a re-entry into the securities business.

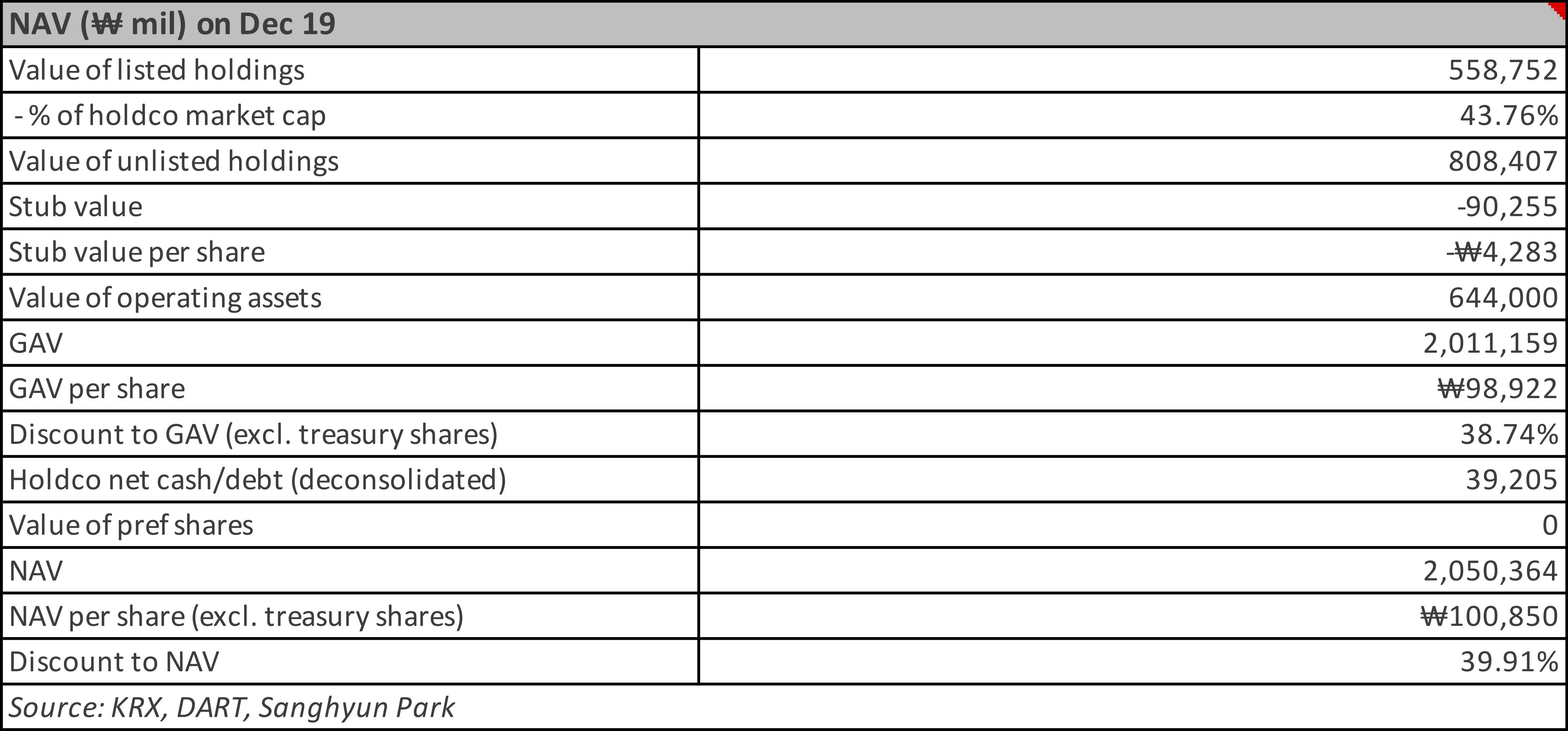

Mando accounts for 45% of Halla’s NAV, which is currently trading at a 50% discount. Sanghyun Park believes the recent narrowing in the discount may be due to the hype attached to Mando-Hella Elec, which he believes is overdone; and recommends a short Holdco and long Mando. Using Sanghyun’s figures, I see the discount to NAV at 51%, 2STD above the 12-month average of ~47%.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

A year ago we began publishing Tracking Traffic/Chinese Tourism as the hub for all of our research on China’s tourism sector. This monthly report features analysis of Chinese tourism data, notes from our conversations with industry participants, and links to recent company news and thematic pieces. Our aim is to highlight important trends in China’s tourism sector (and changes to those trends).

In this issue readers can find:

A review of China’s outbound tourist traffic in November, which strengthened: Lifted by extraordinarily strong growth in visits to Hong Kong and, to a lesser extent, Macau, Chinese outbound travel demand rebounded strongly in the seven regional destinations we track. But the fact that November’s growth was led overwhelmingly by Hong Kong and Macau — destinations close enough for weekend or day trips from population centers in Southern China — suggests Chinese tourists’ purse strings are still tight.

