In this briefing:

- Okinawa Cellular (9436 JP): Warm Tropical Breezes with KDDI

- GMO Internet (9447 JP) – Grossly or Modestly Overrated?

- 58.com Inc. (NYSE: WUBA): Regulatory Pressure Has Long Term Implications

- MYOB (MYO AU): Shareholders Are Caught Between a Rock and a Hard Place

- Infosys Ltd (INFO IN): Another Buyback Coming? Not a Bad Idea, but How Much It Can Really Help?

1. Okinawa Cellular (9436 JP): Warm Tropical Breezes with KDDI

As the colder winter weather is felt and the icy blast of industry tariff cuts continues to chill sentiment, we seek some respite (at least mentally) in the warmer climes of Okinawa. Okinawa Cellular is a unique company. It’s a small cap telecom network operator in Japan with a focus on the sub-tropical islands of Okinawa Prefecture. As part of the KDDI group, the company benefits from its parent’s economies of scale, but with its local presence, it also benefits from being the hometown hero.

Because the stock is relatively small, from an investment perspective it runs into liquidity constraints that the other telcos do not have, so it’s a different type of investment but one that we think is worth looking at. Over the past 12 months Okinawa Cellular’s stock has fallen by 12.3%, but over the past year the stock has delivered a return in the middle of its peer group and has outperformed the broad TOPIX by about 5.5%. Like most telcos, Okinawa Cellular is also ramping its dividend payments, and the current yield is about 3.5%.

2. GMO Internet (9447 JP) – Grossly or Modestly Overrated?

Source: Japan Analytics

THE GMO INTERNET (9449 JP) STORY – GMO internet (GMO-i) has attracted much attention in the last eighteen months from an unusual trinity of value, activist and ‘cryptocurrency’ equity investors.

- VALUE– Many traditional, but mostly foreign, value investors have seen the persistent negative difference between GMO-i’s market capitalisation and the value of the company’s holdings in its eight listed consolidated subsidiaries as an opportunity to invest in GMO-i with a considerable ‘margin of safety’.

- ACTIVIST – Since July 2017, the activist investor, Oasis, has waged a so-far-unsuccessful campaign with the aim of improving GMO’s corporate governance, removing takeover defences, addressing a ‘secularly undervalued stock price we are not able to tolerate’ (sic), and redefining the role and influence of the company’s Chairman, President, Representative Director and largest shareholder, Masatoshi Kumagai.

- ‘CRYPTO!’ – In December 2017, GMO-i committed to spending more than ¥35b or 10% of non-current assets. The aim was threefold: to set up a bitcoin ‘mining’ headquarters in Switzerland (with the ‘mining’ operations being carried out at an undisclosed location in Scandinavia), to develop proprietary state-of-the-art 7nm-node ‘mining chips’, and, in due course, to sell GMO-branded and developed ‘mining’ machines. The move was hailed in the ‘crypto’ fraternity as GMO-i became the largest non-Chinese and the first well-established Internet conglomerate to make a major investment in ‘cryptocurrency’ infrastructure.

OUTSTANDING – Following the December 2017 announcement, trading volumes spiked into ‘Overtraded’ territory – as measured by our Volume Score. Many investors saw GMO-i shares as a safer way of gaining exposure to ‘cryptocurrencies’, even as the price of bitcoin began to subside. By early June 2018, GMO-i’s shares had reached a closing price of ¥3,020: up 157% from the low of the prior year and outperforming TOPIX by 135%. Whatever the primary driver of this outstanding performance, each of our trio of investor groups no doubt felt vindicated in their approach to the stock.

CRYPTO CLOSURE – On December 25th 2018, GMO-i’s shares reached a new 52-week low of ¥1,325, a decline of 56% from the June high. Year to date, GMO-i shares have now declined by 31%, underperforming TOPIX by nine percentage points. On the same day, GMO-i announced that the company would post an extraordinary ¥35.5b loss for the fourth quarter, incurring an impairment loss of ¥11.5b in relation to the closure of the Swiss ‘mining’ headquarters and a loss of ¥24b to cover the closure of the ‘mining chip’ and ‘mining machine’ development, manufacturing and sales businesses. GMO-i will continue to ‘mine’ bitcoin from its Tokyo headquarters and intends to relocate the ‘mining’ centre from Scandinavia to (sic) ‘a region that will allow us to secure cleaner and less expensive power supply, but we have not yet decided the details’. Unlisted subsidiary GMO Coin’s ‘cryptocurrency’ exchange will also continue to operate, and the previously-announced plans to launch a ¥-based ‘stablecoin’ in 2019 will proceed. In the two trading days following this announcement, the shares have recovered 13% to ¥1,505.

RAIDING THE LISTCO PIGGY BANK – As we shall relate, this is the second time since listing that GMO-i has written off a significant new business venture which the company had commenced only a short time before. In both cases, the company was forced to sell stakes in its listed consolidated subsidiaries to offset the resulting losses. On this occasion, the sale of shares in GMO Financial (7177 JP) (GMO-F) on September 25 2018, and GMO Payment Gateway (3769 JP) (GMO-PG) on December 17 2018, raised a combined ¥55.6b and, after the deduction of the yet-to-be-determined tax on the realised gains, should more than offset the ‘crypto’ losses. According to CFO Yasuda, any surplus from this exercise will be used to pay down debt. Also discussed below and in keeping with this GMO-i ‘MO’, in 2015, the company twice sold shares in its listed subsidiaries to ‘smooth out’ less-than-desirable operating results.

