By way of introduction, I have now been posting here at Smartkarma for almost exactly 18 months, mostly writing about transportation, logistics, and tourism in Greater China and elsewhere in the region.

But I got my start in Asian equity research almost a quarter of a century ago in Taiwan. I had been working as an analyst at a corporate — a US-based container shipping company that was later acquired by Neptune Orient Lines Ltd (NOL SP) — but I had grown impatient with the slow pace of change at the company, and decided to head to Hong Kong (where a college roommate had offered a place to stay) to begin looking for…something.

About a month later I landed a job as the shipping analyst at a large brokerage firm in Taipei that was half-owned by the now-infamous Peregrine Securities (raise your hand if you remember Peregrine!). I admit I knew nothing about equity research at the time, but I did know something about how container shipping worked, and that was enough to endear me to a very small group of investors who actually cared about the sector.

When a similar position opened up at SG Warburg (another name from ancient history) a few blocks away, I quickly and happily moved on from my brief stint at Peregrine. I had grown tired of witnessing colleagues break down in tears on a weekly basis — not an exaggeration! — often due to the Managing Director’s, shall we say ‘volatile’ personality and management style. Even my inexperienced eyes could see that SG Warburg’s Taipei office ran like a fine Swiss watch by comparison — and this was before the actual arrival of SwissBank and, later, UBS Group AG (UBSG VX) on the scene.

At SG Warburg (later SBC Warburg, then SBC Warburg Dillon Read, then UBS Warburg Dillon Read, and finally just…UBS) I was asked to cover Taiwan’s listed shipping and airline companies — I believe there were eight at the time. But as an added bonus I was also asked to cover other local cyclical sectors, including steel, paper, and the local auto assembly companies. In other words, I was given the “opportunity” to cover the deeply un-sexy names none of the more senior analysts at the firm wanted to bother with!

After about four years in that position I transferred to the US with UBS to cover freight transportation on their US equity research team in New York. This mostly consisted of following larger names like Fedex Corp (FDX US), United Parcel Service Cl B (UPS US), and the US railroads. And then a few years after that, I went to work on the buy-side as a generalist industrials analyst for a series of US-based but Asia-focused Long / Short hedge funds.

And that pretty much brings us to 2015, when I began writing independent research on Asian equities, and trying (without much success) to market it to institutional investors in the US.

Regrets? I’ve Had a Few: Working as a Sell-Side Shipping Analyst

For the most part, I have very fond memories of my time as a sell-side analyst, particularly the years I spent in Taiwan with SG Warburg / UBS. Still, it wasn’t all fun and games, and certainly I share many of the complaints most sell-side analysts have: subtle pressure from Corporate Finance to maintain positive views on their clients’ shares; a cumbersome and time-consuming editing and publishing process; a rigid requirement that the analyst publish an exhaustive initiation note followed by regularly quarterly updates (usually to the detriment of more interesting idea-oriented pieces).

But in addition to these common complaints, there were other challenges I view as specific to covering cyclicals like shipping:

For long stretches of time, many of the traditional cyclical stocks I covered would report depressed earnings or losses, and their market capitalization would in response often shrink to levels that pushed them off the radar screens of long-only institutional investors. In other words, although the stocks in these sectors certainly deserved at least a baseline level of attention from the analyst throughout the cycle, there were long periods where they really did not bear full-time coverage.

Many of the companies within these traditional cyclical sectors — shipping and steel stand out — are truly global industries. But too often we as analysts covered them as ‘local companies’, and as such we were not encouraged to work with colleagues in other geographic markets who covered similar companies.

Many of the traditional cyclicals I used to cover have been around for a century or more and the pace of change within these industries is often glacial. I remember taking up coverage of the four large US railroads in 1999 and thinking to myself, ‘is there anything new or interesting to say about these companies, some of which have been around since the US Civil War’?

On joint marketing trips with colleagues who covered larger, more popular sectors (tech, financials) I usually ended up with the role of bag-carrier or hailer-of-taxicabs, sometimes given just a few seconds to present my ‘best ideas’ within my coverage. Not that I hold a grudge!

How Smartkarma Has Changed the Game for This Analyst

On the recommendation of an old SG Warburg friend who worked on the buy-side in Singapore, I got in touch with the folks at Smartkarma in Spring 2016 and I’ve been publishing my work there ever since.

Posting my work at Smartkarma addresses some of the mainstream complaints many former sell-side analysts have: there is no pressure from Corporate Finance to temper one’s views on a stock; the editing and publishing process is intuitive and streamlined; and analysts aren’t required to first publish a 60-page initiation note (and then regularly quarterly updates) before they express their views on a sector or an individual name.

But Smartkarma also addresses some of the frustrations specific to this analyst who was once ‘stuck’ covering traditional cyclical names like shipping and steel:

Analysts at Smartkarma can devote their time and resources to covering sectors, companies, and themes that are dynamic and topical and thus likely to generate investable ideas for readers, even if these are only tangentially related to their backgrounds. Analysts need not wait for the cyclical names under their coverage to turn (for better or worse) before publishing; they can instead focus on ideas outside their core coverage that are actionable, and thus worth analyzing, now.

Unbound by geographic restrictions on coverage, analysts here at Smartkarma can take the appropriate Global or Regional view of a sector.

Analysts from different geographical markets or different sectoral backgrounds can also freely collaborate to generate ideas here on Smartkarma, as noted by Douglas Kim in his piece.

In short, analysts (‘Insight Providers’ in Smartkarma parlance) who post their ideas here are free to break out of geographic or sectoral ‘silos’ and direct their time and energy to areas they feel are mostly likely to generate winning ideas. Ultimately, resources are directed to areas where they are mostly likely to generate optimal returns (both for Smartkarma’s Insight Providers and for subscribers). For those of us who used to focus on traditional cyclicals, this flexibility is extremely valuable. For those who cover growth sectors like technology, which is subject to constant change, this freedom may be less noticeable.

