In this briefing:

- ZOZO: The Kingmaker Abandons His King

- GMO.internet FY2018 Results – The Shareholder’s [Re]Turn

- Recruit Holdings Reports Strong 3Q Results; Remains Expensive

- Daiwa House REIT Placement – Well-Flagged but Barely Accretive to DPU

- GMO Internet Reports Solid FY12/18 Despite Heavy Losses Incurred in Crypto Mining Business

1. ZOZO: The Kingmaker Abandons His King

United Arrows’ (7606 JP) decision to cancel its e-commerce services contract with ZOZO Inc (3092 JP) was not a surprise at all but could not have come at a worse time. While a move to direct operation of its online store was expected, United Arrows did not have to choose a moment when Zozo’s stock was collapsing. That it did shows how much cooler relations are between the two firms, a critical development given United Arrows was the principal reason for Zozo’s emergence as the leading fashion mall in the early 2000s.

United Arrows will still be selling through Zozotown and its president last week praised Zozotown’s capacity to bring new and younger customers to its brand. The bigger problem is that United Arrows relies less and less on sales from Zozotown each year and more from its own online store – direct e-commerce sales have increased from 20% of all e-commerce sales in FY2016 to 27% in 9M2018.

At Baycrews, another leading merchant on Zozotown, 50% of e-commerce sales are from its own online store, up 12 percentage points in two years.

A further problem is that other merchants are leaving. We reported before that Onward’s departure, while significant, is less of a threat than it might first appear given that Onward already garners 70-75% of sales from its own store so it did not cost much to leave Zozo.

However, another big retailer, Right On, also quit Zozo last month despite the fact that more than 50% of its online sales come from Zozo and it has intermittently been one of the top 20 merchants on Zozo. Right On has struggled in recent years, so leaving Zozo cannot have been an easy decision, suggesting just how seriously upset it was.

Other merchants are likely to view these departures with some concern. Six months ago, the idea of quitting Zozo was not even a remote thought in Japan’s fashion industry but it is now a lively subject of discussion. While most merchants will stay, the recent high profile departures will make a threat to leave look much more real, giving merchants more leverage to negotiate, particularly on Zozo’s take rates.

