Receive this weekly newsletter keeping 45k+ investors in the loop

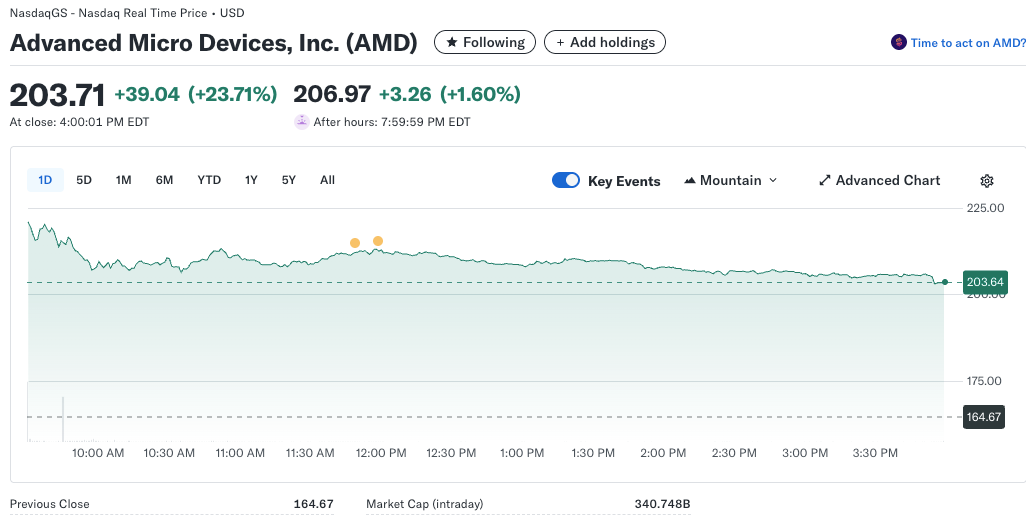

1. OpenAI, AMD Enter Into Strategic Partnership. Guys, This Is Getting Ridiculous!

- OpenAI agrees to deploy 6 gigawatts of AMD GPUs based on a multi-year, multi-generation agreement. The deal could be worth upwards of $100 billion to AMD through 2030

- AMD issued OpenAI a warrant for up to 160 million shares of AMD common stock, structured to vest as specific milestones are achieved, including AMD share price appreciation to $600

- Could a strategic partnership with Intel now also be on the cards? After all, OpenAI needs CPUs as well as GPUs, especially as they ramp into enterprise. Just saying…

2. Hitachi Ltd. (6501 JP): Tie-Up with OpenAI Opens the Flood Gates

- An agreement to supply OpenAI with energy-saving electric power equipment should be accretive to Hitachi’s sales and profits as long as the AI boom continues.

- Hitachi is also building an “AI Factory” based on Nvidia technology. This should accelerate the growth of Hitachi’s Lumada digital services platform, also boosting sales and profits.

- Hitachi’s share price jumped 10.3% on the OpenAI news. Data center news flow and AI sentiment now drive the share price.

3. Intel (INTC.US): AMD to Submit Foundry Orders to Intel? We Think It’s Highly Unlikely.

- What is happening with Advanced Micro Devices (AMD US) and Intel Corp (INTC US)?

- Intel’s stock price has risen about 50% from its April 8 low. However, we have yet to see any tangible progress in its manufacturing technology.

- Intel’s stock price has risen about 50% from its April 8 low. However, we have yet to see any tangible progress in its manufacturing technology.

4. Astroscale (186A.T-JP/ASTRO): The Small-Cap Takaichi Defense Trade

- After months of going nowhere, Astroscale shot up more than 20% in the two trading days following the election of defense hawk Sanae Takaichi as president of the LDP.

- Astroscale made a small gross profit last quarter, but needs a rising flow of contracts and subsidies in order to turn profitable at the operating and net levels.

- At ¥825, the stock price is 38% below the ¥1,326 high reached just over a year ago. If Takaichi becomes prime minister, the chances of regaining that high would improve.

5. Taiwan Tech Weekly: Why Many Tech Companies Could Soon See Their Chip Costs Rise Substantially

- As Chips Move to 3nm and 2nm Designs, Tech Companies Could See a Sharp Increase in Their Chip Manufacturing Cost

- Intel (INTC.US): AMD to Submit Foundry Orders to Intel? We Think It’s Highly Unlikely.

- HBM Stocks Will Keep Running (Micron, SK Hynix), It’s Just the Beginning

6. PC Monitor: Dell Doubles Multi-Year Forecasts; AI PC Up-Cycle, Art Thou Finally Here?

- Dell doubles long-term growth outlook to 7–9% revenue and 15%+ EPS CAGR through FY30, led by AI infrastructure.

- AI PCs emerge as Dell’s next growth engine; global refresh cycle could finally kickstart long-awaited PC upturn.

- Taiwan makers Asus, Acer, Quanta, and Wistron positioned to benefit as AI PC and server demand scales together.

7. Taiwan Dual-Listings Monitor: Weak US Friday Session Opens Up Wide Opportunities Across the Board

- TSMC: +19% Premium; Good Level to Close Out for Those Short the ADR Spread

- UMC: -3.9% Discount; Rare Deep Discount Good Level to Long the ADR Spread

- ASE: -5.5% Discount; Any Spread Below Parity a Good Level to Long the ADR Spread

8. Sovereign AI. National Strategic Imperative, FOMO Or Both?

- If all of the publicly announced sovereign AI initiatives come to pass, they could account for upwards of $1 trillion in AI infrastructure spending through 2030

- For now, “sovereign” AI means mostly means made in the USA. However, there a growing demand for “sovereign” AI from China, particularly among countries disillusioned by the US trade wars

- In general AI infrastructure, the US is outspending China six to one in 2025. Could one be spending too much and the other spending too little? Let’s see…