Confessions of a Shipping Analyst: Voyage of the Damned, Asian Equity Research Version

Blessed are those who can laugh at themselves, for they shall never cease to be amused.

As an analyst, five analytical practices that are common place but need to be changed, in my view are:

Focussing on accounting profits as opposed to cash flows

Inconsistent treatment of on-balance sheet and off-balance sheet debt

Deducting readily marketable inventory from debt, thereby under-stating financial leverage

Focussing on share of net income rather than dividends from associates and

Companies maintaining investment portfolios that are opaque and which often generate lower returns than that of the core business and weighted average cost of capital

Read the unabridged insight for an analysis of and real-life examples of the above-mentioned issues.

Detail

The objective of a Smartkarma insight is usually to help investors make optimal decisions. But I thought I’ll use this platform to solicit responses from fellow analysts and astute investors to five issues that I have not been able to get my head around through my analytical career.

Issue #1: The Income Statement Fixation

One of the parameters of a company’s performance analysts are expected to opine about is a company’s profitability. Financial statements across the globe consist of the income statement, balance sheet and cash flow statement. The funny thing about income statement is that revenues represent sales income that is contractually due to a company but not necessarily collected as cash during the period of reporting, expenses that a company has contractually incurred to generate the revenues it has reported but has not necessarily paid, interest expenses payable on account of the existing businesses and not on account of the capital projects underway…The list goes on.

The income statement does have its utility in terms of “smoothing” a company’s performance, enabling a company to set aside funds for the replacement of plant and machinery that is subject to wear and tear due to the normal course of business aka depreciation, determining tax liability etc.

But what the income statement does not tell you is how much cash the business is generating. A much ignored gem and a more useful tool for analysts (in my view) is the cash flow statement. The list of companies that generate accounting profits (usually EBITDA and net income) but marginal to negative cash flow from operations (CFO) is endless. The financials of Singapore-based Olam International Ltd (OLAM SP) and Hong Kong-based Noble Group Ltd (NOBL SP) illustrate the disconnect between accounting profits and cash flows.

Figure 1

Issue #2: On and Off Balance Sheet Debt

Some companies opt to fund purchases of plant and machinery through debt, cash or a combination of the two. Other companies lease their assets. Several companies operate using a combination of owned and leased assets. The lease rentals are recorded as an expense. Why is there a tendency to estimate financial leverage using on balance sheet debt and ignore the off balance sheet debt i.e. the debt equivalent of leases. There is a wide spread misconception of Singapore Airlines being in a net cash position, as is evident in this article and this one.

The businesses of companies whose business models integrate upstream and downstream operations and commodity traders tend to be working capital intensive. These companies may also hold high levels of readily marketable inventories (RMI). The companies in question and certain analysts argue that RMI, on account of its liquid nature, ought to be deducted from consolidated debt and hence, net financial leverage is lower.

This argument puzzles me. Are we evaluating companies as going concerns or in a liquidation scenario? As long as company is treated as a going concern,

The company requires those inventories to render its services,

Avails of inventory financing through banks, and

Pays interest on the consolidated debt, and not on consolidated debt less RMI.

Hence, is the high ratio of RMI to inventory a source of financial strength?

The spike in Noble Group’s CFO margin to 22% in Q3 2017 (Figure 1) from negative territory during six of the seven preceding quarters was driven by asset disposals including Noble Americas Corp that resulted in:

A working capital release of USD508.29 million driven by

An 86% decline in Q3 2017 revenues to USD1.47 billion over Q2 2017, and

Consolidated debt as of September 30, 2017 declining to USD3.59 billion, around USD1 billion lower than USD4.56 billion as of June 30, 2017

Asian commodity traders like Olam International and Noble Group and agri-business companies like Golden Agri Resources, Wilmar International and IOI Corporation seem to have a higher risk appetite than the global majors like Archer Daniels Midland Co (ADM US) and Bunge Ltd (BG US), who manage their working capital cycles efficiently. Hence, Archer Daniels Midland Co and Bunge Ltd maintain moderate financial leverage, i.e. the ratio of lease adjusted debt to EBITDAR (the sum of EBITDA and operating lease rentals) despite earning wafer thin EBITDA margins.

The following insights demonstrate how leverage may be understated by deducting RMI from consolidated debt.

Issue # 4: The Emperor’s New Clothes aka Acquisitions

Expensive, debt-funded, and unremunerative acquisitions have contributed to the weakening, if not downfall, of several well-regarded corporates. If companies treated such acquisitions (which companies have an amazing knack of making, at the peak of the price / business cycle) as associates, then the share of net income is reported in the income statement (once again…) and the dividends from associates in the cash flow statement.

While we analysts comment about the trend in the share of net income from associates and its impact on accounting profits, we seldom document the dividends these expensive acquisitions generate.

Issue #5: Opaque Investment Portfolios

Blue chip corporates and conglomerates including Genting Bhd (GENT MK) and Tata Group (1396Z IN)grow their financial investment portfolios over time. While the accounting policies of these companies comply with the requisite accounting standards, the disclosure regarding the composition and returns from these investment portfolios is inadequate. My guestimates indicate that the return from these investment portfolios may at times be lower than the CFO margin and weighted average cost of capital.

We analysts could sharpen our analysis in several other areas. Do highlight such issues by commenting on this insight. I’ll be happy to write a sequel to this insight analysing these topics.

True, the field is crowded, and fresh insights are hard to come by. Still, contrary to Douglas Kim’s argument, it’s not mid-caps, but large-caps, that offer profitable subject matter for research. The advantage for the truly independent researcher is that, while the usual corporate doors are quickly shut, there are plenty of other doors no one thinks of opening.

For independent research to be recognized as a credible alternative to sell-side research, it has to play in the same field where the big girls and boys play, and in equities, it is large cap research. There is ample space for unusual perspectives and more importantly critical commentary for enterprising analysts to standout in the faceless herd and do the profession proud.

