BGF Co Ltd (027410 KS) / Bgf Retail (282330 KS) stub trade is at a 4.38% loss. Price ratio is still well below -1 σ. It is actually at a new yearly low. Holdco discount now stands at 48.55% to NAV.

Holdco price discount is too harsh. It’d be too tempting to pass up. An estimated 1.5~2%p difference in dividend yield must be pushing up price ratio soon.

I still believe below -1 σ wouldn’t last for as long as it used to. I’d hold onto this position a bit longer with a 10% loss cut.

The company forecasts an operating profit of Y55bn this year, the consensus is for Y57bn which is not unreasonable as management want to hold profits back. Next year assuming they make about Y64bn, the shares are on about 19x. With long term profits growth expected, and a good shareholder return policy this is a great domestic long term BUY. BUY into recent weakness. Foreigners own 24% of this name.

Dena Co Ltd (2432 JP) used to be the GO-GO internet stock for both retail and institutional investors in Japan during the previous bull run before 2008 and trading at 40-50x PER. The multiples have since then collapsed to 10-20x PER although the business prospect remains solid if not better. Benefiting from the increasing regulation in China, DeNA signed an agreement with Tencent Holdings (700 HK) to distribute Arena of Valor in Japan which will boost revenue and improve margin. At 14x PER and 1.2x PBR, DeNA looks attractive.

CMGE is an intellectual-property (IP) oriented mobile game operator. The company delisted from Nasdaq in 2015 and tried to do a backdoor listing on Shenzhen Exchange in late 2015 but it was canceled due to unfavorable market condition. It is now trying to list on the Hong Kong Exchange when the sentiment is poor due to the game approval suspension.

In this insight, we will take a look at the financial performance, key operating metrics, and analyze its games pipeline.

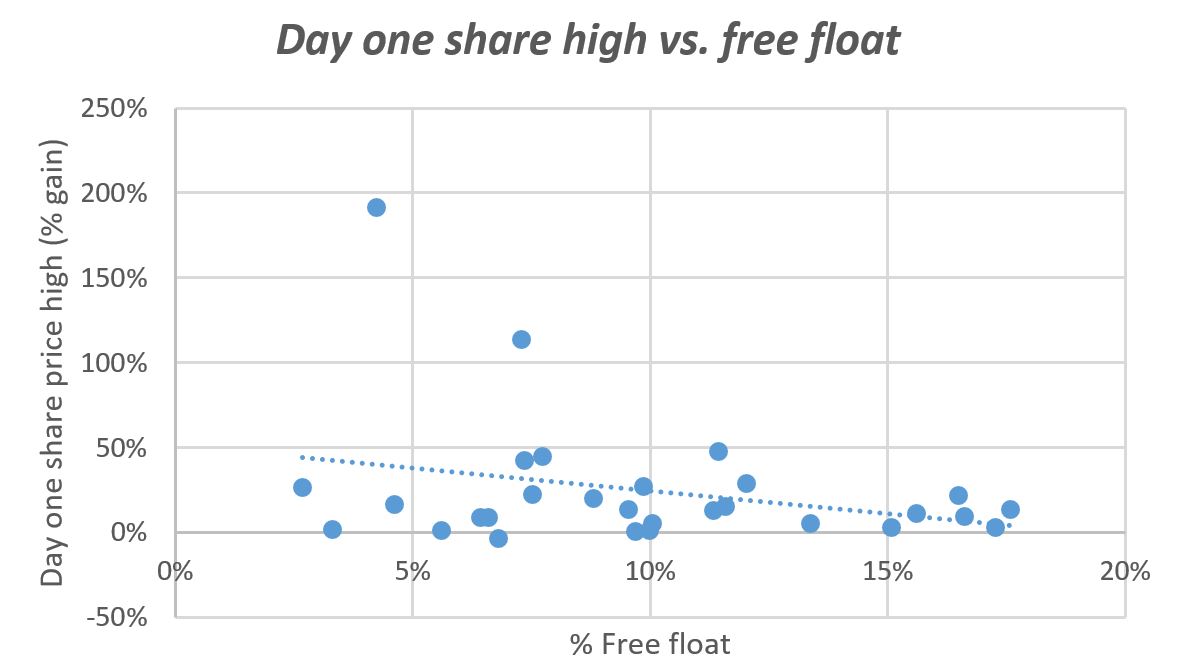

Ahead of Tencent Music (TME US)‘s IPO today , we have done a deep-dive analysis on the past 28 major Chinese IPOs that have listed in the US. We note the following points

A higher pop associated with a lower free float?

If it starts weak , we wouldn’t assume disaster – historically shares have broken above IPO price at some point during day one trade

Day one moves by pricing range – pops across the board

Natural Food International H (1837 HK)‘s IPO was priced at the low-end at HKD1.62/share. The retail tranche was 1.4x covered and the institutional tranche was said to be moderately over-subscribed. I have covered most aspects of the deal in my earlier insight,

In this insight, I’ll provide an update on the deal dynamics, valuations and provide a table with the implied valuations at different share price levels.

Following David Blennerhassett‘s recent StubWorld note, we wanted add a bit more detail on the non Tencent Holdings (700 HK) part of Naspers (NPN SJ). In any discussion of Naspers, this tends to get overlooked but in fact, Naspers has generally done quite well in these businesses, by building them, monetizing them, and in some cases selling them. Alastair Jones believes that, given moves to unbundle the pay-TV assets in 2019, there is scope for the NAV discount to narrow. The current low/negative valuation for the unlisted assets ignores their significant value.

If ever there was a stub business that is poised to capitalize on global trends of factory automation, automated logistics handling and electric vehicle prevalence, it is that of Toyota Industries (6201 JP). In August, I took an in-depth look at the major businesses of Toyota Industries and concluded that the market was not giving the company credit for the global leadership it has established in the forklifts and automobile A/C compressor businesses, nor for the progress it has made in the logistics equipment business. While the market’s oversight appeared to have corrected in September and October as the discount to NAV contracted from 34% to 25%, the trend has since reversed and the discount is back at trough levels of 35%. In August, I implied that this would be a good trading opportunity. Today, I explicitly recommend going long the stub.

