Receive this weekly newsletter keeping 45k+ investors in the loop

1. NVIDIA’s China Dilema Is Worse Than You Think…

- Jensen claims his Taiwan expansion is just about needing more chairs, yet an NVIDIA blog post describes the Santa Clara HQ taking to the skies & landing in Taiwan.

- He was critical of US restrictions on China chip exports while in Taipei, yet had nothing to say on the topic while in the White House or the Middle East

- NVIDIA’s market share in China is down from 95% in 2022 to 50% now, yet the country continues to challenge global AI leadership. That puts NVIDIA in an awkward spot.

2. Semiconductor Tariffs. No Thanks, But If You Insist…

- A total of 154 submissions on proposed tariffs by the US authorities on semiconductors were received by the closing date of May 7, 2025

- Key submissions were made by TSMC, Intel, Texas Instruments, Lam Research, Micron etc. Notable by their absence were Apple, AMD, Cadence, Synopsys, Broadcom, Marvell etc.

- The submissions by key players were universally negative on any types of tariffs with many warnings about unintended consequences as well as the threat of reciprocal tariffs from other countries.

3. NVIDIA Q126. China Restrictions Bring QoQ Growth Screeching To A Halt

- NVIDIA reported Q1FY26 revenues of $44.1 billion, up 69% YoY and up 12% QoQ

- NVIDIA forecasted current quarter revenues of $45.0 billion, marginally up QoQ and weighed down by the loss of around $8 billion in previously anticipated H20 revenues

- Does China really wish to remain reliant on US infrastructure/platforms for its AI build out indefinitely? I think not. Gradually losing China market was inevitable, even without US restrictions.

4. Latest US Restrictions On EDA Sales To China Tanks CDNS, SNPS

- CDNS, SNPS each fall >10% on the back of further US restrictions on sale to China

- Both of their China revenues were around 10% in the most recent quarter, albeit in the case of CDNS, it was 15% in the year ago quarter

- China’s domestic EDA ecosystem has grown significantly in recent years. These latest restrictions, if fully implemented, will simply serve to further accelerate its development

5. Silergy (6415.TT): Annual Growth Could Be Lower Than Earlier Expectation Of 20-25%.

- Looking ahead to the second quarter, Silergy Corp (6415 TT) did not provide specific guidance targets but emphasized that uncertainty in customers’ decisions regarding chip production locations could impact seasonal demand.

- Despite short-term challenges, Silergy Corp (6415 TT) still anticipates 2025 to be a year of growth.

- In terms of profitability, Silergy Corp (6415 TT) expects that capacity at Chinese foundries will approach full utilization, leading to supply chain tightness and helping maintain stable gross margins.

6. Taiwan Dual-Listings Monitor: TSMC Premium Rises Further, to Short Level; UMC Discount

- TSMC: +22% Premium; Consider Shorting ADR Spread at Current Level

- UMC: -1.4% Discount; Wait for More Extreme Discount Before Going Long the Spread

- CHT: +0.9% Premium; Can Consider Shorting the Premium at This Level or Higher

7. GlobalWafers (6488.TT): Shareholders’ Meeting Held; US Tariff Effects Pending; SiC Chances Ahead.

- Globalwafers (6488 TT) held its shareholders’ meeting yesterday (May 26th).

- Regarding the U.S. market, Globalwafers (6488 TT) noted that the U.S. government will impose tariffs on imported products, although the specific rates are still unknown.

- Regarding the overall market conditions, the 12-inch silicon wafer market is currently performing significantly better than the 8-inch market, with higher utilization rates.

8. Taiwan Tech Weekly: Google’s Pixel Going All-In on TSMC; TSMC 2025 Symposium Key Take-Aways

- Google’s Pixel Chips to Go All-In on TSMC After Using Samsung Foundry Previously

- TSMC (2330.TT; TSM.US): TSMC Provides Updates at 2025 Technology Symposium in Hsinchu Today.

- GlobalWafers (6488.TT): Shareholders’ Meeting Held; US Tariff Effects Pending; SiC Chances Ahead.

9. PC Monitor: Commercial PC Demand Resilient; AI PC Momentum Builds W/ NVDA Blackwell-Powered Launches

- HP Results Show Commercial PC Growth is Resilient, AI PC Penetration Expanding

- Key Industry Outlook Perspective — HP’s ZGX AI Station with NVIDIA Chips Marks the True Arrival of AI PCs… Locally Run LLMs Signal a Step-Change for PC Capabilities

- Remain Structurally Long PC Makers on AI PC Upgrade Cycle — Emergence of New NVIDIA Blackwell-Powered Workstations Clarifying the Path for AI PCs to Deliver Step-Change Improvements in Value

Receive this weekly newsletter keeping 45k+ investors in the loop

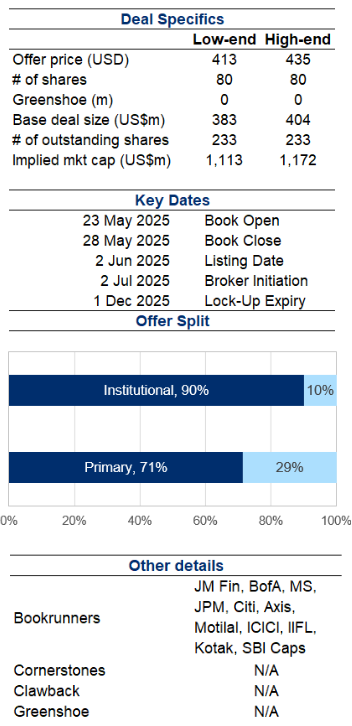

1. Schloss Bangalore IPO – Thoughts on Peer Comp and Valuation

- Schloss Bangalore Ltd (SCHBL IN) is looking to raise about US$409m in its India IPO. The deal has been downsized from an earlier size of around US$600m.

- It is a luxury hospitality company which owns, operates, manages and develops luxury hotels and resorts under ‘The Leela’ brand, through direct ownership and hotel management agreements with third-party owners.

- In this note, we will talk about the IPO valuations.