The proliferation of independent research analysts in the capital market as a result of cost pressures in the industry and introduction of Mifid II in Europe post January 1, 2018 has provided greater flexibility for analysts as well as more variety for institutional clients. As price discovery for independent research remains a work-in-progress, analysts are examining the most cost-effective, value-added service to provide to institutional clients.

In this respect, Douglas Kim has written an in-depth, insightful and well received article, ““Confessions of an Independent Analyst” on Smartkarma, documenting his experience as an independent research analyst and possible strategies analysts can adopt to prosper from 2018 onwards. One aspect of his comprehensive article is to suggest emphasizing mid and small size company research with a focus on generating “great investment ideas,” instead of venturing into the crowded large cap research, which is dominated by the bulge bracket firms. He does acknowledge the trade-off in research to write on “higher market cap stocks which may generate more interest vs. differentiated research in writing about “undiscovered” investment plays.”

Midcap research has a charm of its own. The competition amongst analysts is less, and the thrill of uncovering hidden gems is alluring. However, just as sectors have their day in the sun and can languish in the dark and go into hibernation, the volatility in midcaps can be far more severe and the winters long and hard. Typically, midcaps are a product of a bull market, rising rapidly with generous doses of liquidity. But come a bear phase, and liquidity in stocks dries up as institutional interest wanes.Exiting stocks may not be possible on account of high impact cost. In such a phase, dedicated midcap analysts are left high and dry, while large cap sector analysts can still survive on maintenance research.

Generating great investment ideas is the Holy Grail for analysts, but consistently recommending great investment ideas is extremely difficult for a single analyst, unless the market is bullish and all stocks are on fire. In the rare instance of an independent analyst consistently picking winners, he/she might well decide that, rather labouring and framing a logical argument to convince others, investing in those ideas makes better sense. Midcaps are also high risk, and their revenue can be volatile as they typically lack broad-based stability. Midcap analysts can earn a name recommending winners but lose credibility in any downturn.

No doubt, recommending winners is the ultimate objective for analysts. However, in the real world, to be recognized and appreciated as an analyst, it is more practical to consistently produce interesting, original insights on stocks, industries and the economy, defying the consensus when necessary. Framing a logical, well-researched angle is within the expertise of the analyst, but to achieve consistency in predicting winners and losers and the future direction of stock prices, which are influenced by a host of factors, is beyond the analyst’s control. Equity research analysts typically have their share of multi-baggers and stocks where their calls go horribly wrong, and that is par for the course. And while honest analysts make a genuine attempt to get their calls right, it is difficult to be consistent in getting calls right.

It is this writer’s contention that independent analysts, in recommending large cap stocks, should focus on providing unusual insights on the company, industry and the economy. Although large cap research is a highly competitive space, there is adequate room for providing critical research, an area which is largely and deliberately ignored by most analysts. Bloomberg’s Gadfly estimates that between “50 and 70% of a senior analyst’s time is spent on corporate access.” Unsurprisingly, then, not only does critical corporate analysis become a no-go area for most large cap analysts in bulge bracket firms, but also less time is devoted for thorough analysis. As a result, most large cap research has become an extension of corporate public relations in enhancing the image of the corporate. As Howard J Klein rightly points out in his erudite insight in the casino sector, sell-side analysts avoid asking about tough issues lest they injure ongoing relationships with corporate contacts they need to do their jobs. This is entirely understandable. But the downside is that the process tends to produce far too many softball questions in order to maintain a general air of civility and nurse relationships.

The business media are no better than most sell-side research. In India, the business media are focused on getting exclusive interviews with large cap Chief Executive Officers (CEOs) and Chief Financial Officers (CFOs). Anchors/editors hand over “Best CEO” and “Best Corporate” awards to large companies, and organise corporate round table conferences. And, of course, their business model is dependent on corporate advertising. As a result, in India, at least, investigative business reporting on large companies is virtually non-existent in the corporatized business media.

This is fertile, virgin territory for independent researchers to showcase their expertise in providing critical analysis: on corporate strategy, exposing senior management incompetence, accounting transparency, and the likely chinks in the layered armour of large corporates. It is highly unlikely that institutional investors will approach independent analysts to fix meetings with large corporates, and hence the corporate contact loss to an independent analyst is far less. Large corporates may, in retaliation, boycott the critical independent analyst from their regular news flow; this is inconvenient, but an experienced analyst normally should have developed multiple sources in the companies and industry that he/she covers to compensate for the loss of official contact. Moreover, the mandatory disclosures and regular corporate analysts’ presentations provide adequate information on developments for independent analysts to be kept informed without having corporate access. ICICI Bank Ltd (ICICIBC IN), India’s second largest private sector bank by assets has refused to interact with this writer for nearly two decades post the publication of a critical research note in January 1999, and Axis Bank Ltd (AXSB IN), India’s third large private bank by assets in June 2017, declined to entertain any further queries from this writer. The management boycott has not prevented this writer from regularly publishing (here and here) critical, non-consensus research on both these banks which has been appreciated by not only institutional investors but also by insiders in these banks.

In large cap research, institutional investors are not only looking for investment ideas but are also looking for unusual insights contributing to earnings’ drivers. And since considerable sell-side coverage is flattery disguised as research, there is a huge, unsatiated appetite for well documented, critical research. Unfortunately, over time, sell-side research has got used to being spoon-fed (instead of the rigours of data analysis and reading the fine print) by investor relations (IR) executives and CFOs of the companies they cover, and loss of official corporate contact cuts off any flow of information, as analysts did not develop alternative sources of information within these companies or from the industry. In his over 20 years of experience, this writer, as a sector analyst and head of research had noticed a reluctance by analysts to develop contacts such as labour union leaders, corporate whistle-blowers, regulators and auditors – interacting with such individuals can provide an alternative to the image projected by industry chieftains. Such management-spoon-fed individuals have no future as independent analysts, as sell-side research will provide corporate access and regurgitate management commentary to institutional clients.