Receive this weekly newsletter keeping 45k+ investors in the loop

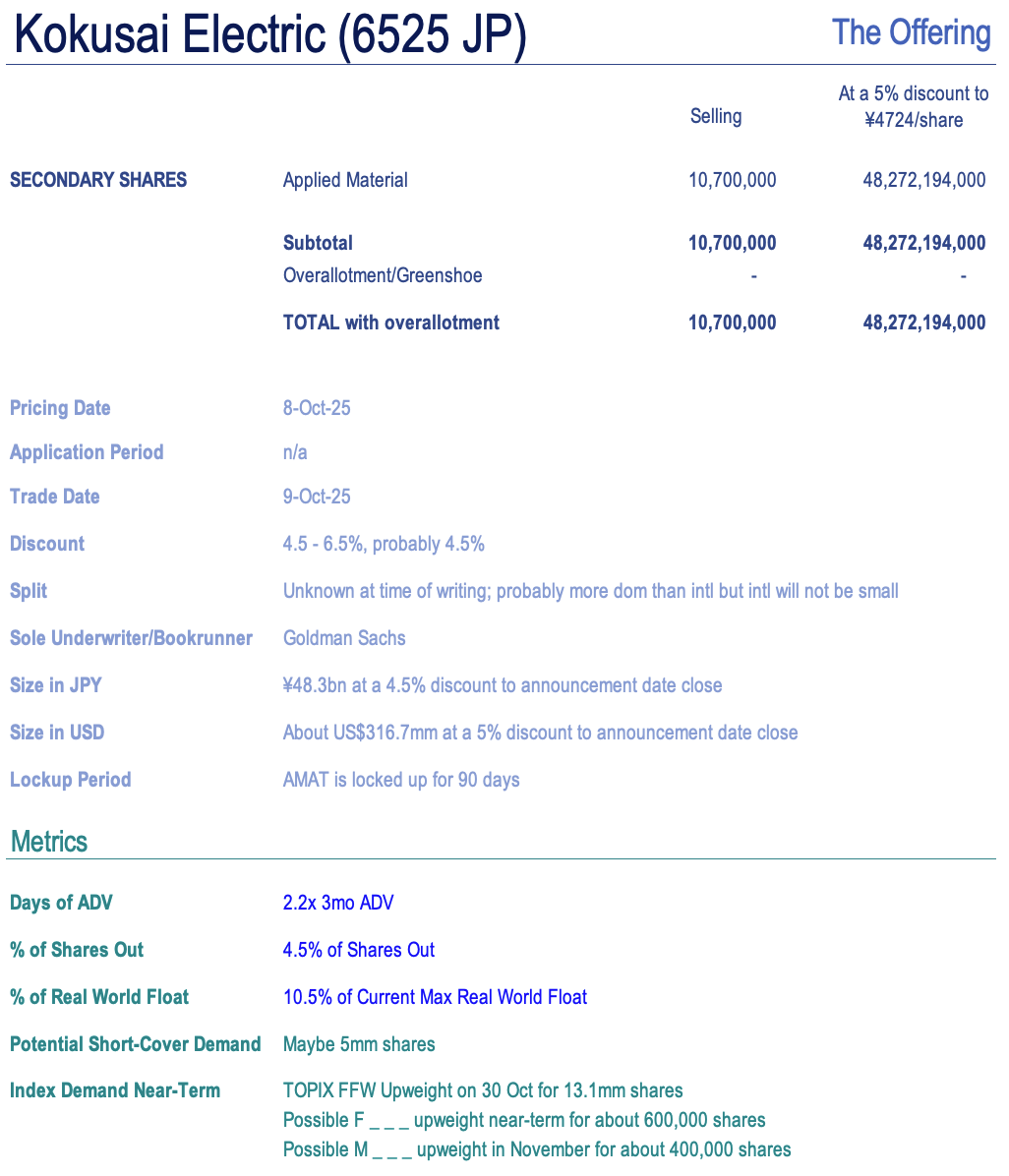

1. [Japan ECM] Kokusai Elec (6525) – Applied Materials $330mm Selldown

- Three weeks ago I wrote that KKR’s lockup would expire about now in [Japan ECM] Kokusai Elec (6525) – KKR’s Lock Up Expiry in 3 Weeks – $700mm Clean-Up Coming?

- Today post-close, Applied Materials (AMAT US) announced a 10.7mm share (4.5%) Accelerated Block Offering to be priced tomorrow morning, at an indicated 4.5-6.5% discount. This would put them at 10+%.

- This should be very well taken up. There is index demand on the follow. The question is more about the unwind of KKR’s last bit. Perhaps to come soon?

2. FineToday Holdings (420A JP) IPO: The Investment Case

- FineToday Holdings Co Ltd (289A JP), a Japanese personal care business, is seeking to raise US$286 million. It previously pulled an IPO to raise US$500 million in December 2024.

- FineToday has four product categories: Hair care, Skin care, Body care and others. Hair care is the largest category, accounting for 49.0% of 1H25 revenue.

- The investment case rests on top-tier revenue growth, top-quartile profitability, peer-leading FCF generation and manageable leverage.

3. Kokusai Electric Placement – Unexpected Seller but Relatively Small Deal

- Applied Materials (AMAT US) is looking to raise approximately US$330m through an accelerated secondary offering for around 4.5% of Kokusai Electric (6525 JP) (KE) stock.

- KE had seen two selldown earlier, from KKR, with mixed results. KKR just came out of its last lockup.

- In this note, we will talk about the placement and run the deal through our ECM framework.

4. LG Electronics India IPO – Thoughts on Valuation – Better Placed This Time Around

- LG Electronics (066570 KS) is looking to raise US$1.3bn via part-selling its stake in LG Electronics India.

- LG Electronics India (LGEI) was the market leader in India in major home appliances and consumer electronics (excluding mobile phones) in terms of volume, as per Redseer Report.

- We have looked at the company’s past performance and undertaken a peer comparison in our previous note. In this note, we talk about valuations.

5. Tekscend Photomask IPO: Market Leader with Strong Prospects Ahead

- Established in 2022, Tekscend Photomask (429A JP) (previously Toppan Photomask) is the world’s leading semiconductor photomask supplier, holding a global market share of 38.9%.

- Tekscend provides a diverse portfolio of high-precision photomasks for semiconductors, displays, MEMS, and R&D, including cutting-edge EUV masks, leveraging its expertise in microfabrication.

- The company is planning for a listing on TSE on 16th October and plans to raise proceeds of around US$800m through a combination of existing and new share issues.

6. LG Electronics India IPO: Attractive Upside

- After incorporating the company’s FY25 results, we have tweaked our income statement estimates and valuations of LG Electronics India IPO.

- Our base case valuation is target price of 1,514 INR which is 33% higher than the high end of the IPO price range.

- It appears that the company wants the IPO to be successful and after much review the company has decided to price the IPO at more attractive levels to new investors.

7. Innoscience Suzhou Tech Placement – Selling Ahead of Lockup Expiry, Relatively Small

- InnoScience Suzhou Technology (2577 HK) aims to raise around US$200m in its Hong Kong placement.

- Innoscience was only listed in Dec 2024 and it undertook another primary raising in July 2025, the lockup for which has yet to expire.

- In this note, we will talk about the placement and run the deal through our ECM framework.

8. LG Electronics India IPO: Leading Player Priced at a Steep Discount ?

- LG Electronics (066570 KS) will divest a 15% stake in its 100% subsidiary LG Electronics India (123D IN) through an IPO, raising Rs116 billion (USD 1.3 billion).

- The IPO pricing implies a valuation well below that of listed Indian peers and appears to overlook the sector’s underlying near term macro demand tailwinds.

- LGEIL’s 1QFY26 financial performance came in weak, primarily due to a seasonal slowdown in cooling product sales, particularly air conditioners. This follows a strong FY2025.

9. FineToday Pre-IPO – Refiling Updates

- FineToday Holdings (420A JP) (FT) is planning to raise around US$280m via selling a mix of primary and secondary shares.

- FineToday (FT) is a beauty and personal care company in Asia offering a range of products, including hair care, skin care and body care products.

- In our previous note, we had looked at its past performance. In this note, we will talk about the updates from its most recent filings.

10. LG Electronics India IPO- Strained in Legal Heat

- LG Electronics India (123D IN) much awaited INR 116.1 bn IPO is set to open for subscription this week. It’s a complete OFS by the Korean Parent.

- While LG is the market leader, there are huge litigation liabilities ~74% of net-worth which could pose a serious threat to the financials, with particular attention to AMP spends proceedings.

- We also find it disturbing to note that the parent has taken out 175% of the free cash flows in FY23 and FY24 as interim dividends.