2. Curator’s Cut: Korea’s Value, CATL’s Charge and Copper’s Surge

- Welcome to Curator’s Cut, a fortnightly roundup of standout themes from the 1,200+ insights published over the past two weeks on Smartkarma

- In this cut, we look at Korea’s compelling valuation versus AxJ equities, CATL’s blockbuster Hong Kong listing and its market implications, and explore copper’s price surge amidst Chinese demand

- Want to dig deeper? Comment or message with the themes you think should be highlighted next

3. [Japan ECM] Financial Crossholders Offering Isuzu (7202) – Big Buyback Covers Most Of The Back End

- In line with the trend of financial institutions led by non-life insurers selling out of their cross-holdings, today we get an offering of shares held in Isuzu Motors (7202 JP).

- Today we got an announcement of 29.28mm shares being offered by a dozen financial institutions and a greenshoe for 15% more. At a 10% discount from here it’s ¥57bn/US$400mm.

- It is 16 days of ADV, which is big, but the company also announced a ¥50bn buyback from Pricing+6 to end of March 2026. That should stabilise things.

4. HK Strategy: Some Consumer IPO Pipelines and Their Proxies

- Hong Kong’s IPO market has gathered momentum lately, especially with the overwhelming response to CATL (3750 HK). Consumer IPOs are the next ones to gather interest.

- Foshan Haitian Flavouring & Food Co (FHF HK) is the most imminent one, potentially seeking up to US$1bn. Without significant peers in Hong Kong, it should attract good attention.

- The other interesting ones include Zhou Liu Fu Jewellery Co., Ltd. (1716396D CH), Three Squirrels (TRS HK), and Eastroc Beverage Group (EBG HK).

5. Interglobe Aviation (Indigo) Placement – Another US$800m+ Deal by Co-Founder

- InterGlobe Aviation Ltd (INDIGO IN)‘s co-founder, Rakesh Gangwal, aims to raise around US$803m via selling around a 3.3% stake in Indigo.

- He had earlier stated his intention to pare down his stake after a long drawn, and very public battle, with his co-founder Rahul Bhatia. He has sold many times before.

- In this note, we run the deal through our ECM framework and comment on deal dynamics.

6. Foshan Haitian Flavouring H Share Listing: The Investment Case

- Foshan Haitian Flavouring & Food (603288 CH), a leading Chinese pharmaceutical company, has filed its PHIP for an H Share listing to raise US$1 billion.

- Foshan Haitian Flavouring & Food Company (FHF HK) has been China’s leading condiments company in terms of sales volume for 28 consecutive years.

- The investment case rests on its market positioning, return to growth, industry-leading profitability, cash generation and strong balance sheet. However, the valuation of the A Shares is full.

7. Isuzu Motors Placement – Relatively Small Deal Along with Buyback

- A group of shareholders aims to raise around US$380m via selling around 4% of Isuzu Motors (7202 JP).

- Being another cross-shareholding unwind in Japan, it shouldn’t carry much negative connotations, in our view.

- In this note, we will talk about the placement and run the deal through our ECM framework.

8. Foshan Haitian Flavouring A/H Listing – PHIP Updates and Thoughts on A/H Premium

- Foshan Haitian Flavouring & Food (603288 CH) (FHCC), China’s leading condiments company, now aims to raise around US$1bn in its H-share listing.

- FHCC is China’s leading condiments company within its main product categories of soy sauce, oyster sauce, flavored sauce, specialty condiment products and other products.

- We have looked at the past performance in our earlier note. In this note we talk about the PHIP updates and likely A/H premium.

9. ECM Weekly (26 May 2025) – CATL, Hengrui, Eastroc, Haitian, Schloss, Aegis, Hyundai Marine, Pony

- Aequitas Research’s weekly update on the IPOs, placements, lockup expiry and other ECM linked events that were covered by the team over the past week.

- On the IPO front, Contemporary Amperex Technology (CATL) (300750 CH) and Jiangsu Hengrui Pharmaceuticals (1276 HK) performance has paved the way for a slew of A/H listings to follow.

- On the placements front, there was a large selldown in HD Hyundai Marine Solution (443060 KS) and a lockup release for Pony AI (PONY US) is coming up.

10. Capitaland Ascendas REIT Placement: DPU and NAV Accretive

- CapitaLand Ascendas REIT (CLAR SP) is looking to raise at least S$500M in a private placement, to fund the acquisition of some valuable properties.

- These acquisitions will expand the firm’s portfolio exposure to Singapore and data centers.

- In this note, we comment on the deal dynamics and run the deal through our ECM framework.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Horizon Robotics (9660 HK): Southbound Stock Connect Inclusion Today & Upcoming Index Flows

- Horizon Robotics (9660 HK) will be added to Southbound Stock Connect from the start of trading today. Then there will be passive buying at the close on 20 June.

- The lock up expiry in April will result in large buying from trackers of the Hang Seng TECH Index (HSTECH INDEX) and HSIII Index in September.

- The stock will also be added to another large global index, though the timing on inclusion is not certain at the moment.

2. Zomato/Eternal: The BIG Passive Selling Starts

- Following shareholder approval of the proposal to reduce the Foreign Ownership Limit from 100% to 49.5%, NSDL has updated the FOL. This starts the process of passive selling in Zomato.

- Passives will sell US$350m at the close on Tuesday. There is a low probability of more selling later in the week. There will be bigger selling in August.

- The size of the selling in August and beyond will depend on what foreign investors do in the stock till the end of June. Watch the red flag/ breach list.

3. [Japan Activism/M&A] Taiyo Holdings (4626) Now an MBO Target? KKR and One More Bidding

- Taiyo Holdings (4626 JP) has an interesting background, embroiled in a separate activist event via its equity affiliate sponsor Dic Corp (4631 JP), and recently an activist target itself.

- Today a Bloomberg article said KKR and one other PE fund had made acquisition proposals via TOB. Taiyo confirmed, establishing a Special Committee. A deal is months away, at earliest.

- Shares shot up to limit up, opened briefly, then resumed at limit up. The question here and now is valuation.

4. [Japan M&A] Makino Milling (6135) – MBK as White Knight Appears To Have Made a Binding Bid

- In December, Nidec Corp (6594 JP) made an unsolicited bid for Makino Milling Machine Co (6135 JP). Makino wanted more time. Nidec wanted to squeeze. Makino proposed a poison pill.