Financial Times All-World Index

Source: Financial Times

Equity analysts, in general, are more comfortable presenting bullish arguments and normally ‘Buy’ recommendations outnumber ‘Sell’ calls. Even during bearish phases, the analyst community remains optimistic and expects the phase to be short-lived – near term hiccups but long term growth story intact is the common message articulated. On account of global liquidity and some recent mild economic revival, global equity indices have been on an upswing since early 2016. It is, therefore, no surprise that even on Smartkarma, a platform dedicated for independent research analysts, bullish views are in the majority, while bearish views remain in the minority and critical commentary on large companies and their management is rare.

Bullish & Bearish Views on Smartkarma

Source: Smartkarma

Analysts Coverage of Large Banks By Market Capitalisation in India

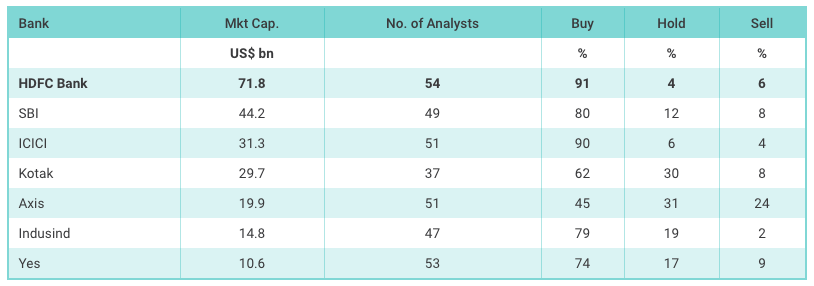

Source: Bloomberg

In India, large cap research is competitive and most of the global bulge bracket firms are present. As the financial sector has a high weightage in the market index, banks are extensively covered. HDFC Bank Limited (HDFCB IN) with a market capitalization of US$ 71.8 bn. is tracked by 54 analysts with 91% maintaining a ‘Buy’ recommendation and commentary is naturally positive. Yet Daniel Tabbush, an Insight provider at Smartkarma, is cautioning investors on HDFC Bank’s rising impairment costs. It is possible that HDFC Bank’s share price may continue to reward shareholders as it has done in the past, but Daniel Tabbush is taking on the consensus with a contrarian view supported by data. It is such outliers who get the attention of institutional investors and most importantly they will read and evaluate the merits of his argument.

Critical, independent, analytical research is not for the meek and there are pitfalls. There is no room for errors in critical research as the concerned corporate and investors will cross verify all the data points and analysts have to cross and double check the data prior to publishing. Corporates can boycott the critical analyst and deny her/him information and corporate access. Worse, vengeful companies can tie down analysts in lengthy, expensive law suits on charges of defamation and even use their extensive political contacts to make analysts experience the hospitality of the police – as happened in the case of fellow Smartkarma Insight provider, Nitin Mangal, for his critically acclaimed research on Indiabulls when he was with the independent research firm, Veritas.

For independent research to be recognized as a credible alternative to sell-side research, it has to play in the same field where the big girls and boys play, and in equities, it is large cap research. Midcap research is exotic, and can provide fabulous returns, but it is volatile and high-risk and in economic and market downturns, companies vaporise, as does the research. Independent research can and should do midcap research, but it should not be identified with midcap companies. Mifid II has provided a gateway for those brave, seasoned and enterprising analysts to forge a path of independence in a market heavily compromised by large corporate vested interests. It should use this opportunity to take the competition head-on, raise the bar on large corporate analysis, and in doing so, make proud the tribe of independent analysts.

The Profits (And Perils) Of Independent Large Cap Research

Investors in this expanding sector are deluged with me-too analytics that can often inhibit, rather than illuminate the road to smart price discovery driven by under the radar management moves.

Casino stocks have their temperatures taken like flu patients every time news breaks whether it is a true catalyst or simply a vapid space filler for media outlets.

The nature of the symbiotic relationship between standard buy and sell-side analysts and managements unavoidably is built off a process that hasn’t changed in decades but is now being challenged by sources of independent research.

Douglas Kim’s recent insight on SK Confessions of an Independent Research Analyst astutely pointed out how the role of independent research as a value added source of opinion to investors is riding on what many of us believe is a growing tide of analytics. They’re coming from new algorithms developed by quants that at times appear to be something of witches brew difficult to tease out in real-world performance. And they’re also originating from technical analysis sources that attempt to bring deeper more measurably predictive analytics to weigh in on the final investment idea. At the same time, we see investors beginning to disrupt the process by sourcing ideas and valuations from independent researchers who in a sense, have no dog in any particular fight.

Over my own career, I have been asked many times by investors what other than the standard set of data points usually applied to company performances, are the key, under the radar realities that longer term, actually drive bottom lines and by extension, casino share prices. I have developed what I call an “alternate reality” set of proprietary metrics and valuations entirely based on a view from the inside out. It’s the intellectual property of my consulting practice, but I am happy to share some its foundational principles with Sk readers. I think investors who are clients of wealth management divisions of banks, hedge funds should nudge their advisors to enhance their research beyond the standard data points that are the holy grails of the sector, to impart a keener insight to the company or idea that would normally be the case in a buy, sell or hold call.

While the casino industry shares many elements of related businesses, like lodging, entertainment, dining, and tourism, it has by any measure in my view, totally unique performance elements that can’t readily be judged by the same data sets applied to those sectors. What’s needed is a more nuanced understanding of what makes the business unique and by knowing that, bringing a depth and perspective to an investment idea in the space.

1.The casino business is probably more heavily regulated than most any other type of enterprise at a multiplicity of levels. Where governments feverishly compete for industries like manufacturing, energy, tech and retail with all kinds of tax concessions, waivers and infrastructure emoluments, they have historically needed to be nudged, or indeed pushed, by pro-legalization advocates to open the doors to casinos. Most recently we’ve seen how Japan, despite the relentless support of Prime Minister Abe and passage of the act, has resisted the process at every stage to the evolution of that nation’s Integrated Casino Resort industry.

