In this briefing:

- Are Chip Oligopolies Real?

- Global Banks: Some New Year Pointers

- Extraordinary Fiscal and Monetary Policies Have Disrupted the Global Economy

- M1 Offer Despatched – Dynamics Still Iffy

- ASIC Review of Allocation in Equity Raising – Some Truths, Some Half-Truths – No Improvements

1. Are Chip Oligopolies Real?

In the semiconductor industry, particularly in the DRAM sector, there has been significant consolidation leading some to hypothesize that there’s now an oligopoly that will cause prices to normalize and thus end the business’ notorious revenue cycles. Here we will take a critical look at this argument to explain its fallacy.

2. Global Banks: Some New Year Pointers

Here is a look at how regions fare regarding key indicators.

- PH Score = value-quality (10 variables)

- FV=Franchise Valuation

- RSI

- TRR= Dividend-adjusted PEG factor

- ROE

- EY=Earnings Yield

We have created a model that incorporates these components into a system that covers>1500 banks.

3. Extraordinary Fiscal and Monetary Policies Have Disrupted the Global Economy

In their public presentations, central banks seem to be contemplating the use of neutral interest rates (r*) in addition to unemployment/inflation theories. R* has the advantage of appearing to be subject to mathematical precision, yet it’s unobservable, and so unfalsifiable. Thus, it permits central banks to present any policy conclusion they want without fear of verifiable contradiction. R* is the policy rate that would equate the future supply of and demand for loans. It rises and falls as an economy strengthens and weakens. Long-term observation during the non-inflationary gold standard, period indicated that r* in an average economy was 2% plus, which would become 4% plus with today’s 2% inflation target. The Fed may soon end this tightening cycle with the fed funds rate at or near 2¾%, which would be r* if the rate of lending and borrowing in America remained stable thereafter. Rising (falling) lending would indicate a higher (lower) r*.