- Makino appeared to act slowly but white knight bidders were mooted in the media. Nidec launched, but apparently approvals may have been hard. They withdrew. Makino cancelled the poison pill.

- Shares fell sharply. Yesterday, they rose because it appears Effissimo owns 3%. Today, we got news post-close that MBK may be close to making an ¥11,000+ bid.

5. [Japan M&A] NTT To Buy Out SBI Sumishin Net Bank (7163) At a HUGE Price for Minorities

- Late Nov-2024, SBI Sumishin Net Bank (7163 JP) was trading ¥2,900, weekly mag Bunshun scooped a possible NTT Docomo deal. The stock popped, I was skeptical. It popped more.

- At Q3 earnings, NTT seemed to downplay the possibility saying they wouldn’t overpay. SBI Sumshin fell. Then fell some more.

- Today we get a deal whereby NTT buys out SBI Holdings (8473 JP)‘s 34% stake, and minorities, and partners with Sumitomo Mitsui Trust. Then a side deal with SBI.

6. Tsuruha (3391 JP)/Welcia (3141 JP): Vote Musings

- Leading proxies recommend that Tsuruha Holdings (3391 JP) shareholders vote against the Tsuruha/Welcia Holdings (3141 JP) merger on 26 May.

- The share exchange terms favour Welcia over Tsuruha shareholders. The Tsuruha vote will be close but likely to be approved. Long Tsuruha is the trade, irrespective of the vote.

- For a vote pass, you are long synergies and a likely partial offer bump. For a fail, you are long an undemanding multiple and the optionality of a new bid.

7. A/H Premium Tracker (To 23 May 2025): AH Premia Contract, H Premia Names Perform Best; Batteries!

- AH spreads are slightly narrower, but performance is concentrated in fewer names and broad spread volatility is up. BYD (1211 HK) now 5% through. CATL 10% through will help.

- It feels like there were some concentrated shorts on H vs A. BYD performance on CATL and Hang Seng upweight/inclusion exacerbate the issue. CATL H less liquid than people think.

- The data tables below update on a daily basis in the Tools section of Smartkarma. The SOUTHBOUND Flow Monitor and AH Monitor are both there free for SK readers.

8. [Japan Activism/M&A] – Shareholders Approve Tsuruha/Welcia Merger – Now It’s Partial Offer+Synergies

- This morning the Nikkei reported shareholders of Welcia Holdings (3141 JP) and Tsuruha Holdings (3391 JP) approved their Merger. Activists opposed but it was going to be close at best.

- As expected, Welcia shares popped, and the spread converged to 2% with Tsuruha falling back to just below ¥11,400. Some of this is unwind of speculative interest in Tsuruha.

- The new yuhos are out, which shows roughly where we stand (as of end-Feb, and some updates). Now the trade is NEWCO vs Aeon’s interest and NEWCO vs World.

9. NIFTY Index Outlook (With an Eye on Zomato’s Passive Selling Starting…)

- As reported by Brian Freitas , one of the NIFTY Index (NIFTY INDEX) ‘s component (Zomato: Eternal (ETERNAL IN) ) will be subject to big passive selling beginning on Tuesday.

- Let’s have a look at the NIFTY Index (NIFTY INDEX) to evaluate the tactical outlook according to our model.

- Since our last BUY recommendation in a previous insight in early May, the index has made some progress uptrending, let’s see if the rally can continue…

10. [Quiddity Index] GMO (9449) Sub GMO Financial Gate (4051) Moves to TOPIX

- Today after the close, GMO Internet Group (9449 JP) subsidiary GMO Payment Gateway (3769 JP) announced its subsidiary GMO Financial Gate (4051 JP) would move to TSE Prime 5 June.

- That means it moves to TOPIX at the close of trading 30 July 2025.

- This growth stock appears to have “de-growthed” somewhat in stock price terms – trading near its IPO price from covid era, so it is worth a look.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Alibaba (9988 HK): Unpacking the Week’s Savvy Top Options Trades

- Over the past five trading days, Alibaba Group Holding (9988 HK) multi-leg option strategies showcased a variety of approaches. Strategy highlights are provided.

- Popular Strategies: Over 35% of all strategies are Calendar or Diagonal Spreads. Bullish and bearish views prevail at equal rates, with very few market-neutral views expressed.

- Top Trades: Some market participants were betting on a short term re-bound after the post-earnings drop. Others take a bearish view with finely calibrated medium-term hedges. Trade-examples are presented.

2. Alibaba (9988 HK): Navigating Post-Earnings Volatility

- Implied Volatility Trends:Alibaba Group Holding’s (9988 HK) one-month implied volatility has significantly receded to the 37th percentile after its 15 May earnings, reflecting a substantial implied vola crush.

- Skew and Term Structure Dynamics: The implied volatility term structure is now slightly upward-sloping with longer-dated options commanding a small premium. Skew dynamics indicate cheaper puts.

- Open Interest Distribution: Liquidity is greatest in the June and September expiries. Short term strikes are concentrated near or at the money.

3. HDFC Bank Tactical View: Inflection Point or Just a Pause?

- HDFC Bank (HDFCB IN) is navigating a mix of positive growth indicators and emerging regulatory challenges but average 12-month target is ₹2,194, with estimates ranging from ₹1,627 to ₹2,793.

- Consensus rating: predominantly “Buy” from major brokerages, including ICICI Securities and Motilal Oswal, citing strong loan growth and stable asset quality.

- The stock’s strong fundamentals and growth outlook remain intact, but momentum has stalled in recent weeks following the sharp rally we correctly anticipated from January 14, 2025.

4. CATL (3750.HK): Rich Vols, Strong Start, and a Tactical Hedge

- CATL’s options debut in Hong Kong has been active, with strong Call interest and rising open interest suggesting early investor enthusiasm.

- Implied vols are holding firm post-listing and appear rich —potentially justifiable given the trading dynamics and catalysts.

- We recommend a tactical hedge structure that skews return favourably, targeting recent highs and protecting against downside drift.