The old fears persist: Problem gambling, corruption, entry for criminal elements, game integrity, money laundering run wild. These are not official or public objections that are ever likely to greet plans to build standard hotels, entertainment arenas, auto assembly plants, technology companies. After developers finally win over officialdom and elements of the public, they find themselves subject to high, sometimes punitive taxation percentages on gaming win, constant monitoring by massive regulatory bodies that track and let’s be frank, police, daily business on the casino floor, in its accounting departments, room towers, restaurants and dining establishments. The operating assumption to be brutally frank: We have to watch these guys. Those regulatory bureaucracies, tend to grow exponentially, every time the complications common to all cash movement businesses surface. Beijing’s junket crackdown crashed the Macau sector in 2015. It was perfectly understandable as part of a policy to curb political corruption and money laundering. And in its aftermath, stocks in the sector took a major hit. Yet, some analysts published recommendations built on doomsday scenarios. The facts as later developed, indicated that the action was clearly a baby with the bathwater situation. Offenders were indeed rooted out–by the handfuls. But VIP players stayed away by the bushel loads due to an immediate government induced paranoia. People who had nothing to hide, hid anyway or took off for the casinos of the Philippines. So the relationship between the scope of the actual problem and reality was distorted. This has subsequently been proven by the robust recovery of VIP business in Macau. related type industries, life is much simpler. You either make, distribute, buy or sell a product or service to an end user period. In casinos, skepticism accompanies daily business. Regulators, both in new and mature gaming markets tend to assume policies that fundamentally say: Look Mr. Casino operator, you exist at our pleasure so watch your step or we’ll pull the plug faster than you can roll a pair of dice. That is quite a difference than the attitude toward other related type businesses that are subject to a fairly normal set of regulations as to safety, sanitation, employment rules, and environmental impacts. In casinos, you have all that PLUS the mountain of regulations covering the dealing and administration of games of chance.

Beside the junket crackdown in Macau, we had moves on smoking that hit the sector stocks, ATM withdrawals, ad nauseum and bureaucrat decisions on the number of tables allowed for a given casino. These were not made by managements making business judgments, but by officials. And if you think officialdom in the SAD were singularly overbearing—consider this. In the early days of Atlantic City New Jersey, it required an on site inspection, and a lengthy approval process to move a sign from one zone of slots to another. As a senior level executive I was required to apply for and be cleared for, an A or Key License. The application was 130 pages long on two sides. I had to list every relative I knew up to and including second cousins including their names, addresses and phone numbers. The commission had all my bank information and by the way, escorted by enforcement officials, we were all required to go to any bank in which we maintained a vault lock box, open it and go through all the contents which were duly reported. My license, when issued, was the imprimatur of a person who easily could have walked in the next day to CIA headquarters and be immediately qualified as a field officer handling top secret information. None of this accompanies your average tech startup, movie theater, pizza parlor or two hundred room motel operator. What it tells us is that this is a business that is a creature of government more so than most others and when government sneezes, the industry, and its stock, can catch pneumonia.

So the lesson here is this: Government moves, sudden or planned are not all very good reasons to sell off a stock position in an otherwise strong performing casino operator unless of course, you see options play or are a day trader looking for a quick in and out on a sudden dip. But the government isn’t the only culprit per se, in the movement of casino shares. The other is the news cycle. This is a high visibility business. People are interested in happenings in a casino venue. The media know this and when anything happens, big or small, reporters call up analysts for comment. Most recently we’ve seen how tragedies in Las Vegas, Manila have hit gaming shares in the short term when analysts weighed in on the impacts. November’s early numbers in Macau indicate a robust 28% YoY increase during the first twelve days of this month. Yet, when asked to comment, several analysts also pointed out the start of the imminent Grand Prix event that “could dampen” Novembers strong start. Why? Because historically that has been the case. Whether that happens or not, its a slender reed for sure. This is a business where played delayed is usually mortgaged to the following month: It does not disappear.

To give some color on this issue I have studied the relationship between regulatory and force maejure elements in both Macau and Las Vegas. Early this year., associates spooked by news asked my opinion on a group of gaming stocks. “No knee shaking or knee jerking. Just stay long,” I said. I am no oracle. I merely based these picks on a broad lens view of how the industry tends to move over time and my understanding of the management dynamics that always play into results. Here are the results of my calls to date:

Note: Monarch is a US regional casino, relatively low cap, low visibility company with properties in Reno and Colorado only. Buried just below the surface of its usually strong performances in EBITDA over time was a pattern of management skills that in my view displayed themselves in strict fiscal discipline, excellent margins and a know-how employed in creating a customer mix–most critical of all, that added a valuation far above the market price. The alpha here lay in the longtime family management linked to a pattern that suggested the company was entering the next scale-up of its base which could be added to by development or acquisition.

As the year unfolded, it would appear support for the stock began to heavy up. And the single most valuable standard metric in valuing this sector is EV/EBITDA. This is a very Capex intensive business to the debt to equity ratios will always reveal more leverage than what many standard analysts may find comfortable. But Capex is the mother’s milk of the casino business. In the right hands, it produces great returns. Secondly, investors, I believe, always need to ask themselves this key question no matter what the standard metrics like P/E, PEG, 50 day moving averages, PTs–all part of a decision to be sure. But none them alone can answer this question: Do I want to be in business with these guys? Don’t think like someone buying a blip on a trading screen, think of yourself a buying into a business–mainly a management. And the extension of that is this: What does the EV/EBITDA ratio tell me about what this business is worth if someone showed up with a fistful of money and wanted to buy in. And think of yourself as a selling shareholder.

The Symbiotic relationship between standard buy and sell side analysis and independent research.