Receive this weekly newsletter keeping 45k+ investors in the loop

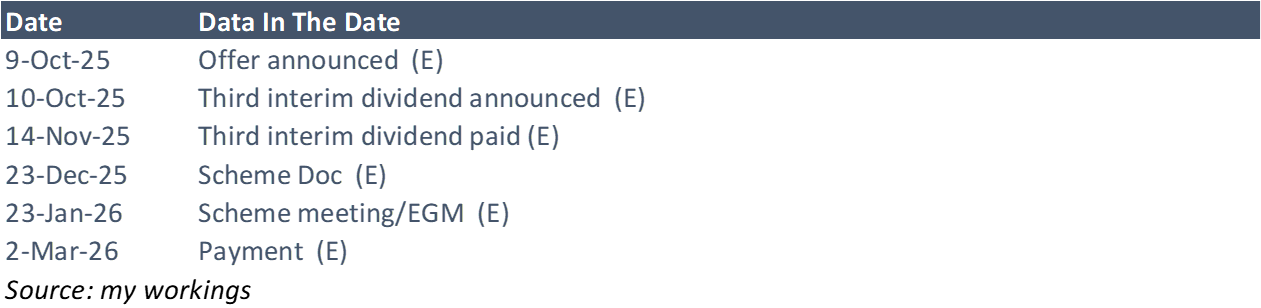

1. HSBC (5 HK)’s Clean Offer for Hang Seng (11 HK)’s Minorities

- Hang Seng Bank (11 HK) has announced an Offer from controlling parent (63.3551%), HSBC Holdings (5 HK), by way of a Scheme, in a HK$106bn (US$13.6bn) deal.

- The Scheme Consideration is HK$155/share, a 30.3% premium to last close. The price is final. A “third interim dividend” will be added. Optically, the price is bang on.

- The long stop for conditions is the 30th September 2026. I think this transaction can be wrapped up in around five months.

2. Tata Motors (TTMT IN) Demerger: Interesting Index Implications

- Tata Motors (TTMT IN) is demerging the company into two separate listed entities that will focus on the Passenger Vehicle business and the Commercial Vehicle businesses.

- Based on the estimated valuation for the two entities, both stocks will continue to remain in the MGlobal Index and the FGlobal Index.

- NIFTY and SENSEX trackers will need to sell their Commercial Vehicle business holdings soon after listing. There could be selling in the Passenger Vehicle business holdings at a later rebalance.

3. [Japan Event] Sony Financial (8729 JP) Moves On From ToSTNeT-3 Buybacks, Now In the Market

- Sony Financial Group (8729 JP) started ToSTNeT-3 buybacks last week and did one this week to jumpstart the buyback, cushioning the Nikkei 225 deletion on 29 Sep and subsequent overhang.

- In three ToSTNeT-3 buybacks in 6 trading days spending ¥28.9bn, the company bought back 177.513mm shares or 2.5% of shares out, or about 6.2% of Max Real World Float (MRWF).

- With ¥71.1bn left, at last that’s 460mm shares, or 16.2% of MRWF. Over 10mos that is 1.62%/month. That will boost Mar26 DPS, Mar27 DPS projections, EPS, etc.

4. Dongfeng Motor (489 HK): VOYAH Listing Docs Underscore the Upside

- On 22 August, Dongfeng Motor (489 HK) disclosed a pre-conditional privatisation by merger by absorption by Dongfeng Motor Corporation, along with a proposed distribution and listing of VOYAH shares.

- The VOYAH application proof, filed on 2 October, points to strong fundamentals and suggests that the appraised value of VOYAH and the offer are conservative.

- Based on the data points from the application proof, I calculate that the implied offer is HK$12.11-12.25 per H Share, a 11.6%-12.9% premium to the appraised value of HK$10.85.

5. Korea’s Mandatory Treasury Share Cancellation Situation Creates New Passive Flow Dynamics

- KRX may preemptively adjust KOSPI 200 screening, switching from full market cap to market cap excluding treasury shares for index inclusion.

- With treasury-share cancellation likely this quarter, KRX may act before June ’26. For December KOSPI 200, we should run both full-cap and ex-treasury screens; flows could behave unusually.

- Focusing on Hanssem (009240 KS) and Taekwang (003240 KS); borderline, high treasury shares, potential KOSPI 200 exclusion, making them key flow-sensitive setups for December reshuffle.

6. Dongfeng (489 HK): On VOYAH’s Updated Financials

- On the 22nd August 2025, SOE-backed Dongfeng Motor (489 HK) announced a privatisation; together with a concurrent listing of its EV arm, VOYAH.

- Dongfeng has now released the application proof for VOYAH, with finances through to July 2025. Of interest, VOYAH is in the black for 7M25.

- The market is implying a price-to-trailing-sales of 1.5x for VOYAH versus the basket average of 2.1x.

7. [Japan Activism] Sun Corp (6736) Gets ANOTHER Public Activist – ValueAct Reports 7.9%

- Today after the close, Value Act reported that it owned 7.87% of shares outstanding in Sun Corp (6736 JP) and it may make proposals to management.

- This has been trading cheaply (and I pointed it out on 13 Aug and 12 Sep). Cellebrite DI (CLBT US) is up 35% in those 8 weeks. Sun Corp +50%.

- ValueAct had owned 4.9+% for at least a few months before, but now it has gone public. They were likely in already under a different name in March, now public.

8. Merger Arb Mondays (06 Oct) – Kangji, Soft99, I-Net, Daiseki, Mandom, Changhong, Smart Share

- I summarise the latest spreads and newsflow of merger arb situations we cover across Hong Kong, Australia, New Zealand, Singapore, Japan, Indonesia, Malaysia, Philippines, Thailand and Chinese ADRs.

- Highest spreads: Smart Share Global (EM US), Mayne Pharma (MYX AU), ENN Energy (2688 HK), Soft99 Corp (4464 JP), I Net Corp (9600 JP), Daiseki Eco. Solution (1712 JP).

- Lowest spreads: Bright Smart Securities (1428 HK), Pacific Industrial (7250 JP), Humm Group (HUM AU), Mandom Corp (4917 JP), Seven West Media (SWM AU), Ainsworth Game Technology (AGI AU).

9. [Japan M&A/Activism] Soft99 Board Rebuts Effissimo’s Rebuttal. Still An Awful “Fiduciary” Response

- Today after the close, Soft99 Corp (4464 JP)‘s Board issued a statement on “Our View” of Effissimo’s “Our View” Press Release. It’s bad.

- But it points out the “weaknesses” that Effissimo’s Tender Offer Press Release had as it concerns a counterbid. And that tells you how Effissimo should amend their Tender Offer docs.

- Soft99 Board’s response is interesting. It asks Effissimo to not be coercive (i.e. bid for 50%+) in response to the MBO Bid’s coerciveness. Not a winning argument but not impossible.

10. [Japan Activism] Mandom (4917 JP) MBO Sees Murakami Pushing Harder, Now at 16.59%

- Four weeks ago, CVC announced a family-led MBO of hair care and cosmetics company Mandom Corp (4917 JP) at a price which was decidedly too light, well below company plans.

- One activist wrote a letter clearly calling them out for accepting a low-ball price well below the Medium Term Management Plan target. Another bought a lot of shares.

- On 25 September, Murakami-san and affiliates reported an 8.39% position. Seven trading days later it is 16.59% and the shares are up small from my last piece + 1.