5. China Mobile (941 HK) Poised for Pullback: A Tactical Low-Cost Options Play With High Upside

- With a 5-week rally China Mobile (941 HK) is in overbought territory and quantitative models flag potential for a pullback.

- Options may be underpricing the downside risk, creating an attractive opportunity to buy cheap options with high payoff potential.

- This Insight outlines an option strategy combining quantitative signals with volatility analysis.

6. KOSPI 200 Tactical Outlook After Index Rebalancing

- Korea Exchange announced its KOSPI 200 rebalance changes on 27 May, Sanghyun Park and Douglas Kim wrote extensively about this, here we want to focus purely on the tactical strategy.

- The KOSPI 200 INDEX pulled back last week, then surged on Monday and stagnated on Tuesday, the index has plenty of room to go higher according to our model.

- According to our model, the number of rallies vastly offset the number of pullbacks when this pattern is encountered (=pullbacks are rare), this could be read as a bullish indication.

7. HSI Index Options Weekly (May 26-30): Choppy Tape, One Strike Rules Them All

- HSI traded sideways for a third straight week as macro headlines swirled and tariffs turned internally litigious.

- Volatility drifted lower, with 1M implied vol dropping below its 1-year median for the first time in months.

- Call volumes were significantly higher led by one strike in particular.

8. All Eyes On Nvidia (NVDA US): Post-Earnings Outlook and Profit Targets

- By the time this insight is published, NVIDIA Corp (NVDA US) will have reported earnings. Our model does not rely on fundamentals or news, so the forecast is made in advance.

- The stock pulled back last week, mild pullback, not oversold, ideally a buy-the-dip opportunity. Support targets: 123-112

- If the stock rallies, the rally could last 3 weeks and reach 156. Read the detailed analysis in the insight.

9. Nifty Index Options Weekly (May 26 – 30): Rally Pauses, Vol Holds at Elevated Levels

- Nifty had limited movement this week with the rally off the April low stalling out.

- Elevated volatility metrics contrast with an otherwise quiet tape over the past week. We recommend taking some chips off the table, taking advantage of vol levels.

- Nifty has given up about 1/2 its outperformance vs the SP500 over the past couple of weeks.

10. TLT – From Hedge to Risk Asset: Behavior Continues to Shift

- TLT is showing signs of shifting behavior, no longer acting like a classic flight-to-quality asset.

- One-Month implied vol sits above average, though not at extreme levels.

- The evolving vol structure suggests caution for those expecting traditional bond market flight to quality behavior.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. US vs EU: Crying ‘Wolf’?

- Ursula von der Leyen had a call with Donald Trump on 25 May.

- The call can be interpreted as a ‘win’ for Trump as he had threatened to impose 50% tariffs on the EU from 1 June.

- Another perspective could be that Trump’s reversion is a new manifestation of the TACO principle.

2. More USD Depreciation on the Cards – Who Wins, Who Loses.

- US is focusing on propelling growth with tax cuts, ignoring the debt problem. The obvious consequence, more USD depreciation, could drive more money from US assets into Asia and Europe.

- If 1% of US free float market cap flows into Asia, it would constitute 7.2% of Asia’s market cap. That’s more than 5x the highest ever annual Asian FII inflow.

- Taiwan, Korea and India have seen the biggest FII flow revival. To sidestep the deleterious effect of sharp USD appreciation on Asian exports, investors should play China, India, Indonesia, Philippines.

3. Steno Signals #198 – A 20–25% Weaker USD May Solve All Trump’s Problems

- Morning from Europe.

- Trump’s classical stop-and-go approach to negotiations is starting to get baked into markets, but we’re still surprised by the extent of market moves when these impulsive threats are announced on Truth Social — and markets remain poor at assessing the “realistic outcomes” of this approach.

- On Friday, markets at one point priced in a 40–60% probability that 50% tariffs on the EU would actually take effect on June 1.

4. The Week Ahead – Big and Beautiful

- Yield steepenings may be linked to fears of fiscal profligacy and concerns of inflation expectations

- US Exceptionalism theme unraveling, dollar facing downward pressure

- US tax bill moving through House, expected to have modest stimulative economic impact

This content is sourced through publicly available sources and has been machine generated. Information displayed is for general informational purposes only.

5. Biggest One Day Move in Higher Share Performance YTD in 2025 for Major Korean Holdcos Today – Why?

- In this insight, we provide five major factors that may have caused higher share price movements (up 7.6%) of 10 major Korean holdcos/quasi holdcos today.

- This is the best one day share price performance on average for these stocks so far in 2025.

- Emphasis on improving corporate governance by both leading Presidential candidates and potential mandatory cancellation of treasury shares are among the five major factors.

6. Overview #27 – The Big Beautiful Tragi-Comedy Continues

- A review of recent events/data impacting our investment themes and outlook

- What are major global bond markets telling us about the world?

- We look at potential beneficiaries of the next wave of inflation

7. Texas Power Play: Grid Sovereignty, Bitcoin, and the Future of AI

- The speaker discusses events surrounding the downgrade of the US economy and the response from government officials

- The speaker highlights the increasing adoption and performance of bitcoin compared to traditional assets like gold

- The discussion transitions to the business efforts and partnership of Lisa and Dan, who met at a Houston bitcoin meetup in 2021.

This content is sourced through publicly available sources and has been machine generated. Information displayed is for general informational purposes only.

8. KOSPI 200 and KOSDAQ 150 Constituent Changes Announced: A Few Surprises

- Korea Exchange announced its KOSPI200 rebalance changes on 27 May. It added 8 companies and deleted 8 companies. KRX also added 9 companies and deleted 9 companies in KOSDAQ 150.

- These 8 new inclusions in KOSPI200 are up on average 49.8% in the past one year. The 8 deletions to KOSPI200 are down on average 45.2% in the past one year.

- There were numerous surprises to the KOSDAQ150 rebalances. In particular, three companies are relative surprises to the KOSDAQ150 additions including Solid Inc, Zeus Co, and Wemade Max.

9. Asian Equities: To Sidestep ASEAN’s China Problem, Focus on Select Pockets

- ASEAN’s underperformance could continue. The low growth region is facing the additional risk of increasing Chinese exports, which could dent domestic companies’ revenues and margins and engender a deflationary spiral.