In this insight I will cover:

A market-neutral trade setup

A review of the core unlisted businesses

Alternative data used to gauge performance in the core business

Risks of the trade

A recap of ALL my stub trade ideas on Smartkarma, including track record of performance

Shorting on Tire has softened in the last two trading days. No yearend dividend boosting effect is expected on Holdco. Holdco discount isn’t particularly high. Price ratio is well above yearly avg. I’d close this position now at a 6.07% yield.

Trade Me (TME NZ), the largest online auction platform operating in New Zealand, has entered into a scheme implementation agreement with Apax Partners. Apax Partners has upped its bid for Trade Me from NZ$6.40 to $6.45 a share, to match Hellman & Friedman’s bid.

Hellman & Friedman has until the shareholder vote scheduled for April 2019, to make a binding offer which is superior to Apax Partners, according to press reports. While Hellman & Friedman will likely have one last roll of the dice with an improved bid, we continue to believe that that the formal “winning” bid is unlikely to present a material bump.

We maintain Plan B Media (PLANB TB) with a BUY rating, and the new target price of Bt8.30 derived from 1.5xPEG’2019E, which is the average of Thailand’s consumer discretionary sector or equivalent to 32xPE’19E

The story:

Revising up net profit in 2018-20E by 2-11% mainly from BNK office

Music and sports marketing drive earnings momentum north

Plenty of opportunities to monetize underutilized capacity

Risks: Obstacles for renewing concession contracts with state-owned enterprises along with falling consumer spending and a share-price dilution effect on the back of then generally mandated raise in capital.

Titan Company Limited manufactures and sells watches, jewellery, eyewear, and other accessories and products in India and internationally. The company operates through four segments: Watches, Jewellery, Eyewear, and others. It is one of the few companies operating in organised jewellery retail industry of India. We visit stores & markets in Kochi (Kerela) and Chennai (Tamil Nadu), the biggest consumption markets to understand structural changes that have taken place in the industry, with an objective to tweak our revenue and margin estimates. We believe consensus might be underestimating growth from the jewellery segment which is the largest contributor with 81.60% of Sales as of FY2018. Our revenue estimates for FY19 and FY20 are 5.8% & 2.98% higher than consensus, primarily based on higher than expected market share gains from unorganised players. Our EBITDA margins for FY 19 & FY20 are 1% & 1.30% higher than consensus estimates primarily based on product mix which is in favour of studded jewellery and operating leverage as sales across stores pick up. Our EPS for FY19 & FY20 is estimated at INR 18.60 and INR 24.26 per share which is higher than consensus by INR 2.47 and 4.05 per share for FY 19 and FY 20. Based on an average forward multiple of 49x we arrive at a target price of INR 1187, representing a 30% potential return from current market price.

The conclusion from a recent meeting with the management of Surya Citra Media Pt Tbk (SCMA IJ) in Jakarta was that the company is ready to grasp the nettle of moving a significant focus towards the digital space. That said, it is clear that Free-to-Air business is still very much alive and kicking and will be the core driver for some time to come.

Media Partners Asia suggests that the advertising revenues for the Free-to-Air TV industry in Indonesia can grow +5.6% CAGR between 2017-2023.

Internet companies are driving growth at the margin but also make-up 2/3rds of the 15% of total spend on digital advertising, which suggests only 5% lost from TV.

Surya Citra Media Pt Tbk (SCMA IJ) is on the cusp of a significant move into the digital advertising and content space through Vidio.com, Kapanlagi.com, as well as its payments gateway Dana.

The company will also enter a new advertising medium of outdoor billboards, where it will seek to consolidate the industry through acquisitions, with the aim of controlling 50% of this market.

Surya Citra Media Pt Tbk (SCMA IJ) remains the best media proxy for advertising in Indonesia. It has seen its two main Free-to-Air stations SCTV and Indosiar command number 1 & 2 audience share positions over the last two months, giving an overall prime-time audience share YTD of 35%. The company estimates that the core business can probably achieve growth of +10% over the next two years. The real kicker to growth for the company will come from its significant move into the digital and content space through a series of acquisitions, mainly from its parent Elang Mahkota Teknologi Tbk (EMTK IJ). These transactions are will be done at arm’s length so as to avoid any corporate governance concerns. According to CapIQ consensus, the company is trading on 16.7x FY19E PER and 15.1x FY20E PER, with forecast EPS growth of 8.6% and 10.6% for FY19E and FY20E respectively. The company also has a dividend yield of 3.9% for FY19E and generates an ROE of 32%.

Late last week, Australian media reported that preliminary discussions were underway between NineEntertainment Co Holdings (NEC AU) and Macquarie Radio Network (MRN AU)’s second-largest shareholder, John Singleton. This development is not entirely unsurprising, just that formal discussions were deferred until the Nine/Fairfax Media (FXJ AU) merger was formally completed.

In July, Nine and Fairfaxentered into a Scheme Implementation Agreement in which the two companies would merge (albeit a Nine takeover) via a cash/scrip structure, in an A$4bn deal, creating Australia’s largest integrated media player. This included the acquisition of Fairfax’s 54.5% stake in MRN. The scheme was implemented on the 7 December. I discussed the merger in my insight Nine & Fairfax – Integrated Advertising.

In an interview with The Daily Telegraph last month (paywalled), John Singleton confirmed that he was ready to sell his 32% stake in MRN as he was not interested in being a small player in a big operation.

The Australian (paywalled) is reporting that Nine has offered $2/share (a 9.3% premium to the closing price of A$1.83 on December 4th), with Singleton believed to be holding out for $2.15/share. In a further twist, Alan Jones, with 1.27% of MRN, is understood to have certain conditions/clauses attached to that stake should Singleton sell, which may make an offer tabled by Nine potentially untenable.

For its part, Nine has confirmed it has held preliminary discussions regarding the outstanding shares, and further announcements will be made by Nine should these discussions progress to a transaction. MRN is currently trading at ~$1.90/share.

NIO Inc (NIO US) surged 30.7% in November after reporting steady growth in production and following certain notable investors such as Baillie Gifford & Co (largest investor in Tesla Motors (TSLA US) after Elon Musk) acquiring a stake in the company creating a bullish view on the company.

The EV start-up delivered 3,089 vehicles in November, registering a more than 96% increase from October, indicating a smooth flow in its production line of ES8. The latter was something its rival, Tesla, took long to establish. The company has reached a total production of more than 10,000 units thus far.