Receive this weekly newsletter keeping 45k+ investors in the loop

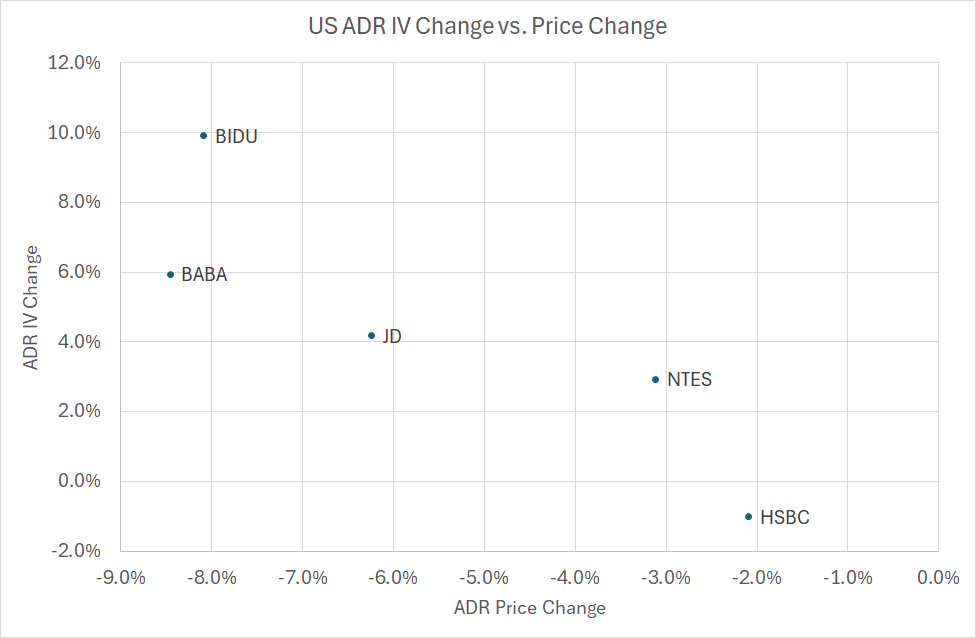

1. Alibaba Drops 8%: What Friday’s U.S. Sell-Off Means for Hong Kong Stocks

- Context: Friday’s sell-off occurred after the Hong Kong market closed, but several Hong Kong–listed companies were caught up in the rout through their U.S.-listed ADRs.

- This Insight details the impact on 15 prominent Hang Seng Index constituents — including Alibaba, Tencent, and HSBC. Implied volatility in U.S.-traded options on these ADRs moved sharply in response.

- Why Read: Understand what to expect when the Hong Kong market reopens after the weekend — both in terms of price performance and implied volatility.

2. Market Sell-Off (Oct 10): How Asian Index ETFs Responded to Market Slide

- A renewed tariff threat from Trump sparked a sharp, sell-off across North American Equity markets.

- The sell off was broad based and accordingly we look at the performance of Asian Index ETF’s that trade in North America to help prepare for Monday’s price action.

- Implied volatility, price and option volume are displayed for each symbol.

3. Nikkei 225 (NKY) Tactical Outlook: Flying Too High…

- The Nikkei 225 (NKY INDEX) has reached eye-popping valuations, a 20% rally from the end of June into early October (40k to 48k).

- Our forecast is always short-term, 3-5 weeks horizon, so we cannot say if the index will continue to rally in 2026, but right now it’s OVERBOUGHT.

- We expect a pullback soon, you can buy the pullback, we discuss the support areas in the insight.

4. HSI Tactical Outlook: Maybe It Is a Large Pullback…

- In our previous insight dedicated to the Hang Seng Index we formulated a key question: is this going to be a small pullback or a large pullback?

- The HSI pulled back just for 1 week, small pullback, our models were reset. But this week the index pulled back again, almost reaching Q2 support (mildly oversold).

- Then, on Friday, Trump tweeted something against China, after the Asian markets closed and all hell broke loose. The HSI Oct. futures tanked to 25300. Let’s discuss support zones…

5. Amazon: Still Riding the Tech Volatility Wave

- Amazon is navigating a dynamic tech landscape, leveraging its strong position in AI infrastructure and cloud services to drive long-term value creation and maintain a premium valuation in the market.

- The company is making strategic investments in AI chips and foundational AI companies like Anthropic, aiming to optimize efficiency and scalability in its AWS segment.

- Despite a current range-bound stock price, Amazon’s financial metrics and company culture approach underscore its commitment to growth and competitive advantage in the evolving tech ecosystem.

6. Cheap Vs. Rich Volatility: Diverging Signals Across Alibaba (9988 HK), Tencent (700 HK) & The HSI

- Context: Volatility cones provide a straightforward framework to evaluate whether options are trading cheap or rich. This Insight provides volatility analysis for 8 prominent Hong Kong stocks and the benchmark index.

- Highlights: In contrast, Alibaba’s IV remains rich, while Hang Seng Index IV is cheap across the curve, offering attractive hedge entry points.

- Why Read: Spot opportunities, assess regime shifts, and manage risk effectively — volatility cones turn complex data into actionable insights for traders and investors.

7. Monthly Macro Markets (October): Diverging Volatility Trends Highlight Risk Sensitivity

- October seasonals, despite their reputation, show most markets with better than 60% odds of finishing higher albeit with meager returns.

- Volatility trends have diverged, with implied vols climbing even as realized vols fell, raising questions about early signs of risk sensitivity.

- Implied vols on most markets have been trending higher vs the SP500 despite the US being ground zero for policy uncertainty.

8. Hong Kong Single Stock Options Weekly (Oct 06 – 10): Options Calm But Stormy Seas Ahead

- Hong Kong equities erased last week’s gains, with further losses on Monday likely after Trump’s social media post Friday morning.

- Weakness was not widespread, though there was a sharp reversal in breadth week over week.

- Option volumes and ratios suggest there’s little concern in the market at this point.

9. Tactical Alert: Undervalued Stocks Poised to Rally This Week

- China Mobile (941 HK) and Meta (META US) are both oversold according to our quantitative tactical models.

- We have been discussing China Mobile (941 HK) before, in early September, we said the pattern was bearish (“brief rally then down again”) , but now this has changed.

- Meta (META US) is a different story, looks like a bearish pattern but it is very oversold, it could rally 2 weeks before going lower.

10. From Banks to Miners: Cheap Vs. Rich Volatility Across Australia

- Context: Volatility cones provide a straightforward framework to evaluate whether options are trading cheap or rich. This Insight provides volatility analysis for ten prominent Australian stocks and the benchmark.

- Highlights: December implied volatility tends to be rich for the banks and cheap for the miners. S&P/ASX 200 (AS51 INDEX) implied volatility is cheap across the curve.

- Why Read: Spot opportunities, assess regime shifts, and manage risk effectively — volatility cones turn complex data into actionable insights for traders and investors.