- China exports more to ASEAN than to the US or EU. Margin pressure in consumer and industrials is palpable. Thailand is in deflation and inflation is nosediving in the region.

- We recommend playing the region through markets with low China import intensity (Indonesia, Philippines) and through consumer services and select banks. We have Digiplus, DBS, BCA in our model portfolio.

10. Sell America = Buy Gold

- The Sell America investment theme is becoming as a dominant market narrative, and it’s bullish for gold.

- It is driven by the combination of rising deficits, shaky bond markets, an increasingly hawkish Fed and policy uncertainty.

- For a long-term perspective of the upside potential in gold, a point-and-figure chart of monthly gold prices shows a measured objective of almost $7,000.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Nvidia (NVDA.US): Jensen Delivers Keynote Speech at COMPUTEX Today; Confirm Offshore HQ Location

- NVIDIA Corp (NVDA US) CEO Jensen Huang visited Taiwan to attend the COMPUTEX Taipei International Computer Exhibition.

- Meanwhile, NVIDIA continues expanding its workforce, recently opening over a thousand job vacancies globally.

- Throughout his speech, Huang repeatedly mentioned Taiwan. He opened with “Hello Taiwan,” noting that both of his parents were present in the audience, highlighting his personal connection to Taiwan.

2. US Middle East AI Splurge. A Bold Move But Also A Curious Affair

- AMD & NVIDIA both pocket deals to equip 500MW data centers in Saudi Arabia over the next 5 years.

- UAE announced plans to build 5GW of data centre capacity with local champion G42 leading the charge. Microsoft and Cerebras were notable by their absence last week.

- The Middle East deals are good news for US AI/Technology champions however the benefits will likely take years to fully accrue.

3. TSMC (2330.TT; TSM.US): TSMC Provides Updates at 2025 Technology Symposium in Hsinchu Today.

- TSMC explained that the growing demand for autonomous driving technologies in smartphones, PCs, IoT devices, and the automotive industry is driving the development of its N4/N3 and N6RF process technologies.

- TSMC announced that the A14 process, which will adopt the new NanoFlex Pro technology, is scheduled to begin production in 2028.

- TSMC plans to launch CoWoS-L with 5.5x reticle size in 2026 and surpass current CoWoS limitations with 9.5x reticle size by 2027.

4. Taiwan Tech Weekly: COMPUTEX 2025 Kicks Off — Nvidia CEO Unveils Taiwan AI Supercomputer Investment

- COMPUTEX 2025 Kicks Off — Nvidia CEO unveils Taiwan AI Supercomputer investment plan with Hon Hai, TSMC as key partners.

- Nvidia Opens Up Ecosystem with new “NVLink Fusion” — A strategic move to cement long-term platform dominance.

- PC Monitor — Asus Results Warn of Coming Slowdown; PCs’ Next Edge AI Shift

5. Taiwan Dual-Listings Monitor: TSMC Spread Rebounds Back to Recent Highs; ChipMOS Premium at Extreme

- TSMC: +19.2% Premium; Rebounded from Previous Lows, Consider Shorting ADR Spread at 20% or Higher

- ASE: +6.0% Premium; Near Level to Go Short the ADR Spread

- ChipMOS: +3.4% Premium; Good Level to Short the ADR Spread

6. TSMC (2330.TT; TSM.US): Xiaomi Launch “Surge O1” With 3nm.

- Xiaomi to launch strategic new products on the 22nd, including the new SoC chip “Surge O1”.

- Xiaomi Surge O1 at a glance: benchmark scores suggest it’s a strong rival to MediaTek and Qualcomm.

- While Xiaomi has not confirmed the chip’s foundry partner, we believe it is very likely manufactured by Taiwan Semiconductor (TSMC) – ADR (TSM US).

7. AMD. Adding $6 Billion Buyback & Authorizing 78% Increase In Share Count. But Why?

- Following its AGM on May 13 last, AMD announced a new $6 billion share repurchase program, despite still having $4 billion remaining on the previous buyback program

- The AGM also approved a proposal to authorize a 78% increase in the company’s share count, from 2.25 billion to 4 billion shares

- It’s a bold move on AMD’s part and it reawakens memories of the company’s acquisition of Xilinx back in 2022 in a $35 billion all stock deal. Deja vu ?

8. TSMC (2330.TT; TSM.US): TSMC’s Arizona Subsidiary Sent a Letter in Response to the U.S. Authorities.

- The U.S. Department of Commerce’s Bureau of Industry and Security (U.S. BIS) recently released a series of public consultations regarding Section 232 related to semiconductors.

- TSMC stated that any import measures should not create uncertainty for existing semiconductor investments.

- Any measures taken by the U.S. government should not undermine the national security policy objectives of the U.S. government, including advanced semiconductor production at TSMC Arizona.

9. PC Monitor: Asus Results Warn of Coming Slowdown; PCs’ Next Edge AI Shift

- ASUS beat 1Q25 expectations, but flagged tariff risks and a potential PC demand slowdown in 2H25 as consumers front-load purchases ahead of pricing uncertainty.

- PC segment growth outperformed the market, led by >30% YoY gains in commercial PCs and strong momentum in AI-capable and gaming systems.

- On-Device AI execution is emerging as the next PC evolution; Asus is preparing for this shift with GX10 edge devices and deeper integration of AI across product lines.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. GMO Internet (4784) – Squeeze-Able So Squeezing, Offering Likely Gets Pulled – AVOID LIKE THE PLAGUE

- GMO Internet (4784 JP) was created by the reverse takeover of a listed cad/media company by its parent company’s “internet infrastructure” business. GMO Internet Group ended up with ~98%.

- In the process, the stock rose 500%. Now, as part of its promise to the TSE allowing TSE Prime membership for the extraordinarily low-float target, the parent is offering shares.

- The squeeze has it at 180x Dec25e EPS, 111x EBIT, 70x book. The offering likely gets pulled and the stock isn’t shortable… so what next? Pain, and an ECLWO.

2. CATL A/H Trading – Strong Demand, Upsized, Included in Short-Sell List

- Contemporary Amperex Technology (CATL) (300750 CH), one of the world’s largest battery solutions providers, raised around US$5.2bn in its H-share listing.