An analysis of November domestic Chinese travel activity, which turned weaker: November data from China’s three leading airlines and the Ministry of Transport show moderating domestic travel demand. For combined rail, highway, and air travel, November demand grew by less than 3% Y/Y. Along with the change in destination mix for outbound travel (that favors ‘nearby’ destinations), it now appears domestic demand has weakened, too.

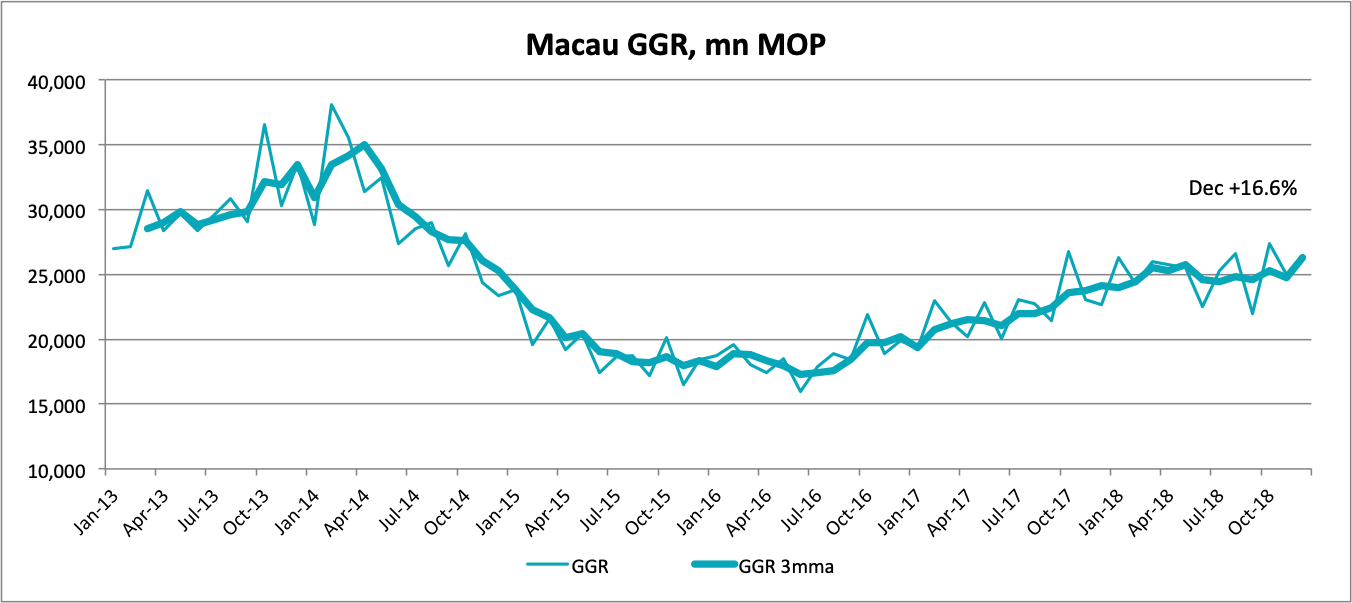

Links to other recent news & research on Chinese tourism: Readers can check out our quick takes on Macau’s December GGR figure, preliminary GTV and revenue figures released by Ctrip.Com International (Adr) (CTRP US), declining US visa issuance to Chinese tourists, and Qatar Airways’ new investment in a leading Chinese airline.

Although we remain positive on the long-term growth of Chinese tourism, it’s clear that near-term demand has weakened substantially. We continue to take a negative view of travel intermediaries like Ctrip, which face intensifying competition from many sources. We are more positive on the prospects of actual owners of Chinese travel and tourism assets, like hotel chain Huazhu Group (HTHT US) and Air China Ltd (H) (753 HK).

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP)and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of FD shares. The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.08 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

M1 has seen ~175mm shares traded since the initial announcement – all at prices above the proposed Offer Price of S$2.06. In that time, Starhub has popped and fallen back, and SingTel has fallen almost 10% to its lowest level in seven years.

Clearly, there is expectation that either Axiata will counter or Keppel and SPH will raise the Offer to bring Axiata onside. Travis Lundy doesn’t see who would join Axiata in bidding for M1 at a price of 8+x TTM EBITDA when there is price competition to come. He thinks it more likely that a small kiss (perhaps even a decent bump to S$2.30 or even more) to the price is made by the Offerors SPH and Keppel to get Axiata over the line. However, he does not think the Offerors need to offer that much to dislodge retail shareholders if the IFA comes out and says “increased competition puts the dividend in danger“.