On the 15th of December which is the company’s ‘Nio Day’, Nio hopes to launch its ES6, a 5-seater, two-row, high-performance premium electric SUV that will have a longer range and at a lower price than its three-row seven-passenger ES8. Production and delivery of ES6 are expected to begin in 2019.

Q3 FY2018 results although slightly below the company’s expectations was an improvement compared to the previous quarter and acted as a tailwind in increasing investor confidence in the company. Sales increased to USD214m in Q3 from USD 46 in Q2. Though the company has not yet generated any profits, operating losses as a % of revenues have declined to -191.2% in Q3 cf.-4,077% in Q2.

For Q4 FY2019E the company expects to deliver 6,700 to 7,000 vehicles more than double the total deliveries during Q3, forecasting revenue between USD 418.5-436 m, at 95-100% increase from Q3. The company has not guided on OP.

Although the company is still fighting for profits, which seems to be normal for a start-up, it should be noted that the company has a quite steady cash reserve to fund its operation and ramp up production of its to-be-released ES6 model. In our opinion, if the launch of ES6 is as successful as ES8 and the company avoids production delays like Tesla, then it may break even or even make profits within a shorter time period than which Tesla took (almost 8 years). That said, Nio’s stock is likely to witness further surges through 2019 following its recovery since November.

The price has been set. The book building is done. Like watching a sleek race car aligned on the starting grid, the world eagerly awaits the start of trading for Softbank Corp (9434 JP) on Wednesday, 19 December.

We are also eager to see the stock go live. It’s not only nostalgia for the stock code “9434” to be brought back into the race, but it will be helpful to be able to compare the stock and to gain better insights into the domestic Japanese telecom industry.

That said, the past few weeks have been full of drama, and some of the drama has longer-term implications. In this insight, we take a more detailed look at some of the challenges facing SoftBank Corp. and some of the concerns that may give investors pause, or at least some things to keep in mind, over the months ahead.

Lawson (2651 JP) Fresh Pick is the convenience store operator’s new e-commerce solution for food launched earlier this year, and replacing various other less successful experiments.

Unlike competing services, Lawson’s service is limited to just 600 SKUs (stock keeping units), all fresh foods, and Lawson offers no home delivery, only click-and-collect.

In the nine months since launch, the service has expanded from 200 to 1,200 stores, currently concentrated in west Tokyo and Kanagawa.

It is a model that will expand rapidly across the rest of the country because Lawson has to invest so little to make this happen.

Specialty steel maker Nisshin Steel (5413 JP) is slated to merge with parent company Nippon Steel & Sumitomo Metal (5401 JP) as of January 1, 2019. For that, Nisshin Steel will be delisted on December 26th (i.e. the last day of trading is the 25th) and that means the Nikkei Inc was obliged to choose a replacement to take Nisshin Steel’s place in the Nikkei 225 and other indices.

The only one which matters is the Nikkei 225 (the other two have tiny tracking), and this is not a huge index trade as both Nisshin Steel and DIC are deemed 500 yen par value stocks.

This is an event one could “miss.”

And it will happen on Christmas Day, after a long weekend for Japan traders.

Amer Sports Oyj (AMEAS FH)announced (ANTA’s is here) an Offer at €40/share (a 39% premium to the undisturbed price of 10 September 2018), and announced that the Board of Directors of Amer Sports has decided to unanimously recommend that Amer Sports’ shareholders accept the Tender Offer. Several major shareholders holding 7.91% have irrevocably undertaken to tender, and Maa-ja vesitekniikan tuki r.y., who hold ~4.29%, have expressed that they view the Tender Offer positively. ANTA indirectly holds 1,679,936 shares (1.4%) as well.

ANTA and consortium appear to have the funding. As suspected and discussed in the original doc, FountainVest is a fair bit smaller than 50%. The equity stakes are, indirectly, 57.95% ANTA, 15.77% FountainVest, 5.63% Tencent Holdings (700 HK), and 20.65% Anamered Investments (Chip Wilson’s vehicle). There is a Shareholders’ Agreement which allows FountainVest the right to effect a Trade Sale if a “Qualified IPO does not take place within 5 years”, which seems reasonable. This effectively means that the company will be put up for sale in 5yrs.

It should be 11.5 weeks from Monday to Tender Offer completion, with 81-83 days between trade settlement and payment for Tender shares. That is ~27.1% annualized as of Friday’s close. This spread should drop at least by half after the Tender Launch scheduled for 20 December. Anti-trust and other authorities’ approval will be required. If ANTA gets over 90% of the shares, they intend to commence mandatory redemption (squeezeout) proceedings.

It should be noted that this deal offers significant leverage to ANTA and even more to the minority investors. ANTA is effectively collateralizing some LBO debt with its own earnings. As ANTA will not consolidate, the only way to see the numbers will be to look through the affiliate income. The saving grace here for everyone may be that it is remote from ANTA, which means transfer pricing will be carefully watched.

NHK reported JDI was in talks to sell about a 33% stake to a Chinese consortium for $440m (probably ¥50bn) which would value the company at about 3.5x (at the time) its current market cap. INCJ is also, apparently, considering support. These moves would go a long way toward restoring the company’s beaten-up balance sheet and the cost cuts should allow the company to survive – although Apple’s struggles still cast a shadow on a return to a strong level of profitability. JDI’s share price shot up 34.6% on the news on Friday.

JDI’s massive share price drop since its listing has been due to its weakened balance sheet and a slow shift to OLED, which this reported funding will go some way to addressing. Mio Kato, CFA‘s view is that JDI has some very promising businesses and the company is undervalued.

JDI still has an unhealthy over-dependence on Apple but they are doing everything they can to dilute the influence, increasing automotive display sales at double-digit rates and maintaining and growing their top market share in that segment, as well as producing more VR and notebook LTPS screens.

There still remains excess capacity in the industry due to Chinese government subsidies for display panel manufacturers and an over-ambitious build-out of both LTPS and OLED capacity. This is not going to improve drastically anytime soon but some of the planned OLED capacity expansions are being pushed out and much of the LTPS capacity increases have already been completed.

After Pioneer revealed in September it had sold its Tohoku Pioneer subsidiary to Denso Corp (6902 JP) for ¥10.9bn, it announced an MOU with Barings and went into debt to them. That seemed like “the end of the line” for the company. Pioneer needed a sponsor, but it was going to stay listed. Last week,Pioneer announced a “Partnership” with Baring Private Equity Asia which is a revitalization plan of ¥102bn. The deal offers minority shareholders an exit. The announcement does not mention investors are effectively being asked to approve their own squeezeout at 25% below the last price.