- Contemporary Amperex Technology (3750 HK) is the global leader in new energy vehicle battery solutions, in China and globally, as per SNE Research. Its A-shares have been listed since 2018.

- We have looked at the company’s past performance and valuations in our earlier notes. In this note, we talk about the trading dynamics.

3. GMO Internet Placement: Extremely Overvalued at the Moment

- GMO Internet Group (9449 JP) is looking to sell its 33.4% stake in its subsidiary GMO Internet (4784 JP) to meet free-float requirements.

- Shares are very overvalued at the moment and should be worth a mere fraction of its current trading value.

- We have looked at the company’s deal dynamics in our earlier notes. In this note, we discuss the firm’s outlook as well as valuation.

4. Jiangsu Hengrui Pharma H Share Listing (1276 HK): Trading Debut

- Jiangsu Hengrui Pharmaceuticals (1276 HK) priced its H Share at HK$44.05 to raise HK$9,890.1 million (US$1.3 billion) in gross proceeds. The H Share will be listed tomorrow.

- The timing of the H Share listing is fortuitous, as the peers have materially re-rated since the prospectus was released on 15 May.

- Hengrui had the highest oversubscription rates among recent large AH listings. The AH discount implied by the offer is attractive.

5. CATL H Share Listing (3750 HK) IPO: Trading Debut

- Contemporary Amperex Technology (3750 HK) priced its H Share at HK$263 to raise HK$35,657.2 million (US$4.6 billion) in gross proceeds. The H Share will be listed tomorrow.

- The H Share listing price implies an AH discount of 6.6% at the A Share price of RMB63.51. This compares to Midea Group (300 HK)‘s AH discount of 4.7%.

- CATL had the highest oversubscription rates among recent large AH listings. Our valuation analysis suggests that the H Share listing price is attractive.

6. Eastroc Beverage A/H Listing – Energized – Fast Growth, Better Margins

- Eastroc Beverage Group (605499 CH) (EB), a China-based functional beverage company, aims to raise around US$1bn in its H-share listing.

- According to Frost & Sullivan (F&S), EB has been the largest functional beverage company in China in terms of sales volume for four consecutive years since 2021.

- In this note, we look at its past performance and other deal dynamics that might impact the listing.

7. ECM Weekly (19 May 2025) – CATL, Hengrui, Green Tea, SMPP, Unisound, Renesas, Genda, GMO, PayTM

- Aequitas Research’s weekly update on the IPOs, placements, lockup expiry and other ECM linked events that were covered by the team over the past week.

- On the IPO front, Contemporary Amperex Technology (CATL) (300750 CH) and Jiangsu Hengrui Medicine (600276 CH) will remain in the spotlight in the coming week as well.

- On the placements front, Japan deals appear to be picking up again.

8. HD Hyundai Marine Placement – Very Well Flagged, Overhang Easing but Last Deal Didn’t Do Well

- KKR is looking to raise around US$410m via selling some of its stake in HD Hyundai Marine Solution (443060 KS).

- KKR had come out of its IPO linked lockup in Nov 2024 and had tried to launch a deal in Dec 2024 and finally undertook a deal in Feb 2025.

- In this note, we will talk about the placement and run the deal through our ECM framework

9. Hanwha Aerospace: Higher Rights Offering Price and Amount

- On 21 May, Hanwha Aerospace (012450 KS) announced that the rights offering price increased to 684,000 won (up 26.9% from 539,000 won previously) due to recent increase in price.

- Due to the higher rights offering price, the scale of the capital raise has increased from 2.3 trillion won previously to 2.9 trillion won (US$2.1 billion).

- Issue price is determined by applying a 15% discount rate to the one-month weighted arithmetic average price, one-week weighted arithmetic average price, and the closing price on the base date.

10. PegBio 派格生物 IPO: A Hardsell but Mostly Done Deal

- PegBio, a China-based near commercial stage biotech company, launched its IPO to raise up to US$39m via a Hong Kong listing.

- We have previously covered the company’s fundamentals and valuation. We highlight issues of the company.

- In this note, we look at the deal term. We think the valuation is demanding, but the company managed to get support from local government facilitate its listing.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. CATL (3750 HK): Reassessing Index Fast Entry; Need Overallotment Exercised by Tomorrow

- CATL (3750 HK) is trading at a 6.9% premium to Contemporary Amperex Technology (CATL) (300750 CH) – if that is due to expectations of Fast Entry, that premium could drop.

- CATL (3750 HK) has not announced the overallotment option as exercised and that puts Fast Entry at risk. An announcement prior to the close tomorrow could lead to Fast Entry.

- The earliest inclusion could be at the close on 30 May while the other global index inclusion looks likely in December.

2. [Japan M&A/Activism] Toyota Industries (6201) Deal Could Be Announced Near-Term

- Friday 25 April, Toyota Industries (6201 JP) released earnings for last year, guidance for this year and a Bloomberg scoop suggested Toyota Motors chairman Akio TOYODA would launch an MBO.

- In some ways surprising, but activists/”noisy shareholders” and TSE guidance on dual listings caused pressure, and Toyota Motors was trying to walk the good governance walk.

- I discussed the situation here on Day 1, and here a few days later. Long-only shareholders sold. Today, Kyodo had a follow-up article. Then Nikkei. Looks more solid now.

3. CATL (3750 HK): The Tail Wags the Dog

- The buying in Contemporary Amperex Technology (3750 HK) over the last couple of days has dragged Contemporary Amperex Technology (CATL) (300750 CH) higher as the arbs trade the AH spread.

- The Fast Entry into a global index could keep CATL (3750 HK) supported over the next few trading days, but reality will take hold pretty soon.

- Short CATL (3750 HK) / long CATL (300750 CH) offers great risk/reward, while an outright CATL (3750 HK) short offers higher return albeit at a much higher level of risk.

4. CATL (3750 HK)’s Concentration Warning

- Contemporary Amperex Technology (3750 HK) (CATL H), a global leader in providing battery solutions, was listed on the 20th May at $263/share. Here is the prospectus.