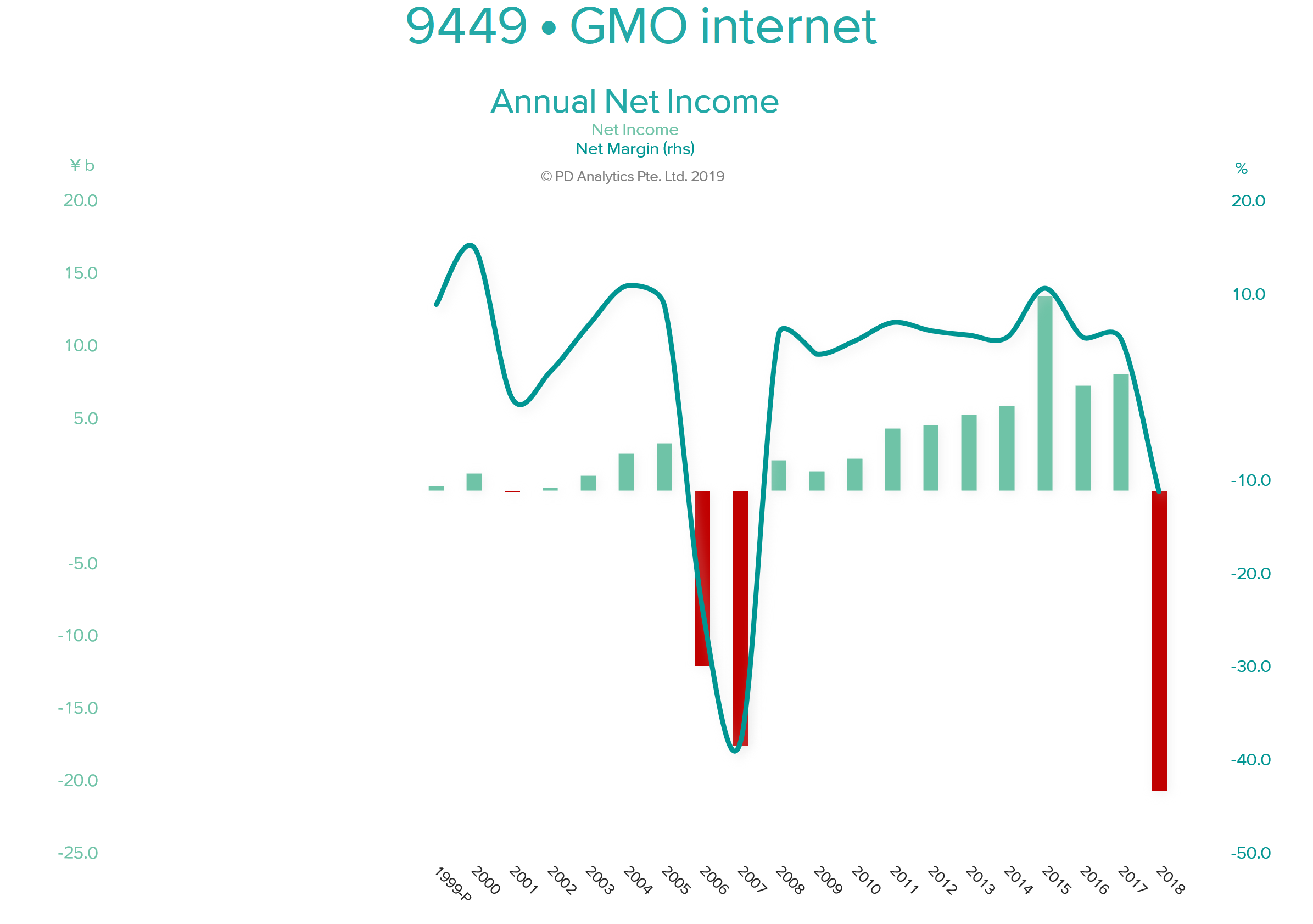

2. GMO.internet FY2018 Results – The Shareholder’s [Re]Turn

GMO internet (9449 JP) released 2018 full-year results in 12th February. 2018 was a turbulent year for the company as it ‘surfed’ the cryptocurrency wave. The subsequent downfall was swift and brutal. However, the company deserves some plaudits for cutting its (substantial) losses and attempting to move on (albeit somewhat half-heartedly). Unfortunately, GMO-i has ‘form’ in writing off large losses as shown above. The positive consequence of this saga is a renewed commitment to return value to shareholders with a stated aim of returning 50% of profits. Two-third of that goal is to be met by quarterly dividends, with the balance allocated to share repurchases in the following year.

Having royally ‘screwed up’ with ‘cryptocurrencies’, and trying the patience of remaining shareholders yet again, this policy is to be commended, particularly if more attention is paid to generating the wherewithal to meet the 50% without raiding the listed subsidiaries’ ‘piggy bank’. Apart from the excitement that this move has generated and the year-long support this buying programme will provide to the share price, our two valuation models, find little in the way of further upside potential.

We remain sceptical of investing in GMO-i over the long-term and prefer GMO Payment Gateway (3769 JP) – the best business in the GMO-i ‘stable’ – but consider GMO-PG’s stock overvalued at 57x EV/OP.

3. Recruit Holdings Reports Strong 3Q Results; Remains Expensive

Recruit Holdings (6098 JP) reported its 3Q FY03/19 financial results on Wednesday (13th February). Recruit’s revenue and EBITDA were up 6.0% YoY and 11.1% YoY respectively in 3Q FY03/19. This was mostly due to 1) consolidation of the results of Glassdoor Inc. (the company which operates the employment information website glassdoor.com), 2) steady growth in Japanese staffing operations and 3) growth in beauty and real estate app users during the quarter, partially offset by slowdown in global recruitment activity.