In the DETAIL section below we will cover the following topics:-

I: THE GMO-i TRACK RECORD – TOP-DOWN v. BOTTOM UP

- BOTTOM LINE No. 1: NET INCOME

- BOTTOM LINE No.2 – COMPREHENSIVE INCOME

II: THE GMO-i BUSINESS MODEL – THROWING JELLY AT THE WALL

III: THE GMO-i BALANCE SHEET – NOT SO HAPPY RETURNS

IV: THE GMO-i CASH FLOW – DEBT-FUNDED CASH PILE

V: THE GMO-i VALUATION – TWO METHODS > SAME RESULT

- VALUATION METHOD No.1 – THE ‘LISTCO DISCOUNT’

- VALUATION METHOD No.2 – RESIDUAL INCOME

CONCLUSION – For those unable or unwilling to read further, we conclude that GMO-i ‘rump’ is a grossly-overrated business. Despite having started and spun off several valuable GMO Group entities, CEO Kumagai bears responsibility for two decades of serial and very poorly-timed ‘mal-investments’. As a result, the stock market has, except for the ‘cryptocurrency’-induced frenzy of the first six months of 2018, historically not accorded GMO-i any premium for future growth, and has correctly looked beyond the ‘siren song’ of the ‘HoldCo discount’. According to the two valuation methodologies described below, the company is, however, fairly valued at the current share price of ¥1,460. Investors looking for a return to the market-implied 3% perpetual growth rate of mid–2018 are likely to be as disappointed as those wishing for BTC to triple from here.

3. 58.com Inc. (NYSE: WUBA): Regulatory Pressure Has Long Term Implications

● We notice that Anjuke’s Oct.-Nov. traffic declined. We attribute this decline to the tightening of registration requirement in various cities, which will reduce the number of housing leads on WUBA platform;

● We, however, believe new home business will deliver strong revenue for WUBA this year, contributing Rmb2bn in revenues by our estimate;

● We rate the stock Buy and cut TP from US$84 to US$79.

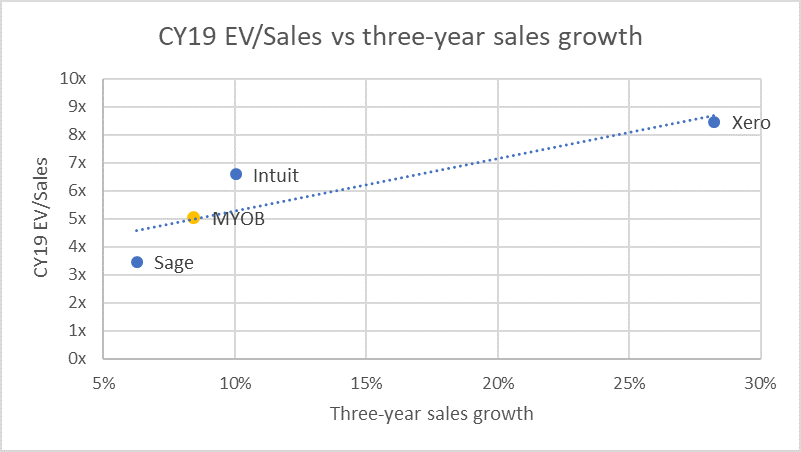

4. MYOB (MYO AU): Shareholders Are Caught Between a Rock and a Hard Place

On 24 December, MYOB Group Ltd (MYO AU) announced that it entered into a scheme implementation agreement under which KKR will acquire MYOB at $3.40 per share, which is 10% lower than 2 November offer price of A$3.77. MYOB claims its decision to recommend KKR’s lower offer was based on current market uncertainty, long-term nature of its strategic growth plans and the go-shop provisions of the deal.

We believe that KKR’s revised offer is opportunistic, but MYOB’s shareholders are caught between a rock and a hard place. Shareholders can take a short-term view and grudgingly accept the revised offer. Alternatively, shareholders can take a long-term view by rejecting the offer and hope MYOB’s strategic growth plans and a market recovery can reverse the inevitable share price collapse.

5. Infosys Ltd (INFO IN): Another Buyback Coming? Not a Bad Idea, but How Much It Can Really Help?

As per reports, Infosys Ltd (INFO IN) may consider a proposal for a share buyback of $1.60 billion very soon. The buyback announcement is likely to be made on January 11 when the company board meets to consider the 3Q FY19 results. Before this, in November 2017, Infosys Ltd (INFO IN) had announced a buyback and spent Rs130 bn to buy a total of 113mn equity shares. This fresh buyback could be an important development and could be an important support for the stock, it is also sensible for other reasons.

There are no major acquisitions in recent times by Infosys Ltd (INFO IN) and if this is likely to be the trend for near future, share buyback is not a bad idea. The company is still struggling with some of the legacy issues and the priority as of now is to streamline the organic growth. We think Infosys Ltd (INFO IN) is also cautious with inorganic growth opportunities as the company had serious issues with acquisitions in the past. What could be another key driver behind this is that in valuation terms, Infosys Ltd (INFO IN) is not very expensive.