- Via the H-share listing, CATL raised ~US$5.2bn. Shares have since gained ~26% and trade at HK$330/share, as I type.

- It is worth noting the HKEx issued a high concentration warning in CATL’s H shares the day before shares were listed.

5. [Japan Activism/M&A] – Thinking About Positioning Around the Tsuruha/Welcia Vote

- The Tsuruha Holdings (3391 JP) and Welcia Holdings (3141 JP) AGMs to elect directors and approve the share exchange agreement to merge the two.

- 10% Tsuruha shareholder Orbis objects to the merger ratio AND the later tender whereby Aeon goes to 51%, saying everything is underpriced. ISS/GlassLewis recommend voting against the merger.

- I haven’t seen the proxy reports but I’ve done the math. Investors/arbs should look at the possibilities/probabilities and understand what dependencies exist. Shareholders are not helpless, no matter the outcome.

6. [Japan M&A] Mitsubishi Logisnext (7105) – The Deal Still Looks Mighty Good

- On 9 May Mitsubishi Logisnext Co., Ltd. (7105 JP) delayed earnings by 30 minutes. Shares popped. Then earnings were released, no deal, and shares crashed. Now they are rebounding.

- But they remain volatile and subject to dips like the one this AM -5% at one point. Fears may be due to the idea that first smoke here was Dec-2024.

- 5 months later, no deal yet. Bids were due pre-earnings but with tariffs and writedowns, one wonders if bidders were waiting for results.

7. Melco (200 HK) Trading “Cheap” Into Rights Issue

- In my stub monitor flagged in StubWorld: Toyota Industries/Motors, GMO Internet, I see Melco International Development (200 HK) is trading “cheap” to Melco Resorts & Entertainment (MLCO US).

- Last month, Melco proposed one new rights share for two existing shares at a subscription price of HK$1.0286/share, a 72.93% discount to undisturbed, and a 64.28% discount to the TERP.

- Lawrence Ho will backstop ~54% of the rights, if need be. Depending on the level of support for the rights, expect Lawrence to further chip away against minorities.

8. Toyota Industries (6201 JP): A Potential Privatisation Sooner than Expected

- Kyodo news agency reported that Toyota Industries (6201 JP) plans to accept a tender offer by Toyota Motor (7203 JP) and Toyota Chairman Akio Toyoda, potentially in May or June.

- The Nikkei reported that Toyota plans to borrow JPY3 trillion to fund the acquisition. These articles provide more clarity on price, composition of the offeror, financing structure, and timeline.

- These articles increase the probability of a tender offer around JPY18,515 (JPY6 trillion market cap). At the last close, the gross spread was 12.1%.

9. [Japan Buybacks] ShinEtsu Chem (4063) – How the FCSR Works

- Late April, Shin Etsu Chemical (4063 JP) announced a huge ¥500bn 200mm shares (10.2%) buyback. That was never ever going to happen. That needed a ¥2500 share price, not ¥4300+.

- But it was big, and started in late May. Today, they announced how. It is a “Japan ASR”, the Nomura version, this time with an interesting twist.

- In response to a couple of reader questions today, I provide a brief overview of how these things work.

10. Soundwill Holdings (878 HK): An Opportunity or Another HK Arbageddon?

- The spread to the Foo family’s HK$8.50 offer for Soundwill Holdings (878 HK) has materially increased to 15.8% over the last two trading days. The vote is on 23 May.

- Several readers have asked if the Soundwill offer will mirror the Goldlion Holdings (533 HK) deal break. The two schemes share similarities but are also different in several ways.

- The share price action either reflects an imminent deal break or a result of a negative feedback loop. Tread carefully as this is a high-risk/high-reward situation.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Toyota Motor (7203 JP) Tactical View: Privatization Momentum Builds — Ready to Rally?

- Since April 28th we traced a path for Toyota Motor (7203 JP)‘s stock price, first here (forecast: going down) and then here (forecast: potential 2-week pullback to 2578).

- Last week Toyota Motor (7203 JP)pulled back to 2598 (pretty close to our 2578 target). The stocks closed down for 2 weeks, as predicted. A rally may be starting.

- Rumors of an acceleratingof privatization bid for Toyota Industries (6201 JP)could act as a fresh catalyst for the stock—aligning with our model’s forecast from May 8th.

2. Fast Retailing (9983 JP)Tactical Setup: Buy-This-Dip

- Fast Retailing (9983 JP) presents a mixed outlook characterized by strong earnings momentum tempered by some geopolitical and macroeconomic challenges. Analyst opinions are mixed but consensus is mostly = “Hold”.

- The stock started a pullback this week and is reaching a support zone that offers the possibility of entering LONG positions at a discounted price.

- This is a short-term tactical setup but the stock can be hold for the long run if the rally continues in the coming weeks.

3. Samsung Electronics (005930 KS) Tactical Outlook Amid Rumored Phase 2 Buyback Confirmation

- As reported by Sanghyun Park, Samsung Electronics (005930 KS) ‘s phase 2 buyback disposal plan appears to be virtually finalized (or will be finalized soon – not official yet).

- As always, we’ll assess what our tactical models suggest about the trend from here—interpreted alongside the latest catalysts.

- We have been monitoring Samsung Electronics (005930 KS) for a while: the stock has been bottoming, then flat for a while, rallied modestly, now a minor pullback… time to BUY?

4. BYD (1211 HK) Outlook: Near-Term Upside Still Possible, but Rally Looks Stretched…

- BYD (1211 HK) has been rallying hard since its 309.80 bottom in early april, the stock closed at 465.20 last Friday, a +50% rally! Probably well deserved.

- This insight analyzes the short-term tactical outlook on a WEEKLY time period basis. Our model finds that the stock is currently very overbought, however some upside is still possible.

- You may want to consider hedging your bets with some puts (probably cheap at this point), 1-2 weeks expiry, to protect against a (probably mild), upcoming pullback.

5. Tencent (700 HK): Strategic Insights and Top Trades from HKEX Options Trading

- Over the past five trading days, Tencent (700 HK) multi-leg option strategies showcased a variety of approaches. Strategy highlights are provided.

- Calendar and Diagonal Spreads make up a quarter of all strategies. Several examples are presented incorporating upfront cost, upfront credit, or zero-cost combinations.