Over a long career, I have participated both as a corporate executive answering the questions of analysts gathered for earnings calls as well as a consultant on the asking end of the conference. As a result, I came to know many from major houses and found them to provide good guidance on fundamentals based on their inquiries. But at the same time, I limned a distinct proclivity in them to keep questions in the safety zone that avoided asking about tough issues lest they injure ongoing relationships with corporate contacts they need to do their jobs. This is entirely understandable. But the downside is that the process tends to produce far too many softball questions in order to maintain a general air of civility and nurse relationships. Enter the estimable Chinese Wall of old financial institutions who made it almost a fetish to insist that there existed an unbreachable wall between the interests of their investment banking departments and their security analysis people.

There was, to an extent, a separation that presumably was enforced but facts are facts. It has never been lost on me that institutions that raised billions over time for large and small cap casino operators, generally got rave reviews from their analyst departments. Was security analysis a tacit marketing arm of investment banking? Is it now? Let’s leap closer in time to think this out. During the 2007/8 financial crisis, many of us learned that bond rating services now and again pegged their calls on tranches of mortgage bonds on rather exotic formulations of the bundles of gold-plated obligations, so-so ones and an uncomfortable bulge of downright garbage. And at the same time, the same rating services worked with issuers for fees becoming symbiotic partners if you will, in the total transaction. There are pitfalls that are avoidable and those to be perfectly frank, that are not. And that is where in my view, the role of independent analysis comes powerfully to the front as representing a source of investing ideas and recommendations to a large extent, not in thrall to the confirmation bias, the proclivity that Doug’s insight alluded to. Its root can be in a corporate goal that finds its way into a data set and analysis of the numbers that reinforce those goals, ending up in a less than valuable piece of research for the investor. And that is where I believe, particularly in sectors with action elements that apply to no other businesses, independent analysis will continue to grow exponentially. It is not merely the disruptive technology of the delivery system, but the extent to which the work itself is free of institution biases and favor exchanges.

Next: In our next insight this month, we will look at how to value management performance outside of standard indices and metrics to bring out insights that lead to alphas not readily apparent in the casino space.

How Independent Research Can Add Depth to Valuations in High Visibility Sectors like Casinos

This is a follow-up to my report Independent Research in Asia 2.0. I borrowed the title from a memorable book called Confessions of an Economic Hit Man written by John Perkins. The purpose of this report is to provide a more detailed account of my personal experience as an independent research analyst in the past couple of years as well as the growth of the independent research platforms such as Smartkarma.

I hope to present an honest view of my experience and discuss both the rewards and the challenges of an independent research analyst and third-party research platforms. Many insight providers are likely to have similar struggles and may have asked the same questions that are highlighted in this report.

The global research in a post-Mifid II environment is likely to change dramatically. The clients that read this report may also get an improved understanding of how to better utilize independent research analysts and recognize their limitations as well. In particular, I discuss the following three major issues in detail:

The Beginning & The Network Effect

Warren Buffett’s “Knowing Your Circle of Competence” & Key Challenges of Coverage

What is Most Important?

The Beginning & The Network Effect

More than two years ago, I decided to give it a try as an independent equity research analyst. The job market was tough and with nearly two decades of experience as an equity research analyst, I thought there could be an interesting opportunity as an independent research analyst. After Googling “Asia” and “Independent equity research analyst”, I came across a company with a catchy name called Smartkarma, which provided a third party platform for independent research analysts like myself. After a review process and a chat with Jon Foster, I was allowed to contribute on this platform. My first report on the Smartkarma was about a Korean dairy & baby formula company called Maeil Dairy Industry (005990 KS). Biggest Beneficiary in Korea from China’s Two Children Per Family Policy? I think I spent about 3 weeks on this one report (nearly 40 pages). The initial response was disappointing, with the report getting a relatively low response from the Smartkarma community and its clients.

Nearly two years have passed since then and a few days ago, Smartkarma announced a major breakthrough investment by Sequoia Capital, which I believe is a home run for the company. What did Sequoia Capital see in Smartkarma? Sequoia has funded monster companies such as Apple, Google, Oracle, PayPal, YouTube, Instagram, Yahoo!, and WhatsApp in the past. Sequoia’s investment in Smarkarma is a HUGE thumbs up for independent research in a post-Mifid II environment. Smartkarma’s ability to capitalize on the network effect was probably one of the integral reasons as to why Sequoia Capital invested in this company.

The network effect is simply defined as a phenomenon where a good or service becomes more valuable as more people use it.

Companies such as Google, Instagram, and WhatsApp are prime examples of this network effect. They have built enormous moats capitalizing on this network effect which is difficult to break into by its smaller competitors.

In the global independent research platforms, SeekingAlpha is probably the most well known. However, there have been a lot of questions regarding the overall quality of their contents as well as their content providers, especially from the institutional investors’ points of view. Despite these concerns, SeekingAlpha has built a strong brand name and many investors like to view this website for generating investment ideas. As Smartkarma expands in the US market as well, a key challenge will be trying to compete against established players such as SeekingAlpha.

About a decade ago, I was doing some Korean investments related consulting work for a multi-billion dollar hedge fund called Luxor Capital based in NYC. Here, I was introduced to a website called Value Investors Club, which is widely used in the hedge fund/buy-side community for generating ideas. Unlike SeekingAlpha, the contributors at Value Investors Club are anonymous, which has its pros and cons. Overall, the research generated in Value Investors Club tends to be more on an “institutional” level compared to the ones on SeekingAlpha. Established by a well-known hedge fund manager, Joel Greenblatt, the Value Investors Club’s purpose is not to make money for the website itself, but more for its users (mainly institutional buy-side firms) to generate ideas that are not normally available in regular sell-side research. The Value Investors Club is another example of a website that has benefited from the network effect.

Right now, Smartkarma has a distinct lead in the Asian independent research platform with regards to the network effect (including the overall number of independent research providers). However, as it continues to expand in Europe and North American markets, it will face tough competitive pressures. Nonetheless, Sequoia Capital’s investment in Smartkarma provides a major vote of confidence and capital for the company to continue to successfully break into new markets globally.