Despite its strong 3Q results and steady topline and bottom line growth over the forecast period, at a FY2 EV/EBITDA multiple of 16.0x, Recruit doesn’t look particularly attractive to us. Recruit’s internet advertising business and employment business peers, Yahoo Japan (4689 JP) and Persol Holdings (2181 JP) are trading at FY2 EV/EBITDAs of 6.8x and 7.5x respectively.

| FY03/18 | FY03/19E | FY03/20E |

Consolidated Revenue (JPYbn) | 2,171 | 2,327 | 2,478 |

YoY Growth % | 11.9% | 7.2% | 6.5% |

Consolidated EBITDA (JPYbn) | 258 | 288 | 312 |

EBITDA Margin % | 11.9% | 12.4% | 12.6% |

4. Daiwa House REIT Placement – Well-Flagged but Barely Accretive to DPU

Daiwa House Reit Investment (8984 JP) (DHR) is raising about US$329m in its placement to fund the acquisition of properties.

The deal scores well on our framework owing to strong price and earnings momentum. The assets to be acquired are a good mix of logistics, retail, and hotel.

However, the properties to be acquired mostly have an NOI yield lower than the average NOI yield of DHR’s existing assets in the respective asset classes. Despite increasing the portfolio value by almost 10%, the ten properties are only expected to be 1.37% accretive to DPU.

That said, DHR’s acquisition has been well-flagged as it was highlighted in its September presentation.

5. GMO Internet Reports Solid FY12/18 Despite Heavy Losses Incurred in Crypto Mining Business

GMO Internet, Inc. (9449 JP) announced its consolidated financial results for its full-year FY12/18 yesterday (12th February). Despite heavy losses incurred in the cryptocurrency mining business in FY12/18, GMO managed to achieve a solid year with 20% YoY growth in top-line alongside a 23.5% YoY growth in operating profits. Excluding the crypto losses, the operating profit increased 35.7% YoY, with an OPM of 13.2% compared to 11.4% reported a year ago. For the full-year, the company has reported a net loss of JPY20.7bn as opposed to a net profit of JPY8bn in FY12/17, blaming the crypto losses for the decline. For FY12/18, the management has proposed a dividend of JPY29.5 per share (compared to JPY23 paid in FY12/17) in spite of reporting net losses for the fiscal year. Further, the company has also allocated JPY1.36bn (equivalent to 0.7% of outstanding shares at the current price) for share repurchases in FY2019.

JPY (bn) | FY12/17 | FY12/18 | YoY Change | FY12/18 Excluding Crypto | FY12/18 Excl. Crypto Vs. FY12/17 | Consensus | Company Vs. Consensus |

Revenue | 154.3 | 185.2 | 20.1% | 180.9 | 17.3% | 183.3 | 1.0% |

Operating Profit | 17.6 | 21.8 | 23.5% | 23.9 | 35.7% | 22.8 | -4.5% |

OPM | 11.4% | 11.8% |

| 13.2% | 12.4% |

| |

Net Profit | 8.0 | -20.7 | -357.9% | 8.4 | 4.1% |

|

|

GMO is currently trading at JPY1,741 per share which we believe is undervalued compared to its combined equity stake in 8 listed subsidiaries. The company share price has lost more than 40% since it peaked in June last year due to the negativity surrounding its cryptocurrency and mining segment. However, we believe further downside is limited as the company has closed down a majority of its mining related business which weighs very little on the consolidated performance of the company. Further, the company’s key businesses, Internet Infrastructure, Online Advertising & Media and Internet Finance generate solid recurring revenues, which should help the company achieve strong growth. Following its earnings announcement, the share price gained 5.6% from the previous days close.

Get Straight to the Source on Smartkarma

Smartkarma supports the world’s leading investors with high-quality, timely, and actionable Insights. Subscribe now for unlimited access, or request a demo below.