- While there is a bias towards bullish strategies, 26% of all strategies express a market-neutral view in the form of Straddles, Strangles, Butterflies or Condors.

6. Tencent (700 HK): Strategies to Navigate Low Volatility and A Flat Term Structure

- Implied Volatility Trends: One-month implied volatility is currently cheap, trading in its 14th percentile, while Tencent (700 HK) approaches its twelve-months high.

- Skew and Term Structure Dynamics: A pronounced skew smile and a relatively flat term structure make spreads and calendar / diagonal spreads attractive strategies.

- Open Interest Distribution: Liquidity can be found in the monthly May expiry and the Quarterly expiries. The historically low implied volatility facilitates longer term positions.

7. 10Y US Treasury Futures Rally: Tactical Outlook & Key Profit Zones

- 10Y US Treasury Futures started to rally on Thursday, after the House of Reps approved Trump’s Big, Beautiful Bill

- The Trump administration has dismissed concerns that the latest bill will harm the nation’s financial standing, even after the U.S. lost its top-tier credit rating last week.

- This is a brief insight to try to identify potential profit targets and duration of this rally.

8. NSE NIFTY50/ Vol Update / Indo-Pak Ceasefire! Large Markdowns in IV-Skew-Smile Triggered

- Indo-Pak ceasefire triggers risk-premia markdowns – Monthly IVs -4.0 vols lower, Skew & Smile get compressed

- Vol-Regime stays in “High & Up” state with high likelihood of switching to “High & Down” in the upcoming week.

- IV term-structure flattened as the week progressed. Leaving front-end vol-differentials in Contango & Back-end Backwardation now eased to +0.60 vols.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. Market Intel from a Commodity Trader & China Analyst

- Discussion shifts towards the market consensus on China, highlighting a cyclical stabilization within a structural slowdown.

- China’s credit cycle, green shoots in the economy, and property market are discussed.

- Speaker shares insights on the Chinese real estate sector, mentioning a contraction and the need for new areas of investment.

This content is sourced through publicly available sources and has been machine generated. Information displayed is for general informational purposes only.

2. UK Inflation Flies Hawkish Pressures

- Our above-consensus forecast was exceeded by UK inflation flying higher in April amid administered price rises and postponed price increases due to the late Easter in 2025.

- Airfares still soared 10pp more than the norm for a late Easter, and 20pp above the April average. This stoked service and core inflation, although the median was steadier.

- We expect inflation to grind up until October, whereas the consensus assumes stability until then. Persistently excessive inflation should discourage the BoE from cutting again.

3. Top 100 Korean Firms with Highest Treasury Shares as % of Market Cap (Tender Offer and M&A Targets)

- We provide an analysis of the top 100 companies with the highest percentage of treasury shares as a percentage of market cap.

- These 100 companies are prime targets of tender offers and M&As. Many of these companies have low PBR ratios.

- Number five in this list is Telcoware (078000 KS) which just announced a tender offer by the CEO who is trying to take the company private.

4. Trump Doctrine: All Talk And No Trousers

- The US has been extremely active in the international arena in recent weeks, particularly in trade and diplomacy.

- Showmanship is currently taking precedence over substance in these activities.

- This approach poses significant risks for both policymakers and investors.

5. “What-Ifs”

- What if the proportion of core CPI categories experiencing upward inflation momentum is on the rise?

- What if the improvement in the more persistent categories of CPI inflation has more-or-less stalled?

- What if longer-term inflation expectations are no longer wiggling sideways or actually creeping higher?

6. Steno Signals #197 – The Mood(Y)’s Is Bad in the Fiat

- Morning from Copenhagen ahead of a big week.

- I was coincidentally sitting in front of the screens when Moody’s announced its downgrade of the US late in the Friday session, and the timing was admittedly peculiar—with just 5–10 minutes left of futures trading before the closing bell.

- Back in August 2023, when Fitch downgraded the US, it did spark a mild risk-off environment, with the long end of the yield curve continuing its upward trend.

7. Asian Equities: Relative Valuation Divergence Opens up Index Trade Opportunities

- A glance at the growth-adjusted valuations of the Asian markets reveals that Korea and China are undervalued and India, Thailand, Singapore and Malaysia are overvalued.

- We take a granular look at long histories of each market’s relative valuations, and their medium-term trends relative to long term averages. We combine the conclusions with growth-adjusted valuation outlook.

- We conclude that HK/China, Korea, Indonesia and Philippines could be in for rerating in the near term. Derating could be on the cards for India, Singapore and Thailand.

8. HEW: Fiscal Anxiety As Rates Rise

- Jitters over the sustainability of US fiscal easing knocked equities and the dollar over the past week. Dovish BoE pricing was pared back further towards our contrarian call.

- UK inflation exceeded our already elevated forecast, while the manufacturing PMIs were broadly resilient again in May. UK retail data were also sensationally strong.

- Next week is relatively quiet and shortened by a bank holiday. Flash inflation for some euro member states, updated US GDP data, and the RBNZ decision are our highlights.

9. Asian Equities: Taking Stock After the Result Season: Where Are EPS Estimates Rising and Falling?

- As the earnings season draws to a close, we look at Asian markets’/sectors’ EPS estimate progression during the reporting season and earlier. Specifically, we search for upward or downward inflections.

- Korea and Taiwan had the strongest EPS upgrades during this reporting season, despite the trade uncertainties. Philippines, Indonesia, Malaysia also had decent upgrades. HK/China and India continue to be downgraded.

- Korean and Taiwanese technology, Korean industrials, HK Technology Services had strong upgrades. So did Singapore and Philippines financials, and Thailand Communications – the latter two with a long upgrade history.

10. Korea Value Up Index Rebalance Announcement Next Week

- Korea Exchange plans to announce the first rebalance of the “Korea Value Up Index” next week on 27 May. The actual rebalance is expected to take place on 13 June.

- Korea Exchange plans to reduce the constituents to 100 (from 105 currently) and change 30% of the included stocks in this index to better reflect the Value Up program incentives.

- In this insight, we provide a list of 20 potential exclusion candidates and 20 inclusion candidates in the Value Up index rebalance.