Healius, a leading Australian owner of GP clinics and pathology centres, announced an unsolicited and conditional proposal from Jangho Group Co Ltd A (601886 CH) for A$3.25/share (~9.6x FY19 EV/EBITDA) in a A$2.0bn deal. Jangho currently holds a 15.9% stake in Healius and could potentially go hostile here.

Pricing looks off according to Arun George, at a 15% discount to peers on a CY2019 EV/EBITDA metric.

Still, Healius is not without issues, having to pay a backpay bill to staff last year, bump salaries for workers at its Victorian pathology division, while also losing a lucrative national bowel screening contract in 2017.

Notwithstanding the price, as Healius is an owner of sensitive medical data, the FIRB would take a very close look at this transaction, especially one where the acquirer is a Chinese entity, given the recent rejection of the CKI/APA Group (APA AU) deal and Huawei’s 5G.

As the merger between TMB and Thanachart gets a nudge from the Ministry of Finance and could be finalized this month, Athaporn Arayasantiparb, CFA tackles the obvious questions – what price and what benefits?

Based on his estimates, the potential improvements in ROE from the merger and potential divestment of Thanachart’s 19% stake in MBK, he thinks it justifies a Bt11.1/sh premium or Bt64.25/sh. Anything above that would feasibly be value destroying.

In terms of benefits, Thanachart has a higher ROE than TMB and appears smaller but better managed. The merger would allow TMB to re-enter the securities business (more cross-selling), enlarge its asset management franchise, and scale up the deposit base for both banks.

Reportedly Nexon’s founder Kim Jung-Joo and other related parties plan to sell their 98.64% stake in NXC Corp, which owns a 47.98% stake in Nexon. Nexon has a market cap of $11.6bn but the rumoured price tag for the 47.98% take is $8.9bn implying a significant management premium.

Initially launched as a voluntary conditional Offer late November, DNO ASA (DNO NO)crept over 30% in Faroe this week and is now required to launch an MGO. The Offer price remains the same at GBP 1.52/share, however, the acceptance condition falls to 50% from 57.5% previously.

Faroe’s pushback on the Offer – that the 21% premium offered to pre-announcement price is only “about half the average premium paid on all UK takeovers over the last 10 years” – is disingenuous. DNO built a 27.68% stake in a matter of days back in April 2018, clearly telescoping that a full-blown Offer was a possibility (although denying it at the time). The unaffected price prior to the acquisition of that stake should be used as a reference point for the current Offer. This translates to a 44.8% premium.

DNO has 43.1% in the bag, close to the 50% needed. There are investors (like Cavendish, holding 1.38%) who side with Faroe saying that the Offer is too low. With shares trading through terms, my bet is that DNO may need to kiss this offer, say 5-10%, to get it over the line.

Curtis Lehnert recommends closing out the set-up trade, now that he sees the stub having reverted to its long-term average level. Since his recommendation, the trade has made a notional gain of 5% in a two and a half month time span. As an aside I back out a discount to NAV of 21%, off its recent low of ~28% in early Nov, and compares to a 12-month average of 19%.

Back in September, I discussed in StubWorld: Matheson Unloads JLT, Unwind Takarathat Matheson may use the net proceeds of £1.7bn (US$2.2bn) from selling its 40.16% stake in Jardine Lloyd Thompson Group P (JLT LN)into Marsh & Mclennan Cos (MMC US)‘sOffer, towards increasing its stake in JS, as there was/is still some room before the maximum 85% ownership level was reached. This is what happened (or at least a token amount of the proceeds), with Matheson buying ~2.5mn shares in Strategic for ~US90mn in early October. Matheson now holds a little less than 84% by my calculation – the group unhelpfully states it holds 84% without going into decimal places.

After touching a 17-year low ratio level of 1.41x (JM/JS) last September, that has blown out to 1.83x, having closed the year at 1.89x, a two-and-a-half year high, and compares to the long-term average of 1.7x.

Strategic continues to trade “cheap” at ~44% discount to NAV, adjusted for the cross-holding. The spread between Matheson and Strategic is around its widest inside a year. Furthermore, as Matheson increased its stake, Strategic also acquired shares in Matheson earlier last year. Both elevate the cross-holding, which in principle you would expect the two companies to become even more closely aligned.

I’d recommend buying into Strategic for its attractive NAV discount and further share acquisitions from Matheson.

Stub Wrap

Using a basket of 40 Holdcos I constructed, the average NAV discount in 2018 steadily widened throughout the year. Elsewhere:

Passive, tech-related and illiquid Holdcos widened most; while cross-border and property Holdcos were the best of the worst.