Receive this weekly newsletter keeping 45k+ investors in the loop

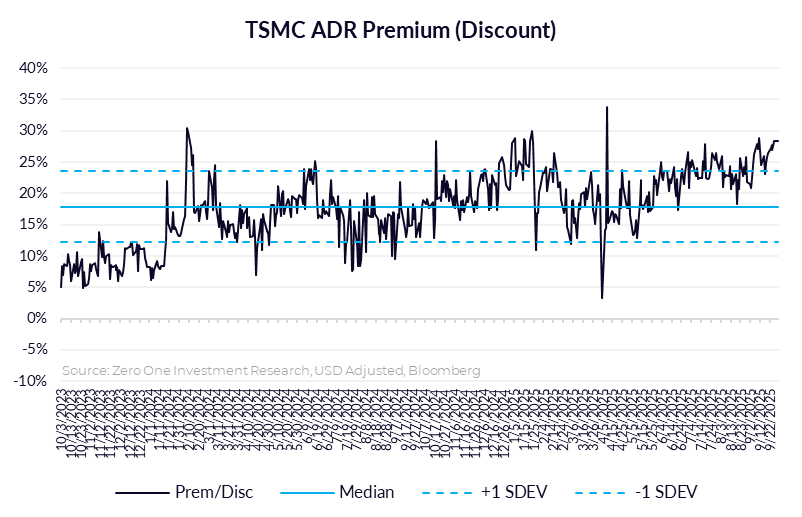

1. Taiwan Dual-Listings Monitor: TSMC & UMC Spreads Higher After Taiwan Market Holiday

- TSMC: +28.3 Premium; Historically Extreme Level, Can Short the ADR Premium

- UMC: +3.3% Premium; Historically Extreme Level, Short the ADR Premium

- CHT: -0.7% Discount; Near Lower Bound, Consider Going Long the Spread

2. TSMC: New Signals Underscore N2’s Rise as a Blockbuster Node

- Latest Signals Continue to Indicate N2 Is Emerging as TSMC’s Blockbuster Node

- N2 Commercialization Timing Aligns With Major AI HPC Platform Roadmaps

- TSMC Market Share Over 70%… Could N2 Drive This Number Even Higher? Maintain Our Structural Long Rating for TSMC

3. PC Monitor: Nvidia GB10 PCs Poised to Redefine the AI PC Category

- GB10 Brings Nvidia AI Performance From Data Center to the Desktop

- GB10 PCs Will Be “True” AI PCs, Their Capabilities Will Be More Evident

- From Niche to Market Driver; Maintain Structural Long for Mediatek, Asustek, Acer

4. TSMC (2330.TT; TSM.US): Is It Possible TSMC’ Output Reach a 50:50 Ratio Between the U.S. And Taiwan?

- The U.S. Secretary of Commerce, Howard Lutnick, has requested that Taiwan Semiconductor (TSMC) – ADR (TSM US)’s production output reach a 50:50 ratio between the U.S. and Taiwan.

- By contrast, TSMC’s fab construction also requires strong supplier coordination, and in the case of its U.S. fabs, there are numerous regulatory hurdles to overcome.

- Meanwhile, Semiconductor Manufacturing International Corp (SMIC) (981 HK)’s share price in Hong Kong has surged this year (+209.14%), significantly outperforming TSMC’s share price increase (+28.15%).

5. It’s Official, OpenAI Is Becoming A Multi-Trillion Dollar Hyperscaler

- Inference compute is going increase by a factor of one billion. It’s already gone up at least 2x in the past twelve months

- OpenAI will become the next multi-trillion dollar hyperscaler. NVIDIA is going to make sure this happens

- AI-Related revenues have already reached $1 trillion since all hypercaler revenues are now AI related according to Jensen. Problem solved!

6. Taiwan Tech Weekly: OpenAI to Consume Nearly Half of Global DRAM; Why TSMC 2nm Will Be A Blockbuster

- OpenAI, Samsung & SK Hynix Lock In Memory Pact — Taiwan Next Stop

- MediaTek’s Major ASIC Ambitions Face Delays from Some Key Clients

- TSMC: New Signals Underscore N2’s Rise as a Blockbuster Node

7. Intel (INTC.US): Seeking Investment from TSMC?

- NVIDIA Corp (NVDA US)’s investment is focused on joint AI development.

- Intel Corp (INTC US) may seek to invite Taiwan Semiconductor (TSMC) – ADR (TSM US) to join its investment initiative.

- Meanwhile, Intel Corp (INTC US)’s stock price has risen about 50.2% from its recent low.

8. Taiwan Dual-Listings Monitor: TSMC Premium Remains High Ahead of 3Q Results; CHT Rare ADR Discount

- TSMC: +26.8% Premium; Remains at Historical Extreme; Earnings Release Ahead

- ChipMOS: +1.3% Premium; Wait for Higher Level Before Shorting the Spread

- CHT: -1.0% Discount; Good Level to Go Long the ADR Spread

Receive this weekly newsletter keeping 45k+ investors in the loop

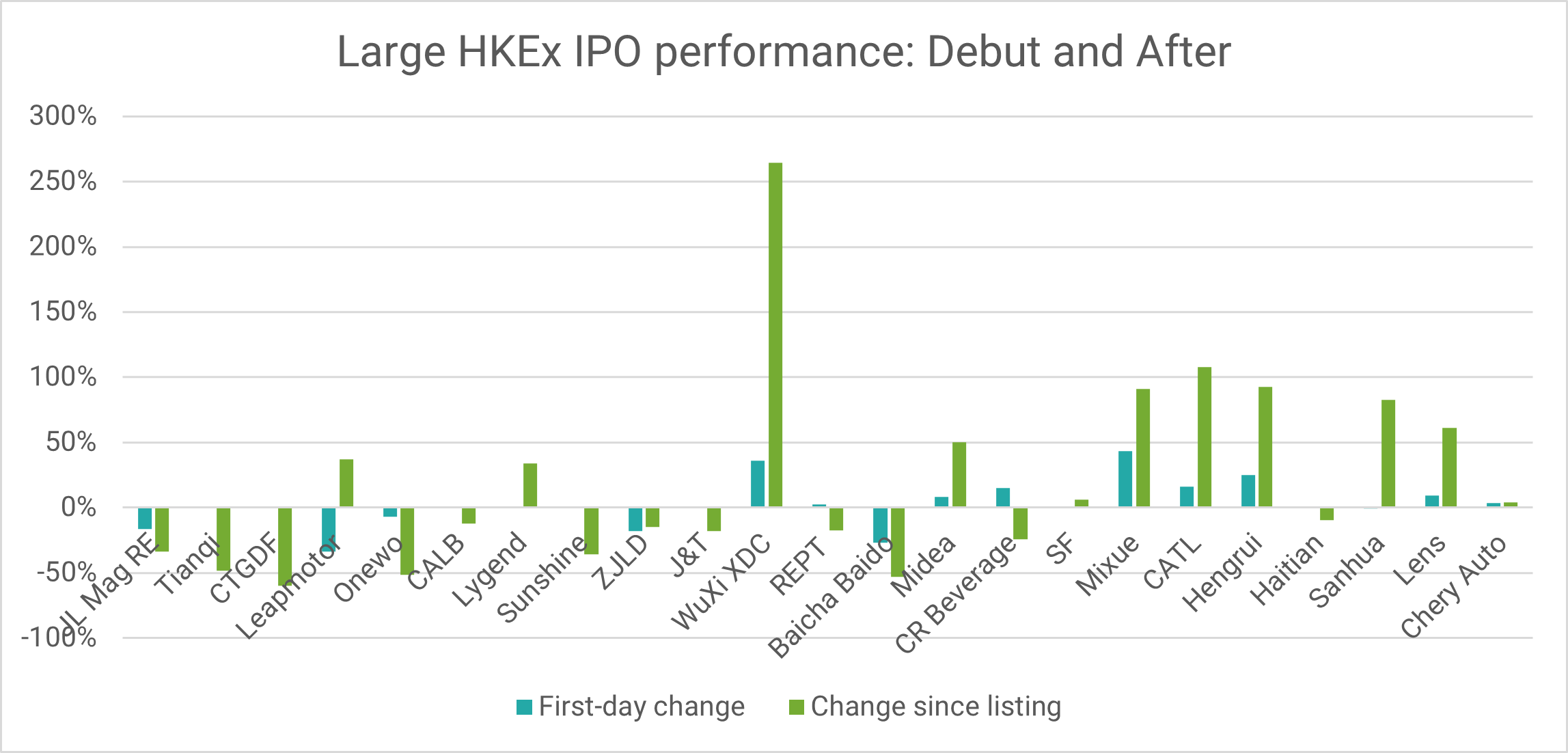

1. Zijin Gold IPO (2259 HK): Trading Debut

- Zijin Gold (2259 HK) priced its IPO at HK$71.59 per share to raise gross proceeds of approximately US$3.2 billion. The shares will begin trading on September 30.