In the deal as presented, shareholders are being asked to approve an exit price 75% below 52-week highs which came AFTER the capital reduction in summer 2017, and after the sale of assets earlier this year, sell their shares at roughly one-third of existing book value per share, and sell its 3D LiDAR business and technology for… zero.

There are caveats. ALL of Pioneer’s net equity is intangibles. It has payables higher than receivables as of the end of September, and ¥25bn in net debt (increased by the ¥25bn lent by Baring). The company has roughly 2.5x EBITDA in inventory, and in a company which is losing money by being in business, inventory as marked is not as good as cash. The company has close to ~¥30bn in underfunded pension liabilities.

Travis does not expect a public activist outcry. Activists who wanted to buy into this have already done so. Any who do going forward have no vote because the record date for the vote was 7 December.

On December 3rd, the boards of both Hindustan Unilever (HUVR IN) (“HUL”) and GlaxoSmithKkine (“GSKCH”) approved a merger (subject to regulatory and shareholder approval) – at an exchange ratio of 4.39 HUL shares for every 1 GSKCH share – in a £3.1 bn deal. Combining with GSKCH should see HUL leapfrog both Britannia Industries (BRIT IN)and Nestle India (NEST IN)in food and refreshment revenue, and put it roughly on level pegging with ITC Ltd (ITC IN).

Approvals should be a foregone conclusion. With neither Unilever or GSK required to abstain, the 75% shareholder approval threshold is all but a lock. GSKCH’s shareholders get the benefit of HUL’s vast distribution network, while HUL gets a better understanding of the pharma channel.

Regulatory approval should not be an issue. 90% of cases handled by India’s anti-trust body CCI have been approved without the requirement for any modification. There is minimal overlap here – this is HUL’s big splash to build a sustainable and profitable food and refreshment business in India. Greater opposition would be expected if either BRIT, NEST or ITC made a tilt for GSKCH.

The transaction should be completed in one year, subject to regulatory and shareholder approvals. It’s a long-dated, but low-risk deal. Expect the tight spread to remain tight – this deal may close faster than the “expected” one-year timeframe.

Red Hat has set a meeting date of January 16, 2019 for shareholders to vote on the merger agreement withIntl Business Machines (IBM US), and related matters. Red Hat also set a record date of December 11th, 2018 for shareholders entitled to vote on the deal.

The fact the meeting date has been set means the SEC chose not to review the merger proxy (a less common occurrence than a review) and notified the companies of this decision within the expected 10 calendar days.

While the Company issued the press release, a new proxy has not yet been filed. John DeMasi expects we will see a definitive merger proxy filed within the next few days. Since the HSR U.S. antitrust 30 day waiting period will not expire until December 21st, he doesn’t expect an update on HSR in the definitive proxy, and it still appears the EC Competition filing has not been made according to the EC website.

John believes the deal is still on track for a Q2/Q3 2019 close and believes the risk/reward looks attractive here.

Reportedly, preliminary discussions are underway between NineEntertainment Co Holdings (NEC AU) and MRN’s second-largest shareholder, John Singleton. This development is not entirely unsurprising; it appears formal discussions were deferred until the Nine/Fairfax Media (FXJ AU) merger was formally completed (which occurred on 7 December). Nine acquired Fairfax’s 54.5% stake in MRN in the merger, discussed in my insight Nine & Fairfax – Integrated Advertising.

Also reported in the press, Nine has offered $2/share (a 9.3% premium to the closing price of A$1.83 on December 4th), with Singleton (a willing seller) believed to be holding out for $2.15/share. In a further twist, Alan Jones, with 1.27% of MRN, is understood to have certain conditions/clauses attached to that stake, which may make an offer tabled by Nine potentially untenable.

MRN was trading between A$1.20 and A$1.60 during the first half of the year. Following the announcement of the Nine-Fairfax merger in July, the share price reached a high of A$2.18. While the expected offer price of A$2.00 is 8.3% lower than this lifetime high, it is still 26% higher than the stock’s undisturbed price of A$1.59 before the Nine-Fairfax merger deal was announced.

Nine is interested in mopping up shares in MRN it does not already own. John Singleton is a seller, at the right price. Nine’s CEO Hugh Marks is keen to move quickly, not just taking full control of MRN, but also divesting assets that do not focus on digital subscriptions, mass audiences andnational advertisers. It’s now a question of how much Nine is willing to pay, and the added benefits therein to Nine from a privatisation compared to its current majority and consolidating stake.

While Inc and Healthcare are not cross-linked by any shareholding, Healthcare is ostensibly Celltrion’s internal sales arm. Their fundamentals and prices should be (& are) highly correlated.

Sanghyun initiated a pair trade (short Celltrion / long Healthcare) on Oct 22. The ongoing FSS investigation is hammering both, Healthcare more so as it is more directly exposed. But given what happened to Samsung Biologics Co., (207940 KS), it is very unlikely that this will be a serious risk.

Sigma Healthcare had seen its share price fall 70% in 18 months after its relationship with MyChemist/Chemist Warehouse went sour in 2017, then their existing contract was not renewed for post-June 2019. This appears to be because Sigma did not want to continue trading under overly-generous (to MC/CW) terms and capital usage.

In September, API started buying shares in Sigma Healthcare on the market when they were down by half from the July 2017 news, buying just under 5% before approaching Sigma with an Indicative Proposal to Merge in a Scheme. Sigma responded saying it was willing to engage with API, but API did not respond in the subsequent months it appears. Thursday API bought half of Allan Gray’s stake to lift its own stake to 13.95%, then it publicly announced the same Indicative Proposal.

So now we wait. There is a business review in progress. Full year results for Sigma are due in March. ACCC clearance may take until mid-year.

The deal is at a nice premium – 46.8% to the one-month average, and 69% to the day before. It was about 10% better than where API started buying.

But it may not be good enough. The deal offers some cash, but also offers expensive scrip. API appears to need this deal as much as some would say Sigma does.

Sigma is in the process of doing a zero-based full business review with Accenture and indications are that everyone thinks the company is worth a lot more than where it was trading last week.

This deal looks like it has a big premium but it may not be enough.