Illiquid, property, and passive Holdcos’ underperformance (or widening) was more pronounced in the first half. Tech Holdcos primarily widened in the second half.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

We recently attended the extraordinary general meeting (EGM) of Zydus Wellness (ZYWL IN). The primary agenda for the EGM was to approve the issue of fresh equity and raise debt to finance the acquisition of Kraft Heinz Co (KHC US) ‘s Indian subsidiary Heinz India Private Limited jointly with Cadila Healthcare (CDH IN). This will include the brands Complan (Health Food Drink), Glucon D (Glucose Powder), Nycil (Talcum Power) and Sampriti Ghee. We believe the deal is in sync with management’s vision of developing Pharma oriented consumer brands. However with recent acquisition of Glaxosmithkline Consumer Healthcare (SKB IN) by Hindustan Unilever (HUVR IN) the competition in the health food drink market may get intense. Having said that, the largest brand Glucon D will likely continue market leadership along with Everyuth and Nycil which will be a good addition to the Zydus Portfolio. Any attempt for market share gains with Complan and Sampriti ghee will be futile and may come at a cost of margins. Based on preliminary, we expect full effect of the deal to appear on FY 2020 financials. Our preliminary estimates indicate a FY 2021 EPS of 51.68, which with a average PE multiple of 34.56 leads to a price target of INR 1809 per share implying an upside of 35% from latest close price of INR 1342. We will revisit our estimates post Q4 FY19 numbers when a much clearer picture is likely to emerge.

Avanti Feeds (AVNT IN) Q2 FY19 results were significantly below our expectations. While revenues declined by 14% YoY due to low shrimp cultivation as well as low demand particularly in US , the net profit declined by 68% YoY due to increase in raw material prices in the same period. We analyze the results.

Wonderla Holidays (WONH IN) Q2 FY19 results were below our expectations. While revenues declined by 16% YoY, EBITDA decreased by 18% YoY in Q2 FY19. The impact was primarily from its Kerala based amusement park that got affected by the devastating flood that the state has witnessed after a gap of near 100 years. We analyze the result.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Hankook Tire Worldwide (000240 KS) is another local single sub dependent holdco in Korea. Hankook Tire (161390 KS) accounts for nearly 90% of the sub holdings. Holdco is now at a 35% discount to NAV. This is substantially better than the local peer average.

Sub is taking a harsh hit now mainly on concerns over 4Q results. It is currently down 7% today. In contrast, Holdco is holding steady. It is rather up 1%. This is creating a massive price divergence. As of now, they are close to +3 σ on a 20D MA.

Holdco’s real world float is much less than 10% of total shares. This often serves to help Holdco stave off market volatility like today’s. But this much divergence is a rare one. Sub’s current PER on FY19e is at 7x. This is 20% less than its usual level. It should be that Sub is being oversold.

I’d make a very short-term trade at this point. I’d go short Holdco and long Sub for a quick mean reversion.

Please see some recent buy ideas, all very cheap, that we believe offer decent longer term growth and have had a dreadful December. We have written on all recently and below is a summary of the main points as well as an some valuation metrics. All are sensibly priced in our view now.

Amarin (AMRN US), a US-listed biotech firm, presented the full results of its “Reduce-It” (RI) clinical trial at a conference for the American Heart Association (AHA) last November. The new data announced showed that, Vascepa–Amarin’s cardiovascular drug–when used with statins, reduces the risk of heart attacks by 31%, strokes by 28%, and cardiovascular death by 20%–all with minimal safety issues. The stock has plunged by -37% since the AHA event, largely due to concerns–which are misplaced in our view–regarding the placebo used in the RI trial.

We attended the AHA event and its ancillary meetings in Chicago and, in this Insight, detail the main points covered there, the powerful efficacy of Vascepa, the addressable market, the placebo issue, and why we think Amarin could be 2019’s biggest buyout candidate among Big Pharma. We also analyze Amarin’s 2018 preliminary results and 2019 guidance from last Friday in detail.

Enthusiastic Response from Doctors over the “Reduce-It” Trial Data: The data released at the AHA event for Vascepa from its Reduce-It (RI) trial was so robust that it drew applause from the 2,500 doctors in attendance, 87% of whom were polled, responding that they would prescribe Vascepa. Given how safe the drug is and its high relative risk reduction (RRR) of cardiovascular events, Vascepa should be a blockbuster drug.

Q4 2018 Revenues & Prescriptions Surge Post Trial Results: Amarin just announced Q4 revenues and 2019 guidance last Friday. While its conservative 2019 guidance of $350m in revenues (+55% YoY) may disappoint, as it’s 16% below consensus estimates, the key focus should be on Q4 revenue growth of 38% YoY, with 35% growth in new prescriptions. This came on the back of the RI trial results and without any label expansion, which Amarin plans to file with the FDA during Q1. If label expansion is approved, Vascepa sales should soar further.