Warren Buffett’s “Knowing Your Circle of Competence” & Key Challenges of Coverage

One of Warren Buffett’s favourite maxims is “knowing your circle of competence” and this has direct relevance to independent research analysts as well. Warren Buffett is famous for investing in companies that he understands. He has made investments in companies that he understands very well such as Coca-Cola and American Express. As an independent research analyst, you are “unshackled” to provide research on essentially any company in the world, unlike the traditional sell-side research analyst who typically has “core” coverage in 12-20 companies.

But who came up with the “industry rule” that the traditional sell-side research analyst needs to cover 12-20 companies and is this optimal? The equity research industry has its roots in the developed US/European markets. The need to maintain quarterly earnings updates is one of the key reasons why a typical senior equity research analyst has 12-20 companies under coverage. Think about it. Many of these companies have quarterly announcements in a similar time frame. Plus, there is a time limit as to how well an analyst can update an excel model and write about a company during the earnings seasons. The counter-party buy-side analyst (who works for a portfolio manager) typically has about 50-70 companies under “core” coverage.

Breadth vs. Focus Coverage – One of the goals of the traditional sell-side analysts is to dominate a few, core coverage stocks. For example, a few years back when I was a sell-side analyst covering renewable energy sector in Korea, one of the core stocks under my coverage was Oci Co Ltd (010060 KS), a leading producer of polysilicon. It was my job to better understand this company, write more research, and call more clients on this name than any other analyst on the Street. The salesforce always kept a record of how much trading was done on this name (and all other companies under my coverage) on a monthly basis.

This business structure is similar for the other sell-side analysts that cover stocks like Apple, Samsung Electronics, or Alibaba. Plus, there were long overseas marketing trips throughout the year. It is fair to say that about one-third of my time was spent on marketing/speaking with clients and the other two-thirds on writing research reports, updating models, and thinking about the changing industry dynamics. The amount of marketing versus writing reports may differ for each sell-side analyst but most of the sell-side analysts typically spend an awful lot of time on marketing and speaking with clients.

One of the benefits of the traditional sell-side analyst model is the fact that the biggest long-only funds sometimes have active engagement with the sell-side analysts for the stocks that they are interested in with regards to discussing key earnings estimates assumptions, for example. Analysts with solid track record of consistently forecasting earnings with logical assumptions tend to receive higher points from major long-only investors.

On the other hand, this advantage of being able to “dominate” a few stocks could work against the analyst, especially during a major downcycle in a particular industry. In addition, the extreme focus on a particular industry could also mean that this sell-side analyst maybe less aware of how the entire stock market, as well as other companies in different industries, are faring. This is where experienced strategist, salesperson, and equity traders can really help to bring incremental value to the buy-side clients.

Given this background, one of the major dilemmas for the independent research analysts is to pick the companies and industries that they want to cover and this goes back to Warren Buffett’s emphasis on “circle of competence.”

In the stock market, there are so many sectors to cover. But it is almost impossible to understand in depth so many different industries at the same time. Plus, many analysts may not have had previous exposure to certain industries. For example, Warren Buffett tends not to invest in biotech stocks. This does not mean there aren’t great biotech investments out there. In Korea, biotech stocks have been on a tear and they have been some of the best investments in the past several months.

With nearly two years of experience in independent research, I had to do some “soul searching” in terms of additional coverage. For example, there have been several interesting IPOs in Korea related to the biotech sector in 2017. After much thought, I decided against writing about them, despite the temptation to do so, mainly because writing research about Korean biotech stocks would mean losing some focus on my existing coverage.

In addition, the top three stocks including Samsung Electronics Co Ltd (005930 KS), SK Hynix Inc (000660 KS), and Hyundai Motor Co (005380 KS) represent nearly one-third of the entire Korean Stock Market in terms of market cap and they are well covered by existing sell-side analysts. As a result, I have concluded that it is very difficult for me to provide any differentiated view on these names and I have not written about these companies in-depth. Overall, I have tried to keep my coverage “limited” to IPOs, M&As, spin-offs, as well as on existing listed stocks related to the Korean consumer, telecom/Internet/games, industrial, rechargeable batteries, and special situations.

Challenges of Market Cap – There are many diverse investors with different needs for research on large vs. small/medium sized companies. Post-Mifid II, the low-tiered investment banks are likely to face extreme competitive pressure from the bulge bracket firms and independent research providers. As these low-tiered investment banks further downsize their research operations, their ability to cover mid-small caps will be further hampered and in this space, the independent research firms and research platforms such as Smartkarma have a chance to flourish.

In the past couple of years, I have found that clients typically show greater interests in IPOs of companies with market cap of more than US$300 to US$500 million. Personally, I have found that there are many interesting IPOs in Korea less than this market cap range but have tried to put a floor limit on trying to write research on companies with at least US$100 million in market cap.

Typically, writing about the biggest companies in the world such as Alibaba, Apple, and Tencent tend to generate more interest than companies with less than US$300 million in market cap but again there is a trade-off in being able to differentiate one’s research for companies that are not well covered. The insight providers at Smartkarma are consistently posed with this trade-off in research (higher market cap stocks which may generate more interest vs. differentiated research in writing about “undiscovered” investment plays).

Challenges of Country vs. Sector Coverage – There are great benefits to having a sector coverage (for example in banking or telecom/Internet) for numerous companies across multiple countries in Asia. Numerous independent research providers have adopted this approach. However, one of the difficulties of taking this approach is that it may require additional capital (for example, hiring additional help for different languages).

For example, Japan and Korea are two vastly different markets and require specific language skills to cover companies adequately. For many independent research analysts in Asia, it may be easier to cover companies on a country-specific basis, given the capital constraints of many smaller independent research firms. As a result, the traditional sell-side approach to covering many companies on a sector basis may provide some competitive advantage for now.

Cooperation among insight providers – This is one area where there is potentially a super potential for independent research platforms such as Smartkarma. There are so many opportunities to interact with various insight providers and try to create innovative joint research products.