Huatai Securities Co Ltd (A) (601688 CH)(and Huatai H) announced that the CSRC had given the company approval to list up to (but not more than) 82,515,000 GDRs. The English language LSE announcement of the “Intention to Float” can be found here and here. Each GDR represents 10 A shares, that is up to RMB13.7bn at the (then) last traded price of the A shares prior to the announcement. If all the shares were issued that would be about 10% of the share capital of Huatai (pre-issuance). This GDR launches the London side of the London-Shanghai Connect. A prospectus is expected in the new year.

Assuming the GDRs trade similarly to the Hs, or even 1% of their maximum issuance quantity, and assuming they have a similar discount to the As as do the Hs, the GDRs will not likely trade more volume than the H Shares.

It is not clear WHY the GDRs would, over time, maintain a tighter discount to the A Shares than the H Shares would …. Except for the fungibility. Which may be the only reason to hold the GDRs at a 20% discount when you can get the H-shares at a 30+% discount. But the system may not be ready to handle GDR creation by mainland domestic investors trying to export capital, even at a discount.

The whole deal comes across as somewhat iffy. It is not clear why the deal needs to be done other than to fill a political need to get the ball rolling. But one wonders why the London-Shanghai Connect ball actually needs to be rolled.

Naspers’ recent underperformance against Tencent has resulted in the discount to NAV widening to near-on 12 months lows. While Naspers remains a function of what happens to Tencent, it offers potentially interesting long-term prospects.

This pseudo-venture capital company is taking steps to narrow the valuation gap via the reduction in its Tencent stake, the sale of successful investments (Flipkart and tbogroup), the listing of profitable entities (Multichoice), the investment in specific areas (classifieds, online retail, payments businesses and food delivery), working to reduce its exposure to the Johannesburg Stock Exchange, and perhaps pursue a dual listing outside of SA, such as Hong Kong. To me, Naspers’ risk profile appears attractive here.

New Street Research‘s Alastair Jones views the most recent Naspers results as broadly positive with continued progress in profitability from its e-commerce assets. He also believes that, given moves to unbundle the pay-TV assets in 2019, there is scope for the NAV discount to narrow. The current low/negative valuation for the unlisted assets ignores their significant value.

Curtis Lehnert recommends a Toyota Industries’ set-up at current levels which are in excess of -2 Standard Deviations below the long-term average, while Toyota Industries is trading at a 35% discount to his NAV – Toyota Industries’ stake in Toyota Motor accounts for 60%).

The group boasts the #1 global market share in forklifts with an estimated 20% market share. Toyota Industries’ closest competitor in the materials handling business is KION Group AG (KGX GR); however, Curtis estimates the market is implying 0.83x for these ops, 28% lower than Kion’s 1.15x.

Newton’s Three Laws of Motion And How They Pertain to Index Inclusions

Travis Lundy noted that Newton’s Third Law, commonly understood that for every action there is always an equal and opposed reaction, applies in some measure to index inclusions.

For every index upweight, there is an equal and opposite downweight.

Travis published his H/A Spread Monitor Project offering a brief look at recent changes in H-Share and A-Share spreads, Southbound flow and impact, and where the spreads are trading within their own historical ranges. My share class monitor provides a snapshot of the premium/discounts for 215 share classifications around the region. Ke Yan, CFA, FRM issued his Discover HK Connect series, to help understand the flow of southbound trades via the Hong Kong Connect.

The 1P (005385 KS)/ 2P (005387 KS) dividend yield difference of 0.53% is close to a year high. Of interest is the recently announced hydrogen cell investment, which may be considered a signal that the HMG-government relation has vastly improved. This potentially suggests that any HMG restructuring may get accelerated, which would be positive for 1P. (link to Sanghyun’s insight: Hyundai Motor Share Class: Time for 1P to Catch Up)

OTHER M&A UPDATES

Trade Me (TME NZ)and Apax Partners have entered into a scheme implementation agreement. Apax Funds have increased their offer price to $6.45/share (from $6.40) since the indicative proposal, following the completion of their due diligence. The Board has unanimously backed the offer. A booklet containing information relating to the scheme is expected to be mailed to Trade Me shareholders in March 2019. The Board expects that Trade Me shareholders will have the opportunity to vote on the scheme at a meeting in April 2019. If all the conditions are satisfied, the scheme is expected to be implemented in the second quarter of 2019. Hellman & Friedman was not expected to materially counter and promptly pulled out of the race.

Cityneon Holdings (CITN SP). West Knighton now has 98.6% of shares out and will move to compulsory acquire shares it does not own. The closing date has been extended until the 26 December.

Sinotrans Shipping (368 HK). As expected from the onset, shareholders approved the privatisation. Turnout was low – around 47.6% of shareholders entitled to vote, did so. Friday was the last day of trading. Cheques are expected to be dispatched on or before the 22 Jan 2019.

Stanmore Coal (SMR AU)‘s has released the Target Statement. The board continues to recommend shareholders reject the $0.95/share unsolicited Golden Investments. The IFA has a fair value range of $1.48-$1.90/share. Shares closed at A$1.04 on Friday.

CCASS

My ongoing series flags large moves (~10%) in CCASS holdings over the past week or so, moves which are often outside normal market transactions. These may be indicative of share pledges. Or potential takeovers. Or simply help understand volume swings.

Often these moves can easily be explained – the placement of new shares, rights issue, movements subsequent to a takeover, amongst others. For those mentioned below, I could not find an obvious reason for the CCASS move.

December turned out to be more eventful than expected. Guess not everyone is waiting peacefully at home for Santa to hop by. Here’s a quick run-down on stories that have impact (at least indirectly) on Thai equities.

Winning bids, losing confidence. PTTEP crushes Chevron in a mighty bid to secure the Bongkot and Erawan fields, but investors responded by driving their shares down 6%. Energy guru Manoon Siriwan pushes back on the bears saying that while costs are high, getting Erawan field on a greenfield basis should more than outweigh the negatives.

Huawei and trade wars. Trump’s trade wars take a strange turn following the arrests of Huawei CFO and Canadian citizens in China. As commerce and politics gets mixed up, talks abound about Apple moving production to Vietnam or…Thailand?

ERC puts the final nail to Glow’s coffin. This is lamest ruling ever! ERC rejects GPSC’s appeal saying that other industrial estates are already monopolies, and they don’t wanna turn MapTaPhut into another one. Their reasoning defies logic and forced us to capitulate on our Glow position.