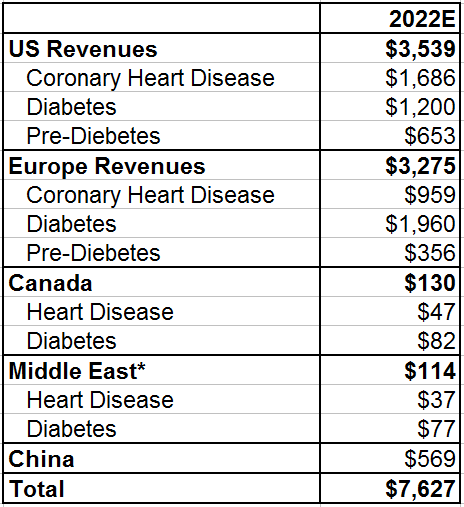

Peak Sales Could Easily Surpass $10bn if Vascepa is Approved in Europe & China: Counting only the patients with coronary heart disease and diabetes–the core target for Vascepa–there are 48m patients in North America, 98m in Europe and 230m in China. If only 30% of these patients use Vascepa by 2030–when its patent expires–peak sales could reach at least $12bn (see Table-3 below). The need for Vascepa is dire, as cardiovascular disease (CVD) is the leading cause of death worldwide (see chart-1). In the US, one in four adults have elevated triglycerides, yet only 4% have been treated. The upside for Vascepa is huge.

Stock Plunges Due to Concern Over Placebo Used in Reduce-It Trial: Just 16 minutes into the Reduce-It trial results being revealed at the AHA conference last November, Forbes published a “kill” story on the trial outcomes. The Forbes article (here) claimed that results were not trustworthy (quoting doctors in charge of clinical trials for a rival drug), as the mineral oil used in the placebo arm of the trial impacted statin absorption. This sent the stock plunging by -26% in the following two days after the conference. Below we discuss why these concerns are misplaced, especially since the FDA approved of mineral oil for use as a placebo.

Amarin is Now an Attractive Take-Over Candidate for Big Pharma: Based on our estimates, Amarin should reach $7.6bn in 2022 revenues and $8.40 in EPS (consensus is at $1.5bn and $2.23) on just 40% penetration of the CVD patients in the US and the Middle East (where Vascepa is already approved) and 30% penetration in Canada and Europe. On average, it takes drug makers at least $4bn over 10 years for new drug development and the success rate for FDA approval is only one in ten. In light of this, Amarin has become an attractive take-over candidate, with potential peak sales of $16bn (if China is successfully penetrated) and current market cap of only $4.2bn.

The rest of our event-driven research can be found below

Best of luck for the new week – Rickin, Venkat and Arun

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

Amarin (AMRN US), a US-listed biotech firm, presented the full results of its “Reduce-It” (RI) clinical trial at a conference for the American Heart Association (AHA) last November. The new data announced showed that, Vascepa–Amarin’s cardiovascular drug–when used with statins, reduces the risk of heart attacks by 31%, strokes by 28%, and cardiovascular death by 20%–all with minimal safety issues. The stock has plunged by -37% since the AHA event, largely due to concerns–which are misplaced in our view–regarding the placebo used in the RI trial.

We attended the AHA event and its ancillary meetings in Chicago and, in this Insight, detail the main points covered there, the powerful efficacy of Vascepa, the addressable market, the placebo issue, and why we think Amarin could be 2019’s biggest buyout candidate among Big Pharma. We also analyze Amarin’s 2018 preliminary results and 2019 guidance from last Friday in detail.

Enthusiastic Response from Doctors over the “Reduce-It” Trial Data: The data released at the AHA event for Vascepa from its Reduce-It (RI) trial was so robust that it drew applause from the 2,500 doctors in attendance, 87% of whom were polled, responding that they would prescribe Vascepa. Given how safe the drug is and its high relative risk reduction (RRR) of cardiovascular events, Vascepa should be a blockbuster drug.

Q4 2018 Revenues & Prescriptions Surge Post Trial Results: Amarin just announced Q4 revenues and 2019 guidance last Friday. While its conservative 2019 guidance of $350m in revenues (+55% YoY) may disappoint, as it’s 16% below consensus estimates, the key focus should be on Q4 revenue growth of 38% YoY, with 35% growth in new prescriptions. This came on the back of the RI trial results and without any label expansion, which Amarin plans to file with the FDA during Q1. If label expansion is approved, Vascepa sales should soar further.

Peak Sales Could Easily Surpass $10bn if Vascepa is Approved in Europe & China: Counting only the patients with coronary heart disease and diabetes–the core target for Vascepa–there are 48m patients in North America, 98m in Europe and 230m in China. If only 30% of these patients use Vascepa by 2030–when its patent expires–peak sales could reach at least $12bn (see Table-3 below). The need for Vascepa is dire, as cardiovascular disease (CVD) is the leading cause of death worldwide (see chart-1). In the US, one in four adults have elevated triglycerides, yet only 4% have been treated. The upside for Vascepa is huge.