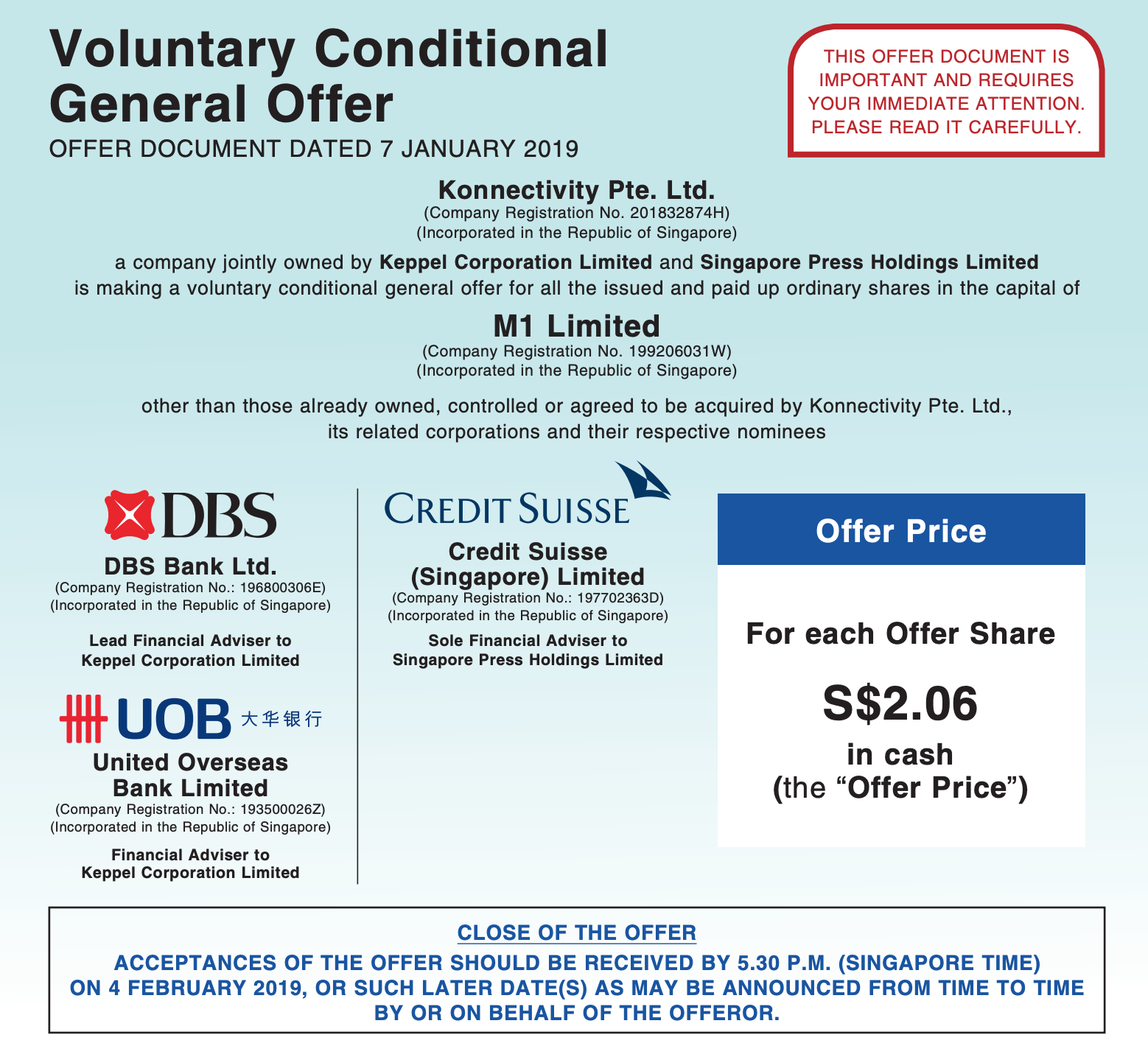

4. M1 Offer Despatched – Dynamics Still Iffy

On January 7th after the close of trading, Konnectivity Pte. Ltd officially announced the launch of its Offer to by M1 Ltd (M1 SP).

The closing date, as clear there, is 4 February.

After three-plus months of speculation that Axiata Group (AXIATA MK) was unhappy with the price and might make a counter-offer, no offer has been forthcoming.

After I wrote on the 2nd in M1 Offer Coming – Market Odds Suggest a Bump But… that the reward/risk did not look that great, shares drifted downward from the S$2.09-2.11 area and into the afternoon of the 7th, traded in the S$2.05-2.07 range, which was the first time in months the shares had traded at or below the prospective offer price.

Some 20mm+ shares (5.5% of the shares out other than the three major holders) traded between 3pm Singapore time on the 7th and a few minutes after the open the day after the announcement. Then part-way through the day, someone bought a large number of shares lifting the share price two spreads for a while. Since then, the shares have settled back down to the $2.07-2.08 range.

Depending on your opinion of the likelihood of a bump, your execution strategy will differ. It’s still not clear that a bump or counterbid will be forthcoming, but at S$2.07, the risks are better than they were higher.

5. ASIC Review of Allocation in Equity Raising – Some Truths, Some Half-Truths – No Improvements

Over 2017-18, the Australian Securities & Investments Commission (ASIC) undertook a review of allocation in equity raising transactions. The review involved large and mid-sized licensees (brokers), Issuers, International investors and other international regulators. The results of the review were published by ASIC in Dec 2018. This insight highlights some of the key findings.

It’s good to see that some of the standard practices of banks allocating more to existing clients and participants of earlier deals have at least been acknowledged. Even though some institutional investors have outright labelled the allocation process as a “black box”, ASIC doesn’t seem to want to do much about it.

The area where ASIC is more concerned is the messaging to investors which highlights the different definitions of “well-covered” across banks. Although, the banks seem to have mislead the regulator on interpretation of “real-demand” with ECM bankers saying that all orders are taken at face-value. That raises a whole new level of questions on the messaging around demand for the deal.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.