End of the LTF era. As the tax exemptions from LTFs are phased out, critics point that equities-based programs favor the rich over the poor, while the Puay Ungpakorn Institute points out that insurance companies could benefit from this unfortunate event.

CP Group Routs the Mighty BTS in its bid for the high speed railway project, though their victory still predicates on the terms of government subsidy. Though this CP Group entity isn’t listed and many consortium members are foreign, two listed Thai consortium members include BEM and ITD, the country’s biggest construction company.

Aequitas Research puts out a weekly update on the deals that have been covered by Smartkarma Insight Providers recently, along with updates for upcoming IPOs.

IPO listings this week have mostly been within our expectation. Mobvista (1860 HK), Natural Food International H (1837 HK), and Fosun Tourism (1992 HK) have all struggled to hold on to their IPO price on the first day of trading. Unfortunately, WuXi AppTec Co (2359 HK) has also struggled on this first day despite our expectation that the company should be trading at a relatively smaller 19% A-H premium which would imply about 11% upside based on Ke Yan, CFA, FRM‘s sensitivity analysis and Wuxi Apptec’s A share Friday close price.

In the US, Tencent Music Entertainment (TME US) performed well within our expectation. The company’s share price opened about 9% above IPO price. As Sumeet Singh has mentioned in his insight, Tencent Music IPO – Firework – Trading Strategies, this is unlikely going to be a bumper IPO and short-term investors could take profit at high single-digit to low double-digit returns on debut. Indeed, after a decent debut, TME has collapsed below its IPO price, probably due to investors taking profit as the broad market traded poorly on Friday.

Next week, all eyes will be on Softbank Corp (9434 JP)‘s debut and Mio Kato, CFA summarised in his note some of the reasons why Softbank Corp could perform poorly in the near term. Bookbuild results have been mixed. Bloomberg report suggested that Softbank’s international bookbuild was 2-3x oversubscribed while retail offering was at almost 2x. However, Nikkei Asian Review’s article reported that it has been a struggle to sell the IPO shares to retail investors. In any case, we will put out a note next week on our thoughts on bookbuild, updated valuation of peers, and how we think the IPO will likely trade after the recent series of events.

Our overall accuracy rate is 72% for IPOs and 64% for Placements

(Performance measurement criteria is explained at the end of the note)

New IPO filings this week

Shanghai Henlius Biotech (Hong Kong, ~US$500m)

Ingrid Millet (Hong Kong, re-filed)

Below is a snippet of our IPO tool showing upcoming events for the next week. The IPO tool is designed to provide readers with timely information on all IPO related events (Book open/closing, listing, initiation, lock-up expiry, etc) for all the deals that we have worked on. You can access the tool here or through the tools menu.

Weichai Power, China’s largest independent Diesel engine producer, has been looking for a new core business to survive in long term downward trend of its current core business (Diesel engine for commercial vehicle and construction machines) since 2012 when it acquired 25% stake of KION Group AG (KGX GR). By now Weichai owns KION (materials handling equipment), Dematics (integrated automated supply chain technology, directly own ed by KION), Power Solutions International (PSIX US) (cleantech engine). It also has stakes in Ballard Power Systems (BLDP CN) (PEM fuel cell products), Ceres Power Holdings (CWR LN) (fuel cell technology and engineering). Lately, Weichai entered into an agreement with Westport Fuel System (WPRT.US) to develop and commercialise HPDI 2.0.

It seems Weichai decides to put its chip on fuel cell and low-emission engines. However, our analysis shows all the above investment would not be enough to secure Weichai’s market outlook in the next 5-10 years.

This note focus on an evaluation of Weichai’s technology choices on a 5-10 year time horizon. We will discuss the company’s 12-months view in another note.

Mahindra & Mahindra (MM IN) reported 2QFY19 PAT of Rs 17,788 mn vs our estimate of Rs 15,240 mn. The revenues were 2.5% lower than estimated. EBITDA was Rs 18,493 mn as against our estimate of Rs 20,721 mn. EBITDA margins were 14.5% against our estimate of 15.8%. Overall the performance was lower than our expectation.

EBITDA margins were impacted due to higher raw material cost and higher launch cost related to Marazzo (7/8 seater utility vehicle). We expect the margins to remain under pressure for the 2HFY19E as the Company has lined up more new model launches.

The shift in the festive season from 2Q to 3Q impacted the tractor sales volume in this quarter. M&M management expects the tractor industry to growth in the range of 12-14% YoY in FY19E where M&M is expected to grow at 12.5% YoY in FY19E.

We have lowered EPS estimates for FY20E by 8%. Over FY18-21E, we expect revenue and PAT to grow at CAGR 14% and 13% respectively. We expect EBITDA margin to expand from 14.8% in FY18 to 15.5% in FY21E.

Our EPS estimates for FY20E & 21E stand at Rs 47.3/- & Rs 53.7/- respectively. We have maintained the PE multiple of 17x with an EPS of Rs 47.2/- for the year ending September- 20E and valued its share in the subsidiaries at Rs 315/- to arrive at the fair value estimate of Rs 1,115/- for the next 12 months.

Particulars (Rs mn)

FY18

FY19E

FY20E

FY21E

Revenue

477,922

546,092

626,964

709,620

PAT

46,397

53,545

58,840

66,811

EPS (Rs)

37.3

43.1

47.3

53.7

PE (x)

20.4

17.7

16.1

14.2

Source- M&M Annual Report FY18, Trivikram Consultants Research as on 13/12/2018

Fosun Tourism (1992 HK)‘s IPO was priced at the low-end, HKD15.60/share. The retail tranche was undersubscribed while the institutional tranche was said to be moderately over-subscribed. I have covered most aspects of the deal in my earlier insights:

In this insight, I’ll provide an update on the deal dynamics, valuations and provide a table with the implied valuations at different share price levels.

1P (005385 KS) was supposed to make a catchup move yesterday relative to 2P (005387 KS). But it didn’t. Price ratio is currently well below -1 σ. Div yield difference is at 0.53%p. This is close to yearly high. At this level, 1P has no other way but to catch up with 2P.

In my previous insight, I suggested holding onto 1P/2P long/short position. This trade hasn’t performed well. We are at a 5.07% loss at yesterday’s closing. I’d still hold onto this position for the same reasonings as before.