- The IPO was discussed in Zijin Gold IPO: The Investment Case and Zijin Gold IPO (2259 HK): Valuation Insights.

- The market sentiment of the peers has increased since the IPO launch. My analysis suggests that the IPO price range is attractive.

2. Tekscend Photomask (429A JP) IPO: Valuation Insights

- Tekscend Photomask (429A JP) is a global leader in semiconductor photomasks. It is seeking to raise up to JPY123 billion (US$828 million). Pricing is on 30 September.

- I previously discussed the IPO in Tekscend Photomask (429A JP) IPO: The Bull Case and Tekscend Photomask (429A JP) IPO: The Bear Case.

- In this note, I present my forecasts and discuss valuation. My analysis suggests that Tekscend is attractively valued at the IPO price range compared to peer multiples.

3. Tekscend Photomask IPO – Thoughts on Valuation

- Tekscend Photomask (429A JP) (429A JP), a manufacturer and distributor of semiconductor photomasks, aims to raise around US$830m in its Japan IPO.

- TP is a global provider of photomasks and related support services. It has been the leader in the merchant photomask market in terms of sales since 2016.

- We have looked at the company’s past performance in our previous note. In this note, we talk about valuations.

4. LG Electronics’ BOD Gives the Green Light for LG Electronics India IPO in 2025 – Updated Valuation

- LG Electronics’ BOD finally approved a plan to sell a 15% stake in LG Electronics India in an IPO to be completed in 2025.

- According to local media, LG Electronics India is now valued at about US$13 billion which is higher than LG Electronics’ market cap of US$8.8 billion.

- Our base case valuation of LG Electronics India is implied market cap of 1,280 billion INR or US$14.4 billion.

5. [Japan ECM] MIGALO Holdings (5535 JP) Offering to Raise Capital, Generate Interest

- Migalo Holdings (5535 JP) is one of the rare TSE Prime-listed companies which got the boot from TOPIX, stayed in Prime, and is clawing its way back.

- As of end-March-25, it met all the criteria to stay in Prime and rejoin TOPIX. Now they are launching a primary offering, and this may presage an effort to rejoin.

- They are adding float and 10% of shares to the pile, in this ¥4.4-5.0bn offering. But instos are net short this stock.

6. ECM Weekly (29 September 2025)- Zijin, Chery, CAREIT, Orion, Butong, Victory Giant, Northern Star

- Aequitas Research’s weekly update on the IPOs, placements, lockup expiry and other ECM linked events that were covered by the team over the past week.

- On the IPO front, this week saw a few good listings across the region while the spotlight will be on Zijin Gold (2259 HK) in the coming week.

- On the placements front, it was a relatively quiter week, as compared to some of the more recent weekly flows.

7. Zijin Gold : Listing Pop Likely. Know Your Thresholds. Avoid Valuation Pitfalls.

- Riding on strong investor demand, Zijin Gold (2259 HK) has exercised its over-allotment option, boosting the total IPO size to USD 3.7 billion from USD 3.2 billion previously.

- As Hong Kong’s only pure-play gold miner with global exposure, Zijin Gold may command a premium, though any sharp price gains still depend on sustained gold price strength.

- Investors should define their medium- to-long-term gold price thresholds to shape a clear post-IPO strategy for Zijin Gold.

8. Tekscend Photomask IPO – Peer Comparison

- Tekscend Photomask (429A JP), a manufacturer and distributor of semiconductor photomasks, aims to raise around US$830m in its Japan IPO.

- TP is a global provider of photomasks and related support services. It has been the leader in the merchant photomask market in terms of sales since 2016.

- We have looked at the company’s past performance in our previous note. In this note, we will undertake a peer comparison.

9. Zijin Gold (2259 HK) IPO Debut – Some Points Worth the Attention

- Based on DCF model, valuation is about US$28.4 billion. We think this is the valuation bottom line. Conservative investors can take profits at this valuation level.

- Valuation has the potential to reach US$34-42bn (or 18-22x P/E ) if based on 2025 forecast.Optimistic investors can choose to wait for stock price to fall within this valuation range.

- Considering better profitability/shareholder resources, Zijin Gold has more advantage than Shandong Gold Mining. Therefore, market value of Zijin Gold will widen the gap with Shandong Gold Mining in the future.

10. Zijin Gold IPO Trading: Decent Retail but Strong Insti Demand

- Zijin Gold (2259 HK) raised around US$3.2bn in its Hong Kong IPO.

- It is a global leading gold mining company formed by combining all of the gold mines of Zijin Mining, located outside of China.

- We have covered various aspects of the deal in our previous note. In this note, we will talk about the demand and trading dynamics.

Receive this weekly newsletter keeping 45k+ investors in the loop

1. [Japan Event] Sony Financial (8729 JP) Overhang Hangs Over, Company Buys Back, ADR Selldown Awaits?

- Sony Financial Group (8729 JP) listed on Monday with a “Reference Price of ¥150. It opened at ¥205, quickly running to ¥210, then fell to ¥198 by lunch. Close? ¥173.8.

- That got a big ToSTNeT-3 buyback at ¥173.8. It traded lower on Day 2, closing at ¥164. Then lower still on Weds with another TN-3 buyback now ¥159.4.

- Neither buyback was full. SFGI has bought back 124mm shares. But the stock has fallen hard. ADRs/ADSs start trading Tuesday. That could see more selling.

2. Tekscend Photomask (429A JP) IPO: TPX Add in Nov; Global Index: One in Feb; One in June

- Tekscend Photomask (429A JP)‘s listing has been approved by the JPX and the stock is expected to start trading on the Prime Market from 16 October.

- At the top end of the IPO range at JPY 3000/share, Tekscend Photomask (429A JP) will be valued at JPY 298bn (US$2bn).

- The stock should be added to the TOPIX INDEX at the close on 27 November while inclusion in global indices should take place in February and June.

3. [Japan M&A] Mitsubishi Logisnext (7105) – This Deal Looks Mighty Bad

- JIP and MitHeavy have announced a takeunder to buy out MitHeavy sub Mitsubishi Logisnext Co., Ltd. (7105 JP) at a weighted average price 42% lower than Target Advisor DCF range midpoint.

- No/Minimal transparency. A sales process interrupted by Trump tariffs, leaving one low-ball bidder. And the sellers goes ahead with it BUT gets to reinvest on the back end. You don’t.

- The Board “supports” the Tender Offer, but leaves it to the opinion of the shareholders as to whether they tender. MitHeavy has 64.4% already so that basically gets done. But…

4. Mitsubishi Logisnext (7105 JP): JIP’s Takeunder Offer

- Mitsubishi Logisnext Co., Ltd. (7105 JP) announced a pre-conditional tender offer from Japan Industrial Partners (JIP) at JPY1,537 per share, representing a 15.3% discount to the last close price.

- The offer resulted from an auction process. The offer is light in comparison to peer multiples and is below the midpoint of the target IFA DCF valuation.