Stock Plunges Due to Concern Over Placebo Used in Reduce-It Trial: Just 16 minutes into the Reduce-It trial results being revealed at the AHA conference last November, Forbes published a “kill” story on the trial outcomes. The Forbes article (here) claimed that results were not trustworthy (quoting doctors in charge of clinical trials for a rival drug), as the mineral oil used in the placebo arm of the trial impacted statin absorption. This sent the stock plunging by -26% in the following two days after the conference. Below we discuss why these concerns are misplaced, especially since the FDA approved of mineral oil for use as a placebo.

Amarin is Now an Attractive Take-Over Candidate for Big Pharma: Based on our estimates, Amarin should reach $7.6bn in 2022 revenues and $8.40 in EPS (consensus is at $1.5bn and $2.23) on just 40% penetration of the CVD patients in the US and the Middle East (where Vascepa is already approved) and 30% penetration in Canada and Europe. On average, it takes drug makers at least $4bn over 10 years for new drug development and the success rate for FDA approval is only one in ten. In light of this, Amarin has become an attractive take-over candidate, with potential peak sales of $16bn (if China is successfully penetrated) and current market cap of only $4.2bn.

A year ago we began publishing Tracking Traffic/Chinese Tourism as the hub for all of our research on China’s tourism sector. This monthly report features analysis of Chinese tourism data, notes from our conversations with industry participants, and links to recent company news and thematic pieces. Our aim is to highlight important trends in China’s tourism sector (and changes to those trends).

In this issue readers can find:

A review of China’s outbound tourist traffic in November, which strengthened: Lifted by extraordinarily strong growth in visits to Hong Kong and, to a lesser extent, Macau, Chinese outbound travel demand rebounded strongly in the seven regional destinations we track. But the fact that November’s growth was led overwhelmingly by Hong Kong and Macau — destinations close enough for weekend or day trips from population centers in Southern China — suggests Chinese tourists’ purse strings are still tight.

An analysis of November domestic Chinese travel activity, which turned weaker: November data from China’s three leading airlines and the Ministry of Transport show moderating domestic travel demand. For combined rail, highway, and air travel, November demand grew by less than 3% Y/Y. Along with the change in destination mix for outbound travel (that favors ‘nearby’ destinations), it now appears domestic demand has weakened, too.

Links to other recent news & research on Chinese tourism: Readers can check out our quick takes on Macau’s December GGR figure, preliminary GTV and revenue figures released by Ctrip.Com International (Adr) (CTRP US), declining US visa issuance to Chinese tourists, and Qatar Airways’ new investment in a leading Chinese airline.

Although we remain positive on the long-term growth of Chinese tourism, it’s clear that near-term demand has weakened substantially. We continue to take a negative view of travel intermediaries like Ctrip, which face intensifying competition from many sources. We are more positive on the prospects of actual owners of Chinese travel and tourism assets, like hotel chain Huazhu Group (HTHT US) and Air China Ltd (H) (753 HK).

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP)and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of FD shares. The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.08 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

M1 has seen ~175mm shares traded since the initial announcement – all at prices above the proposed Offer Price of S$2.06. In that time, Starhub has popped and fallen back, and SingTel has fallen almost 10% to its lowest level in seven years.

Clearly, there is expectation that either Axiata will counter or Keppel and SPH will raise the Offer to bring Axiata onside. Travis Lundy doesn’t see who would join Axiata in bidding for M1 at a price of 8+x TTM EBITDA when there is price competition to come. He thinks it more likely that a small kiss (perhaps even a decent bump to S$2.30 or even more) to the price is made by the Offerors SPH and Keppel to get Axiata over the line. However, he does not think the Offerors need to offer that much to dislodge retail shareholders if the IFA comes out and says “increased competition puts the dividend in danger“.

Healius, a leading Australian owner of GP clinics and pathology centres, announced an unsolicited and conditional proposal from Jangho Group Co Ltd A (601886 CH) for A$3.25/share (~9.6x FY19 EV/EBITDA) in a A$2.0bn deal. Jangho currently holds a 15.9% stake in Healius and could potentially go hostile here.

Pricing looks off according to Arun George, at a 15% discount to peers on a CY2019 EV/EBITDA metric.

Still, Healius is not without issues, having to pay a backpay bill to staff last year, bump salaries for workers at its Victorian pathology division, while also losing a lucrative national bowel screening contract in 2017.

Notwithstanding the price, as Healius is an owner of sensitive medical data, the FIRB would take a very close look at this transaction, especially one where the acquirer is a Chinese entity, given the recent rejection of the CKI/APA Group (APA AU) deal and Huawei’s 5G.