Tricky one is the recently announced hydrogen cell investment. This may be seen as something boosting Common and likely 2P. Hydrogen cell investment should rather be considered as a signal that the HMG-government relation has vastly improved. This suggests that the restructuring may get accelerated. Anything positively affecting the restructuring should be positive on 1P.

Marketing of sports brands has become increasingly retail-led in the last decade and a focus on retailing has enabled Goldwin (8111 JP) to make serious gains while the two biggest domestic brands, Asics Corp (7936 JP) and Mizuno Corp (8022 JP), have been distracted by overseas expansion.

Goldwin took a close look at its beleaguered business 15 years ago and decided retail could be its salvation.

At current rates it will catch up with Mizuno’s domestic sales in a few years.

Overall, we are bullish about Goldwin but also the wider sports category because sports and sports fashion is in many ways one of the few consumer categories to be largely immune to a demographically challenged market like Japan – all age segments are buying into sports apparel, including the over 60s.

Hengan Intl Group (1044 HK), China’s leading sanitary towel and nappy producer, has been targeted by a short seller, Bonitas Research. Hengan has denied Bonitas’ allegations to which Bonitas has responded that Hengan’s response was weak and evasive. The shares have continued to slide suggesting that investors are less than convinced with Hengan’s rebuttal.

The aim of our note is to analyse alternative financial metrics to judge if Bonitas’ allegations are groundless or have some substance. Overall, our analysis suggests that Bonitas’ claims have some substance and investors should not be so quick to dismiss them.

Alpha Smart (ALS HK), the parent of Chinese menswear fashion retailer GXG, plans to raise US$300m in its Hong Kong IPO. L Catterton, LVMH’s investment arm, along with another PE investor, owns a 73% stake in the company.

Earnings have been consistently growing with the highest contribution still coming from its flagship brand “GXG”. The recent expansion of the online channel has further aided sales growth, with ASL claiming to be the largest menswear retailer in terms of online sales.

Apart from a large dividend payout which covered half of the acquisition costs for L Capital, nothing much seems to have changed recently. In addition, operating cash flow has not kept pace with earnings due to a consistent increase in inventory. To add to that there are a few related party issues as well including some stores being run by former employees.

Breadtalk (BREAD SP) has been a great Singapore Inc story since its founding in 2000. The company, under the leadership of George Quek, has grown from a few bakery outlets to hundreds of outlets across Asia. Profitability at Breadtalk has been lackluster but shares remain cheap on an EV/EBITDA basis.

Meanwhile, the group has an aggressive target to achieve 8% NPM by 2020 which not a single sell-side analyst believes they can achieve. Over the past week, the CEO was quoted in a Business Times article saying that he wants to achieve a “1 billion SGD market cap” vs the 480 million SGD market cap currently. While this could be easily dismissed as marketing talk, this target is not unrealistic at all.

With the launch of its first Din Tai Fung outlet in London investors better take notice. One of the drivers of upside surprises might be the rapid roll-out of Din Tai Fung in the UK and the rest of Europe. The CEO is even keen to explore expansion in the US market and has done research trips to Texas, LA and New York.

With the shares having derated from 1.16 SGD in early August to 0.86 SGD recently the valuation (6.8x 2019 EV/EBITDA) is now attractive once again. My Fair Value estimate remains at 1.25 SGD (47% upside).

Trade Me (TME NZ), the largest online auction platform operating in New Zealand, has entered into a scheme implementation agreement with Apax Partners. Apax Partners has upped its bid for Trade Me from NZ$6.40 to $6.45 a share, to match Hellman & Friedman’s bid.

Hellman & Friedman has until the shareholder vote scheduled for April 2019, to make a binding offer which is superior to Apax Partners, according to press reports. While Hellman & Friedman will likely have one last roll of the dice with an improved bid, we continue to believe that that the formal “winning” bid is unlikely to present a material bump.

We maintain Plan B Media (PLANB TB) with a BUY rating, and the new target price of Bt8.30 derived from 1.5xPEG’2019E, which is the average of Thailand’s consumer discretionary sector or equivalent to 32xPE’19E

The story:

Revising up net profit in 2018-20E by 2-11% mainly from BNK office

Music and sports marketing drive earnings momentum north

Plenty of opportunities to monetize underutilized capacity

Risks: Obstacles for renewing concession contracts with state-owned enterprises along with falling consumer spending and a share-price dilution effect on the back of then generally mandated raise in capital.

Titan Company Limited manufactures and sells watches, jewellery, eyewear, and other accessories and products in India and internationally. The company operates through four segments: Watches, Jewellery, Eyewear, and others. It is one of the few companies operating in organised jewellery retail industry of India. We visit stores & markets in Kochi (Kerela) and Chennai (Tamil Nadu), the biggest consumption markets to understand structural changes that have taken place in the industry, with an objective to tweak our revenue and margin estimates. We believe consensus might be underestimating growth from the jewellery segment which is the largest contributor with 81.60% of Sales as of FY2018. Our revenue estimates for FY19 and FY20 are 5.8% & 2.98% higher than consensus, primarily based on higher than expected market share gains from unorganised players. Our EBITDA margins for FY 19 & FY20 are 1% & 1.30% higher than consensus estimates primarily based on product mix which is in favour of studded jewellery and operating leverage as sales across stores pick up. Our EPS for FY19 & FY20 is estimated at INR 18.60 and INR 24.26 per share which is higher than consensus by INR 2.47 and 4.05 per share for FY 19 and FY 20. Based on an average forward multiple of 49x we arrive at a target price of INR 1187, representing a 30% potential return from current market price.

The conclusion from a recent meeting with the management of Surya Citra Media Pt Tbk (SCMA IJ) in Jakarta was that the company is ready to grasp the nettle of moving a significant focus towards the digital space. That said, it is clear that Free-to-Air business is still very much alive and kicking and will be the core driver for some time to come.

Media Partners Asia suggests that the advertising revenues for the Free-to-Air TV industry in Indonesia can grow +5.6% CAGR between 2017-2023.

Internet companies are driving growth at the margin but also make-up 2/3rds of the 15% of total spend on digital advertising, which suggests only 5% lost from TV.

Surya Citra Media Pt Tbk (SCMA IJ) is on the cusp of a significant move into the digital advertising and content space through Vidio.com, Kapanlagi.com, as well as its payments gateway Dana.

The company will also enter a new advertising medium of outdoor billboards, where it will seek to consolidate the industry through acquisitions, with the aim of controlling 50% of this market.