- While Mitsubishi Heavy Industries (7011 JP) irrevocable has a competing proposal clause, it is unlikely that a bidding war will transpire. The low required tendering rate suggests a done deal.

5. Merger Arb Mondays (29 Sep) – Soft99, Ashimori, Mandom, Paramount, OneConnect, Dongfeng, Spindex

- I summarise the latest spreads and newsflow of merger arb situations we cover across Hong Kong, Australia, New Zealand, Singapore, Japan, Indonesia, Malaysia, Philippines, Thailand and Chinese ADRs.

- Highest spreads: Mayne Pharma (MYX AU), Smart Share Global (EM US), ENN Energy (2688 HK), Dongfeng Motor (489 HK), Soft99 Corp (4464 JP), Joy City Property (207 HK).

- Lowest spreads: Bright Smart Securities (1428 HK), Pacific Industrial (7250 JP), Humm Group (HUM AU), Mandom Corp (4917 JP), Paramount Bed Holdings Co Lt (7817 JP).

6. Curator’s Cut: BABA Hedges, Substantive Spin-Offs & Japanese Activist Situations

- Welcome to Curator’s Cut, a fortnightly roundup of standout themes from the 1,000+ Insights published over the past two weeks on Smartkarma

- In this cut, we review strategies to hedge Alibaba (9988 HK) exposure, examine signficant Asian spin-offs, and explore engaging activist situations in Japan

- Want to dig deeper? Comment or message with the themes you’d like to see highlighted next

7. LG Electronics India IPO: Big Market Cap, Small Float -> Small Passive Flows

- LG Electronics India (123D IN) is looking to list on the exchanges by selling 101.8m shares at a valuation of US$8.7bn and raising around US$1.3bn in its IPO.

- The new valuation is around 24% lower than the rumoured valuation at the time of the DRHP filing last December.

- The stock will not get Fast Entry to global indices. Inclusion at regular rebalances will commence in June 2026 but flow will be small given the low float.

8. Jardine Matheson (JML SP): Additional Office Recycling Speculated

- The prior MO for the Jardines group was never sell your commercial buildings. This year marks a paradigm shift in that line of thinking.

- First Hongkong Land (HKL SP) sold nine floors of One Exchange Square to HKEX (388 HK). The first such sale since 1988.

- Now Mandarin Oriental (MAND SP) is negotiating the sale of “certain office space” at One Causeway Bay. Jardine Matheson (JM SP)‘s NAV discount and implied stub are at 12-month lows/highs.

9. Tata Capital IPO: Big Listing, Big Valuation, Small Float

- Tata Capital Limited (TATACAP IN) is looking to list on the exchanges by selling up to INR155bn (US$1.75bn) of stock at a valuation of around INR 1,384bn (US$15.6bn).

- The stock will not get Fast Entry to either of the global indices. The earliest inclusion in a global index should take place in June 2026.

- The stock should be added to the Large Cap segment in the AMFI Classification in January and to the Nifty Next 50 Index in March.

10. LG Chem: Announces a PRS Worth 2 Trillion Won Using Its Shares in LG Energy Solution as Base Asset

- LG Chem announced that it plans to complete a price return swap worth about 2 trillion won (US$1.4 billion) using its stake in LG Energy Solution as the base asset.

- This 2 trillion won PRS is likely to have a slightly positive impact on LG Chem and slightly negative impact on LG Energy Solution.

- Our NAV valuation of LG Chem suggests implied NAV per share of 369,187 won, which is 31% higher than current levels.

Receive this weekly newsletter keeping 45k+ investors in the loop

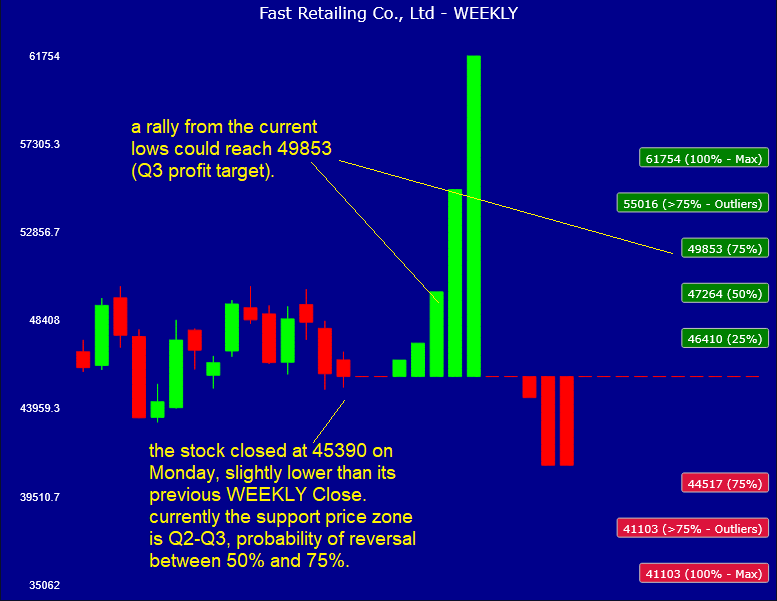

1. Fast Retailing (9983 JP) Tactical Outlook: Waiting for A Rally

- In our previous Fast Retailing (9983 JP) insight we identified a potential BUY opportunity ahead of the September 25 rebalance, but the rally failed to materialize.

- The stock at the moment is oversold, according to our quantitative model, so we would like to review its tactical outlook in this insight.

- Right now, the stock is the most oversold of all the Asian stocks we track, probability of WEEKLY reversal stands at 72%, after last week’s Close.

2. Asia/Pacific Stocks Outlook For the Week Sep 29-Oct 3

- Multi-Week forecasts for the Asian indices and stocks we track, based on our proprietary probability model.

- OVERBOUGHT: Samsung Electronics (005930 KS) , Softbank Group (9984 JP) , Toyota Motor (7203 JP) , Nikkei 225 (NKY INDEX)

- OVERSOLD: China Mobile (941 HK) , Fast Retailing (9983 JP)

3. BYD (1211 HK) Tactical Outlook: A Rally May Be Underway

- BYD (1211 HK) is currently in a position from where it could rally. Our previous insight suggested a possible bottoming area around 100.9 but the stock never reached that low.

- This week the stock rallied to 114.7, then pulled back. If the stock is temporarily bottoming, it could rally past 115 and up to 130 from here.

- According to our TIME MODEL the duration of the rally could be up to 3-4 weeks (2-3 more weeks up from here).

4. Hong Kong Single Stock Options (Sept 29 – Oct 03): Materials and IT Lead Amid Rising Option Activity

- HSI extended gains to fresh highs, supported by strong breadth, surging Materials and IT names, and rising single stock option activity

- Broad gains across all sectors highlighted strong momentum, with leadership from Materials and Information Technology.

- We examine the distribution of returns since the April lows finding that the tails are distinctly unbalanced.

5. A Rundown of the Last Month’s Futures and Options, Stock Options Views

- 3 global futures and options topics we covered included global equities, Brent, and Gold. We review the topics discussed and look forward to another interesting month of volatility trades.

- NK remains moderately interesting for NK vs MSCI World vol with the leadership change coming up, though deep downside swings would not be expected.

- Were bullish on AI stocks, and highlighted a few favorites with some tactical options trades to monetize existing equity longs or put on new hedged volatility positions.