As the merger between TMB and Thanachart gets a nudge from the Ministry of Finance and could be finalized this month, Athaporn Arayasantiparb, CFA tackles the obvious questions – what price and what benefits?

Based on his estimates, the potential improvements in ROE from the merger and potential divestment of Thanachart’s 19% stake in MBK, he thinks it justifies a Bt11.1/sh premium or Bt64.25/sh. Anything above that would feasibly be value destroying.

In terms of benefits, Thanachart has a higher ROE than TMB and appears smaller but better managed. The merger would allow TMB to re-enter the securities business (more cross-selling), enlarge its asset management franchise, and scale up the deposit base for both banks.

Reportedly Nexon’s founder Kim Jung-Joo and other related parties plan to sell their 98.64% stake in NXC Corp, which owns a 47.98% stake in Nexon. Nexon has a market cap of $11.6bn but the rumoured price tag for the 47.98% take is $8.9bn implying a significant management premium.

Initially launched as a voluntary conditional Offer late November, DNO ASA (DNO NO)crept over 30% in Faroe this week and is now required to launch an MGO. The Offer price remains the same at GBP 1.52/share, however, the acceptance condition falls to 50% from 57.5% previously.

Faroe’s pushback on the Offer – that the 21% premium offered to pre-announcement price is only “about half the average premium paid on all UK takeovers over the last 10 years” – is disingenuous. DNO built a 27.68% stake in a matter of days back in April 2018, clearly telescoping that a full-blown Offer was a possibility (although denying it at the time). The unaffected price prior to the acquisition of that stake should be used as a reference point for the current Offer. This translates to a 44.8% premium.

DNO has 43.1% in the bag, close to the 50% needed. There are investors (like Cavendish, holding 1.38%) who side with Faroe saying that the Offer is too low. With shares trading through terms, my bet is that DNO may need to kiss this offer, say 5-10%, to get it over the line.

Curtis Lehnert recommends closing out the set-up trade, now that he sees the stub having reverted to its long-term average level. Since his recommendation, the trade has made a notional gain of 5% in a two and a half month time span. As an aside I back out a discount to NAV of 21%, off its recent low of ~28% in early Nov, and compares to a 12-month average of 19%.

Back in September, I discussed in StubWorld: Matheson Unloads JLT, Unwind Takarathat Matheson may use the net proceeds of £1.7bn (US$2.2bn) from selling its 40.16% stake in Jardine Lloyd Thompson Group P (JLT LN)into Marsh & Mclennan Cos (MMC US)‘sOffer, towards increasing its stake in JS, as there was/is still some room before the maximum 85% ownership level was reached. This is what happened (or at least a token amount of the proceeds), with Matheson buying ~2.5mn shares in Strategic for ~US90mn in early October. Matheson now holds a little less than 84% by my calculation – the group unhelpfully states it holds 84% without going into decimal places.

After touching a 17-year low ratio level of 1.41x (JM/JS) last September, that has blown out to 1.83x, having closed the year at 1.89x, a two-and-a-half year high, and compares to the long-term average of 1.7x.

Strategic continues to trade “cheap” at ~44% discount to NAV, adjusted for the cross-holding. The spread between Matheson and Strategic is around its widest inside a year. Furthermore, as Matheson increased its stake, Strategic also acquired shares in Matheson earlier last year. Both elevate the cross-holding, which in principle you would expect the two companies to become even more closely aligned.

I’d recommend buying into Strategic for its attractive NAV discount and further share acquisitions from Matheson.

Stub Wrap

Using a basket of 40 Holdcos I constructed, the average NAV discount in 2018 steadily widened throughout the year. Elsewhere:

Passive, tech-related and illiquid Holdcos widened most; while cross-border and property Holdcos were the best of the worst.

Illiquid, property, and passive Holdcos’ underperformance (or widening) was more pronounced in the first half. Tech Holdcos primarily widened in the second half.

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

We recently attended the extraordinary general meeting (EGM) of Zydus Wellness (ZYWL IN). The primary agenda for the EGM was to approve the issue of fresh equity and raise debt to finance the acquisition of Kraft Heinz Co (KHC US) ‘s Indian subsidiary Heinz India Private Limited jointly with Cadila Healthcare (CDH IN). This will include the brands Complan (Health Food Drink), Glucon D (Glucose Powder), Nycil (Talcum Power) and Sampriti Ghee. We believe the deal is in sync with management’s vision of developing Pharma oriented consumer brands. However with recent acquisition of Glaxosmithkline Consumer Healthcare (SKB IN) by Hindustan Unilever (HUVR IN) the competition in the health food drink market may get intense. Having said that, the largest brand Glucon D will likely continue market leadership along with Everyuth and Nycil which will be a good addition to the Zydus Portfolio. Any attempt for market share gains with Complan and Sampriti ghee will be futile and may come at a cost of margins. Based on preliminary, we expect full effect of the deal to appear on FY 2020 financials. Our preliminary estimates indicate a FY 2021 EPS of 51.68, which with a average PE multiple of 34.56 leads to a price target of INR 1809 per share implying an upside of 35% from latest close price of INR 1342. We will revisit our estimates post Q4 FY19 numbers when a much clearer picture is likely to emerge.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.