Surya Citra Media Pt Tbk (SCMA IJ) remains the best media proxy for advertising in Indonesia. It has seen its two main Free-to-Air stations SCTV and Indosiar command number 1 & 2 audience share positions over the last two months, giving an overall prime-time audience share YTD of 35%. The company estimates that the core business can probably achieve growth of +10% over the next two years. The real kicker to growth for the company will come from its significant move into the digital and content space through a series of acquisitions, mainly from its parent Elang Mahkota Teknologi Tbk (EMTK IJ). These transactions are will be done at arm’s length so as to avoid any corporate governance concerns. According to CapIQ consensus, the company is trading on 16.7x FY19E PER and 15.1x FY20E PER, with forecast EPS growth of 8.6% and 10.6% for FY19E and FY20E respectively. The company also has a dividend yield of 3.9% for FY19E and generates an ROE of 32%.

Late last week, Australian media reported that preliminary discussions were underway between NineEntertainment Co Holdings (NEC AU) and Macquarie Radio Network (MRN AU)’s second-largest shareholder, John Singleton. This development is not entirely unsurprising, just that formal discussions were deferred until the Nine/Fairfax Media (FXJ AU) merger was formally completed.

In July, Nine and Fairfaxentered into a Scheme Implementation Agreement in which the two companies would merge (albeit a Nine takeover) via a cash/scrip structure, in an A$4bn deal, creating Australia’s largest integrated media player. This included the acquisition of Fairfax’s 54.5% stake in MRN. The scheme was implemented on the 7 December. I discussed the merger in my insight Nine & Fairfax – Integrated Advertising.

In an interview with The Daily Telegraph last month (paywalled), John Singleton confirmed that he was ready to sell his 32% stake in MRN as he was not interested in being a small player in a big operation.

The Australian (paywalled) is reporting that Nine has offered $2/share (a 9.3% premium to the closing price of A$1.83 on December 4th), with Singleton believed to be holding out for $2.15/share. In a further twist, Alan Jones, with 1.27% of MRN, is understood to have certain conditions/clauses attached to that stake should Singleton sell, which may make an offer tabled by Nine potentially untenable.

For its part, Nine has confirmed it has held preliminary discussions regarding the outstanding shares, and further announcements will be made by Nine should these discussions progress to a transaction. MRN is currently trading at ~$1.90/share.

Ahead of Tencent Music (TME US)‘s IPO today , we have done a deep-dive analysis on the past 28 major Chinese IPOs that have listed in the US. We note the following points

A higher pop associated with a lower free float?

If it starts weak , we wouldn’t assume disaster – historically shares have broken above IPO price at some point during day one trade

Day one moves by pricing range – pops across the board

Natural Food International H (1837 HK)‘s IPO was priced at the low-end at HKD1.62/share. The retail tranche was 1.4x covered and the institutional tranche was said to be moderately over-subscribed. I have covered most aspects of the deal in my earlier insight,

In this insight, I’ll provide an update on the deal dynamics, valuations and provide a table with the implied valuations at different share price levels.

Following David Blennerhassett‘s recent StubWorld note, we wanted add a bit more detail on the non Tencent Holdings (700 HK) part of Naspers (NPN SJ). In any discussion of Naspers, this tends to get overlooked but in fact, Naspers has generally done quite well in these businesses, by building them, monetizing them, and in some cases selling them. Alastair Jones believes that, given moves to unbundle the pay-TV assets in 2019, there is scope for the NAV discount to narrow. The current low/negative valuation for the unlisted assets ignores their significant value.

If ever there was a stub business that is poised to capitalize on global trends of factory automation, automated logistics handling and electric vehicle prevalence, it is that of Toyota Industries (6201 JP). In August, I took an in-depth look at the major businesses of Toyota Industries and concluded that the market was not giving the company credit for the global leadership it has established in the forklifts and automobile A/C compressor businesses, nor for the progress it has made in the logistics equipment business. While the market’s oversight appeared to have corrected in September and October as the discount to NAV contracted from 34% to 25%, the trend has since reversed and the discount is back at trough levels of 35%. In August, I implied that this would be a good trading opportunity. Today, I explicitly recommend going long the stub.

In this insight I will cover:

A market-neutral trade setup

A review of the core unlisted businesses

Alternative data used to gauge performance in the core business

Risks of the trade

A recap of ALL my stub trade ideas on Smartkarma, including track record of performance

Shorting on Tire has softened in the last two trading days. No yearend dividend boosting effect is expected on Holdco. Holdco discount isn’t particularly high. Price ratio is well above yearly avg. I’d close this position now at a 6.07% yield.

BGF Co Ltd (027410 KS) / Bgf Retail (282330 KS) stub trade is at a 4.38% loss. Price ratio is still well below -1 σ. It is actually at a new yearly low. Holdco discount now stands at 48.55% to NAV.

Holdco price discount is too harsh. It’d be too tempting to pass up. An estimated 1.5~2%p difference in dividend yield must be pushing up price ratio soon.

I still believe below -1 σ wouldn’t last for as long as it used to. I’d hold onto this position a bit longer with a 10% loss cut.

The company forecasts an operating profit of Y55bn this year, the consensus is for Y57bn which is not unreasonable as management want to hold profits back. Next year assuming they make about Y64bn, the shares are on about 19x. With long term profits growth expected, and a good shareholder return policy this is a great domestic long term BUY. BUY into recent weakness. Foreigners own 24% of this name.

Dena Co Ltd (2432 JP) used to be the GO-GO internet stock for both retail and institutional investors in Japan during the previous bull run before 2008 and trading at 40-50x PER. The multiples have since then collapsed to 10-20x PER although the business prospect remains solid if not better. Benefiting from the increasing regulation in China, DeNA signed an agreement with Tencent Holdings (700 HK) to distribute Arena of Valor in Japan which will boost revenue and improve margin. At 14x PER and 1.2x PBR, DeNA looks attractive.

CMGE is an intellectual-property (IP) oriented mobile game operator. The company delisted from Nasdaq in 2015 and tried to do a backdoor listing on Shenzhen Exchange in late 2015 but it was canceled due to unfavorable market condition. It is now trying to list on the Hong Kong Exchange when the sentiment is poor due to the game approval suspension.

In this insight, we will take a look at the financial performance, key operating metrics, and analyze its games pipeline.