In this briefing:

- Harbin Electric: The Price Is Not Right

- MYOB (MYO AU): Shareholders Are Caught Between a Rock and a Hard Place

- New Pride Rights Offer: Tempting but Tricky

- LG Chem Share Class: Another Pref to Watch as Div Yield Gap at 4Y High

- Daelim Industrial Share Class: One of Prefs to Arb Trade on Div Payout Record Date

1. Harbin Electric: The Price Is Not Right

As speculated in Harbin Electric Expected To Be Privatised, Harbin Electric Co Ltd H (1133 HK) has now announced a privatisation Offer from parent and 60.41%-shareholder Harbin Electric Corporation (“HEC”) by way of a merger by absorption.

The Offer price of $4.56/share, an 82.4% premium to last close, has been declared final. The price corresponds to the subscription of 329mn domestic shares (~47.16% of the existing issued domestic shares and ~24.02% of the existing total issued shares) @$4.56/share by HEC in January this year.

Of greater significance, the Offer price is a 37% discount to HE’s net cash of $7.27/share as at 30 June 2018. Should the privatisation be successful, this Offer will cost HEC ~HK$3.08bn, following which it can pocket the remaining net cash of $9.3bn PLUS the power generation equipment manufacturer business thrown in for free.

On pricing, “fair” to me would be something like the distribution of net cash to zero then taking over the company on a PER with respect to peers. That is not happening. It will be difficult to see how independent directors can justify recommending an Offer to shareholders at any price which gave cash less cavalier than cash.

Dissension rights are available, however, what constitutes a “fair price” under those rights, and the timing of the settlement under such rights, are not evident.

As all PRC approvals have been obtained, this transaction may complete earlier than prior mergers by absorption, which have taken 6-8 months from the initial announcement.

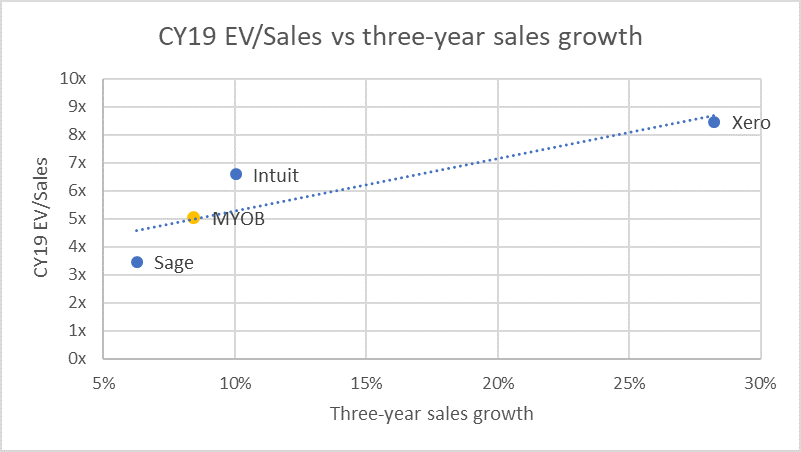

2. MYOB (MYO AU): Shareholders Are Caught Between a Rock and a Hard Place

On 24 December, MYOB Group Ltd (MYO AU) announced that it entered into a scheme implementation agreement under which KKR will acquire MYOB at $3.40 per share, which is 10% lower than 2 November offer price of A$3.77. MYOB claims its decision to recommend KKR’s lower offer was based on current market uncertainty, long-term nature of its strategic growth plans and the go-shop provisions of the deal.

We believe that KKR’s revised offer is opportunistic, but MYOB’s shareholders are caught between a rock and a hard place. Shareholders can take a short-term view and grudgingly accept the revised offer. Alternatively, shareholders can take a long-term view by rejecting the offer and hope MYOB’s strategic growth plans and a market recovery can reverse the inevitable share price collapse.

3. New Pride Rights Offer: Tempting but Tricky

- New Pride Corp (900100 KS) announced a ₩36.2bil rights offer. This is a public offering, so there won’t be subscription rights to trade. Pricing will be done as 3-day VWAP on Jan 9~11 at a 30% discount.

- Supposedly, we can have ample opportunity to arb trade. This may be what the company is hoping. Simply, we wait until Jan 16~17 (subscription period) and see the spread. At this much discount, there must be a huge spread opening.

- Proration risk can be much more annoying than a usual stockholder offering. In the previous public offering event by New Pride, subscription rate went as high as 370 to 1. It should be way much lower this time. But still this is risky enough.

4. LG Chem Share Class: Another Pref to Watch as Div Yield Gap at 4Y High

- LG Chem Ltd (051910 KS) 1P is now at a 44.20% discount to Common. Div would be the same as last year of ₩6,000 despite lower earnings. Payout would be 28%. Div yield for Common will be 1.68%, and 3.03% for 1P. Div yield difference stands at 1.35%p. This is a record high at least since 2014.

- 1P’s discount to Common is hovering at the highest level in 2 years. On a 20D MA, it is close to +1 σ. It may not be tempting enough for those seeking high yields. Otherwise, this’d be worth giving it a shot. Liquidity shouldn’t be an issue. Short recovering risk on Common also appears to be limited.

5. Daelim Industrial Share Class: One of Prefs to Arb Trade on Div Payout Record Date

- Daelim Industrial (000210 KS) is one of the main targets of local activist movement. This makes a setting for higher dividends. Common div yield to 1.58% and Pref to 4.18%. Difference is 2.59%p. This is the widest gap in many years.

- Pref is currently at a 60.89% discount to Common. Among those > ₩100bil MC prefs, it is the second highest discounted pref, only behind CJ Cheiljedang 1P (097955 KS). Local street expects at least ₩1,600 div per share. This should be a conservative estimate. On a 20D MA, Pref is above +1 σ.

- Dec 26 is record date of dividend payout. I expect a price catchup movement tomorrow in favor of Pref. I’d go long Pref and short Common as early in the morning as possible.