While Rizap Group (2928 JP) has seen its share price crash and its CEO bow in apology after profit warnings and a plan to radically cut back on M&A, Jeans Mate Corp (7448 JP), which Rizap acquired last year, has quickly moved to modernise stores. It has just replaced its Shibuya store with a new concept called JEM that could mean the end of the Jeans Mate name altogether and posted its first operating profit in years. While many of Rizap’s acquisitions were dubious, Jeans Mate is one business that could be turned around into a modestly successful casual apparel retailer.

Minnesotan Authorities declined to charge the founder of JD.

JD’s stock price has already plunged 52% in 2018. We believe JD is a defensive equity for portfolios, as the NASDAQ Composite just plunged 50% at most in the financial crisis of 2008.

Compared to 2014, today’s JD has a higher market share in the larger e-commerce market. However, JD’s stock price is at the same level as the first trading day in 2014.

JD continued to generate operating cash inflows in 2018 as previous years despite of its zero net margins.

We are not concerned about the programmer layoff in December, as we believe JD overly invested in “hi-tech” that will not bring revenues in the near future.

Based on historical Price / GMV, we believe there is an upside of 270% for JD’s stock price.

Thanks to improved Korea-China relation, Opco (004320 KS) shares have nicely rebounded lately. Nongshim Holdco hasn’t caught up. This created the highest price ratio gap in 2 years. On a 20D MA, they are close to the mean. But on a 2 year mean, Holdco is currently and still severely undervalued.

Liquidity has played a major role in the recent price gap widening. At a rebounding cycle like this, liquidity must have been a huge factor. But it shouldn’t be too long until Holdco catches up. Opco has kinda drifted sideways for a while now. This should be time for Holdco to begin a catchup.

Singapore telecom firm M1 announced on the 28th of December 2018 that Konnectivity Pte. Ltd. (a company jointly owned by Keppel Corp Ltd (KEP SP) and Singapore Press Holdings (SPH SP)) had made a Voluntary Conditional General Offer following the satisfaction of the pre-condition (IMDA approval) mentioned in the pre-conditional offer made in September.

The offer is to buy a minimum of 16.69% of the total share capital of M1 at a price of S$2.06 in order to increase the collective holding of the acquirer and its related parties from the current level of 33.32% to 50+% of fully-diluted shares (current shares out + 26.826mm Options + ~2.1mm Award shares).

The Offerors will buy all shares tendered if they get to a minimum of 50+%.

The other terms and conditions of this deal will be set out in the offer document which is expected to be despatched in mid-January 2019 (14-21 days from 28 December).

The offer price of S$2.06 translated to a premium of 26.4% to the undisturbed price before the trading halt for the pre-conditional offer. At the time of writing, the stock is trading at S$2.10 which is higher than the proposed Offer Price, indicating the market is expecting a bump or an overbid.

With the fourth quarter just a few hours from closing, CEO Elon Musk says he is keeping Tesla Motors (TSLA US) stores open until midnight so buyers can still get the coveted $7,500 tax credit on a new car before it gets cut in half January 1st.

This is interesting since Tesla started warning months ago that buyers need to order by October to be guaranteed delivery by December 31st since said demand was purportedly so hot the company couldn’t make its cars fast enough. It remains to be seen how many early birds rushed in, because as time passed that deadline has been extended through November and then December. I snapped this from Tesla’s website yesterday:

Tesla web site, December 30th

The takeaway here is that despite months of extraordianary sales efforts, price erosion, and declining production, Tesla’s inventory remains troublingly bloated, conditions I warned about in the third quarter as accelerating threats for the fourth quartert and likely through 2019 (see my report “Great Magic Trick Tesla; Now Do It Again,” 11/29/18).

Monthly sales trends for October and November also signalled that Tesla needs strong December performance if it still hopes to meet ambitious guidance for profits and free cash flow the company desparately needs to generate sufficiently sustainable cash flow to support operations plus hefty nearterm debt maturities, much less its burgeoning R&D and capex obligations where it’s already fallen behind.

Otherwise Tesla is likely to get really creative, again, with accounting and cash managment strategies to keep up the illusion of progress and stability.

Read more as Bond Angle Analysis continues.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.