For example, one of hottest markets in the world right now is Vietnam. Plus, Korea is one of the biggest foreign direct investors in Vietnam. Given the strong investors’ interests in Vietnam coupled with the fact that Vietnam possesses many of the attributes that South Korea had about 30 years ago, I thought that a joint “Vietnam-South Korea” research report would be a good idea and contacted Vietnam & Frontier Markets specialist Dylan Waller to write joint reports involving Vietnam and South Korea, which were well-received.

I also noticed a research product produced by Angus Mackintosh called The Week That Was in Asean@Smartkarma. I thought to myself, “Why not replicate such a product for the North Asian market involving Japan and South Korea?” So I contacted Travis Lundy, Mio Kato, CFA, and Sanghyun Park to see if we could create a similar product and we all agreed that it was a good idea so we started a weekly for the North Asian market a few months back. After a while, I noticed that there was a regular weekly called The Week that Was in Greater China@Smartkarma written on a rotating basis among Scott Laprise/ 乐天虎, Valerie Law, CFA, Ke Yan, CFA, FRM, and Daniel Hellberg.

In early 2017, I also started to read reports on the Smartkarma platform written by Howard J Klein who is an industry veteran in the gaming industry. In writing my reports about the Korean gaming industry, Howard provided valuable inputs that helped to improve the overall quality of the reports.

In addition, I have noticed that two insight providers including Angus Mackintosh and Nicolas Van Broekhoven actually have joined forces to create a firm called CrossAsean Research a few months back, capitalizing on their experience in covering the Southeast Asian stocks.

These examples are just tip of the iceberg. As Smartkarma continues to expand globally and increases its network effect, there are likely to be many ways that the insight providers could share ideas and expertise to create joint reports that add real value to the buy-side clients.

Knowing Your Strengths and Weaknesses – At the core of Warren Buffett’s “circle of competence” also includes knowing your strengths and weaknesses in terms of skill sets. For research analysts, there are several important skill sets/experiences that are required which include 1) analyzing a given industry/company (including building models & making recommendations), 2) writing in a logical, clear manner, 3) communicating verbally/marketing, and 4) years of experience covering a specific industry/playing a key role in taking a company in overseas roadshows/company visits.

Personally, I believe I have an “above-average” skills in analyzing a company, making recommendations, and writing in a clear, logical manner. However, I am “mediocre” in verbal skills and making presentations. Being in this industry for many years, I have seen some other analysts making wonderful presentations to clients that were quite “awesome.”

For independent research analysts with these “awesome” verbal communication and presentation skills, this actually poses a major dilemma. Working as independent research analysts may mean that they may have a lot fewer direct face-to-face meetings with buy-side clients initially as compared to when they were at traditional sell-side firms. As a result, they may be disheartened a bit since they may not be maximizing their strongest skill sets. In the long-run, as the demand for independent research increases, there will be greater opportunities for one-on-one meetings with clients. However, for now, the demand for one-on-one meetings with independent research analysts is relatively low compared to the traditional sell-side firms.

Knowing Your Client and Who Reads Your Research – For nearly two decades, I did not really know who read my research, until Smartkarma! When I was working in the sell-side, I wrote research which was distributed to the buy-side clients in a PDF format. This has been the industry standard for nearly 20 years since the adoption of the Internet and email. The sales team would occasionally tell me that a few clients liked/disagreed with my reports. There were very low visibility in terms of who actually read my reports. Having also worked in the buy-side, there is simply not enough time in a day to read all the reports. I believe I took a look at perhaps 5-10% of the reports coming in my email, and this is probably on the high side for the majority of the buy-side! According to a recent Reuters article, it notes that less than 1% of all research produced by the top 15 global investment banks are read by investors. http://www.reuters.com/article/us-markets-research/online-competitors-take-on-global-banks-in-securities-research-shake-up-idUSKBN16Z0L5

Smartkarma’s functionality of allowing the insight providers to know what clients clicked on one’s report will likely be the industry standard in the coming years. In the past couple of years, I have noticed the clients that regularly click on my notes but also the ones that no longer read my reports!

What is Most Important?

Having worked many years on the sell-side as well as an independent research analyst in the past two years, I realize that there are clear differences in the NUMBER ONE PRIORITY as a research analyst on these two different platforms. As a sell-side research analyst, the number one most important thing was quite clear – which was to get ranked by the biggest global buy-side firms including Capital, Blackrock, Allianz, JP Morgan, and Fidelity. The amount of bonus (or lack of bonus) was largely determined by whether you can get ranked by these Tier-1 firms.

However, my priority as an independent research analyst has changed. My number one priority as an independent research analyst is to generate great investment ideas. There is no longer any pressure to get ranked by these Tier-1 firms. However, there is a different kind of pressure, which is to think and write about great investment ideas.

In addition to the rankings by the Tier-1 buy-side firms, the annual Institutional Investors (II) polls, have been highly important to the sell-side analysts. In the post-Mifid II environment, it remains to be seen how much importance II polls will continue to be. As the major investment banks adopt research platforms that are less PDF dependent but with a greater transparency of which clients are reading what reports (similar to the Smartkarma system), this should improve the ability to have a more data-based system to better understand what reports the clients are reading. As a result, the “beauty contest” based II polls are likely to be de-emphasized and data analytics based system will increasingly be preferred in determining the “value” of investment research produced by both independent and traditional sell-side research analysts in the coming years.

Confessions of a Shipping Analyst: Voyage of the Damned, Asian Equity Research Version

Confessions of a Shipping Analyst: Voyage of the Damned, Asian Equity Research Version Confessions of a Shipping Analyst: Voyage of the Damned, Asian Equity Research Version

Confessions of a Shipping Analyst: Voyage of the Damned, Asian Equity Research Version

The Profits (And Perils) Of Independent Large Cap Research

The Profits (And Perils) Of Independent Large Cap Research

How Independent Research Can Add Depth to Valuations in High Visibility Sectors like Casinos

How Independent Research Can Add Depth to Valuations in High Visibility Sectors like Casinos