6. Microsoft Corp: Balancing Cloud and AI Strength Against Cost and Execution Risk

- Microsoft’s cloud strength and AI leadership, particularly with Copilot, position it for growth, though its current valuation likely reflects these expectations, necessitating new market drivers.

- The company faces increasing pressure on efficiency metrics like gross margin and free cash flow due to significant, long-term AI infrastructure investments.

- We suggest a tactical approach to capitalize on anticipated stable price movements, leveraging current market conditions and implied volatility.

Receive this weekly newsletter keeping 45k+ investors in the loop

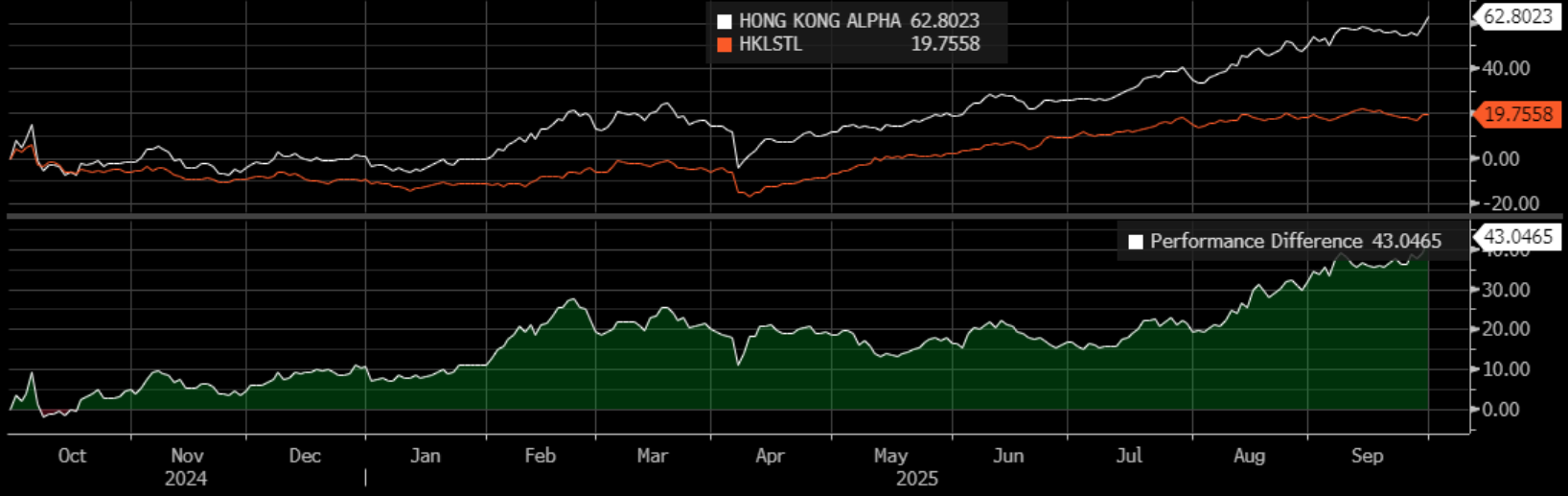

1. HONG KONG ALPHA PORTFOLIO: (September 2025)

- Hong Kong Alpha portfolio gained 8.45% in September and 60.89% and 62.80% YTD and since launch one year ago. The portfolio has outperformed Hong Kong indexes by more than 40%.

- The portfolio has a Sharpe ratio of 3.23 YTD and has generated more than 40% of its returns from stock-picking (alpha). Its beta is low at only 1.17.

- At the end of September, we increased exposure to AI and robotics and sold positions in the consumer and finance sectors.

2. UK: Lending Looks Stimulated

- Lending activity is sustaining beyond the levels prevailing before the stamp duty tax hike distortion. Only housing transaction volumes are down, but by less than before.

- New loan rates have fallen by 23bp since then, for a 110bp cumulative fall. New rates are close to the outstanding stock. Many borrowers are refinancing for similar deals.

- Past tightening has broadly passed through, but the strength in broad money growth signals that monetary conditions are settling at a slightly stimulative setting.

3. EA: Core Excess Revealed In Sep-25

- Inflation’s break above target to 2.23%, within 1bp of our forecast, came as past energy price falls dropped out to reveal the more resilient underlying pressures.

- Small upside surprises in large countries, like Germany and Italy, were balanced in number and contribution by larger surprises in small ones, like Greece and Estonia.

- We expect less negative payback in October and January, preventing our profile from languishing below the target through 2026, like the consensus view does.

4. UK: Government Leads Imbalances

- Household saving and inflation have eroded their debt burden while corporates remain prudent. A lack of imbalances to correct starves the UK of fuel for a recession fire.

- Persistent fiscal and current account deficits highlight where the UK’s primary risk lies. If the market regime focuses on fiscal issues, the corrective pressures could be fierce.

- We don’t expect that correction to occur, but the Chancellor should tread carefully, while doves need not worry about a recession arising from healthier other UK sectors.

5. Australian Equities: Where are we now, and what’s next?

- Australian economy remains sluggish, but some positives include recovery in small caps and resilience of Australian consumers

- Market volatility and narrow leadership driving unhappiness among active investors

- Resilience of Aussie consumer and strong retail results stood out in recent reporting season, with small caps and US housing exposure also notable themes

This content is sourced through publicly available sources and has been machine generated. Information displayed is for general informational purposes only.

6. HEW: Watching What Didn’t Happen

- The US government shutdown removes the potential for official statistics to damp dovish concern, raising the likelihood of October’s cut, especially with other weak data.

- EA unemployment’s rise reflected rounding rather than substance. UK national accounts revealed healthy balance sheets, aside from the government, and bullish lending stats.

- Next week’s calendar stays thin with US releases suspended and Europe’s cycle focusing on the following week. The RBNZ, BoT, BSP and Peru announce rates next week.

7. Gold Mania, Niobium Dreams, and Antimony Nightmares (Datt)

- US monetary policy is accommodative and markets are buoyant, especially in commodities

- Investors need to be cautious about being overly bullish in current environment

- Similarities seen with 2006-2007 period, particularly in disruptions in copper supply and new technologies in metal recovery; investors should be wary of hype and potential risks involved

This content is sourced through publicly available sources and has been machine generated. Information displayed is for general informational purposes only.

8. Get Ready to Buy the Dip, But Not Yet

- We remain intermediate-term bullish on stocks, but the market is at risk of a correction.

- If last week’s weakness is the start of a pullback, short-term trading indicators point to further downside potential.

- Investors should be prepared to buy the dip, but not yet.

9. Indian Market: WANT TO BUY THE DIP, THINK AGAIN !!

- India’s markets continue to underperform Asia since our insight last November recommending investors to “Fade the Market”.

- Foreign investors continue to exit the market this year with the largest net outflow since COVID.

- The Trump administration is pressuring India in trade negotiations with reciprocal tariffs (25%), additional tariffs for importing Russian oil (25%), pharma tariffs (100%), and new restrictions on H-1B visas.

10. EA: Rounding Jobs For Migrants

- A surprise rise in EA unemployment reflects rounding rather than alarming weakness, with labour supply and demand still surging. Finland’s woes are more idiosyncratic.

- Supply has trended much faster post-pandemic, sustaining demand at its old trend without extreme capacity constraints. Migration has more than accounted for the rise.

- Ukrainians are dominating the flow and complicating the read through to disinflationary spare capacity. Wage growth is an even more critical signal when supply is uncertain.

Entity | Insights | Analytics | News | Discussion | Filings | Reports |